Mod. 4 Choosing Projects & Investment Decision Rules

1/19

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

20 Terms

mutually exclusive projects

when you must choose only one project among several possible projects

NPV rule: select the project with the highest NPV

IRR rule: selecting the project with the highest IRR may lead to mistakes

Net Present Value (NPV)

rule: take the project with the highest NPV

PV benefits - PV costs =

NPV rule: net profit created by project, is a $ (dollar) amount

Internal Rate of Return (IRR)

NPV = 0 → PV benefits - PV costs

take any investment where this exceeds the cost of capital

turn down any investment where this is less than the cost of capital

is a % return on the project (% at full recovery of the project based on spending)

payback rule

the sense of time, how long it takes to recover from all the costs of the project

ranges from short term to a few decades

amount of time it takes to recover or pay back the initial investment.

•If the payback period is less than a pre-specified length of time, you accept the project.

•Otherwise, you reject the project.

•The payback rule is used by many companies because of its simplicity.

Perpetual Project

if the project lasts forever, how to solve?

CANNOT use financial calculator

need to use PV of a perpetuity: C / r

NPV = (Cash flow / return) - cost of project (the PV)

NPV is dependent on the discount rate (cost of capital)

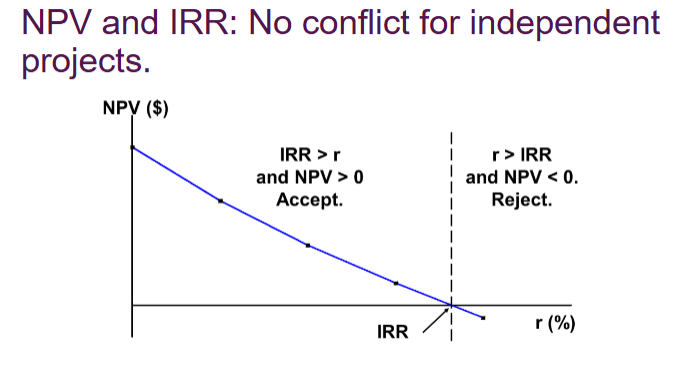

NPV v. IRR rules

• The IRR Investment Rule will give the same answer as the NPV rule

in many, but not all situations.

• In general, the IRR rule works for a stand-alone project if all of the

project’s negative cash flows precede its positive cash flows.

• In other cases, the IRR rule may disagree with the NPV rule and

thus be incorrect.

• Situations where the IRR rule and NPV rule may be in conflict:

• Delayed Investments

• Nonexistent IRR

• Multiple IRRs

Project Choice

take when r < IRR and NPV > 0

Reject project when r > IRR and NPV < 0

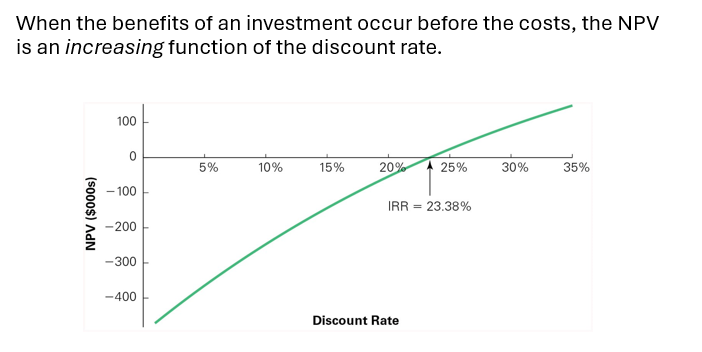

Delayed Investments (example)

•Assume you have just retired as the C E O of a successful company. A major publisher has offered you a book deal. The publisher will pay you $1 million upfront if you agree to write a book about your experiences. You estimate that it will take three years to write the book. The time you spend writing will cause you to give up speaking engagements amounting to $500,000 per year. You estimate your opportunity cost to be 10%.

Pitfall #1 of IRR

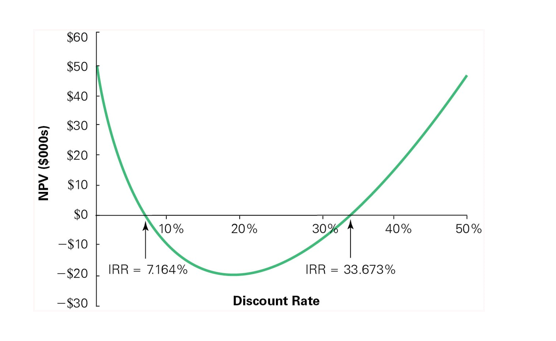

Multiple IRR’s (example)

•Suppose Star informs the publisher that it needs to sweeten the deal before he will accept it. The publisher offers $550,000 advance and $1,000,000 in four years when the book is published.

•Should he accept or reject the new offer?

pattern: +, -, -, -, + (has a sign change twice)

pitfall #2 of IRR

Noneexistent IRR

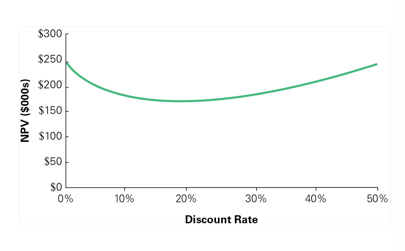

•Finally, Star is able to get the publisher to increase his advance to $750,000, in addition to the $1 million when the book is published in four years.

•No I R R exists.

Pitfall #3 of IRR

Project Choice Notes

When NPV and IRR disagree, always follow NPV

There is a disagreement due to upward curve (opposing recommendations)

shape of the curve decides whether NPV or IRR gives the same or opposing answers

cash flows impact the shape of the curve

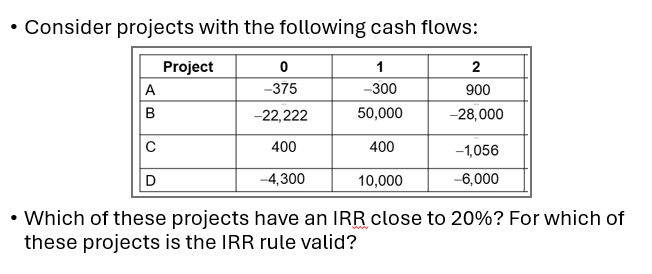

option A

A: cost is first, then benefits after

B: cash flow changes twice, U-shape = multiple IRR’s

C: cash flows change, + early on, - after = delayed investment

D: Cash flows change twice nonexistent IRR (only seen when graphed)

Paybacks strengths and weaknesses

•Strengths:

•Provides an indication of a project’s risk and liquidity.

•Easy to calculate and understand.

•Weaknesses:

•Ignores the TVM.

•Ignores CFs occurring after the payback period.

•No specification of acceptable payback.

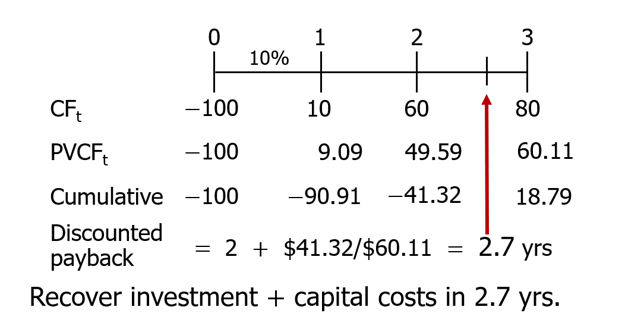

requires using discounted CF’s = find the PV of each cash flow then do the method

time value of money (requires finding discounted CF’s)

what does the payback rule violate?

Mutually Exclusive Projects

•When you must choose only one project among several possible projects, the choice is mutually exclusive.

•N P V Rule: pick the highest

•Select the project with the highest N P V

•I R R Rule: may lead to mistakes in choice

•Selecting the project with the highest I R R may lead to mistakes

IRR difference from NPV

Scale of investment

timing of cash flows

riskiness

Difference in Scale

•If a project’s size is doubled, its N P V will double. This is not the case with IRR.

•Thus, the IRR rule cannot be used to compare projects of different scales.

Timing of Cash flows

•the IRR can be affected by changing the timing of the cash flows, even when the scale is the same.

Difference in Risk

•not affected by the cost of capital (risk) while NPV is sensitive to the risk.

Profitability index

can be used to identify the optimal combination of projects to undertake

measures bank for buck

warning: multiple resource constraints, can be broken down completely

have to pay attention to the cost constraints of choosing a project