FRM Unit 3 - Financial Products & Markets

1/146

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

147 Terms

Describe the Dutch Auction Approach to raising capital.

Under the DAA, potential investors enter their bids quoting the number of shares they intend to purchase and the price they are willing to pay per share. Once the bids have been submitted, the allotment is done starting from the highest bid down, until all the allotted shares have been assigned. However, the final price paid per share is that which has been quoted by the last successful bidder – the buyer whose bid coincides with the end of the intended allotment.

The presence of deposit insurance can lead banks to assume greater risks in investment strategies, under the assumption that deposit protection will buffer against depositor panic and withdrawal. This can be described as what problem?

Moral Hazard Problem

Deposit insurance provides protection to depositors in case their bank fails, which reduces the risk for depositors. However, it also creates a moral hazard problem for banks, as they are incentivized to take on riskier investments since the cost of default is borne by the insurance fund, not the bank itself.

The term 'moral hazard' refers to the risk that a party insulated from risk may behave differently than it would if it were fully exposed to the risk.

The originate-to-distribute banking model can indeed lead to a misalignment of incentives between banks and investors. Why is this the case?

This is because banks, under this model, may prioritize the quantity of loans originated over their quality. This is due to the fact that banks do not retain the loans on their balance sheets and, therefore, do not bear the risk of default. As a result, they may be incentivized to originate loans without adequately assessing the creditworthiness of the borrowers, leading to increased risk for the investors who purchase these loans. This misalignment of incentives was one of the factors that contributed to the subprime mortgage crisis in 2007-2008.

The LCR helps to ensure that banks can meet their short-term obligations even under severe liquidity stress scenarios. How is it calculated?

The liquidity coverage ratio (LCR) is a regulatory requirement introduced by the Basel Committee on Banking Supervision. It is designed to ensure that banks have sufficient high-quality liquid assets to survive a 30-day period of acute stress. This stress could be caused by a variety of factors, such as a downgrade in the bank's credit rating, a loss of deposits, or drawdowns on its lines of credit. The LCR is calculated by dividing a bank's high-quality liquid assets by its total net cash outflows over a 30-day stress period. The aim is to promote short-term resilience of a bank's liquidity risk profile by ensuring it has sufficient high-quality liquid assets to survive a significant stress scenario lasting for one month.

In corporate finance, companies often employ various defensive strategies to protect against hostile takeovers. What is an example of a poison pill?

A poison pill, or shareholder rights plan, is a defensive strategy used by corporations to deter hostile takeovers by diluting the shares held by potential acquirers, making a takeover less attractive or more costly.

Issuing preferred shares that automatically convert to common shares upon a takeover attempt dilutes the voting power and ownership percentage of the acquirer, directly impacting the feasibility and attractiveness of the takeover. This is a classic example of a poison pill tactic.

In the context of banks, the banking book and the trading book represent two distinct portfolios used to manage different types of assets and risks. What is the difference between a banking book and a trading book as used in banks?

The banking book consists of assets on the bank's balance sheet that are expected to be held until maturity. These assets are not marked to market, meaning they are usually held at historical cost. The banking book typically includes loans, mortgages, and bonds. The purpose of the banking book is to earn interest over a long period, and the risks associated with the banking book are credit risk and interest rate risk.

On the other hand, the trading book consists of assets that are available for sale, meaning that they are eligible for day-to-day trading. Under Basel II and III, the trading book has to be marked to market on a daily basis. The trading book typically includes financial instruments like government and corporate bonds, derivatives, and equities. The purpose of the trading book is to earn profits from short-term price fluctuations, and the risks associated with the trading book are market risk and liquidity risk.

Define a broker discretionary account:

A broker's discretionary account is an investment account that allows an approved broker to buy and sell securities without obtaining the client's permission for each transaction. But to be able to do so, the client must sign a discretionary disclosure with the broker.

Such accounts are subject to regular oversight and compliance checks to ensure that all trades align with the client's stated investment goals and risk tolerance. The use of discretionary accounts can be advantageous for clients who may not have the time or expertise to manage their investments actively.

Private placements provide a streamlined fundraising avenue without the need for SEC registration, which is mandatory for public offerings. This exemption from registration saves time and reduces disclosure requirements. In private placements, who are the securities sold to?

In the context of investment banking, a private placement refers to the process where securities are sold to a select group of large institutional investors. These investors can include insurance companies, pension funds, or mutual funds. The investment bank that underwrites the arrangement receives a fee that is negotiated with the issuer.

Regulatory capital and economic capital are two critical concepts in risk management and financial regulation, serving distinct purposes in the financial industry. Distinguish between regulatory capital and economic capital.

Regulatory capital refers to the minimum amount of capital that a bank is required to hold by regulatory authorities. This is to ensure that the bank has enough capital to absorb a reasonable amount of loss and mitigates the risk of failure. The amount is determined based on the bank's financial condition and compliance with regulatory standards.

On the other hand, economic capital is the amount of money that a bank chooses to hold based on its own risk models. This is determined by the bank's internal assessment of potential risks and the capital required to cover those risks.

In insurance, define the loss ratio, expense ratio and combined ratio.

Loss Ratio: Measures the proportion of claims paid to premiums earned by the insurance company.

Expense Ratio: Shows the proportion of operating expenses relative to premiums earned.

Combined Ratio: Sum of the loss ratio and the expense ratio, indicating overall underwriting performance.

The Solvency Capital Requirement (SCR) and the Minimum Capital Requirement (MCR) under Solvency II regulations are two different capital requirements that insurance companies must meet. What are the differences between the two?

The SCR is a higher capital requirement that is designed to ensure that insurance companies have sufficient capital to absorb significant losses with a 99.5% confidence level over a one-year horizon. This requirement takes into account various risk factors, including underwriting, market, credit, operational, and other risks.

The MCR serves as a lower threshold for capital adequacy. If an insurance company's capital falls below this level, it triggers immediate supervisory intervention. The insurance company may be prevented from taking on new business, and existing policies might be transferred to another insurance company.

Therefore, the SCR and MCR work together to ensure the solvency and financial stability of insurance companies.

Adverse selection occurs when individuals with higher risk are more likely to purchase insurance compared to those with lower risk. What is an example of this in the life insurance market?

Adverse selection occurs when the party with more information takes advantage of the party with less information.

In the case of life insurance, adverse selection can occur when the insurance company fails to ask the applicants to disclose pre-existing medical conditions, resulting in a higher-risk pool of policyholders.

One way to mitigate adverse selection is through risk-based pricing, where individuals with higher risk profiles are charged higher premiums.

Given the information below, the operating ratio for a property-casualty insurance company is closest to?

Loss Ratio: 65%

Expense Ratio: 15%

Combined Ratio: 80%

Dividends: 3%

Investment Income: 5%

The insurance company’s operating ratio is a gross profitability measure. It is calculated by adding the loss ratio, expense ratio, and dividends and deducting the investment income earned if the investment earned a positive return. If the investment had a negative return, it should be added to the equation.

Operating Ratio = 65%+15%+3%−5% = 78%

What is variable life insurance?

Variable life insurance is indeed a type of whole life assurance that includes an investment component. This means that a portion of the premium paid by the policyholder is invested in various sub-accounts available within the policy. This feature of variable life insurance makes it a unique and attractive option for policyholders who are not only interested in life coverage but also in investment opportunities.

In property insurance, different types of coverage present varying levels of risk to insurers. What poses the greatest risk of loss for an insurer?

Insurance against natural disasters - this type of insurance falls under Category B risks, where a single event can lead to many claims at the same time.

These risks are particularly challenging to model due to the scarcity of data and the unpredictable nature of catastrophic events. For instance, a hurricane can either occur, leading to most policyholders filing a claim, or not occur, resulting in no claims. This all-or-nothing nature of natural disasters makes them the greatest risk of loss for insurers.

Term life insurance is a type of life insurance that provides coverage for a certain period of time, or a 'term'. If the insured dies during this term, the death benefit is paid out to the beneficiary. What are some features of term life insurance?

Term life insurance is typically more affordable than permanent life insurance because it only provides coverage for a specific term.

Term life insurance does not have a cash value component like some permanent life insurance policies.

Term life insurance is often used to cover specific financial obligations that will decrease over time, such as a mortgage or a child's education expenses.

Term life insurance policies can usually be renewed at the end of the term, but the premiums may increase based on the insured's age and health at that time.

Some term life insurance policies offer the option to convert to a permanent life insurance policy without the need for a medical exam.

What does an increase in mortality risk do to insurance company profits?

An increase in mortality risk decreases the profits made by the insurer.

This is because mortality risk is the risk that policyholders will die sooner than expected due to factors such as epidemics, pandemics, and wars. When mortality risk increases, policyholders live for shorter periods of time than expected and therefore make fewer premium payments to the insurance company before the insurance company needs to make payments for the sum assured. The insurance company will receive less in payments but still be required to pay the policy assured amount to beneficiaries. This reduces the profitability of the life insurance business.

Longevity risk refers to the risk that policyholders may live longer than initially estimated. What is the impact of increase in longevity risk on annuity providers?

It decreases profits. Lifelong annuity contracts are structured such that the insurer agrees to make regular payments to the policyholder from a certain age until their death. If the policyholder lives longer than initially estimated, the insurer is obligated to continue making these payments for a longer period.

An increase in longevity risk can lead to higher costs for insurers, reducing their profitability as they may have to make payments for a longer period than initially estimated.

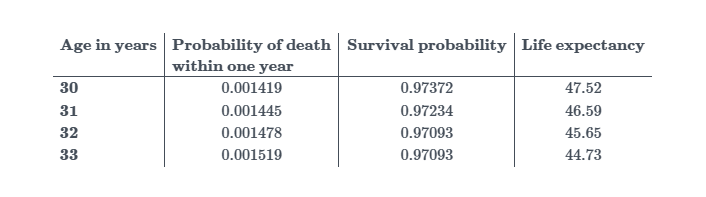

The following data gives the mortality experience among males in Europe in 1931. Calculate the probability of a new-born male dying between his 30th and 31st birthday.

From the table, the probability of a man surviving to age 30 is 0.97372.

The probability that a new-born male dies between age 30 and 31 equals the probability that the newborn lives until age 30 (0.97372) and dies in the 30th year (0.001419)

Thus, the probability of a new-born male dying between his 30th and 31st birthday is: 0.97372×0.001419=0.00138

Define the terms clearing process and settlement process:

Clearing process involves the calculation and netting of payment obligations between parties in OTC derivatives transactions.

Settlement process is the fulfillment of contract obligations after the clearing process has determined the net obligations.

In the insurance industry, certain companies specialize in providing guarantees for specific types of financial products. What is the definition of a monoline?

Monolines, also known as Credit Derivatives Product Companies (CPDCs), are akin to insurance companies with strong credit ratings. They provide credit wraps (financial guarantees) and credit default swaps (CDC) to achieve diversification and better returns. They are structured as an extension of a Derivative Product Company (DPC) that focuses solely on credit default swaps.

What is the definition of a Special Purpose Vehicle (SPV)?

A Special Purpose Vehicle (SPV) is a subsidiary company with a distinct asset/liability structure and legal status that ensures its obligations remain secure, even if the parent company goes bankrupt.

SPVs are typically used in securitization transactions, allowing companies to isolate or pool assets, or to allow investors to invest in a specific set of risks. The SPV's assets are typically held off-balance sheet, which can help to protect them from the parent company's creditors. This structure also allows the parent company to maintain a cleaner balance sheet, while also potentially reducing the amount of capital required to be held against the assets. SPVs are often used in complex financing transactions, such as mortgage-backed securities, collateralized debt obligations, and lease financing.

A trader with a net long position in a call option is not required to post margin by the Chicago Board Options Exchange (CBOE). True or False?

True

A trader with a net long position in a call option is not required to post margin by the Chicago Board Options Exchange (CBOE). This is because when a trader holds a net long position in an exchange-traded stock option, they have no potential future liability.

These positions are often purchased upfront, and the option may or may not be exercised. Consequently, there is no reason for the exchange to require margin from a trader who holds a long position in a call option or a long position in a put option. The trader has already paid the premium for the option, which is the maximum amount they can lose. Therefore, the exchange does not require any additional margin from these traders.

Define Maintenance Margin:

The minimum amount of equity that must be maintained in a margin account to avoid a margin call. e.g a maintenance margin requirement of 40% means the investor must maintain equity of at least 40% of the market value of the shares.

When the balance in a margin account falls below the maintenance margin level, the broker will issue a margin call requiring the investor to deposit more funds.

In the event of a clearing member default, a central counterparty (CCP) seeks to auction off the defaulting member’s portfolio. What is the CCP’s most immediate objective during the auction process?

To reallocate the defaulting member’s portfolio in full, even at a potential loss, in order to restore a matched book and eliminate market exposure.

The CCP does not close out at market prices automatically; it uses the auction to establish a price.

To support their operations and manage the risks, CCPs have two primary sources of revenue, what are these?

Fees on clearing trades and interest on the margins.

CCPs charge fees on clearing trades as a significant source of income.

Interest earned on margins posted by members is another revenue source for CCPs.

CCPs do not earn from trading spreads as they do not participate in trading activities.

Initial margins collected by CCPs serve as collateral and are not direct sources of revenue.

Moral hazard refers to the risk that one party may take on excessive risks because it believes that another party will bear the costs of those risks. Give an example of this in the context of CCPs:

It is the moral hazard related to the effect of disincentivizing counterparty risk management practices by CCP members. Since the CCP acts as the counterparty to the transaction, the party or institution invests little resources in monitoring others parties’ credit quality.

This can lead to a moral hazard as parties may engage in riskier behavior, knowing that the CCP will bear the brunt of any potential losses. This can potentially lead to systemic risk if many parties engage in such behavior and the CCP is unable to cover the losses.

The CCP’s loss waterfall ensures that losses are covered in a carefully ordered sequence. What is this sequence?

The CCP first uses the defaulting member’s initial margin, then the defaulting member’s default fund contribution, followed by the mutual default fund from non-defaulting members, and finally the CCP’s own equity.

This structure incentivizes all members to cooperate in an orderly close-out or auction process to limit systemic risk and protect each member’s default fund contributions from being used.

Central Counterparties (CCPs) play a crucial role in the financial markets by reducing counterparty risk and enhancing market liquidity. However, they are not immune to risks themselves. One of the significant risks they face is liquidity risk. What is one of the main sources of liquidity risk in CCPs?

Varying margin payments. Varying margin payments can lead to liquidity risks as they can cause fluctuations in the amount of cash or collateral required, potentially leading CCPs unable to meet their obligations.

Describe sovereign risk faced by a central counterparty (CCP)

Sovereign risk, in the context of a CCP, is primarily associated with the potential failure of its members who have held sovereign bonds as margin. These bonds may decline in value due to a sovereign default or failure. This situation can significantly impact the financial stability of the CCP and its ability to manage counterparty risk.

Members of a CCP often use repo rates as a risk management tool. During the Eurozone crises, it was observed that sovereign risk is strongly correlated with repo rates. This means that an increase in sovereign risk can lead to an increase in repo rates, which can further exacerbate the financial strain on CCP members holding sovereign bonds as margin.

Price limits are the maximum price movement/limit set by exchanges. Define what is meant by ‘limit up’

Limit up occurs when the price of a futures contract increases by the predefined limit during a trading session.

The Karachi Mercantile Exchange (KME) has set the daily price limit of rice futures contracts to Rs.4. The closing price of the rice futures contract on Monday was Rs.140 per 100 KG. If the evening newspaper on Wednesday reads that “Rice futures contracts closed limit down at Rs.138 per 100 KG,” then which of the following is the most likely closing price of the rice futures contract on the preceding day?

Suppose the intraday increase in the price of the futures contract is equal to the predefined price limit. In that case, the contract is said to be limit up, whereas if the intraday decrease in the price of the futures contract is equal to the predefined price limit, the contract is said to be limit down. Since the newspaper reads that the price of the contract closed limit down (price decreased by Rs. 4) at Rs. 138, the preceding day (i.e., Tuesday) price is:

Limit down close to the current day = Closing price of the preceding day – Price limit

The closing price of the preceding day = Rs. 138 + Rs. 4 = Rs. 142

How are futures settlement prices calculated?

The average price at which the contract is traded during the last period or before the end of a day's trading period. The exchange itself sets the settlement price. This is done to prevent traders from manipulating futures prices. Settlement prices are used for for calculating daily gains, losses, and margin requirements.

A trader wants to sell a call option on a stock in a volatile market but wants to ensure that the option is sold above a certain price point. Which of the following order types should the trader use to guarantee execution at or above that price point?

Stop limit order.

A stop-limit order is an order to sell (or buy) at a specified price or better after the price has reached a specified stop price. This type of order combines both a stop order and a limit order, meaning that the order will be executed at a specified price or better but only after the stop price has been reached. In this case, the trader can set the stop price at the desired price point and the limit price at the minimum price they are willing to accept for the option. This ensures that the option is sold at or above the desired price point.

Define the High-water mark clause in hedge funds fee structures.

A provision in a hedge fund's agreement that ensures the fund manager only earns incentive fees on new profits generated after previous losses have been recovered and hurdle rates surpassed.

Management fees in hedge funds are a fee paid to the investment manager for managing the assets, usually calculated as a percentage of the total assets under management.

Generally what is the fee calculated on?

It is usually assumed that the management fee is calculated on the assets at the beginning of the year and that the incentive fee is calculated after subtracting management fees (usually).

What is a fixed income arbitrage hedge fund strategy?

A fixed income arbitrage hedge fund strategy typically involves exploiting pricing discrepancies between related fixed income securities. The goal is to profit from these inefficiencies by buying underpriced securities and simultaneously selling overpriced ones. These related securities might include bonds of different maturities, issuers, or structures that have mispriced relationships based on market factors.

Define convertible arbitrage strategy:

Convertible arbitrage is a specific type of fixed income arbitrage strategy that involves buying convertible bonds and selling the underlying stock.

Closed-end funds are a type of investment fund and exchange-traded product (ETP). What are some of their key features?

Closed-end funds raise a prescribed amount of capital only once, through an initial public offering (IPO), and list shares for trade on a stock exchange. Unlike open-end funds (mutual funds), closed-end funds do not stand ready to issue and redeem shares on a continuous basis. Instead, the shares can be purchased and sold only in the market.

What undesirable trading behavior involves using market developments after 4 pm to cancel or carry out a trade?

Late trading refers to the practice of placing orders to buy or sell securities after the close of a trading day's official trading hours (typically 4 pm in the U.S.), but still having these orders executed at the closing price of the same trading day.

This is considered undesirable and illegal because it allows traders to take advantage of post-close market developments and information that are not yet reflected in the closing price, thereby creating an unfair trading environment. Late trading is particularly problematic in the context of mutual funds, where it can lead to dilution of the fund's assets and harm to long-term investors. It is considered a serious offense and is punishable by law.

Define the term NAV and how it is calculated.

The Net Asset Value (NAV) of an open-end mutual fund is indeed the total value of all assets held by the mutual fund, minus any liabilities, divided by the total number of shares outstanding. This value is calculated at the end of each trading day based on the closing market prices of the securities held by the fund.

The NAV is used to determine the price at which shares of the mutual fund are bought and sold. If demand for the mutual fund is high, the share price will be above NAV, and if demand is low, the share price will be below NAV. The inverse relationship between share price and NAV is due to the fact that new shares are issued or redeemed at NAV, but shares are bought and sold on the open market at the prevailing market price.

Which measurement bias is primarily associated with voluntary reporting of performance results by hedge funds and mutual funds?

Self-reporting bias is a type of measurement bias that is primarily associated with the voluntary reporting of performance results by hedge funds and mutual funds.

This bias occurs when funds with strong performance are more likely to voluntarily report their results, while funds with poor performance may not report or may selectively report their results. This leads to an overestimation of performance for both types of funds, as the reported performance data may be skewed towards better-performing funds.

What is the hurdle rate?

The hurdle rate in the context of hedge funds refers to the minimum rate of return that must be achieved before the incentive fee can be applied.

When most actively managed mutual funds are compared to index funds such as the S&P 500, they:

Generally do not outperform the market.

This is a well-documented phenomenon in the world of finance. The reason behind this is multifaceted. Firstly, actively managed funds incur higher transaction costs due to frequent buying and selling of securities, which can eat into the returns. Secondly, predicting the market consistently over the long term is extremely difficult, even for seasoned fund managers. Lastly, the fees associated with actively managed funds are typically higher than those of index funds, further reducing the net return for investors. Therefore, while some actively managed funds do outperform the market in certain years, on average and over the long term, they do not tend to outperform the market.

Translation risk and transaction risk are two types of foreign exchange risks that multinational corporations often face. Define these two types of FX risk:

Translation risk arises when a company's financial statements, which are in a foreign currency, are converted back into the parent company's currency. This type of risk does not directly affect the cash flows of a company, but it can impact the reported earnings and equity.

On the other hand, transaction risk is associated with future cash flows that might change due to changes in exchange rates. This type of risk directly affects the cash flows of a company.

What does a 4% appreciation in the CNY/ZAR exchange rate imply?

An appreciation in the exchange rate of two currencies implies that the base currency (the first currency in the pair) has increased in value relative to the quote currency (the second currency in the pair).

In this case, the CNY/ZAR exchange rate refers to the amount of South African Rand (ZAR) one can get for one Chinese Yuan (CNY). Therefore, a 4% appreciation in this exchange rate means that the Chinese Yuan has increased in value by 4% against the South African Rand. This implies that you would now need more South African Rands to purchase one Chinese Yuan than you did before the appreciation.

In a particular year, the interest rates for the EUR increase while that of the USD remain unchanged.

What will happen to the forward exchange rate EUR/USD?

When the EUR interest rate increases while the USD interest rate remains constant, the forward rate, EUR/USD is expected to decrease. Mathematically, this concept can be illustrated using the covered interest rate parity formula:

F = S×(1+rUSD)/(1+rEUR)

As the interest rate of the EUR increases, the denominator in the formula will increase, leading to a decrease in the forward rate.

The nominal interest rate in the country is 3% and the inflation rate is 5%.

Which of the following statements is true about this country?

When an investor earns at 3%, the investor’s purchasing power decreases by 2% each year.

What does the below transaction describe:

Borrow US Dollars (USD) at the prevailing USD LIBOR + 100 basis points and simultaneously enter into another contract with a counterparty. The contract would involve exchanging USD for JPY at the current spot exchange rate, and then at a future date, exchanging JPY back for USD at a pre-agreed forward exchange rate.

An FX swap.

This involves:

Spot Leg: One currency is exchanged for another at the current spot exchange rate.

Forward Leg: The same currencies are exchanged back at a pre-agreed forward exchange rate on a future date.

In an FX swap, there is no exchange of interest payments between the counterparties. Instead, the focus is purely on exchanging currencies at the spot and forward rates.

What is the difference between an FX swap and currency swap?

In an FX swap, there is no exchange of interest payments between the counterparties. Instead, the focus is purely on exchanging currencies at the spot and forward rates.

A currency swap typically involves the exchange of principal amounts at the beginning and end of the agreement, as well as the periodic exchange of interest payments in the respective currencies.

What is the difference between Purchasing Power Parity and Interest Rate Parity?

Purchasing Power Parity (PPP) theory relates to the equilibrium exchange rate between two currencies based on their relative purchasing power.

Interest Rate Parity (IRP) theory is crucial in understanding the relationship between interest rates and exchange rates in the foreign exchange market. IRP theory helps in explaining the equilibrium relationship between spot and forward exchange rates based on interest rate differentials.

What does a net short position in a specific foreign currency mean?

Net short position in a specific foreign currency means the company owes more of that currency than it owns.

What does appreciation of a currency do to imports/exports?

Appreciation refers to an increase in the value of a currency relative to another, making imports cheaper and exports more expensive and thus less competitive.

Depreciation, on the other hand, is a decrease in the value of a currency, making exports cheaper and imports more expensive.

In order to protect from the downside risk of stock prices, investors should select which option type?

Buy a put option

Put options are financial contracts that give the option buyer the right, but not the obligation, to sell a specified amount of an underlying security at a specified price within a specified time frame. This is often used as a protective strategy by investors who are concerned about potential losses in the underlying stock. When an investor buys a put option, they are essentially securing the right to sell their stock at a set price, regardless of how far the market price falls. The cost of this protection is the premium paid for the put option. Therefore, buying put options is a strategy that can effectively protect investors from the downside risk of stock prices.

A forward commitment is a legally binding promise to perform some action in the future. What are 3 types of forward commitment?

Forward commitments include forward contracts, futures contracts, and swaps.

What is a collar strategy?

A collar strategy involves buying a put option to protect against downside risk and writing a call option to generate income and limit upside potential.

A collar strategy provides protection against declines in the price of the underlying asset. By purchasing a put option, the investor has a right to sell the asset at a pre-determined price, offering protection against price declines. Writing a call option provides premium income and caps the potential profit if the asset's price rises significantly. This strategy provides both downside protection and potential for some upside gain.

How do you create a synthetic short futures contract

Created by selling a call option and buying a put option at the same strike price. This setup mirrors the payoff of a short position in a futures contract.

Allan enters into a derivative contract with one of his clients. The client is expected to sell the underlying asset to Allan at the expiration date at price P. Allan wishes to fully hedge his position using derivatives. Which of the following can help him achieve his goal?

Selling a p-strike call and buying a p-strike put is the correct strategy for Allan to hedge his position. This is because the client's obligation to sell the underlying asset implies that Allan is in a long-forward position. To hedge this position, Allan needs to create a synthetic short futures contract. This can be achieved by selling a call option and buying a put option at the same strike price. This strategy effectively replicates a short forward position, thus hedging Allan's long-forward position.

The net cash flow of an options transaction is calculated by considering the premium received at initiation and any gains or losses at maturity.

How is the premium received at initiation calculated?

On the derivatives market, options are quoted in per-share prices but only sold in 100 share lots. In other words, each put has 100 shares. For example, the put option is quoted at $7.6, but the buyer pays $7.6 100 = $760 per put option. For 5 puts, that's $760 5 = $3,800

What is the difference between European and American options?

European options can only be exercised on the expiration date, while American options can be exercised at any time up to the expiration date.

Futures contracts on jet fuel have maturity months in March, May, July, September, and December. An airline is hedging a purchase of 1 million barrels of fuel to be made on June 15 of this year. Which futures contract should it use?

The July Contract

The July contract is the most appropriate choice for the airline company. In the context of futures contracts, most positions are closed out prior to the delivery period specified in the contract. Therefore, a practical guideline for hedgers is to choose the futures contract with the earliest possible maturity month following the maturity of the desired hedge. This approach helps to avoid the volatility that often occurs during the expiration month of the contract. In this scenario, the airline company plans to purchase the jet fuel in June. Therefore, the July contract, which is the earliest maturity month following June, is the most suitable choice for the company's hedging strategy.

Julia Lange, an investment manager, has constructed a portfolio that somewhat mirrors the S&P 500 index. The investment manager intends to hedge the portfolio by taking a short position in S&P 500 futures. The current worth of the portfolio is $672,000,000, and the S&P 500 index futures price is 2,906, with each contract on $250 times the index. If the portfolio's beta is 0.78, then estimate the number of contracts Lange should short to hedge her portfolio.

722 S&P 500 futures contracts

Since the portfolio doesn’t perfectly mirror the S&P 500 index the beta of the portfolio of 0.78 will be considered in the calculation.

The number of contracts required=0.78∗(672,000,000/726,500)=722 contracts.

What is an Bermudan option?

A Bermudan option is a non-standard American option, which can only be exercised at certain dates until its expiration.

This type of option is a hybrid of American and European options. Like American options, Bermudan options can be exercised before the expiration date. However, unlike American options, which can be exercised at any time before expiration, Bermudan options can only be exercised on specific dates stipulated in the contract. This feature makes Bermudan options more flexible than European options but less flexible than American options. The pricing of Bermudan options is typically more complex due to this unique feature. It's important to note that the premiums for Bermudan options are lower than those of American options, but they are more expensive than European options.

A gap option is a non-standard option that is created with a European call option. However, the European call option used in the construction of a gap option is different from the regular European call option.

What is the payoff in a gap call option? Use X1 and X2 for strike prices.

A gap option has two strike prices i.e. X1 and X2 (where X2 > X1). When the final stock price is greater than X2 (S>X2), the payoff of the gap call option is S – X1.

For a gap call option, the payoff is triggered when the final price of the underlying asset is greater than X2, and the payoff is S -X1. Gap options provide the holder with the potential for higher payoff compared to regular call options, depending on the final price of the underlying asset.

What is a Cliquet option and when is it useful?

A Cliquet option (aka Ratchet option) is an exotic option that consists of a series of consecutive forward start options. The first option in the series is active immediately, and the subsequent options become active as the previous one expires. Each option is struck at the money when it becomes active. This means that the strike price of each option is equal to the market price of the underlying asset at the time the option becomes active.

This type of option allows investors to lock in gains periodically, providing protection against significant market downturns. However, it also limits the potential upside if the market performs exceptionally well. The Cliquet option is particularly useful in volatile markets, where the price of the underlying asset is expected to fluctuate significantly over the life of the option series.

arrier options are a type of exotic option that comes into existence or ceases to exist based on the price of the underlying asset reaching a certain barrier level. What are the two types of barrier options?

Knock-in Option: A knock-in option is an option that becomes active only if the price of the underlying asset reaches a certain barrier level.

Knock-out Option: A knock-out option is an option that ceases to exist if the price of the underlying asset reaches a certain barrier level.

What is static options replication?

Static replication is a hedging technique used to offset the risk associated with exotic options by creating a portfolio of plain vanilla options that replicates the payoff of the exotic option.

By using static replication, investors can hedge the risk of exotic options without directly trading the exotic options themselves. Static replication requires careful selection of plain vanilla options with similar attributes to the exotic option to create an effective hedge.

A bond indenture is a legally binding contract between the bond issuer and the bondholders, outlining the key terms, covenants, and responsibilities of all parties involved, including the trustee. What is the role of a corporate trustee?

Trustees provide an additional layer of oversight, which helps protect bondholders by monitoring the issuer’s adherence to the agreed-upon terms and taking necessary action in the event of non-compliance.The role of a trustee in a bond issuance is to act as a representative for the bondholders. Trustees are typically compensated by the bond issuers for their services.

What are Yankee bonds?

Yankee bonds are issued in the U.S. market by foreign entities, including sovereign governments, foreign banks, companies, or government agencies. E.g a bond issued by a German municipal government in the U.S. falls under the 'Yankees' category.

What should be used to calculate the coupon on a bond?

The coupon or interest on a bond is calculated on the par value of the bond. The par value, also known as the face value, is the amount that the bond issuer originally receives from the bondholder and promises to repay upon the bond's maturity. The coupon rate is expressed as a percentage of this par value.

What are participating bonds?

Participating bonds are a type of fixed income instrument that not only pays a fixed coupon at a specific date but also allows the bondholder to share in the issuer’s profit if the issuer's profits exceed a certain threshold. This type of bond is particularly attractive to investors who want to benefit from the potential upside of the issuer's performance while still receiving regular fixed income payments.

What are Debenture bond issues?

Debenture issues are unsecured bonds, which results in lower prices and higher interest rates. Debenture bonds are unsecured bonds that are backed only by the creditworthiness and reputation of the issuer.

Debenture bondholders have a claim on the company's assets after the claims of secured bondholders are satisfied (but are before subordinated bondholders).

A callable bond gives the issuer the right to redeem the bond before its maturity date. When is this beneficial?

Callable bonds are more advantageous for the issuer in a decreasing interest rate environment as they can refinance at lower rates. However callable bonds are less attractive to investors compared to non-callable bonds due to the risk of early redemption.

Hauser Corp., a German portable house construction firm, is raising $500 million through 7-year 9% semi-annual coupon bonds. Classico Investment Company is interested in purchasing 33% of Hauser’s total bond issue, but it has put forward a condition that requires the issuer to retire a portion of the principal of the debt each year until maturity rather than paying the whole capital at maturity. What is this known as?

The sinking fund provision.

This provision is a protective covenant in the bond indenture that requires the issuer to retire a certain portion of the bond issue each year. The issuer can achieve this by either buying back a certain number of bonds in the open market or using a lottery system to select which bonds to retire. The sinking fund provision is designed to reduce the risk to bondholders by ensuring that the issuer does not default on the entire bond issue at maturity. It also helps to reduce the potential impact of a default on the bondholders. The sinking fund provision is beneficial to the bondholders as it provides a form of repayment guarantee. However, it can be disadvantageous to the issuer, especially in a declining interest rate environment, as the issuer may have to retire the bonds at a premium.

What is a tender offer provision?

A tender offer provision is a mechanism that allows for the early retirement of debt, even if it is not included in the bond's indenture. In a tender offer, the issuer of the bond sends an offering circular to the bondholders of record. This circular presents the price that the issuer is willing to pay to buy back the bond, as well as the window of time during which bondholders can sell their bonds back to the issuer. This mechanism is particularly useful in situations where the issuer has sufficient funds to retire the debt before its maturity.

What is Bridge financing?

Bridge financing is a short-term financing option used by companies before they can secure permanent financing. It 'bridges' the gap between when a company's money is set to run out and when it can expect to receive an inflow of funds later. Bridge financing is a common strategy used in leveraged buyouts and mergers and acquisitions to cover the period between the deal closing and securing long-term financing.

Suppose that the bond that will be cheapest to deliver in a Treasury bond futures contract pays annual coupons of 6% per annum on March 1 and September 1 and will be delivered on June 1. Suppose further that the bond's clean futures price is 121.4848 on June 1, and its conversion factor is 1.2424.

If all interest rates are 5% continuously compounded, what is the dirty price on June 1?

We have 184 days( =30+30+31+30+31+31 +1 in March, April, May, June, July, August, and September, respectively)

We have 92 days between March 1 and June 1(= 30 + 30 + 31 + 1 in March, April, May, and June, respectively)

The accrued interest on June 1 is, therefore,

3×92/184=1.5

We know that,

Clean Futures Price=Dirty Futures Price−Accrued Interest Thus,

Dirty Futures Price=Clean Futures Price+Accrued Interest=121.4848+1.5=122.9848≈123

Suppose that a nine-month interest is expected to be paid on a USD 30,000,000 bond. Suppose further that three-month Eurodollar futures contracts are used to hedge the nine-month interest and that the nine-month period starts at the maturity of the futures contract that will be used.

How many three-month Eurodollar futures contracts are necessary to hedge the nine-month interest?

The change in the value of the instrument for a 1-basis point parallel shift in the interest rate is:

USD 30,000,000×(9/12)×0.0001=USD 2250

We know that the interest rate per three months changes by 0.0025%, which is equivalent to USD 25 on a principal of USD 1 million. In other words, a Eurodollar contract is designed in such a way that one basis point(0.01) move in the futures price leads to a profit or loss of $25.

Thus, the number of three-month Eurodollar futures contracts necessary to hedge the nine-month interest is:

(2250/25)=90

Suppose a Treasury bill lasts for 230 days and has a quoted price of 5.5

What is the cash price of the Treasury bill?

96.4861

We can make Y the subject of the formula so that:

=100−(5.5×230)/360=96.4861

Refinancing is defined as the process of replacing an existing mortgage with a new one - sometimes this can be as refinancing to a mortgage that has a lower interest rate. When is this more likely to occur?

During periods of falling interest rates, homeowners are more likely to refinance their mortgage loans. Refinancing allows homeowners to replace their existing mortgage with a new one that has a lower interest rate. This process accelerates prepayments because homeowners are paying off their old mortgage faster than originally planned. Prepayments are the early return of principal on a mortgage security. When prepayments accelerate, the average life of the mortgage-backed security (MBS) reduces. The average life of an MBS is the weighted-average time to the return of a dollar of principal, measured in years. When homeowners prepay their mortgages, the principal is returned sooner, reducing the average life of the MBS.

Public Securities Association (PSA) is a prepayment benchmark used in the mortgage-backed securities market to standardize prepayment assumptions. Describe the PSA model.

PSA prepayment benchmark assumes that the monthly prepayment rate for a mortgage pool increases as it ages (becomes seasoned). The PSA is expressed as a monthly series of Conditional Prepayment Rates (CPRs). The model assumes that:

CPR = 0.2% for the first month after origination, increasing by 0.2% every month up to 30 months; and

CPR = 6% for months 30 to 360

A mortgage pool whose prepayment speed (experience) is in line with the assumptions of the PSA model is said to be 100% PSA. Similarly, a pool whose prepayment experience is two times the CPR under the PSA model is said to be 200% PSA (or 200 PSA).

Consider a pool of mortgages that were issued exactly 16 months ago at an effective interest rate of 6% p.a(they are beginning the 17th month). What is the CPR, and what is the SMM assuming 150 PSA?

Assuming 100 PSA

CPR(month t | t ≤ 30) =6%×t/30

CPR(month 17) = 6%×16/30=3.2%

150 PSA implies that CPR (at the beginning of month 17) = 1.5×3.2%=4.8%

SMM = 1–(1–CPR)1/12=1–(1–0.048)1/12=0.409%

What type of loans are securitized through the Federal National Mortgage Association?

Agency loans, also known as conforming loans, are typically residential loans that are securitized through entities like the Federal National Mortgage Association (FNMA), Government National Mortgage Association (GNMA), and Federal Home Loan Mortgage Corporation (FHLMC).

These loans conform to the guidelines set by these government-sponsored entities (GSEs).

The GSEs buy these loans from lenders, package them into mortgage-backed securities (MBS), and guarantee the timely payment of principal and interest to the MBS investors. This process helps to provide liquidity to the mortgage market, enabling lenders to make more loans. The FNMA, commonly known as Fannie Mae, is one of the leading agencies in this process.

Suppose that an investor owns a pass-through security with an initial principal of $500 million. The remaining mortgage balance at the beginning of a certain month is $400 million. Assuming that the SMM is 0.4125% and the scheduled principal payment is $5 million, the estimated prepayment for the month is:

$1.63M

We only take into account the remaining mortgage balance, not the initial amount of principal.

=0.4125%($400m−$5m)=$1,629,375

GrossHaus Investment Bank is one of the largest mortgage financiers in Germany, holding over 38% of the market share in residential and commercial property lending. In addition to its mortgage lending business, GrossHaus also securitizes mortgage loans and issues structured securities to investors. Robin Frazer recently purchased a mortgage-backed security from GrossHaus that entitles him to receive only the principal portion of the cash flows from a pool of mortgage loans. Which of the following best describes the type of security Frazer has purchased?

A strip.

A strip is a type of security that allows an investor to separately purchase the principal portion and interest portion of the mortgage payments on a mortgage pool. In the context of the question, Robin Frazer has purchased a principal-only strip (PO) from GrossHaus Investment Bank. These PO strips are typically sold at a discount and increase in size over time as the principal component of the mortgage grows. This is in contrast to interest-only (IO) strips, which decrease in size over time as the principal due on the mortgage decreases.

Mortgage-backed securities (MBS) are investment products that are backed by a pool of mortgages, where investors receive payments based on the interest and principal payments from the underlying mortgages. Investors in MBS need to consider various risks such as interest rate risk, credit risk ,prepayment and contraction risk. What is contraction risk?

Contraction risk is the risk related to the decrease in the expected life of a mortgage pool due to falling interest rates and higher prepayment rates. In contrast, extension risk is the risk related to the increase in the expected life of a mortgage pool due to increasing interest rates and lower prepayment rates.

Billy Clark is an investment manager at the Sachsenhausen Investment Bank based in Dusseldorf. Clark manages a pool of mortgages and the assets constructed with the pool. If the pool prepaid 1.1% of its principal above its amortizing principal as the percentage of total outstanding principal in the month of February, then which of the following is the appropriate annualized constant prepayment rate he can come up with?

If the pool prepaid 1.1% of its principal above its amortizing principal as the percentage of total outstanding principal in the month, then its single monthly mortality rate or SMM is 1.1%.

Constant prepayment rate or CPRCPR=1−(1−SMM)^12=

1−(1−0.011)^12=0.1243

Kevin Rodriguez is a candidate for the position of a junior trader at a mid-sized investment bank in Mexico. The bank’s hiring process is rigid, consisting of 1 written exam and 2 interviews. Rodriguez has cleared the written exam and is currently being interviewed by the recruitment committee. The committee asked Kevin to describe the situation where an investor can make a risk-free profit on a forward contract. Kevin presented the following two scenarios:

I. If the forward price of the stock is greater than the current price, the investor can profit by purchasing shares at the current price and shorting shares at the forward price.

II. If the current price of the stock is greater than the forward price, the investor can profit by purchasing shares at the current price and shorting shares at the forward price.

Assuming that the forward price being considered differs from the forward price implied by the spot price and the current interest rate, which of the above-mentioned scenarios will generate profit?

Scenario I will generate a profit, and scenario II will generate a loss

This is because in Scenario I, if the forward price of the stock is higher than the current price, the investor can borrow funds at the risk-free rate to buy shares at the current price and short forward contracts to sell the asset at the higher forward price. This strategy allows the investor to earn a risk-free return. The investor is essentially locking in a higher selling price for the shares in the future, which, if the shares are bought at a lower price now, will result in a profit.

Scenario II will generate a loss. If the current price of a stock is higher than the forward price, the investor would need to short the shares now, invest the proceeds at the risk-free rate, and use the proceeds to take a long position in the forward contract. However, this strategy would not result in a profit because the investor would be buying high (current price) and selling low (forward price), which is the opposite of the profit-making strategy of buying low and selling high.

Ellen Harper, a portfolio manager at Deutsch Investments Group (DIG), is considering investing in the 6-months futures contract on the German DAX-30 index. The DAX-30 is currently valued at 12,240 with a dividend yield of 1.7% per year. If the risk-free rate in Germany is 3.2% (compounded annually), then the price of the futures contract should be:

12,330

Long positions in futures contracts are more desirable to forward contracts when the correlation between futures prices and interest rates is:

Positive

When the correlation between interest rates and futures prices is positive, futures contracts are more desirable to holders of long positions than forward contracts. This is because rising prices will lead to futures profits that are reinvested in periods of rising interest rates and falling prices will lead to losses that occur during periods of falling interest rates. Therefore, it is far better to receive cash flows in the interim than the expiration under such conditions. This is due to the fact that futures contracts are marked to market daily, meaning that gains and losses are realized and can be reinvested daily. This allows the holder of a long futures contract to potentially earn interest on their gains, which can be particularly beneficial in a rising interest rate environment.

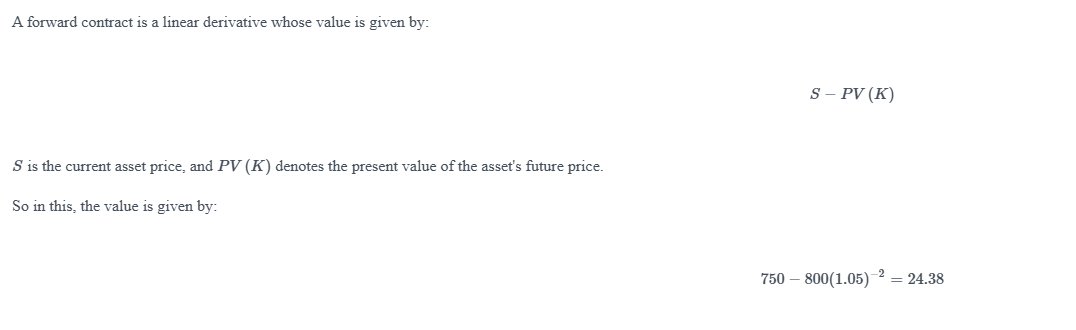

An investor considers investing in a forward contract to buy an asset currently valued at USD 750 for USD 800 in 2 years. Given that the current interest rate is 5% with annual compounding, what is the current value of the forward contract?

24.38

Paul enters into a two-year forward contract on a stock that pays no dividends and that the current stock price is USD 33 and the annually-compounded risk-free rate is 5% per year. Suppose that one year after the forward contract was initiated, the spot price is USD 35, and the risk-free rate has changed to 6% per annum.

What is the value of this forward contract?

0.68

The forward price, initially when the contract is initiated, is given by:

K=S(1+R)^T

=33(1.05)^2=$36.38

After one-year, the forward price is given by:

F=S(1+R)^T

=35(1.06)^1=$37.10

The value of the forward contract is

(37.10−36.38)/1.06^1 = 0.6792≈0.68

When there is a negative correlation between return on assets and interest rates, the forward price will be greater than the futures price. True or False?

True - The forward price is greater than the futures price. This is because when there is a negative correlation between return on assets and interest rates, it implies that when the price of an asset rises, funds are typically invested at a lower rate. This is due to the daily settlement of futures contracts, which can lead to a lower futures price compared to the forward price in a negatively correlated environment. Therefore, in a situation where there is a negative correlation between return on assets and interest rates, one would expect the forward price to be greater than the futures price.

Commodities futures markets consist of hundreds of different commodities with different properties and attributes. Some commodities do not consider the storage costs separately because, in those commodities, the forward price of the commodity compensates the commodity owner for the cost of storage. Such commodity markets are referred to as:

Carry markets - The term 'carry' in financial markets refers to the cost of holding a financial instrument or commodity. In the context of commodities, a commodity is said to be in 'carry' when it is being stored rather than being traded. This concept is akin to the financial cost of carry in financial markets.

Commodities can be classified based on various criteria such as extractable or renewable, primary or secondary, hard or soft, etc. Name a commodity that can be classified as renewable as well as a primary commodity?

Livestock is a renewable and primary commodity.

Renewable commodities are those that can be replenished over time through natural processes. Primary commodities, on the other hand, are commodities that are traded in their raw, unprocessed form.

Describe the steps in a reverse cash and carry

Reverse cash-and-carry arbitrage strategy involves 1) short selling the commodity 2) lending the proceeds from the short sale at market interest rates for the duration of the forward or futures contract, and 3) taking a long position in the futures contract at the market price.

Ahmet Abdullah is a research analyst at Klosky Investment Company. He is interested in analyzing the forward price curve trend of silver prices. Due to a lack of trading, he is unable to get the forward prices for silver. However, he found out that there is an established lending market for silver and the silver lease rate is 7.9%. If the risk-free rate is 8.2%, describe the state of the market.

The market for silver is said to be in contango.

The relationship between the forward and spot prices of a commodity can be expressed using the formula: F = Se^(r - l)T, where F is the forward price, S is the spot price, r is the risk-free rate, l is the lease rate, and T is the time to maturity. In this scenario, given that the risk-free rate (8.2%) is higher than the lease rate (7.9%), the forward prices will be greater than the spot prices, suggesting that the market for silver is in contango.

The spot price of oil is USD 95 per barrel, and the six-month futures price is USD 100 per barrel. The cost of storing oil for six months has a present value of USD 10 per barrel, and the risk-free rate is 5% per year, compounded annually.

Determine the convenience yield, Y.

Duration is a key measure of a bond’s price sensitivity to interest rate changes; for zero-coupon bonds, duration equals time to maturity. All else being equal, what is the impact of time to maturity on duration?

All else being equal, a bond with a longer time to maturity will have a higher duration and thus exhibit greater price volatility for a given change in yield. Price changes due to yield shifts are nonlinear—this is known as convexity; longer-maturity zero-coupon bonds exhibit more convexity, amplifying their price response to rate cuts.

0.045