ch 2: calculation of income tax

1/21

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

22 Terms

What is income tax liability?

Total tax due on taxable income.

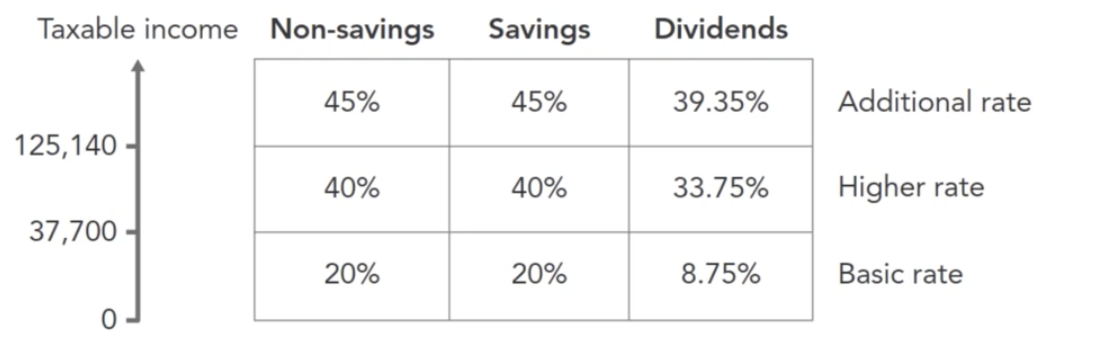

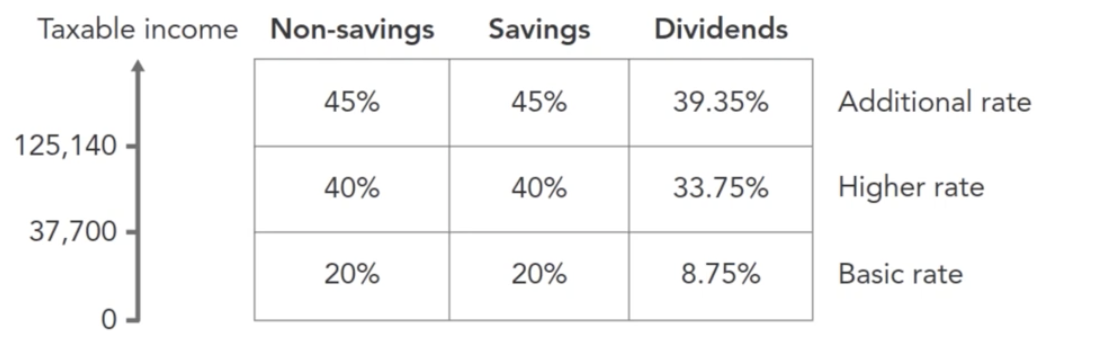

Order income is taxed?

Non-savings

Savings

Dividends

Basic rate band?

£0 – £37,700

Higher rate band?

£37,701 – £125,140

Additional rate band?

Over £125,140

What is Personal Savings Allowance (PSA)?

Savings taxed at 0%

PSA ratess:

basic -

higher -

additional -

£1,000

500

0

If savings = £11,200 and PSA = £1,000 → taxable?

£10,200 taxed

Does additional rate taxpayer get PSA?

no

What extends basic rate band?

Gross Gift Aid

personal pension contributions

How to gross up Gift Aid?

× 100/80

£8,000 donation → gross?

£10,000

What happens when band is extended?

More income taxed at basic rate → less at higher rate

Gift Aid vs payroll giving?

Gift Aid → extend bands

Payroll giving → reduce income directly

dividend allowance

an amount of dividend income that is taxed at 0%. This is £500 for all taxpayers.

payments made to charity via payroll deduction or pension contributions made to an occupational scheme are simply deducted from ____

salary

gift aid donations and personal pension contributions are paid ___ of basic rate (___%) tax.

extend the basic rate band by the ____ amount of any gift ad donation/and or personal pension contributions paid by the taxpayer. this gives further tax relief to _____ and _____ rate taxpayers

net

20

gross

higher

additional

You always tax taxable income, not ANI.

ANI → affects allowances

Taxable income → what you tax

Gift Aid/pension → extend bands, not reduce income

You always tax taxable income, not ANI.

ANI → affects allowances

Taxable income → what you tax

Gift Aid/pension → extend bands, not reduce income

Dean and Barry are civil partners. Dean is a higher rate taxpayer and Barry is a basic rate taxpayer. They each have savings that yield interest in excess of £1,500 per annum.

Which one of the following options is not a valid method of reducing the total tax payable by Dean and Barry?

dean should make payments into a personal pension

barry should invest some of his savings in an ISA

barry should make payments into a personal pension

dean should transfer some of his savings to barry

barry should make payments into a personal pension

If Dean makes payments into a personal pension it will extend his basic rate band and he will pay less tax at the higher rate.

If Barry invests some of his savings in an ISA he will reduce his taxable interest.

If Dean transfers some of his savings to Barry some of his interest that would have been taxed at 40% will now be taxed at 20%.

If Barry invests in a personal pension the extension of the basic rate band will have no impact on his tax payable as he is a basic rate taxpayer.

bank and building interest is paid ___ to individuals

gross

reduction in tax payable calculation

pension payments x (40% - 20%)