IBM Ch Past CH2

1/120

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

121 Terms

Ratio Analysis

Quantitative managmeent tool comparing financial figures to judge a firm’s financial performance

What Does Ratio Analysis Require

Applying figures of the final accounts: balance sheet and profit + loss account

How to assess if financial performance improved

Comparing current figures with historical figures and/or comparing to rival businesses

Purposes of ratio analysis

Examine a financial position

Assess financial performance

Compare real figures against projected/budgeted figures

Aid decision making

Historical Comparisons

Comparing the same ratio of two different time periods, showing trends and financial performance over time

Inter-Firm Comparisons

Comparing the same ratios of different businesses in the same industry, showing their relative financial performance

When financial ratios are used

Only with rivals in of similar size in the same industry

Types Of Profability Ratios

Gross profit margin

Profit margin

Return on capital employed (ROCE)

Profability Ratios

Profit in relation to other figures i.e. revenue, sales, equity

Profit

Financial surplus earnings of a firm after costs have been deducted

Limtation of profitability ratios

Only applies to profit-orientated businesses

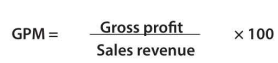

Gross Profit Margin

Firm’s gross profit as a percentage of its revenue

ways to raise sales revenue (PM & GPM)

↓ selling price of products (w/ many substitutes)

↑ selling price of products (w/ few substitutes or loyal customers)

↑ marketing strategies

Alternative revenue streams

ways to reduce direct costs (PM & GPM)

↓ direct material costs; cheaper suppliers/materials

May ↓ brand rep

↓ direct labour costs; ↓ staff, flexitime

Net Profit Margin

Percentage of sales turnover turned into profit

Sales Turnover (Revenue)

Total sales over a given period (financial year)

PM vs GPM

Profit margin covers both cost of sales (direct cost) and expenses (indirect cost) while GPM does not = better measurement of profitability

ways to reduce costs (PM)

Preferential payment terms with trade creditors and suppliers

Negotiate cheaper rent

Reduce indirect costs

Gross Profit Calculation

GP = Net Sales (Revenue) - Cost of Goods Sold (COGS)

how to think about the profitability ratios

For 50% GPM, every $100 in revenue, $50 goes to COGS and $50 is company profit

For 40% PM, every $100 in revenue, the company keeps $40 after paying all expenses

For 30% ROCE, every $100 invested, the company generates $30 of profit back

For 2.5 CR, the company has $2.5 of current assets for every $1 of current liabilities

Return on capital employed (ROCE) (Key Ratio)

Financial performance of a firm based on capital invested

Capital emloyed

CE = Owners’ equity (Net worth) + noncurrent liabilities

Owner’s equity Formula

OE = Total assets - total liabilities

ROCE General Rule

Should be ↑ than interest rate of commercial banks because if not, just deposit it at the bank.

Hence, ROCE needs to be high for investors to choose the company over banks

Which profit is ROCE used for

Net Profit before tax and interest for better historical comparisons

Liquidity Ratios

Firm’s ability to pay its short term liabilities from its current assets

Why Liquidity Ratios Are Sought After

Helps creditors and financial lenders know if they’re getting their money back

Helps shareholders and potential investors know if the firm can pay its debts

Liquid Assets

Assets that can be turned into cash quickly, without losing value

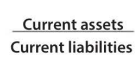

Current Ratio (CR)

Firm’s ability to cover shorrt terms debts in the next 12 months of the balance sheet

Where Current Ratio Should Be Generally & Why

1.5-2.0 because some current assets may be unable to be sold without losing value & shows that there is sufficienct working capital

<1.0: that short term debts > liquid assets

>2.0: business may have too much cash (better spent on trade) or too many debtors (more likely for bad debts or customers defaulting) or too much stock (↑ stock and insurance costs)

Exceptions include Supermarkets w/ 2.1 CR because they need all the stock or biotechnology who has >3.0 due to lengthiness of developing drugs

Working Capital

WC = current asset - current liabilities

Significance of WC

Positive WC = potential to invest and grow

Negative WC = possible problems paying creditors and suppliers or lead to bankruptcy

How to improve CR

Raising value of current assets and reducing value of current liabilities

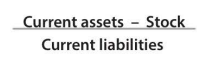

Acid Test Ratio (Quick Ratio)

Current ratio but without the value of stocks

Why ATR Is Used Over CR

When stocks are hard to convert quickly i.e. semi finished goods or highly expensive stock

Where ATR Should Be Generally

1:1 otherwsie working capital difficulties or liquidity crisis

>1 means that firm is keeping too much cash

Liquidity Crisis

Firm is unable to pay its short term debts

Which Liquidity Ratios are wanted by which stakeholders

All use both to know a company will not be able to pay them back

All use both to track liquidity which helps in predicting financial stability

All use both to compare against industry averages

Trade Creditors & Short term Debtors use ATR because stock may be hard to turn to cash quickly

Investors & Shareholdrrs use CR for management efficiency (firm is investing enough cash or not)

Long Term Debtors look at current ratio to assess WC management

How to iprove ATR

↑ amount/price of current assets

↓ amount of current liabilities

Sell fixed assets and lease back to turn into cash

Debt (invoice) factoring - selling all invoices to a 3rd party

Uses Of FInancial Ratios

Employees & trade unions to assess chances of pay rises & job security

Managers & directors to assses chances of management bonsues or identify areas of improvement

Trade creditors to see if debts can be paid back

Shareholders to compare firm’s ROI vs other investments

Financies to see if loans can be paid back

Local community for potential job opportunities or securing spnosohip deals to local projects

Limitations of Financial Ratio Analysis

Do not indicate current or future financial situation

Changes externally not affecting internal workings can still change financial ratios

No universal standard to reporting final ccounts

Qualitative factors ignored

Differing organisatioal objectives between businesses

How to improve ROCE

Pay off long term debt - reduces Capital Employed = ↑%

Net Profit

Net Revenue - all expenses

Investment

Purchase an asset with potential for future financial benefits

Investment appraisal

Quantitative techniques that calculate financial costs and benefits of an investment decision

2 main methods of investment appraisal

Payback period, average rate of return, net present value (HL)

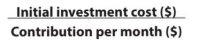

Payback Period

# of time for an investment project to earn enough to repay initial investment cost

Payback period formula

How to calculate PBP with variable contribution

Use cumulative cash flow method

Advantages of using PBP

Simplest and quickest out of all three

Useful for firms with liquidty problems

Lets firms see if an asset can break even before being replaced

Allows different investments projects with different costs

Helps managers assess projects that’ll yield quick returns

Disadvantages of using PBP

Contribution/month is unlikely to be constant

Focused on time and not profits

Encourages short term approach to investing

Not siutable for businesses like property developers who are unlikely to receive pay back for a long time

Prone to errors

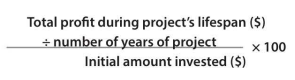

Average rate of return ARR

Average profit of an investment project as a % of # invested

ARR formula

Main function of ARR

Helps managers compare return on diffferent investment projects

Real return of ARR + example

ARR is compared against base interest reate in the economy

Mcdonald’s project is 7% and savings interest rate is 3%, real rate of return is 4%

Advantage of ARR

Easy comparisons of estimated returns on different investment projects

Disadvantages of ARR

Inogres net cash flows

Prone to forecasting errors if considering seasonal factors

Needs a project’s useful life span before calculating

Need of many time based forecasts = ↑ errors bc of ↑ time prediciting

Qualitative investment appraisal methods

PORSCHE

Projections - intuition

Objectives

Risk profile - risk-adverse business or not

State of the economy

Corporate image

Human relations - how it affects staff

External shocks - external influences

Cumulative net cash flow

Sum of investment project’s net cash flow for a year + net cash flow of all previous years

Reminders about quantitative investments

Quality & Reliability of data

Changes in interest rates: affects potential gains of a project

Does not capture all relevant costs and benefits

Capital expenditure

Finance spent on fixed assets

Resons for capital expenditure

Add extra production capacity

Improve efficiency by using better technologies

Replace worn out or obsolete capital equipment and machinery

Comply with changing legislation and regulations

Chllenges of capital expenditure

High cost

Limited sources of finance

Feasability of some investments

Revenue expenditure

Finance spent on daily operations and payment of indirect costs

Collateral

Financial guarantee for securing external loan capital to invest for business growth

Fixed assets

Items of monetary value that have long term function for businesses

Sources of finance

Where or how businesses obtain funds

Internal sources of finance

Money or funds coming from within the business

Types of internal sources of finance

Personal funds (for sole traders)

Retained profit

Sale of assets

Personal funds

Entrepreneur’s own savings

Retained Profit

Profits that a businesss keeps after paying taxes or dividends

Sale of assets

Businesses selling their dormant (unused) assets

Main uses for internal source of finance

Personal funds: Main source of finance for sole traders

Retained profit: Capital expenditure

Sale of assets: If businesses relocate or fight liquidity issues

External sources of finance

Money or funds coming from outside businesses

Types of external sources of finance

Share capital

Loan capital

overdrafts

trade credit

crowdfunding

leasing

microfinance providers

business angels

Share Capital

Money raised from selling shares in a LLC

Share issue (share placement)

exisintg publicly held companies raising finance by selling more shares

Loan capital

med-long sources of finance obtained from commercial lenders

mortgages

secured loans for the purchase of proeprty (land or buildings)

business development loans

highly flexible loans to meet needs of the borrower to develop an aspect of the business

Debentures

Long term loans where holders receive paymentrs regardless of a business’ loss/profit before shareholders are paid dividends

Purpose of debentures

Allows postopnes payments to ease firm’s cash flow problems

Debentures ownership in companies

Debenture holders do not have ownership or voting rights.

Overdrafts

Financial service to allow a business to take more money than available in the account

Whne overdrafts are suitable

When firms need large cash outflow orwhen products are sold on trade credit and are awaiting customer payment

Disadvantage of overdrafts

Overdrafts are repayable on demand (demand immediate payment) by the lender

Trade credit

Allows a firm to postpone payments from the date of the purchase.

Usually allows 30-60 days to pay

Helps ease cash flow problems

Crowdfunding

Raising finance from a large number of indvidusals to finance a new business venture or project

Heavily regulated to protect donors and prevent fraudulent business activites

Start ups often use crowdfunding but often results in loss of ownership and conotrol

Leasing

Cont4ract between lessor and lessee that allows lessee to hire assets by paying rental income to the lessor (leagl owner)

Suitable for owners without enough capitals

Dis/advantages of Leasing

+: Increases cash for other purposes

+: Responsibility of repairs + maintenance is on the lessor

+: Can be classed as business expense to reduce tax bill

-: More expensive that buying in the longterm

Sale and leaseback

Selling a fixed asset (to raise finance) and immediately leasing the property back

Hire Purchase (HP)

Firms pay creditors in instalments (12-24 months) and prpoerty is legally owned by the creditor until all payments are paid.

Generally requires a down payment

Lender can repossess asset if buyer defaults

Microfinance providers

Enables disadvantaged members to gain access to financial services for the purpose of eradicating poverty

Business angels

Wealthy individuals who invest money in businesses

Dis/advantages of business angels

+: Finances firms who are unable to secure finance from banks, shareholders or other investors

+: Business angels’ experience and financial backing massively helps the business

-:Likely to take proactive role in the business venture and will take control from teh owner

-Might have to buy out the bsuiness angel if they wish for control and ownership

Dis/advantages of microfinance providers

+Gives access to people who otherwise cannot get finance

+Creates new job opportunities

+Buyers are less likely to pull children out of schoool and receive better access to healthcare services

-Unethical due to profiting from the poor and unemployed

-Limited finance due to risk of defaulting

-Not all poor ppl qualify due to business seeking profit

Business Angels’ criteria for investing

Return on investment; needs high return due to unprofitable nature of startups

Business plan: the purpose or goals of the businesss venture that help with the business’ direction and identity. ↑ Creatvity = ↑ growth potential

People: People that are part o of the business

Track record: history of the business and its management i.e. earning history and track record of payament

Short term sources of finance

Sources available for <12 months (or fiscal year) to pay for daily/routine business operations

Long term sources of finance

Sources availalble for >12 months (or fiscal year) for purchasing fixed assets or financing expansion

Factors related to choosing financial sources

SPACED

Size and status of firm: ↑ size = ↑ ease of raising finance

Purpose of finance: different sources are more suitable for different needs

Amount required:

Cost of finance: purchase cost of assets and associated costs, ↑ costs ≈ need LTSOF

External factors: Interest rate & stock market volatillity affect confidence levels

Duration: Long term capital expenditure = LTSOF etc