8.24 - Experience & Endowment effect

1/14

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

15 Terms

ST vs Endowment effect

ST - Subject should have same choice always if feasible set the same

Endowment effect - People more attached to things they already ‘have’

Knetsch (1989) recap

3 groups

2 Groups given mug or chocolate bar and allowed to swap

Other group had choice of either (no endowment)

ST predicts proportion who end with mug should be consistent in all groups as feasible set the same in all groups

apart from random sampling variation

Evidence shows Endowment effect (90% of initial E vs ~50% in choice group)

Why introduce a market to test Endowment effect

Knetsch (1989) results could be from weak lure of endowment that ‘tie-breaks’ if nearly indifferent

Only if many are indifferent between M / C

Choices in real life often money vs good (not good vs good)

EE might not survive if “keeping the endowment” is “giving up money”

i.e. not selling

Kahneman et al (1990) - OV

Look at their experiment 1

11 rounds of market exchange involving different goods - repeated market context

Induced value tokens + mugs + pens

Can test for endowment effect for relevant good in each round

Can test for survival of endowment effect in later rounds after earlier experience

Design

Each round 50% of subjects endowed with 1 unit of good

These subjects asked for a range of prices if they would sell at that price

Other subjects asked if would buy at these prices

Given responses experimenter selects price to match S & D - market price

Subjects then trade if they said they would

Innovative method at the time but not best practice now

small samples + experiment in class

Kahneman et al (1990) - Theory

ST

Call the 50% who like the good most ‘likers’ + others ‘haters’

If subject a Liker or Hater shouldn’t be affected by endowment

Regardless of endowment, after trading those holding the good should he those who want the good - Coasian insight

Random allocation of subjects means Endowed group comprises 50%

Likers and 50% Haters

Therefore endowed haters will trade to non likers but endowmed likers wont

Volume of trade should be 50% (those endowed but haters)

Endowment effect

Fewer that 50% of units traded

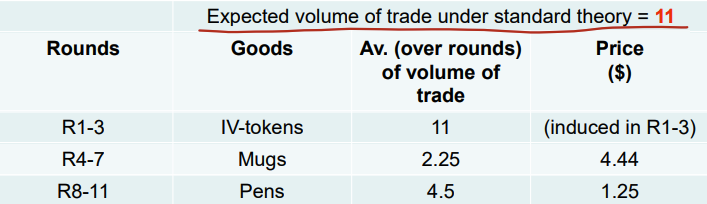

Kahneman et al (1990) - Induced value tokens

Tokens have no intrinsic value

value induced by willingness of experimenter to buy them for cash at end of experiment - only value from disposal

Induced values can be varied by subject

Experimenters can induce distributions of willingness to sell/buy at different prices, creating Likers and Haters

For Mugs / pens value is from subjects own preferences

more chance good kept

Kahneman et al (1990) - RESULTS

No EE for induced value tokens - ST holds

Volume of trade much lower that ST for M/P

EE persists over all rounds

EE only for goods people expect to keep

List (2003) - OV

Sports trading cards field experiment - 2 different goods (small market for both goods)

test for EE in setting that:

Feels natural to participants - Sports memorabilia marketplace

Offers much of control that lab offers

Has measurable variation in participants’ prior market experience

Wide variation in trading experience - dealers make more trades + 80% male + avg age = 36

List (2003) - Design

On entering show (or, for dealers, at their stalls), subjects asked if would fill out survey about participation in similar events

Information on prior trading experience

In return for agreeing,, subject immediately given either good A or good B

Pseudo-random allocation, based on clock

After completing survey, the other good is shown and subject given chance to swap

List (2003) - Theory

ST

same feasible set so preference should vary with which card given 1st

swap rate should be ½ (indpendent of proportion preferring either)

prefer A = p prefer B = 1- p → avg swap rate = (1-p+p)/2 = ½

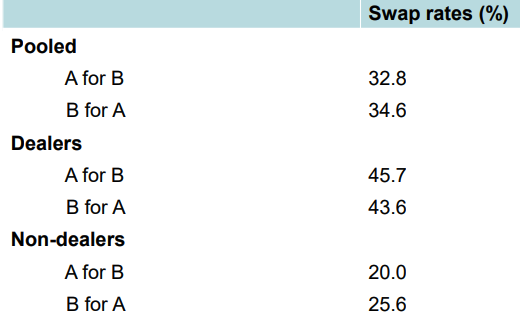

List (2003) - RESULTS

Swap rates higher for dealers - not sig different from 50%

Non-dealers show EE (BUT experience non-dealers also have 50% swap rate)

Experience shown to push preferences towards ST

Increasing Trades per month → less EE

EE found outside lab with non-students

List (2003) - Caveats

Resale - dealers + high-volume traders may never intend to keep good

EE not expected to hold

Good-specificity - Participants have specialised interest in unusual goods

does this trading experience erode EE in other contexts or just sports trading

Reverse causality - Does trading experience / dealership erode endowment effect or do people with weak endowment effects select into dealership / trade a lot

List (2004) - OV & results

Uses Mugs & candy in same trading market-place

addresses resale + good-specificity issues

Results

No EE for dealers or high-volume traders

Strong EE for non dealers (aggregate + low-volume traders)

List (2011) - OV & results

Focuses on group who will commit to come back again to sports trading place

reduces observations

Treated group get additional gift of multiple pieces of memorabilia

may increase their trading between events

Test EE between treated & untreated groups

RESULTS

Some evidence that gifts (induced extra trading experience) weaken subsequent EE

Causality of trading experience causing reduced EE

Although sample size very small

Critique of List’s approach

The market consumers have an extremely specialised interest - does external validity improve from normal set of students?

market experience is of a particular kind - dealers trade on both sides of the market

being a dealer is uncommon

Experience highlighted role (dealer vs non-dealer) + extent of experience (intensity - volume of trades)