ACC20021: Mangement Accounting

1/54

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

55 Terms

What is Management Accounting?

Forward-looking processes and techniques that are focused on the effective and efficient use of organisational resources to support managers in enhancing both short-term and long-term customer value and shareholder value (i.e, planning, decision-making)

Effectiveness

Achieving the most favourable results, goals and targets

Efficiency

Using minimum resources to achieve desired targets

Resources

These can be financial and non-financial, can also be considered as the organisation’s capabilities and competencies

Customer Value

The value that a customer places on a particular feature of a product

Shareholder Value

Improving the business’s value from the shareholders’ perspective

Corporate Strategy

Deciding what kinds of businesses an organisation should own or be involved in. These decisions are made at the overall organisation level and focus on which industries or markets to operate in (i.e, Wesfarmers owns several well-known businesses, therefore buying/selling new/existing businesses are part of its corporate strategy)

Business Strategy

Refers to how each individual business competes with others in its market. A business has a competitive advantage when it does something that competitors find hard to copy (i.e, Aldi keeps costs low by using simple store designs and limited product ranges to reduce expenses, Apple offers higher quality, innovation, or better customer service)

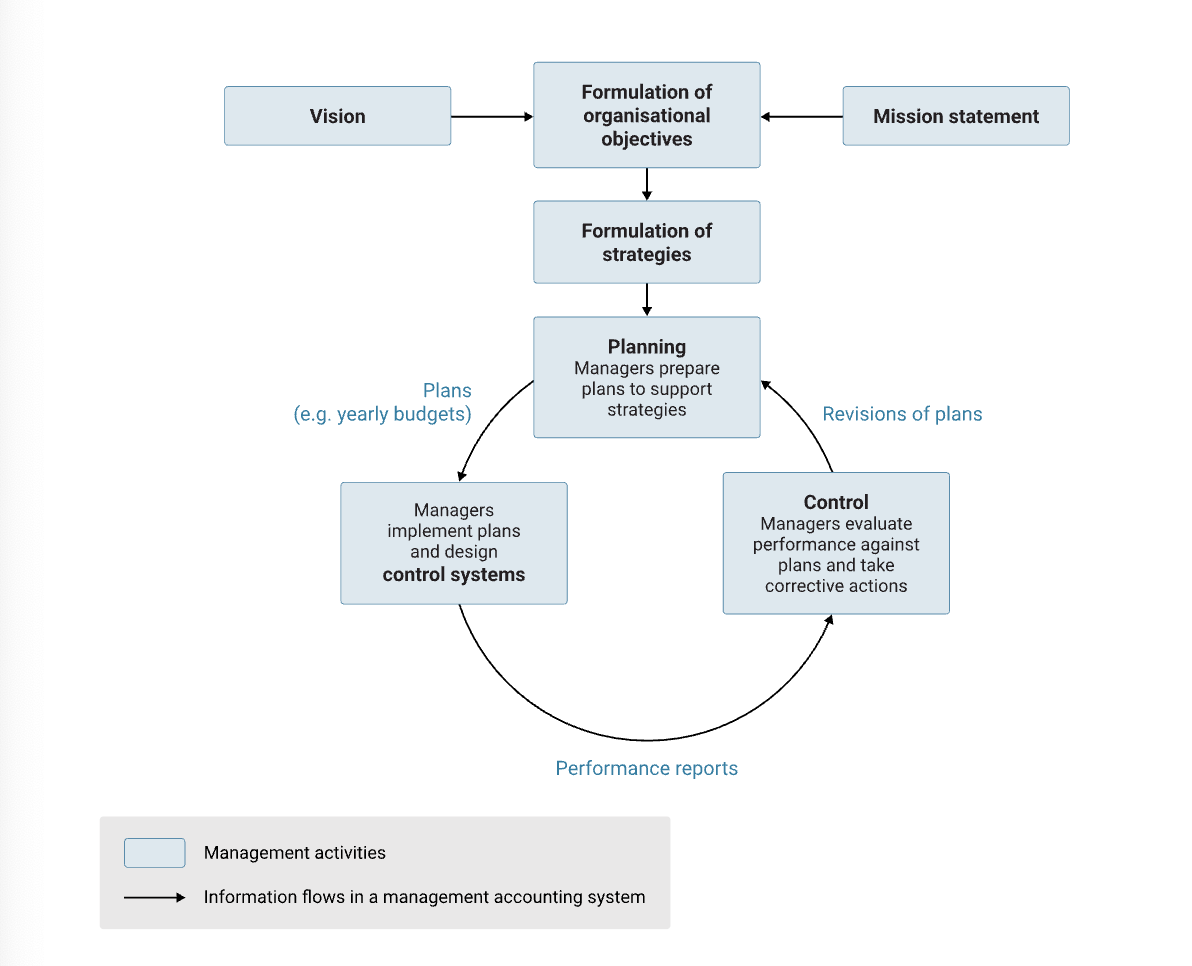

Visualise the ‘Management Accounting Planning and Control Systems’ graph

What are a few important considerations highlighted by the ‘Management Accounting Systems’ graph?

Behavioural and motivaional impacts, costs and benefits of information, and contingency and institutional influences

What is cost classification?

The process of grouping costs based on how the information will be used (i.e, a cost that is useful for one decision may be less useful for another if it is not classified appropriately). Accurate and appropriate cost classification allows managers to assess whether resources are being used efficiently and whether improvements can be made without undermining value creatio

If the purpose is to analyse the costs of goods sold, what would the cost classification be?

Manufacturing or product costs such as direct material, direct labour, and manufacturing overhead

If the purpose is to assess production manager performance, what would the cost classification be?

Controllability options such as controllable and uncontrollable

If the purpose is to plan or budget costs, what would the cost classification be?

Behaviour classifications such as fixed and variable

Variable Costs

Costs that change in direct proportion to changes in the level of activity (cost driver)

Fixed Costs

Costs that remain unchanged in total despite changes in the level of activity

Direct Costs

Costs that can be traced to a particular cost object (i.e, direct labour, raw materials)

Indirect Costs

Costs that cannot be traced to the cost object (i.e, rent)

What are the three components of manufacturing costs (costs incurred within the factory area)?

Direct material, direct labour and manufacturing overhead

Direct Material

Prime costs that are consumed in the manufacturing process and can be traced to products

Direct Labour

Conversion costs such as wages and labour on-costs for personnel who work directly on the manufactured product

Manufacturing Overhead

All manufacturing costs other than direct manterial and labour costs, including the cost of indirect materials and labour (i.e, glue, paint)

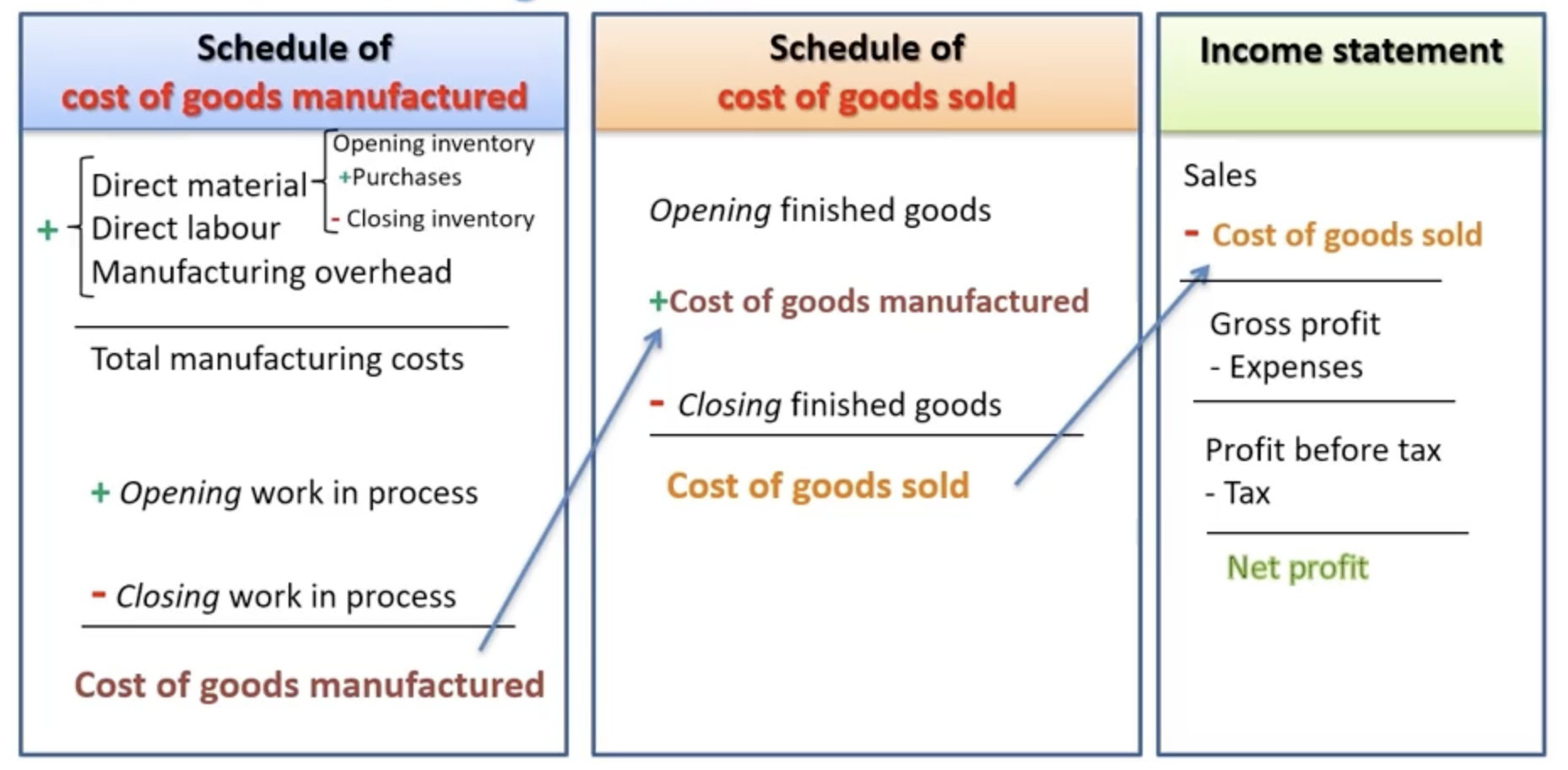

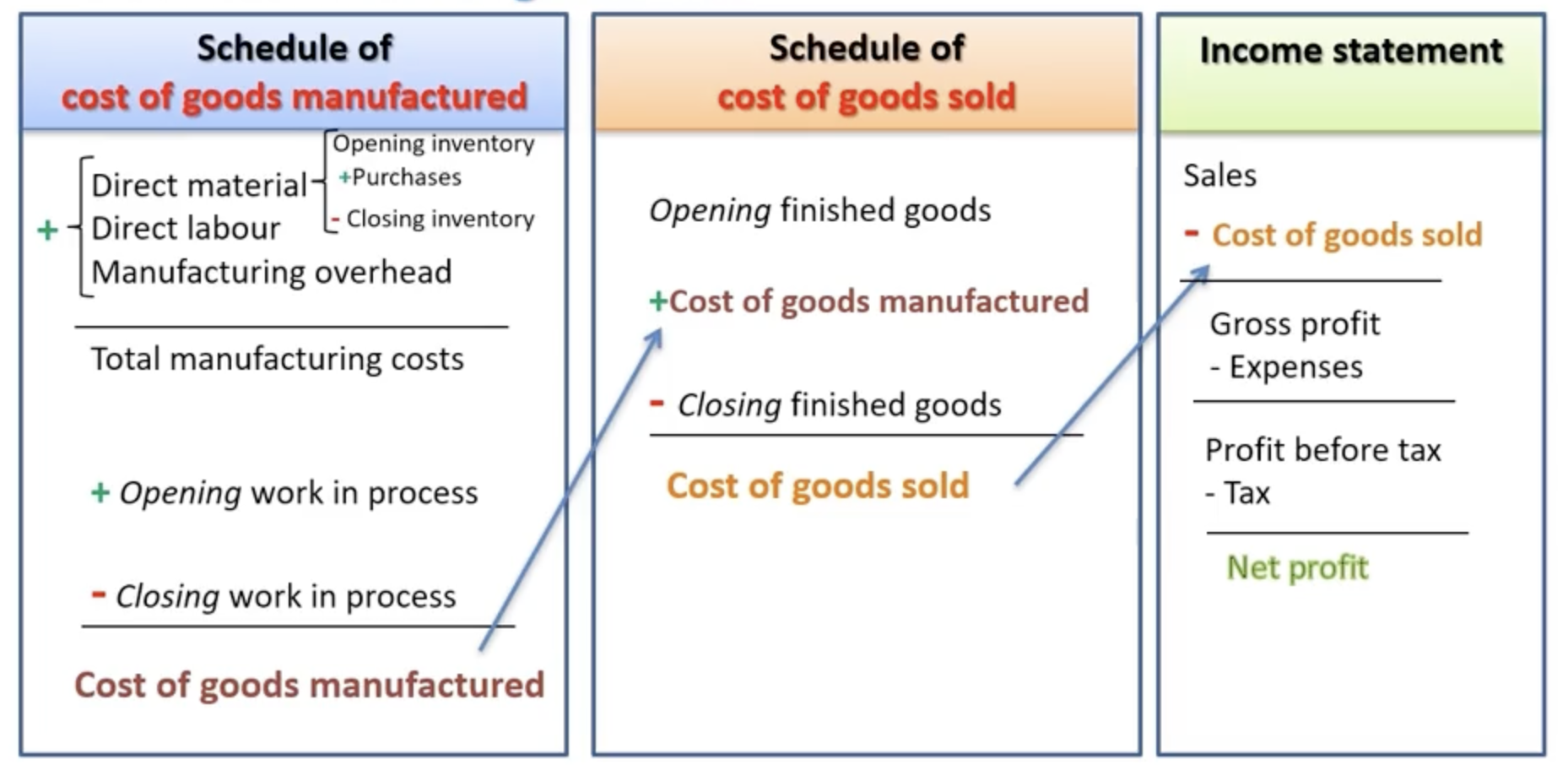

How do you calculate ‘Cost of Goods Manufactured’ (CGM)

= (Direct material + Direct labour + Manufacturing overhead + Opening WIPs) - Closing WIPs

How do you calculate ‘Cost of Goods Solds’ (CGS)

= (Opening Finished Goods + CGM) - Closing Finished Goods

Describe the order in which manufacturing costs flow through inventory accounts

Manufacturing costs flow from raw materials inventory to work in process inventory and then to finished goods inventory as production progresses

Explain when manufacturing costs are recognised as an expense in the income statement

Manufacturing costs are recognised as an expense when finished goods are sold and the cost of those goods is transferred to cost of goods sold

Explain why manufacturing businesses prepare a schedule of cost of goods manufactured and a schedule of cost of goods sold

The schedules summarise how manufacturing costs move through inventories during the period and provide the information needed to calculate cost of goods sold and link production activity to the income statement

When analysing cost behaviour, what do we mean by ‘level of activity’?

When analysing cost behaviour, the ‘line of activity’ refers to the level of work performed in the organisation. The movement causes the cost—for this reason, the activity level is often referred to as the cost driver level. Activity can be expressed in many ways, including units produced, number of machine hours, number of direct labour hours, etc

Briefly describe the key differences between financial accounting and management accounting

Management accounting information is provided to managers and employees, whereas financial accounting information is provided to interested parties outside the organisation

Management accounting reports are unregulated, whereas financial accounting reports are legally required and must conform to Australian accounting standards and corporate law

Management accounting reports often focus on sub-units within the organisation, the data may be subjective, and there is a strong emphasis on reporting relevant and timely information. Financial accounting reports focus on the enterprise in its entirety, are based almost exclusively on verifiable transaction data, and the focus is often on reliability rather than relevance

Focusing on a Compaq notebook, provide examples of costs classified under the three main product cost components

The cost of the components assembled to make the notebook would be classified as direct material

The wages of the workers who assemble the notebook would constitute a direct labour cost

The heating and lighting of the assembly area would be part of the overhead manufacturing cost

Formula for Predetermined Overhead Rate

Formula for Activity Cost Per Unit

Formula for Set-Up Costs

Explain the relationships between cost estimation, cost behaviour and cost prediction

The relationship between cost estimation, cost behavior, and cost prediction is that they are all essential components of effective cost management and decision-making in a business.

Understanding cost behavior is crucial for cost estimation because it helps determine how costs will change with changes in business activity or output.

Cost estimation is necessary for cost prediction because it provides the basis for forecasting future costs.

Cost prediction relies on understanding cost behavior to accurately forecast how costs will change in the future.

In summary, these three concepts are interrelated and all are crucial for effective cost management and decision-making in a business.

Describe the concept of unit-level costs

Occurs everytime a service is performed or a product is made, i.e direct materials, labour, machine maintenance

Describe the concept of batch-level costs

Expenses related to a group of products or services that cannot be readily traced back to an individual item, i.e, production lines, machinery, equipment or costs related to quality

Explain the concept of cost-drivers

Cost-drivers are a factor or activity that causes a cost to be incurred and helps identify what causes a cost to change. There are three perspectives used to understand how costs are driven by activity

Simple view: Assumes that costs are driven mainly by production or sales volume. This view is straightforward to apply, but can oversimplify cost behaviour

Realistic view: Many costs are driven by specific activities rather than volume alone. Under this view, non-volume-based cost drivers are required to better explain cost behaviour

Modern view: Costs are incurred at different levels of activity within an organisation, such as unit-, batch-, product-, and facility-level activities. This perspective underpins more refined approaches to cost analysis

What are volume-based cost drivers?

Costs driven primarily by production or sales volume, i.e, measured by units produced/sold

What are non-volume-based cost drivers?

Costs driven by activities such as setting up equipment, processing batches, handling deliveries, or providing support services. This helps to explain why costs can change even when production volume remains constant

What is cost estimation?

Cost estimation is the process of determining the cost of a particular activity or operation. It involves the use of various techniques and methodologies (e.g, high-low method, regression analysis) to predict the costs associated with a project or a business operation.

i.e, a company might use historical data, industry benchmarks, or mathematical models to estimate the cost of producing a new product

What is cost prediction?

Cost prediction is the process of forecasting future costs based on current and historical cost data, as well as an understanding of cost behavior.

i.e, if a company knows that its variable costs are $5 per unit and it plans to produce 1,000 units next month, it can predict that its total variable costs will be $5,000

What is cost behaviour?

Cost behavior refers to how costs change as the level of business activity or volume of output changes. Costs can be classified into three main categories based on their behavior:

Fixed costs

Variable costs

Mixed costs

What is the Cost-Volume-Profit (CVP) Equation?

Profit = Revenue – Costs

How is revenue calculated?

Revenue = Retail Price x Number of Units

How do you calculate the break-even point in sales units?

Break-even (units) = overhead expenses ÷ (unit selling price − unit cost to produce)

How do you calculate the contribution margin ratio?

(Revenue - Variable Costs) / Revenue

How do you calculate margin of safety relating to target sales?

(Current sales - Break-even sales) ÷ Current sales to determine what percentage your sales can drop before reaching break-even

What is the margin of safety relating to target sales?

The margin of safety is the difference between actual sales and the break even point

What is the role of product costing systems?

Product costing systems gather, track, and assign direct and indirect expenses to goods or services. Their primary role is to provide accurate unit cost data to for pricing decisions, inventory valuation, profitability analysis, and cost control (allocating overhead costs in a systematic way)

Why do managers need different measures of product costs for different purposes?

Because no single cost figure can accurately serve all decision-making needs. Different business scenarios require distinct cost concepts to ensure profitability, accurate pricing, and effective operational control.

i.e, a company may require one system for estimating future products (e.g. for quoting and tendering for jobs) and a separate system for strategic decision-making, particularly for longer-term decisions.

How do you use job costing to estimate product costs? What is the procedure?

Job costing estimates the cost of a unique product or batch by breaking expenses into three distinct categories: materials, labor, and overhead

How do you prepare journal entries to record costs under a job costing system?

How is inventory valued for external financial reporting?

What is a service organisation? What are their features?

Name 3 difference between service organisations and manufacturers.