Insurance part 16

1/82

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

83 Terms

Business Overhead Expense

LO1: Purpose and importance of disability income insurance

Key Concepts:

Disability income insurance protects against loss of income when covered perils make it impossible to work

Often called "living death insurance" because the financial impact can be worse than death

Provides a specified income benefit for a defined period of time

Transfers potentially catastrophic financial risk to the insurer for predictable premium payments

Important Terms:

Accidental bodily injury: Unintended consequence of an action the insured takes

Morbidity: Measures the risk of becoming disabled based on personal and occupational factors

Covered perils: Accidents and illnesses that cause disability

LO2: differentiate between various definitinos of disability used in insurance policies

Total Disability Definitions:

Own occupation: Cannot perform material and substantial duties of insured's own occupation

Any occupation: Cannot perform duties of own occupation or any occupation for which reasonably suited by education, training, or experience

Substantial gainful activity (SGA): Social Security definition requiring the inability to engage in any substantial gainful work

Other Disability Definitions:

Partial disability: Inability to perform one or more key duties or inability to work full-time

Residual disability: Working less than full-time with income loss of at least 20%

Presumptive disability: Specific severe conditions like loss of limbs, sight, hearing, or speech

Concurrent disability: Multiple events causing the same disability period

Delayed disability: Total disability developing after an accident

Confined disability: Requires the insured to remain indoors

LO3: Identify how individuals qulaify for disability benefits under different policy types

Qualifying Requirements:

Must be under a physician's care

Must meet the policy's definition of disability

Must satisfy the elimination (waiting) period

Must have loss of income (presumed or actual)

Recurrent Disability:

Relapse within six months is considered a continuation of initial disability

No new elimination period needed

No new benefit period begins

Relapse after six months is treated as a new claim

At-Work Benefits:

Partial disability: 50% of the total disability benefit

Residual disability: Percentage of total disability benefit based on income loss

LO4: Compare government disability programs with private disability insurance options

Government Programs:

Social Security Disability Insurance (SSDI):

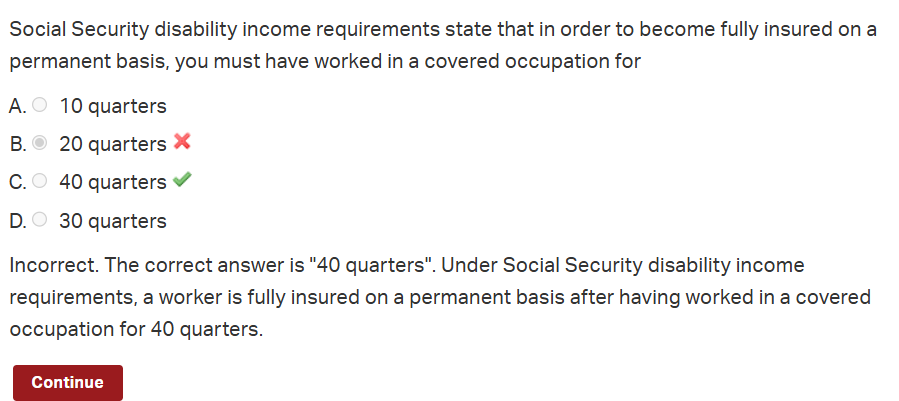

Requires sufficient FICA tax payments (40 quarters for permanent status)

Uses the substantial gainful activity definition

Has a five-month waiting period

Benefit equals 100% of primary insurance amount (PIA)

Workers' Compensation:

Covers work-related accidents or occupational diseases

Provides medical, disability, and survivor benefits

Classifies disabilities as temporary or permanent

Primary coverage for work-related disability

Private Insurance Advantages:

More flexible definitions of disability

Shorter elimination periods

Higher benefit amounts

Customizable with riders

Coverage for both occupational and non-occupational disabilities

LO5: Distinguish between individual and group disability income insurance features

Individual Disability Insurance:

Occupational contract providing 24/7 coverage

Uses a flat amount approach for benefits

Typically limits coverage to 60% of gross income or 80% of net income

Features a probationary period at policy inception

Offers non-cancelable or guaranteed renewable options

Underwritten based on occupation and personal characteristics

Group Disability Insurance:

Often non-occupational coverage

Uses percentage-of-earnings approach

Coordinates benefits with other sources

No probationary period once coverage begins

Requires minimum participation to avoid adverse selection

Premiums based on the group's aggregate risk level

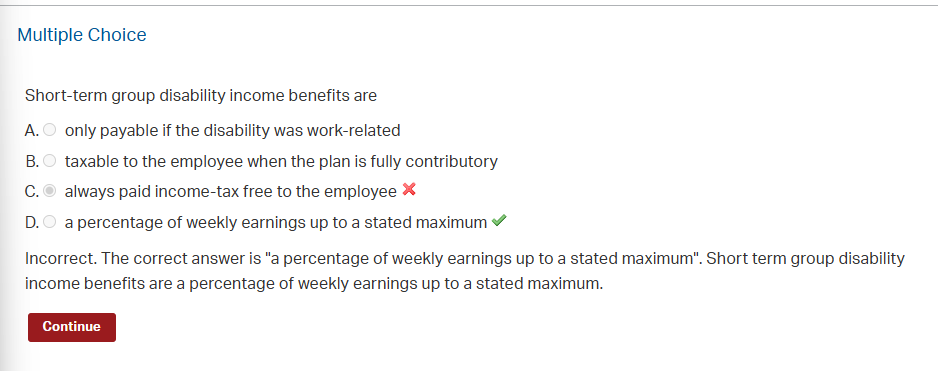

Short-Term vs. Long-Term Disability:

Short-term disability:

Weekly benefit payments

Minimal waiting periods

Maximum benefit period of two years

Often pays benefits for up to 180 days

Long-term disability:

Monthly benefit payments

Longer elimination periods

Benefit periods range from two years to age 65

Addresses more serious injuries or illnesses

LO6: analyze business applications of disability insurance

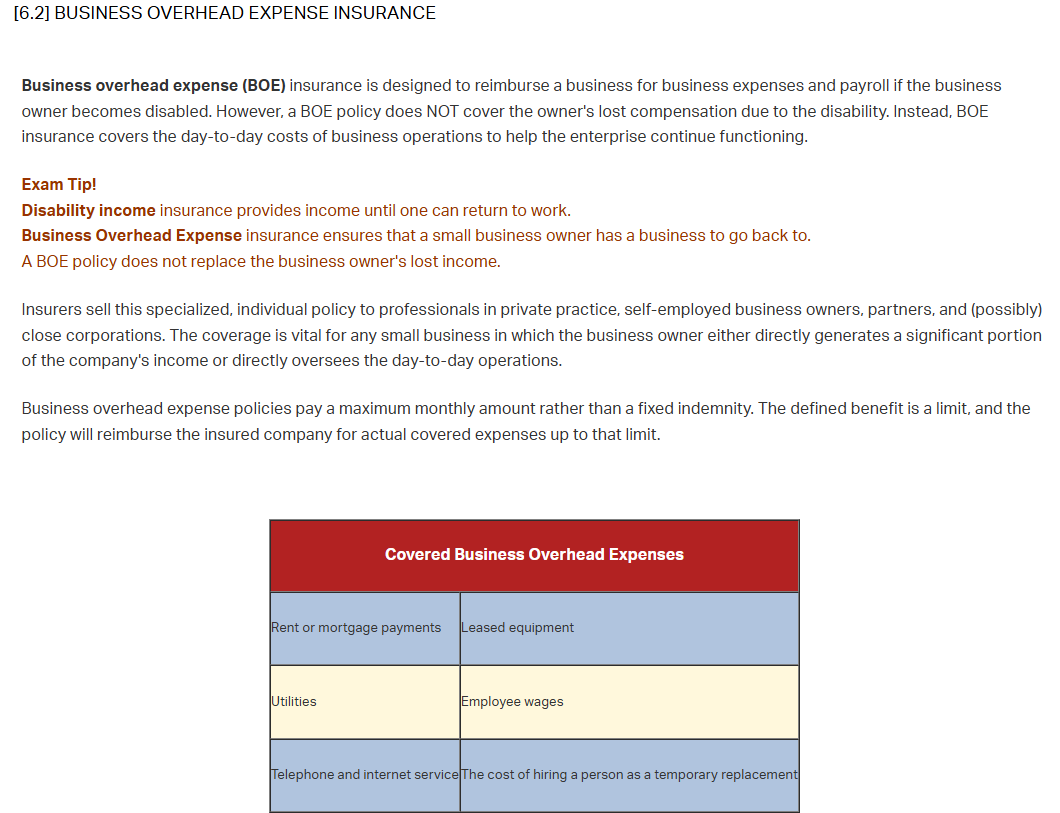

Business Overhead Expense (BOE) Insurance:

Reimburses business expenses if the owner becomes disabled

Does NOT cover the owner's lost compensation

Covers rent, utilities, employee wages, and equipment leases

Pays the actual expenses up to the maximum monthly amount

Vital for small businesses where the owner generates significant income

Disability Buy-Out Policies:

Fund disability buy-sell agreements

Allow remaining owners to buy the disabled partner's share

Available as cross-purchase or entity plans

Often have lengthy elimination periods (up to two years)

May offer lump-sum or periodic payment options

Key Person Disability Insurance:

Indemnifies the business for the loss of services of an essential person

Covers expenses for additional help or outside services

Benefit based on the key person's economic value to the business

Typically has a 30-90 day elimination period

The benefit period is usually one to two years

LO7: How disability insurance benefits are taxed based on premium payment sources

Taxation Principle:

IRS generally taxes money only once (either premiums or benefits)

Individual Disability Insurance:

Premiums are not tax-deductible (paid with after-tax dollars)

Benefits not taxable (premiums already taxed)

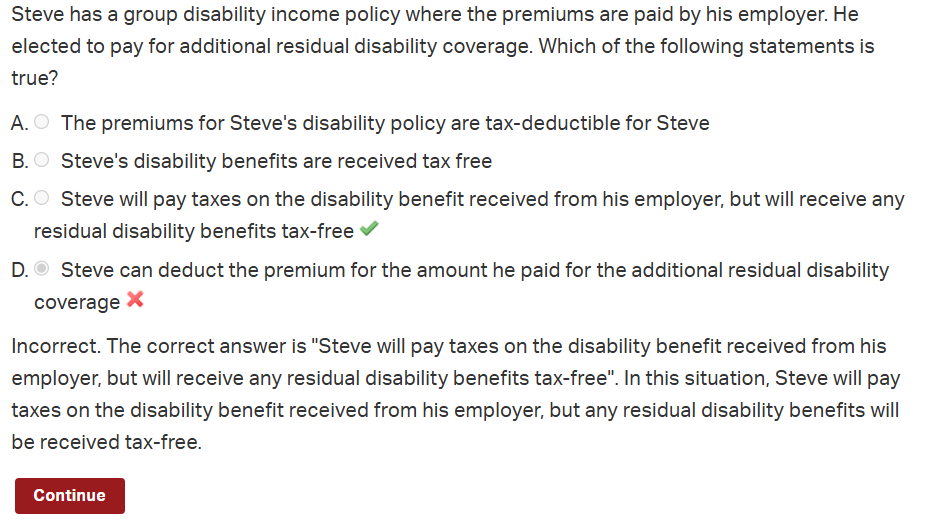

Group Disability Insurance:

Employer-paid premiums:

Tax-deductible business expense for the employer

Benefits are fully taxable to the employee

Employee-paid premiums:

Pre-tax contributions: Benefits are fully taxable

After-tax contributions: Benefits are tax-free

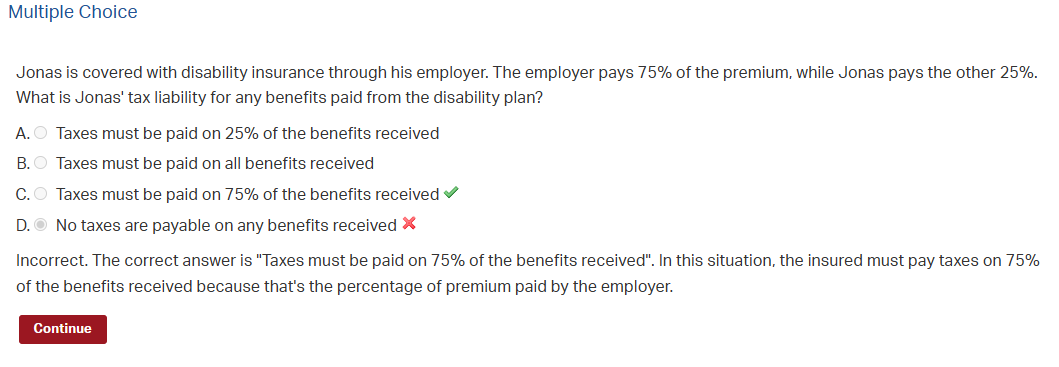

Shared premium payments:

Portion paid by employer: Benefits taxable

Portion paid by employee after-tax: Benefits are tax-free

Government Disability Benefits:

SSDI: Partially taxable if income exceeds threshold

Workers' compensation: Generally, not taxable

Exam Tips:

Exam Tips:

Know the differences between disability definitions

Understand the elimination period vs. the probationary period

Remember that individual policies are occupational, while group policies are often non-occupational

Know that disability benefits can never exceed pre-disability income

Understand the taxation principle: money is taxed only once

Remember the key differences between business disability products

Disability Income Policy Question

Non-occupational disability coverage

Waiting period for lowest premium

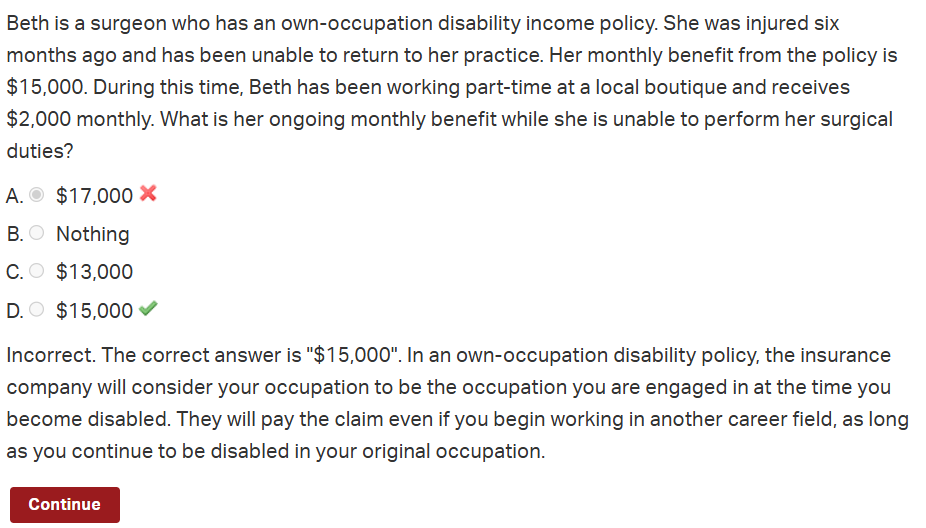

Own occupation disability income insurance

Elimination Period

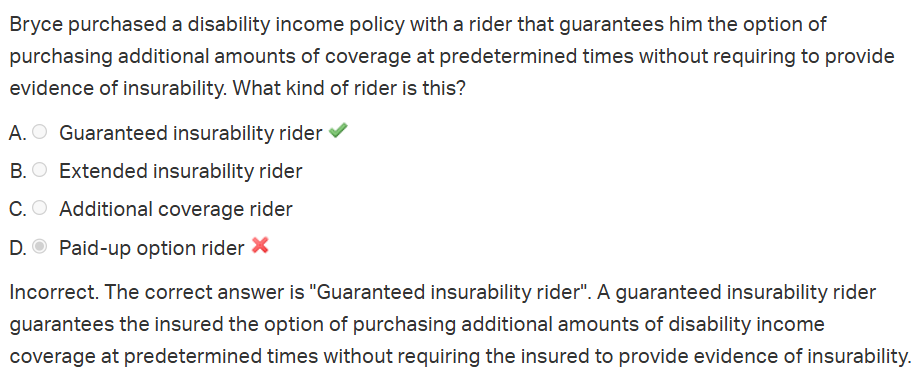

Guarenteed insurability Rider

Elimination Period 2

Reducing benefit

Group Disability income policy

SS disability income requirements

Occupational vs non occupational

No coverage if the insured can also collect workers’ compensation or other work like things is called non-occupational. If a policy gives weekly/monthly benefits of job like disabilities, along with non-occupational losses, its a occupational coverage

EX; group disability insurance: non-occupational, but individual disability insurance: occupational

Short Termdisability Plans

Short term: quickly

1a percentage of the insured income while they recover from a temporary illness. they:

Offered with a LTD beenfit, pays biweekly, minimal waiting period, provide coverage for childbirth, benefits up to 180 days, but max benefit period of 2 years

SHort term disability insruance income benefits

Long term disability Insurance PLans (LTD) Insurance

Provides longer benefit periods and can oftern address needs stemming from a more serious injury or sickness. SInce longer, the cost is higher, but longer elimination can reduce costs. The length depends on

- if they applied for group or individual coverage

- the risk of injury or illness with ones occupation

- Traits of gender, age, and medical history

Total disability

A loss of income, ability to work, or both. Insueres add the “gainful employment” or “in any occupation for wages or a profit” to make sure that those collecting benefits were indemnified and not using insurance to profit from any injury.

Inability to perform duties/ material duties/ substantial duties

Refers to the actual tasks/ activites the person has to do for the job, while the other is for the persons “key duties” and essential capabilities that makes them work

Example: surgeon holding a scalpel (MD) cannot keep their hand steady (SD)

Own occupation

Used in commericla insurance, it considers the insured to be disabled if they "cannot perform the material and substantial duties of their own occupation." Its also very beneficial for the policy owner as its less restrictive and an “any occupation” and can take alternative sources of income

Any occupation

Disabled if they “cannot perform the MD and SD dutie, or any for which they can be reasonably suited by knowledge, training, and experience. If youre a surgeon, and you have a shaky hand, youre disabiled as you cannot perform surgeries anymore

Substanyial gainful activities

The definition to get Social Security Disability Insurance, or ANY GAINFUL WORK. They must be unable to engage in any activities because of a mental or physical activity that is

-expected to be a death

-Has lasted 12 months

- Is supposed to last for 12 more months

and its definition of “gainful” activities include

- Performed for poy or profit

- Generally performed for pay or profit

- Intended for profit, where or not a profit is there

- Perforned part time

Loss of earnings/ Pure loss of income

Loss of wages, salary, commissions, and fees for services, but does not cover rental income form real estate, interest on savings, and investment dividends. PLOI is that a earned income must decrease by 20% for any disability benefit

Recurrent disability

Standard Clause included in a disability insurance policy and applies when the insured suffers a disability

the relapse is considered a recurrence of the initial disability if it occurs within six months after the insured returns to work.

If they have a 5 year benefit and disabled 6 months before work, they would have 4 and a half years of the benefit period remianing

For example, let's assume that Bob owns a disability income policy that pays $1,000 per month with a 30-day waiting period. Bob becomes totally disabled and is out of work for five months. He then returns to work for three months but suffers a relapse of the same disability and is out of work for another four months. How many months of benefits will be paid?

In this case, eight months. He receives benefits four months after the initial elimination period and then another four months during the recurrence because there's no elimination period.

If Bob had gone back to work for seven months and then suffered a relapse, he would have collected seven months of benefits because he would have needed to satisfy a waiting period for each separate disability.

Presumtive disability

Medical definition fo disability. It counts for Double dismemberments, complete loss of sight, hearing, and speech. When the injury falls to severe, it goe sinto this category, and the insurance company waives its other criteria of benefits such as occupational duties, and they ensure the for the physical loss, independent of the financial consequences. Disability is defined by the medical condition, not the financial loss

Concurrent Disability

When disability events occur somuntaneouly and its one period of disability. The insured collects only one benefit as there is only one loss even with multiple causes

Delayed Disability

a total disability that does not occur immediately after an accident; rather, it develops later, and remain eligible for benefits due to theeffects of an accident for an extended period

Confining Versus Non-Confining Disability

first requires the insured to be in doors, while the other is not required to remain indoors

At work benefits

Encourages beneficiaries to return to work by paying a portion of the total disabillity benefit to those who ease back into the workforce.

Partial Disability

The inability to perform one or more of th eimportant orkey duties of ones own occupation, or the inability to work at ones regular occupation full time. Based on insured’s loss of income and the beenfit is paid regardless of if it comes from an illness or accident. I t also allows a partialluuy impaired person to maintain pert-time beenfits while still working part time

The amount of a policy's partial disability benefits payable is dependent on whether the policy stipulates a flat amount or a residual amount. For purposes of this course and exam, the assumption should be that the standard partial disability benefit is 50% of the policy's total disability benefit.

For example, let's assume that an individual earns $4,000 per month and owns a policy with a total disability benefit equal to 60% of their income. Therefore, their total disability benefit is $2,400 per month. The monthly partial disability benefit is 50% of $2,400, which equals $1,200.

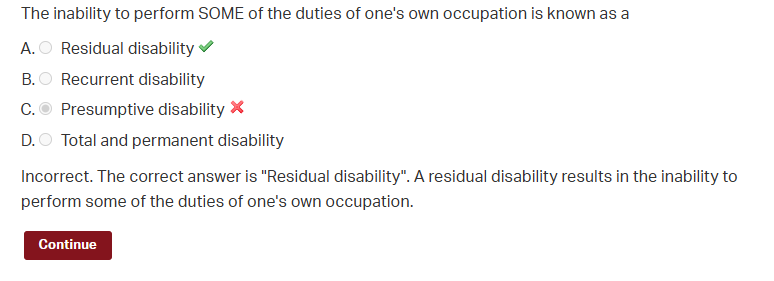

Residual Disability

Proportional disability benefit that a person collects when working less than full-time due to a covered disability and suffers an income loss of at least 20%

Credit Disability insurance

CAn be purchased to help make loan payments if the insured becomes disabled. It pays the monthly installment, and since the policy pays off a specific debt, the benefit is typically decreases as the debt is paid down

Premium rider waiver and the disability income rider

PRW waives the premium if the insured becomes disabled, but DIR provides beenfits such as 1% payable if they become disabled

GOVERNMENT (SOCIAL) DISABILITY INSURANCE

Gov. programs that provide a safety net for people with injuring ocnditions. Provides it with someone with a work history at some point

SOCIAL SECURITY DISABILITY INSURANCE

Social Security Administration (SSA) provides disability-related benefits through the SS OASDI program for fully funded payroll taxes paid by empoyees, employers, and self employed employees. 10 years of fully paid taxes earns the person with a pernament fully insured status. Their diability ounts as expected to die or has lasted or is expected to a disabled for at least 12 months and has been for at least 12 motnsh

Waiting period

5 month time before qualified for benefits, where the benefits themseves can accrue during the 6th month and paid at the end of the month

benefits of a worker

A workers SSDI beenfit equals 100% of their primary insurance amount (PIA)

Primary Insurance Amount (PIA)

An individuals benefit level based on their incomes history and FICA taxes from that time

WORKERS' COMPENSATION

A form of liability that provides medical disability and survivor benefits to workers in work related accidents. They have a temporary and pernament disability, very similar to earlier

PROBATIONARY PERIOD

Not an elimination period as now it happens only once at the policy’s inception. In a disability insurance policy defines the period that must pass before it covers illness claims and acts for 15, 30, or 60 days

THE BENEFIT PERIOD

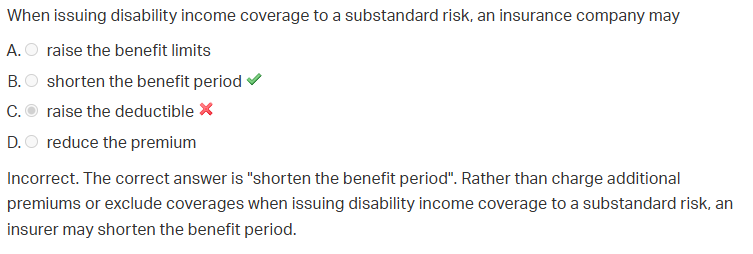

The maximum length of timer per disability claim that an insurer will provide benefits to a covered individual suffering a loss of incomes. Underwriting determinations are based on job categories and one’s health. Shorter beenfit periods are standard with higher risk.

Individual short-term DI policies have benefits of few to 24 months

Individual LT DI are from 2 years to a lifetime if still disabled

DISABILITY BENEFIT AMOUNTS

Issue individual policies that limit coverage to a percentage of the insured’s incme. LTD Policies pay beenfits monthly Insurers use the percent-of-earnings approach or the flat amount method.

THE PERCENT-OF-EARNINGS APPROACH

For example, if an insured's policy provides a 60% benefit based on a monthly gross income of $3,000, the monthly benefit equals $1,800 (60% × $3,000). If the insured's income increases to $3,200, the 60% benefit will increase to $1,920 (60% of $3,200).

THE FLAT AMOUNT APPROACH

For example, if Barry, the policyholder, has $3,000 in gross earned income per month, an insurer could issue a policy with a monthly benefit equal to 60% of the insured's monthly income, or $1,800. Unlike our previous example, a policy using this approach defines the benefit as $1,800 in the contract language, NOT 60%. Because the benefit is defined as $1,800, it would not change in reaction to changes in Barry's income. If Barry's income rose to $3,300, the policy benefit remains $1,800.

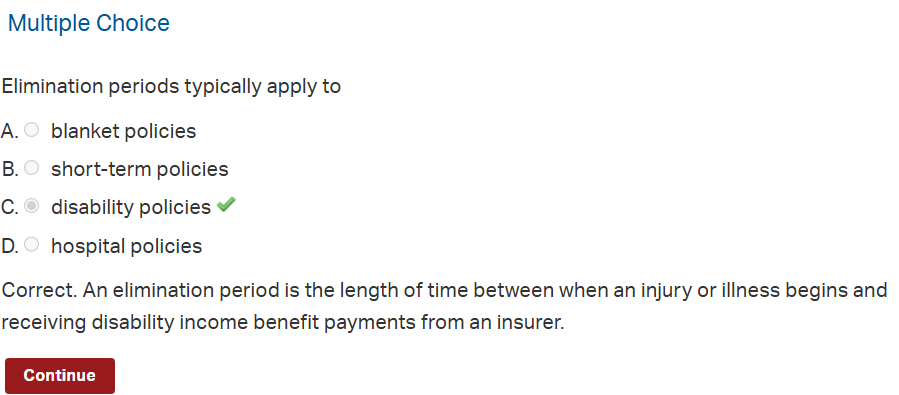

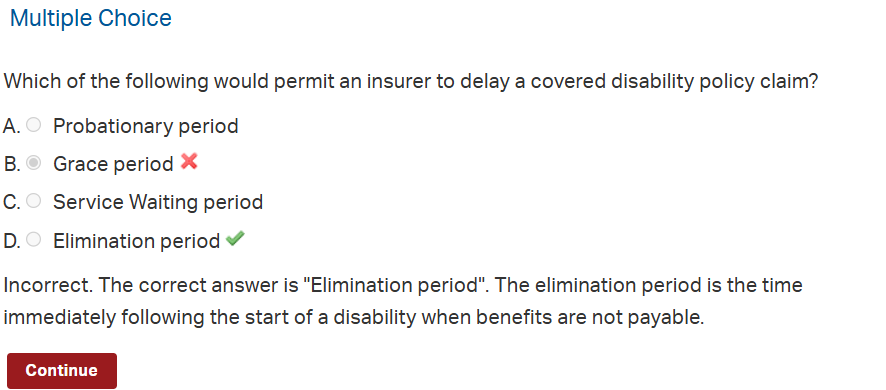

Elimination Period

The waiting period and the period immeidately after the onset of disability which beenfits are NOT payable. The longer the waiting period, the lower the policy premium. Same goes for an elimination premium and allows the insurer to reduce coverage costs

Premiums for DI

Length of the waiting period

Monthly income benefit amount

Length of the benefit period

Age, (gender), income, and health of the applicant

Insured's occupation

Whether the insured owns other disability income insurance

Most IDP are sold with premium that doesnt change with age.

Annually REnewable Disability Insurance

Companies that offer policies with age-sensitive premiums. Costs strat lower than a comparable level premium policy but increase above average.

Exclusions

War (declared or undeclared)

Intentionally self-inflicted injuries

Aviation-related claims of a pilot or crew member, unless a commercial aircraft or pilot is involved (which is covered)

Military service

Losses that result from engaging in any illegal occupation

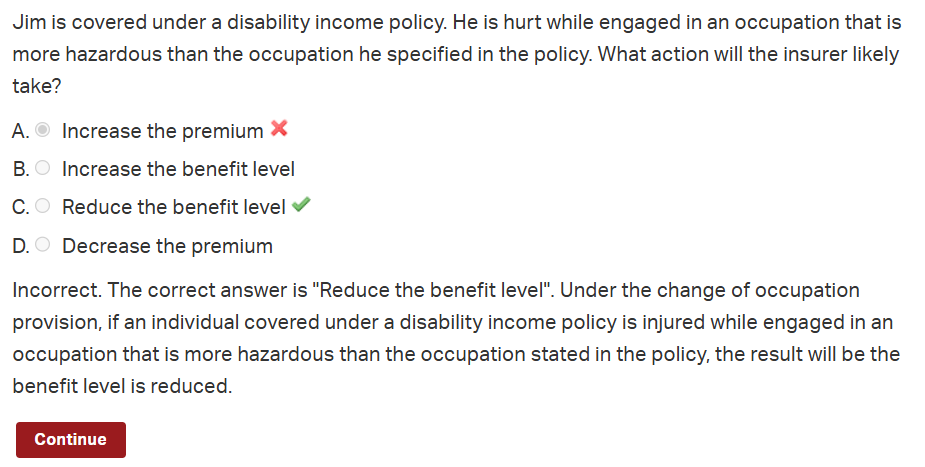

Change of Occupation provision

If a person is covered under a DIP and is injured whiie engaged in an occuation more dangerous that theoccupation that is stated in the policy, the beenfit level is reduced.

RElation of earning to the insurance

Addresses situations where more than one policy covers the same disability claim, so the total beenfits will not exceed the insured’s pre-disability income.

Impairment rider/ Exlcusion rider

This rider ensured certain losses from coverage, and the excluded risk stems from an occupation

Rehabilitation beenfits

Encourages people to actively participate in their recovery and help then return to work in at least a year. It facilitates coational training to help the person for the new occupation

Non-cancelable and guarenteed renewable

The inusrer guarantees the premium charge at the time the policy was issued and the carrier cannot raise the rate during the life of the policy

Tax liability for any benefits paid

What a company should do

residual Disability

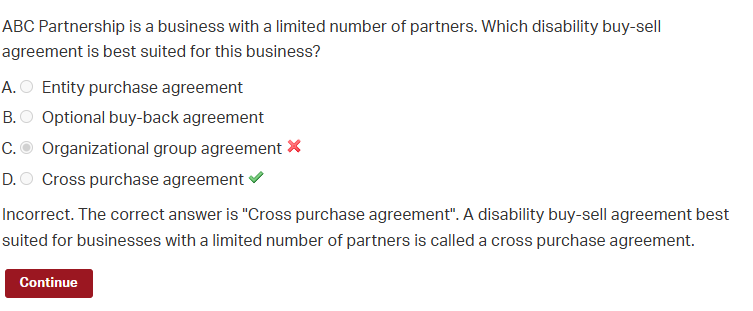

cross purchase agreementf