Corporate Finance

1/110

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

111 Terms

Sole Trader/Proprietorship:

No separate legal identity

Owner operated

Owner has unlimited liability

Profits taxed as personal income (pass-through)

Financed by owner’s access to capital

General Partnership:

No separate legal identity

Partners operated

Partners have unlimited liability

Profits taxed as personal income (pass-through)

Financed by partner’s access to capital

Limited Partnership:

No separate legal entity

General partner operated

GP has unlimited liability LPs have limited liability

Profits taxed as personal income (pass-through)

Financed by partners’ access to capital

Limited Liability Company:

Separate legal entity

Board and Management operated

Owners (shareholders) have limited liability

Profits taxed as personal income (pass-through)

Unbounded access to capital, unlimited business potential

There may be legal limits on number of owners, require a vote for transfer of ownership

Public Limited Company: coporation

Separate legal entity

Board and Management operated

Owners (shareholders) have limited liability

Profits taxed at corporate level (dividends taxed as

personal income)

No restrictions on ownership/transfer

Corporate Issuers

Corporations that raise capital in the financial markets are known as Corporate Issuers

Return on Equity

Net Income / Equity

Private Company:

Private Placements: Company raises capital from accredited investors

risks/terms outlined in private placement memorandum

Go Public : Initial Public Offering (IPO)

company raises capital from public

(private ➞ public) or direct listing : no new shares (no capital raised)

or SPAC : shell company raises capital via IPO then make an acquisition

[special purpose acquisition company]

or via acquisition

secondary offerings (secondaries) : Company raises capital from public

[secondary market: issued shares trade between market participants]

Public v. Private trends

many emerging economics have growing number of public

- high growth

- transition to open market structures

- foreign capital inflows

many developed economies have declining number of public

- mergers & acquisitions

- growing number of private capital sources

- preservation of ownership and control

limited parternership

2 level

one or more GP general partners operating the usiness and have unlimited liability.

but limited partners - only liable to the amount they invest(limited liability) dont invlove in appointing or removing GP.

GP have more profit distribution, taxed as personal income.

Free float

shares actively traded by investors

Shareholder Theory of Governance

- stakeholders only considered to the extent that they affect shareholder value

Stakeholder Theory of Governance

corporate governance should consider all

stakeholder interests

- ESG should be an explicit objective of the board

Primary Stakeholder Groups

Investors : shareholders , debtholders, Board of Directors

Board of Directors

Elected by shareholders to advance their interests

Independent Directors, Inside Directors

Inside Directors links to the company (includes founders and current, former manager.

Independent Directors - no material relationship with the company

- may better represent the interests of minority shareholders

Two-Tier Structure and Staggered Boards

Two-Tier Structure - separate supervisory board oversees board of directors

Independent Directors

Staggered Boards - groups elected separately in consecutive years

Limits the ability of shareholders to effect a major change of control

But, allows for continuity

Managers:

Led by CEO, determine and implement strategy and day-to-day operations

Stock based incentive plans align interests with shareholders

Employees:

Corporations rely on human capital of employees

May have equity via compensation, form unions to negotiate pay

Transition risk

Transition risks are losses related to the transition to a lower-carbon economy. An oil well may become a stranded asset due to government regulations or changes in consumer preferences that affect the price of oil or otherwise impair an issuer’s ability to fully realize the asset value. Physical risks include damage to property stemming from extreme weather, which is expected to increase in both frequency and severity due to climate change.`

Principal agent relationship

one part hires another to perform a task or service, can be present with or without a contract

conflicts - Shareholder v. Directors, Management

Information asymmetry reduces ability of shareholders to assess performance

increases with lower levels of institutional ownership, free float

Principal tool to align interests: compensation

But, interest may still diverge due to:

Insufficient Effort - Unable, unwilling to make investments, manage costs, make hard decisions

Too little monitoring of employees/controls ➞ Risks and Litigation

Too little time due to outside interests

Inappropriate Risk Appetite - Stock grants, options ➞ excessive risk taking

No stock grants, options ➞ risk-averse decision making

(Stockholder’s diversified portfolios increase risk tolerance)

Empire Building - Compensation tied to business size ➞ too many acquisitions

Entrenchment - Play it safe ➞ copy competitors, avoid risks, avoid speaking out

Self Dealing - Exploit firm resources ➞ perquisites (private planes, memberships etc.)

Smaller stakes, less cost to bear for management

Conflicts

Controlling v. Minority Shareholders

Dispersed Ownership: Many shareholders, none with control

Concentrated Ownership: Individual shareholder or group who can exercise control

= Controlling shareholders - can be a family, other companies,

Example Conflicts: Controlling shareholder: Founding family seeking diversification

Minority shareholders: Hold diversified portfolios - focus on max s/h value

Controlling shareholder: Long-term shareholder - multi-decade perspective

Minority shareholders: Seeking quicks gains via asset sales, cost cutting

Voting Schemes

Dual-Class Structure:

Class A: one vote per share, publicly held and traded

Class B: several votes per share, held by company insiders/founders

Corporate Reporting and Transparency

External stakeholders rely on corporate reporting for information on performance and

position investors rely on corporate reports to:

Assess company performance and that of its directors/management

Make valuation and investment decisions

Vote on key corporate matters or changes

Ensure compliance with legal commitments in debt contracts (via trustee)

Shareholder Meetings : Annual General Meeting (AGM)

discuss board elections, auditor appt., approval of F/S,

dividends, director and auditor compensation, equity based

compensation plans, “say-on-pay” non-binding votes on

compensation plans

Extraordinary General Meetings (EGMs)

called when resolutions requiring shareholder approval

proposed or by request by a specified minimum number/%

shareholders

special election, mergers, voluntary liquidation

Shareholder Activism:

Investor strategies to compel a company to act in a desired manner

Aim is to rapidly increase shareholder value

or - Social, Political, Environmental Considerations

Hedge Funds are among the predominant shareholder activists

Fees are based on Returns, able to fund large positions with

leverage (unlike ‘Regulated’ investment entities)

e.g. Encourage corporation to focus on what it does well

Encourage restructuring, replacement of management

Shareholder Litigation:

Activists may pursue ‘shareholder derivative lawsuits’

s/h acting on behalf of Co. in place of directors/management

who have failed to adequately act for the benefit of the company

Laws restrict s/h taking legal action in some countries

minimum thresholds or prohibition

Corporate Takeovers:

Proxy Contest/Fight: Group seeking controlling position persuades

other shareholders to vote for group

Tender Offers: Invitation to existing s/h to sell to group

gain control of board, and hence mgmt.

Hostile Takeover: Attempt to acquire a company without the

consent of its management

Contests for control attract arbitrageurs and takeover specialists

Purchase shares from existing s/h, sell to highest bidder

Bond Indenture

Legal contract that describes the structure of the bond, the

obligations of the company, the rights of the bondholders

Terms and Conditions may - Require certain actions

- Prohibit certain actions

- Require assets to be pledged

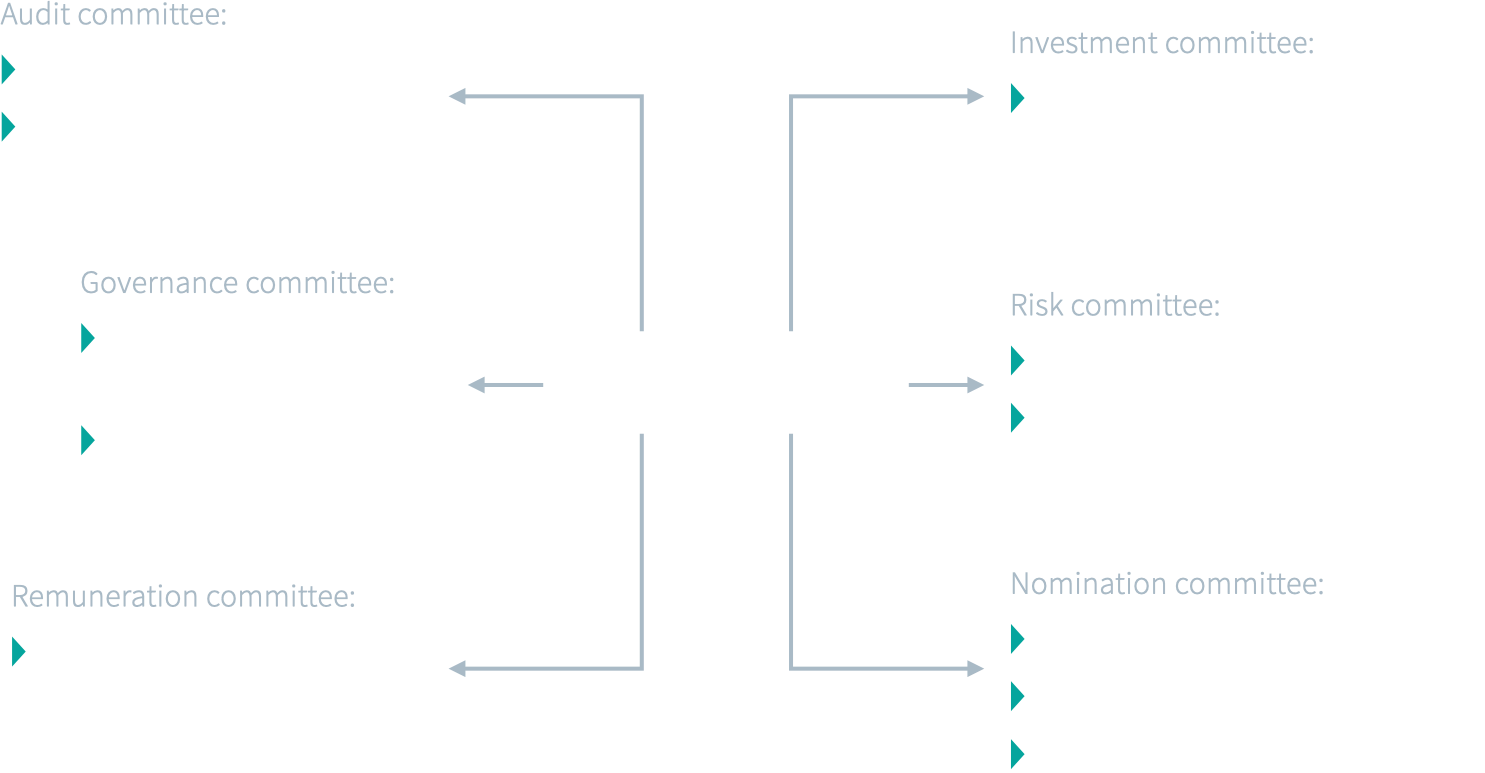

Board of Directors

[Specific functions delegated to committees, responsibility is not delegated]

audit committee - f financial/ac expertise

monitors financial reporiting process

supervises internal audit

recommends external auditor

proposes remedial actions based on reports

may oversee IT security

Nominating/Governance commitee

Typically independent members

appraises director and manger candidates

oversees board election process

set nomination procedures

oversees theestablishment of coporate polices

Compensation commitee

100% independent.

dev remuration policies

Which protects creditor’s interests?

Tender offer

ad hoc commitee

poison pill

Corporate Governance Risks and Benefits

Risks

Weak control systems can benefit one stakeholder group at the expense of others, increasing the perception of a company's riskiness.

Insufficient information can lead to ineffective decision-making.

Poor corporate governance can increase a company's cost of capital as well as its exposure to default risk.

Benefits

Robust corporate governance practices allow risks to be identified earlier when they are easier to manage.

The clear reporting lines and delegation of responsibilities needed to implement strong corporate governance have the additional benefit of improving operational efficiency.

A commitment to corporate governance can reduce a company's exposure to legal, regulatory, and reputational risks.

Board and Management Mechanisms

Creditor committees

Creditor committees are formed by bondholders to represent the interests of lenders during a bankruptcy proceding. They may also be created on an ad-hoc basis when a company is struggling to meet its debt obligations but has not yet filed for bankruptcy protection.

Corporate takeovers

can be executed in several ways, including proxy contests, tender offers, and hostile takeovers. Incumbent managers and directors may adopt anti-takeover provisions (e.g., poison pills, staggered board elections) to prevent acquisitions that might make them redundant.

Corporate Reporting and Transparency

Transparency is critical to reducing the asymmetrical information advantage enjoyed by managers over shareholders. High-quality, timely reporting benefits all of a company's stakeholders, but particularly its capital providers.

who enjoy the advantage of information asymmetry,

Managers enjoy the advantage of information asymmetry,

Shareholders and managers have a classic agency relationship, with shareholders being principals who have hired managers as agents to act in their interests. Managers enjoy the advantage of information asymmetry, which makes it difficult for shareholders to assess their performance. Shareholders also have an agency relationship with the directors who they elect to represent their interests on the board. Corporate governance structures are part of the agency costs that are incurred to reduce the potential for exploitation in these agency relationships.

dual-class share systems,

A dual-class share system is a structure in which a company issues two or more classes of shares, each with different voting rights. Typically, one class of shares is offered to the general public and carries limited or no voting rights, while another class is held by company founders, executives, or insiders and has enhanced voting rights.

CCC - Cash conversion cycle

shows the time it takes for a company to convert its investments in inventory and other resources into cash inflows from sales.

how quickly can company converts investments into cash

CCC = DOH + DSO - DPO

a company reduces its cash conversion cycle in the following ways:

Increase DPO by obtaining longer payment terms from its suppliers.

Reduce DOH by using data analytics to improve demand forecasts or switching to "just in time" inventory management.

Reduce DSO by charging fees for late payments, tightening credit standards, and requiring up-front deposits. Additionally, a company can offer a price reduction for cash settlement within a discount period. The effective annual rate for trade credit is calculated using the following formula:

EAR of supplier financing

[(1 + discount/1-discount) ^ 365/PP-DP]-1

where PP and DP are the number of days in the payment period and discount period, respectively.

Total working captial

current assets - current liabilities

Net working capital

= current assets(excluding cash and marketable securites)- current liabilities(excluding short term and current debt)

Primary Sources of Liquidity

Primary sources of liquidity are readily accessible at a low cost, including:

Cash and marketable securities

Borrowings

Cash flow from operations (CFO)

FCFE

he amount of free cash flow available to a company's shareholders (FCFE) is calculated by subtracting capital investments from CFO

CFF equity = cfo - investments in long term assets

Secondary Sources of Liquidity

Suspending or reducing dividend payments to shareholders

Delaying or reducing capital expenditures.

Issuing new equity.

Renegotiating the terms of contracts with lenders, lessors, customers, and suppliers.

Selling assets.

Filing for bankruptcy protection.

Factors Affecting Liquidity: Drags and Pulls

drag on liquidity: A drag on liquidity is a lag on cash inflows resulting in a shortage of available funds. Major drags include uncollectable receivables, obsolete inventory, and tight credit terms from lenders

A pull on liquidity occurs when disbursements are made before cash can be generated from sales. Major pulls on payments include making payments early, low liquidity positions, and reduced credit limits from lenders and suppliers.

current ration

ca/cl

quick ratio

cash+mark sec + rec/cl

Cash ratio

cash + mark sec / cl

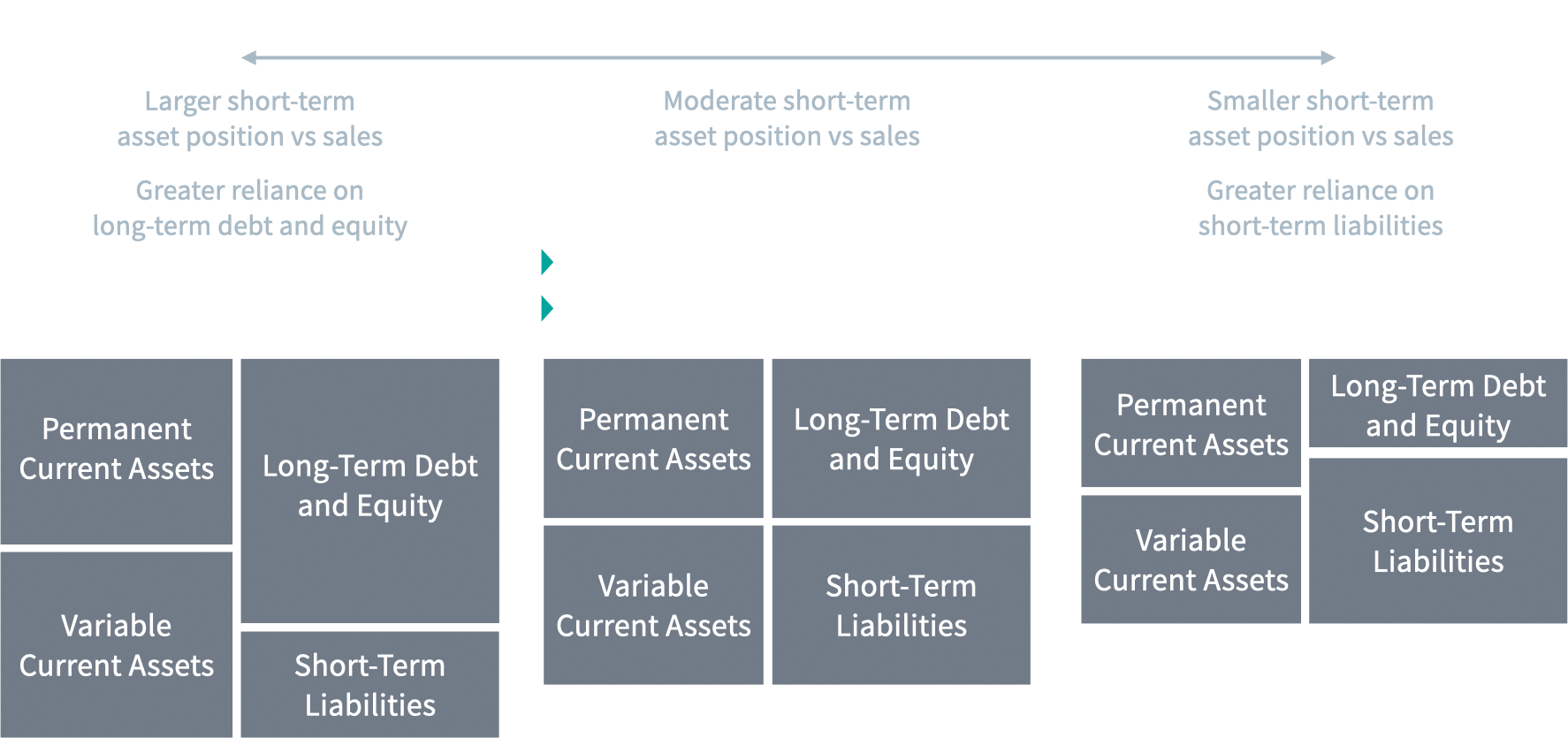

Wokring capital management

conservative - la

Lower working capital = more efficient operations

Conservative: working capital

Largest current assets, most long-term finance = greater certainty at higher cost

Typical for firms in early-growth phase (access to short-term debt limited)

More established companies may be able to pass on higher financing costs to customers

Suitable if expectation is for flat to rising interest rates

Working Capital and Liquidity Management

Aggressive:

Aggressive: Smallest level of current assets, more short-term finance = least flexibility, higher

May be considered for firms with lower profit margins

More suitable when future sales and cash needs can be forecasted with a high degree of

Suitable given an expectation of stable or falling interest rates

May be adopted for firms that expect to shorten CCC, can quickly liquidate inventory,

Pros: Lower financing cost

Flexibility to borrow only as needed (reduces total interest expense)

Short-term debt typically places fewer restrictions on operations

Flexibility to refinance if rates fall

Cons: Variable interest costs

Higher short-term cash needs to service debt

Rollover risk increases bankruptcy risk

More reliance on trade credit, collecting AR (may use 3rd party collection/AR sale)

debt service

returns

precision

collect AR

Capital Investments

Types , Going concern projects, regulatory/compliance, expansion projects

Going Concern Projects

Undertaken for a company to continue operating at its current size.

Relatively easy to evaluate because existing assets are being replaced.

Term of financing typically aligns closely with asset's expected useful life to avoid asset-liability mismatches.

A company's reported depreciation expense can be used as a proxy for its capital spending requirement for these types of projects.

Regulatory Compliance Projects

Pursued to comply with relevant laws, regulations, or contractual requirements.

Not meant to increase revenues or profitability, but may increase barriers to entry for potential competitors.

If the required costs are sufficiently high and cannot be passed along to customers, companies may abandon assets or cease operations.

Business Growth Projects

Investment in growth projects can be estimated as total capital spending less depreciation.

Expansion of Existing Business

Investments required to expand existing operations.

Riskier than going concern projects due to greater uncertainty.

Often developed internally through R&D projects.

External expansion through acquisition creates exposure to the risks of integration and overpaying.

New Lines of Business and Other Projects

Typically high-risk, high (potential) reward projects.

Unconventional projects (e.g., pet projects) are often excluded from normal project analysis process that is used for traditional capital investment

steps in capital allocation process

Capital Allocation

Steps in the Capital Allocation Process

Idea Generation: This can originate from within the company or from outside the company.

Investment Analysis: Collect information to forecast the investment's expected cash flows and profitability.

Planning and Prioritization: Select and prioritize profitable investment opportunities that together best fit the company's strategy.

Monitoring and Post-Investment Review

Net Present Value

A project's NPV is the amount of value that will be added to the company by making this investment. If the project has a conventional cash flow pattern, its NPV can be calculated using the following formula:

= CF0 + cf/(1+k)^1 + ct/(1+k)^t

Decision rule: Invest if NPV≥0. Do not invest if NPV<0.

IRR

Internal Rate of Return

The IRR is the discount rate that makes a project's NPV equal to zero:

Decision rule: Invest if IRR≥𝑟. Do not invest if IRR<𝑟.The required rate of return, 𝑟, is also known as the hurdle rate.

In the event of a conflict between NPV and IRR for mutually exclusive projects, decisions should be based on

In the event of a conflict between NPV and IRR for mutually exclusive projects, decisions should be based on NPV because 1) NPV represents the project's value to the firm, and 2) the IRR measure unrealistically assumes that all cash flows can be reinvested at this rate, while NPV only assumes that they will be reinvested at the required rate of return.

Conventional cash flow pattern

if the sign on the cf changes only once, with one ore more cash outflows followed by one or more cash inflow

unConventional cash flow pattern

has more than one sign change.

Adv & dis of NPV and IRR Methods

adv of npv - diret measure of the expected increase in the value of the firm

adv irr - measures profitablity as a percentage showing the return on each dollar invested.

dis irr - projects cf are reinvested at the irr while npv assumes those cf are reinvested aat the projects rrr

ROCI

ROIC reflects the effectiveness of a company's management in converting capital into profits, regardless of what type of capital is used (e.g., debt, equity). Companies create value for investors by generating an ROIC in excess of their cost of capital.

roci = NOPA/avg book value of total cap

Advantages of ROIC

Calculated using easily-accessible data

Can be broken into components for after-tax operating profitability and asset turnover

Allows aggregate level analysis of a company's ability to create value from capital budgeting decisions

Limitations of ROIC

Accounting-based inputs can be manipulated

Highly volatile, backward-looking measure

Mask differences in profitability among individual projects

Capital Allocation Principles

Capital Allocation Principles

The capital allocation process is based on the following key principles:

Decisions are based on after-tax cash flows, not accounting concepts.

Adjustments must be made for non-cash items (e.g., depreciation).

Include incremental cash flows, net of what would have occurred without the decision.

Only count current and future cash flows, not sunk costs.

Capital Allocation Pitfalls: Cognitive Errors in Capital Allocation

Internal forecasting errors:

Including sunk costs in a project's valuation

Incorrectly estimating a project's overhead costs

Using a discount rate that does not accurately reflect a project's true risk

Failing to account for opportunity costs or the anticipated responses of competitors

Ignoring costs of internal financing: Failing to recognize that all capital has an opportunity cost and treating internally generated funds as "free" capital with a 0% required return.

Inconsistent treatment of inflation: Nominal cash flows should be discounted at a nominal discount rate, and real cash flows should be discounted at a real discount rate. Inflation does not affect all revenues and costs uniformly.

Capital Allocation Pitfalls: Behavioral Biases in Capital Allocation

Inertia: The tendency to reuse their most recent capital budget with only minor adjustments.

Basing decisions on earnings metrics: The focus should be on cash flow-based NPV, not accounting measures.

Pet projects bias: Approving managerial pet projects based on overly optimistic projections or without being subject to a proper capital budgeting analysis.

Failing to consider alternatives: Getting fixated on specific projects and failing to consider other potentially better uses of funds.

Real Options

Real options are opportunities for a firm to delay a decision about a capital project or to amend the project after deciding to pursue it. Like financial options, real options are valuable because they grant the right to defer the timing of a decision until more information has been accumulated.

Types of Real OptionsTypes of Real Options

Types of Real Options

Real options can be classified based on the type of decision-making flexibility that they offer.

Timing options allow a company to delay its initial decision about whether to pursue a investment.

Sizing options allow the company to walk away from a project if the financial results are poor (abandonment option) or make additional investments if the results are positive (growth option).

Flexibility options provide the ability to make adjustments based on subsequent market conditions (e.g., price-setting options, production-flexibility options).

Fundamental options treat an entire investment as an option.

weighted average cost of capital

WACC = [weight of debt x pretax cost of debt (1-tax)] + (weights of equity x cost of equity)

wacc = wd rc (1-t) + we re

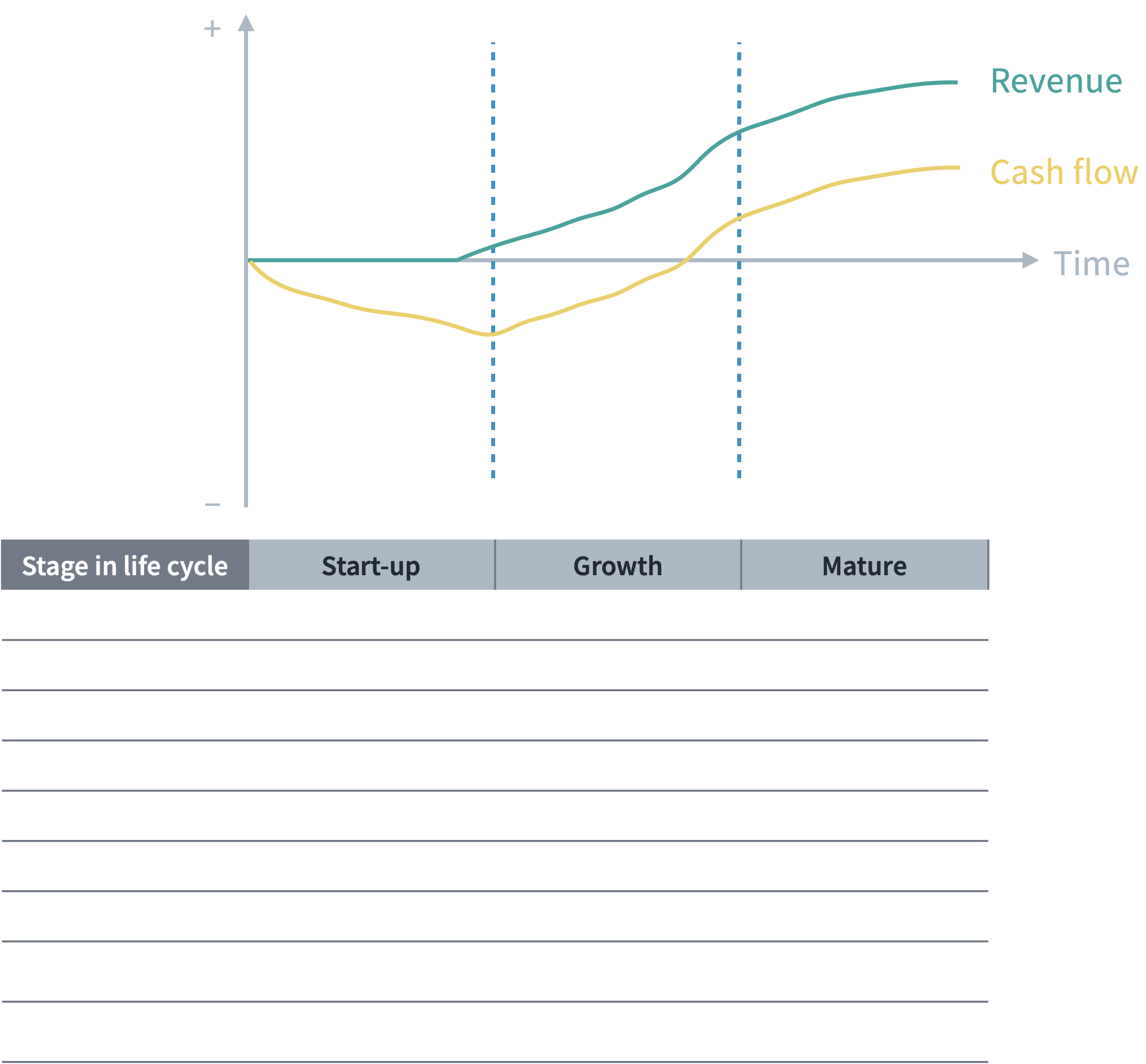

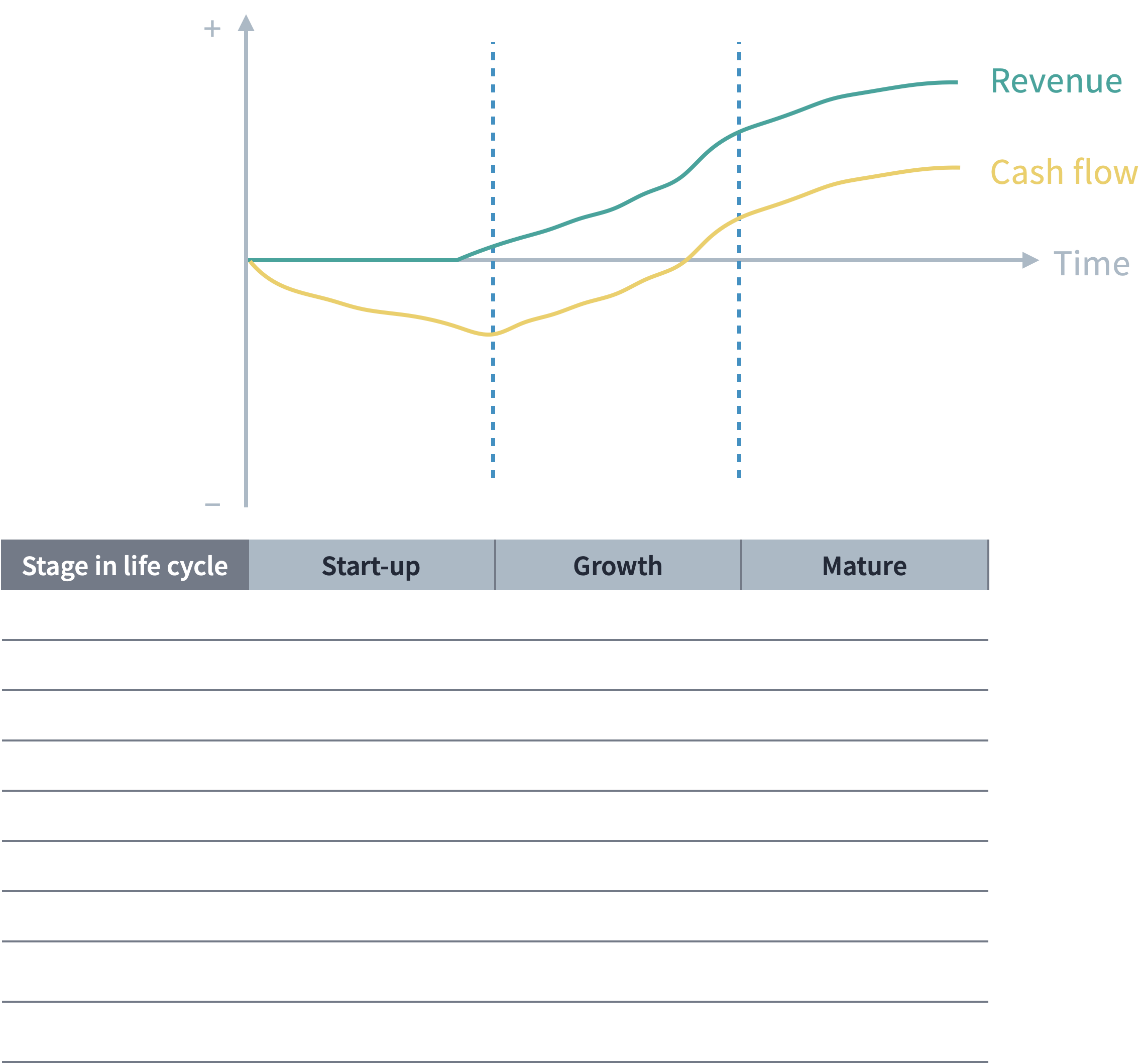

Corporate Life Cycle:

Modigliani–Miller Propositions without Taxes

Proposition I Without Taxes: Capital Structure Irrelevance

The value of an unlevered firm is equal to its levered value (𝑉𝑈=𝑉𝐿) if the following assumptions hold:

Investors have homogeneous expectations.

Capital markets are perfectly efficient.

Investors can borrow and lend at the risk-free rate.

There are no agency costs.

Financing and investment decisions are independent.

Under these theoretical conditions, the present value of a company's future cash flows will be unaffected its capital structure.

Proposition II Without Taxes: Higher Financial Leverage Raises the Cost of Equity

If the five assumptions hold, a company's WACC remains constant because any increase in the use of low-cost debt will be offset by a corresponding increase in the cost of equity to reflect the risk of higher leverage. A levered firm's cost of equity is a linear function of its debt-to-equity ratio:

𝑟𝑒=𝑟0+(𝑟0−𝑟𝑑)(𝐷/𝐸)

Modigliani–Miller Propositions with Taxes

Proposition I With Taxes: Firm Value

If debt payments can be deducted from taxable income, firm value can be increased by the amount of the debt tax shield.

Proposition II With Taxes: Cost of Capital

If all other assumptions hold, introducing taxes (and deductible interest) will reduce WACC at higher debt-to-equity ratios. The cost of equity will rise, but not at the same rate as in a no-tax scenario. Rearranging the updated WACC formula allows us to determine the cost of equity under this revised set of assumptions:

𝑟𝑒=𝑟0+(𝑟0−𝑟𝑑)(1−𝑡)(𝐷/𝐸)

Pricing and Revenue Models

Price Discrimination Strategies:

Tiered pricing

Dynamic pricing

Value-based pricing

Auction/reverse auction models

Tiered pricing

Tiered pricing is a strategy that charges different prices for different levels of service or quantities of products.

dynamic pricing

the practice of varying the price for a product or service to reflect changing market conditions, in particular the charging of a higher price at a time of greater demand.

Value-based pricing

Value-based pricing is a strategy of setting prices primarily based on a consumer's perceived value of a product or service.

Pricing Strategies for Multiple Products:

Bundling: Selling multiple products or services together as a single combined package at a reduced price.

Razors-and-blades pricing: Selling a core product at a low price or at a loss (the razor) while charging higher prices for consumable accessories or components (the blades).

Add-on pricing: Charging extra fees for additional features, services, or products that are optional and not included in the base price.

Pricing Strategies for Rapid Growth:

Penetration pricing - exp jio, gives products at low margin in beginning after growing maket share it will charege

Freemium pricing - offer with basic functionality at no cost but sell or unlock other function for a fee

Hidden revenue business model - ads

value chain

A company's value chain is the answer to the question of how it executes its value proposition. In order to deliver value to its customers, a firm requires relevant assets and capabilities.

supply chain

A supply chain includes all of the steps and processes involved in the physical transformation of a product up to the point that it is purchased by the end consumer.

Unit economics

Unit economics is the quantitative analysis of a company's revenues and costs on a per unit basis.

A company's contribution margin is the difference between the unit price and its variable costs per unit.

The break-even point is the quantity of units sold that allows a company to cover its fixed costs.

Business Model Types

Conventional Business Models

One of the most important determinants of a company's business model is whether it offers products or services. The business models of companies that operate in goods-producing industries have long been understood in terms of their position in a linear supply chain.

banks, manugactures, distributors, retailers, baks, software

Private label manufacturers

producing items that are marketed by other firms under outsourcing arrangements.

Licensing arrangements

allow a firm to sell products that use another firm's brand or intellectual property in exchange for royalty payments.

Produce under a recognized brand name, pay royalty

Value added reseller

provide key follow-up services for the products that they sell.

Franchise models

Franchisor earns a royalty and is responsible for advertising and product

Network effects

Network Effects

The increase in value of a network to its users as more users join

e.g. messaging platforms, payment platforms, social media, payment systems, stock

One sided : there is one type of user that is valuable to other users e.g. Venmo

Two sided : two (or more) types of users e.g. credit card networks

Crowdsourcing : users contribute to the product, the business facilities ‘communities’

Crowdsourcing

allows users to generate a product or service, typically voluntarily and often with little or no oversight. wikipedia