ACC 211 - Exam 2

1/72

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

73 Terms

Balance Sheet Elements

Assets, liabilities, equity

Assets

Things a business owns or controls

provide value or benefits in the future

Liabilities

amount a business owes

obligation to pay money or provide services

Equity

owner’s share of business

after all debts are paid

Asset Categories (6)

current assets

long-term investments

PPE

Right-of-use assets

intangible assets

other assets

Liabilities & Owner’s Equity Categories (3)

current liabilities

long-term debt

owners equity

Current Assets

Cash or assets converted into cash, sold, or consumed in one year or in the operating cycle

whichever is longer

Cash & cash equivalents

any money available on demand

Cash equivalents - short-term, highly liquid, mature within three months or less

Restrictions or commitments must be disclosed

Basis of Valuation: fair value

Short-term investments (equity securities)

BoV: fair value

changes reported in net income unless:

Accounted for under equity

Can’t determine fair value

Short-term investments (debt securities)

Three classifications:

Held-to-maturity: positive intent and ability to hold to maturity

Trading: Bought and held to sell in the near term to generate income

Available-for-sale: Not classified as either

Receivables

Shown in the balance sheet or notes

Clearly identify:

• Anticipated loss due to uncollectibles

• Amount and nature of nontrade receivables

• Receivables used as collateral

Basis of Valuation: Estimated amount collectable

Inventories

Disclose

Cost flow assumption (e.g., FIFO or LIFO)

Basis of Valuation: Lower-of-cost-or-net realizable value/market

Prepaid expenses

Payment of cash

Cash Payment Before Expense Recorded

Basis of Valuation: cost

PPE is measured based on _____

historical cost

Non-current Assets (long-term investments) (4)

securities

tangible fixed assets

special funds

nonconsolidated subsidiaries or affiliated programs

Long-term investments

• Debt investments —> available-for-sale & fair value

• Held-to-maturity debt investments—> amortized cost

• Equity investments—> fair value or equity method

Noncurrent Assets (PPE)

long-lived assets used in the regular operations of the business

Physical property

depreciates or depletes (land as an exception)

Noncurrent Assets (Intangible Assets)

lack physical structure and are not financial instruments

limited life intangibles amortized

indefinite life-intangibles tested for impairment

Noncurrent Assets (other)

long-term prepaid expenses

• Prepaid pension cost

• Noncurrent receivables

• Assets in special funds

• Deferred income taxes

• Property held for sale

• Restricted cash or securities

Current Liabilities

short term debt a company expects to pay off soon by using current assets

Payables resulting from the acquisition of goods

and services

2. Collections received in advance

3. Other liabilities

Long-term Liabilities

debt a company doesn’t expect to pay off within the normal operating cycle

Long-term Liabilities Types

financing situations: issuance of bonds, long-term lease obligations, and long-term notes payable

Ordinary operations: pension obligations and deferred income tax liabilities.

Occurrence or non-occurrence future events: service or product warranties and other contingencies.

Elements of Owners Equity

capital stock

additional paid in capital

retained earnings

accumulated other comprehensive income

treasury stock

Most common form of the balance sheet

report form

lists the balance sheet sections above one another

Classified report form b/s (assets)

Assets

current assets

Long term investments

Equity Investments

PPE

Total PPE

Intangible Assets

total assets

Classified report form b/s (Liabilities & stockholder equity)

Liabilities & Stockholder’s equity

Current liabilities

Long-term debt

Total liabilities

Stockholders equity

Total stockholders equity

Total libabilities & stockholders equity

Statement of Cash Flows purpose

provide relevant information about the cash receipts and cash payments of an enterprise during a period

Operating activity in the statment of cash flow

cash effects of transitions that determine net income

Investing activity in the statment of cash flow

making and collecting loans and acquiring and disposing of investments and property, plant, and equipment

Financing activity in the statment of cash flow

Involves liability and owner’s equity

Statement of Cash Flows format

cash flows from operating

cash flows from investing

cash flows from financing

net increase (decrease) in cash

cash at beginning of year

cash at end of year

Inflows: Operating

when cash revenue excedes expenses

Inflows: Investing

sale of PPE

Sale of debt or equity securities of other entities

Collection of loans to other entities

Inflows: Financing

issuance of capital stock

issuance of debt (bonds & notes)

Outflows: Operating

when expenses exceed revenues

Outflow: Investing

puchase of PPE

purchase of debt & equity securities of other entities

loans to other entities

Outflow: Financing

payment of dividends

redemption of dividends

reacquisition of captial stock

Significant Noncash Activties

financing and investing activities that don’t affect cash

reported at the bottom of the statement of cash flows or in notes

Types of Ratios

liquidity

activity

profitability

coverage

Liquidity Ratio

Measure of the company’s short term ability to pay its maturing obligations

Activity Ratio

Measures how effectively the company uses its assets

Profitability Ratios

Measures of the degree of success or failure of a given company or division for a given period of time

Coverage Ratios

Measures of the degree of protection for long-term creditors and investors

Current Ratio

current assets / current liabilities

measures short term debt paying ability

Quick (acid-test) ratio

Cash - short-term investments + accounts recievable (net) / current liabilities

measures immediate short-term liquidity

Current cash debt coverage Ratio

Net cash provided by operating activities / average current liabilities

measures a company’s ability to pay off its current liabilities in a given year from its operations

Accounts Receivable turnover Ratio

Net sales / average net accounts receivable

measures liquidity of receivables

Inventory Turnover ratio

Cost of goods sold / average inventory

measures liquidity of inventory

Asset Turnover Ratio

net sales / average total assets

measures how efficiently assets are used to generate sales

Profit margin on sales ratio

net income / net sales

measures net income generated by each dollar of sales

Return on assets ratio

net income / average total sales

measures overall profitability of assets

Return on common stockholder’s equity ratio

Net income - preferred divdends / average common stockholders equity

measures profitability of owners investment

Earnings per share ratio

net income - preferred dividends / weighted average common shares outstanding

measures net income earned on each share of common stock

Price earnings ratio

market price per share / earnings per share

measures the ratio of the market price per share to earnings

Payout Ratio

cash dividends / net income

measures percentage of earnings distributed in the form of per-share cash dividends

Debt to assets ratio

total liabilities / total assets

measures the percentage of total assets provided by creditors

Times interest earned ratio

net income + internet expense + income tax expense / interest expense

measures ability to meet interest payments as they come due

Cash debt coverage ratio

net cash provided by operating activities / average total liabilities

measures a company’s ability to repay its total liabilities in a given year from its operations

Book value per share ratio

common stockholder’s equity / outstanding shares

measures the amount each share would recieve if the company were liquidated at the amounts reported on the balance sheet

Free cash flow ratio

net cash provided by operating expenses - capital expenditure - cash dividends

measures the amount of discretionary cash flow

Future value of a $

value of amount invested at a future date

assuming compound interest

FV = PV (FVFni)

FV= future value

PV = present value

FVFni = future value factor for n periods at i interest

Present value of a $

value now of an amount to be paid or recieved in the future

assuming compound interest

PV = FV (PVFni)

PV = present value

FV = future value

PVFni = present value factor for n periods at i interest

Annuities require…

periodic payments or receipts (called rents) of the same amount

same length interval between such rents

compounding of interest once each interval

Ordinary Annuity

rents occur at the end of each period

no interest during the 1st month

Annuity Due

rents occur at the beginning of each period

Interest will accumulate during 1st period

one more interest period thean ordinary annuity

Future value of an ordinary annuity

R (FVF - OAni)

FVF - OAni = ((1+i)^n -1) / i

R = periodic rent

FVF-OAni = future value factor of an ordinary annuity

i = rate of interest per period

n = number of compounding periods

Future value of an annuity due

multiply future value of ordinary annuity factor by 1 + interest rate

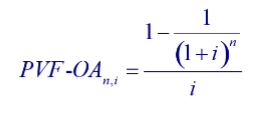

Present Value of ordinary annuity

R= periodic rent

PVF-OAni = present value of an ordinary annuity of 1 for n periods at i interest

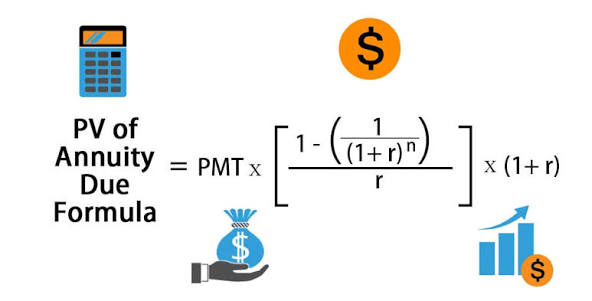

Present Value of Annuity Due

Deferred Annuity

Rents begin after a specified number of periods

Future Value of a Deferred Annuity

Calculation same as future value of an annuity not deferred

Present Value of a Deferred Annuity

Must recognize interest that accrues during deferral period

Valuation of long term bonds

Two Cash Flows:

• Periodic interest payments (annuity)

• Principal paid at maturity (single-sum)