ACC 203

1/201

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

202 Terms

Information is verified by external auditors, Focus is on the past.

Financial Accounting

Main characteristic of information is that it must be relevant

managerial accounting

Reports tend to be prepared for the parts of the organization rather than the whole organization.

managerial accounting

Primary users are internal (i.e., company managers).

managerial accounting

It is governed by Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS).

Financial Accounting

The primary characteristics of information are that it must be reliable and objective.

Financial Accounting

Reports are prepared as needed, It is not governed by legal requirements.

managerial accounting

Primary users are external (i.e., creditors, investors).

Financial Accounting

Focus is on the ruture.

managerial accounting

Reporting is based mainly on the company as a whole.

Financial Accounting

My business paid Facebook for Advertising Expense, my cash would __ and my earnings (equity) would _

Decrease, Decrease

report 3 types of inventory on the balance sheet

Manufacturing companies

for a company such as Best Buy (consumer electronics) includes all of the costs necessary to purchase products and get them onto the store shelves.

Inventory (merchandise)

most for-profit organizations can be described as being in one (or more) of 3 categories

service companies, manufacturing companies, & merchandising companirs

typically do not have an inventory account

Service companies

Wholesalers

but products in bulk from producers, mark them up, & resell to retailers

Direct Cost

cost that can be easily and accurately traced to a specific cost object

Indirect Cost

relates to the cost object but cannot be traced to it in an economically feasible way because it supports multiple departments

product costs

all costs required to manufacture a physical product. Recorded as “inventory” on the B/S & only become an “Expense” (COGS) when the product is sold

If it happens inside the factory

Direct Materials (DM)

The primary raw materials that become a physical part of the finished product. Tracer: must be easily & cost-effectively traceable to a specific unit.

Ex. Milk in a bottle of yogurt

Direct Labor (DL)

The compensation of employees who physically convert raw materials into finished goods. AKA: “touch labor”

Ex. Wages of the assembly line worker

Manufacturing Overhead (MOH)

All indirect costs incurred in the factory that are NOT direct materials or direct labor.

Includes: Indirect materials, indirect labor (supervisors/janitors), factory utilities, factory rent, and factory depreciation

Period costs

costs related to the passage of time rather than the production process. They are expensed on the I/S in the period they are incurred. Categories: Selling, General, & Administratice (SG&A) expenses.

Ex. Advertising, CEO salary, corporate office rent

Calculate COGS

Beginning Inventory

+Purchases

=COG available for sale

-Ending Inventory

= COGS

prepare income statement

Sales Revenues

-COGS

=Gross Profit

-Operating Expenses

=operating income (net)

gross margin

aka gross profit

classify: airplane seats cost object airplaine

Product - DM

classify: Production supervisors’ salaries

Product - MOH

Depreciation on forklifts in factory

Product - MOH

Machine lubricants

Product - MOH

Factory janitors’ wages

Product - MOH

Assembly workers’ wages

Product - DL

Property tax on corporate marketing office

Period

Plant utilities

Product - MOH

Cost of warranty repairs

Period

Machine operators’ health insurance

Product - DL

Depreciation on administrative offices

Period

Cost of designing new plant layout

Period (Design on value chain)

jet engines

Product - DM

Prime costs

Direct materials + Direct Labor

DM + DL

Conversion Costs

Direct Labor + Manufacturing Overhead

DL + MOH

Costs of converting raw materials into finished goods

Relevant Costs

has potential to influence a decision. Must occur in the future & have a differential cost (diff btwn alternatives)

Irrelavant costs

should not influence a decision. Do not differ among alternatives, ignore sunk costs (costs that have alr been incurred & cannot be changed)

Current Assets in B/S of Service, Merchandisers, & Manufacturers

Service companies have no inventory

Merchandisers show inventory (or merchandise Inventory)

Manufacturers show inventory, including the breakdown of Inventory accounts (Raw Materials, Work in Progress, & finished goods)

Manufacturing overhead

visualize the factory if it happens inside those walls it is a manufacturing cost.

Product Costs (Manufacturing costs)

INSIDE the 4 Walls of factory

- Treated as inventory until sold

- For manufacturers:

o Direct Materials (DM)

o Direct Labor (DL)

o Manufacturing Overhead (MOH) (indirect materials, indirect labor, factory utilities, depreciation, etc.)

Period costs

OUTSIDE the factory

- Nonmanufacturing costs

- Expensed immediately

- Includes selling, general, & administrative (SG&A)

Predetermined MOH Rate = __ per DL hour

Estimated Manufacturing Overhead / Estimated Direct Labor Hours

Predetermined MOH Rate = __ % of DL Cost

Estimated Manufacturing Overhead / Estimated Direct Labor Cost

Predetermined MOH Rate = __ $ per machine hour

Estimated Manufacturing Overhead / Estimated Machine Hours

Predetermined Manufacturing Overhead Rate (POHR) =

Estimated Manufacturing Overhead / Estimated DL Hours = $ per DL hour

Total MOH = (use PHOR)

= POHR * Actual DL hours

POHR =

Estimated mOH cost / Estimated total cost driver (hours)

allocation base (i e cost driver)

what causes the overhead costs to be incurred (ex DL hours or Machine hours

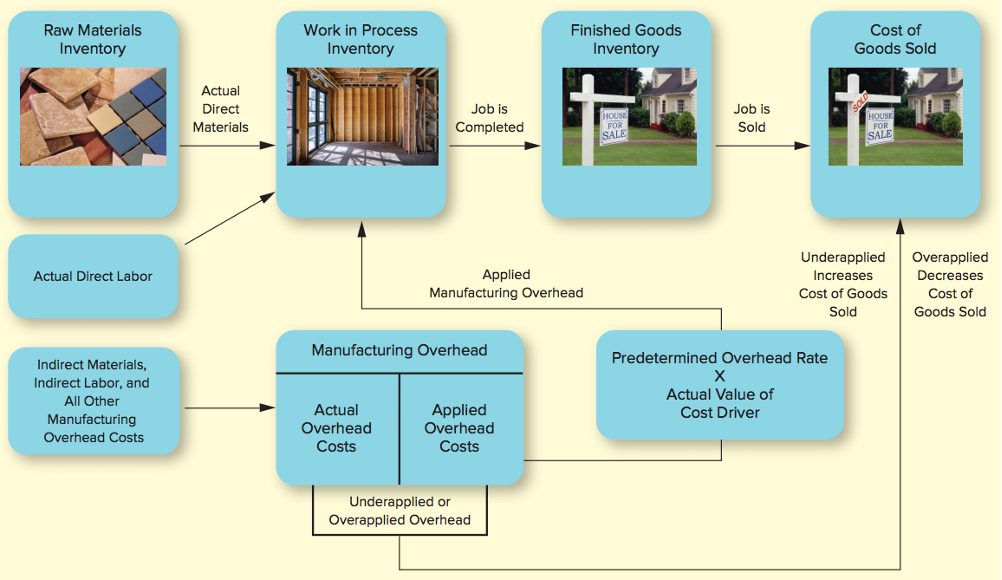

Job Costing Systems

used by companies that produce unique products or services (e.g. acounting firms, custom designers, motion picture studios)

costs are recorded in separate WIP accounts by job

goal is to track & accumulate costs of each unique product, project or service

Process Costing systems

used by companies that produce homogenous/identical products or services (e.g. oil manufacturers, soft drink manufacturers).

○ Costs are recorded in separate WIP accounts by stage of the production process. (FYI only. Beyond the scope of this course)

determine direct materials (DM) cost?

Traced directly to jobs in the WIP inventory account (based on materials used)

determine direct labor (DL) cost?

Traced directly to jobs in the WIP inventory account (based on hours worked)

determine manufacturing overhead (MOH) cost ?

○ cannot be traced directly to specific jobs, so we have to allocate some reasonable amount of these costs to each job.

○ Job costing approach involves “applying” overhead using a predetermined overhead rate (POHR)

Apply manufacturing overhead to jobs by multiplying the POHR by the ACTUAL cost driver

POHR × Actual cost driver = Applied MOH

Raw Materials Inventory, WIP Inventory, Finished goods inventory

Inventory

COGS is an..

Expense.

after a job is sold, it is transferred out of inventory & into COGS

Process

=Gross profit (per unit)

Sales price (per unit) – Total job cost (per unit)

Allocated (Applied) MOH

Predetermined Rate × Actual Activity (e.g., Actual Hours).

What it is: The "estimated" cost added to jobs while they are being worked on.

Overallocated

Allocated > Actual.

Meaning: You put too much cost on the jobs.

Fix: Decrease Cost of Goods Sold (COGS).

Underallocated

Allocated < Actual.

Meaning: You didn't put enough cost on the jobs.

Fix: Increase Cost of Goods Sold (COGS).

3 numbers: estimated, actual, allocated

Estimated: Used only to find the Rate at the start of the year.

Actual: What was actually spent (the "real" bills).

Allocated: The amount assigned to jobs (Rate × Actual Hours).

Why Estimate?

To provide immediate cost info for pricing and bidding without waiting for year-end utility bills.

Allocated MOH =

Predetermined overhead rate * actual amount of the allocation base used by the specific job

cost allocation

Assigning manufacturing overhead costs and other indirect costs to jobs is called:

If manufacturing overhead is overallocated for the period by $100, then

Jobs have been overcosted during the period

When a company uses direct labor, it traces the cost to the job by debiting:

Work in Process Inventory.

Direct labor always increases WIP because it’s a direct, traceable production cost.

materials requisitioned for production aka

DM used

Applied MOH =

POHR * actual hours

Production Supervisor, factory rent, factory utilities, maintenance on machines

MOH

left End. Bal on manufacturing overhead T account

overhead was under-applied, inc COGS

right End. Bal on manufacturing overhead T account

overhead was over-applied, dec. COGS

Gross profit %

gross profit / sales revenue

sales commissions, marketing costs

period costs

Operating income =

gross profit - period costs

when products are sold, the journal entry to record the sale of goods includes

a credit to finished goods inventory

Variable Costs

change in total with changes in activity (e.g., total vc inc as activity Inc.)

vc per unit is constant as activity Inc

Fixed Costs

remain the same in total regardless of activity level (e.g., total fixed costs remain constant as activity increses

Mixed costs

have a fixed and variable component. fixed portion represents the base amount that will be incurred regardless of activity

(ex. 0 units - 350, 100 units - 400, 200 units-450, 300 units-500, 400 units- 550)

Step costs

fixed over small range of activity and then jump to a new fixed level

(ex. to allow more customers to be served, Starbucks might hire an additional supervisor or rent additional space or equipment)

(ex. 0 units, 100 units, & 200 units - 500, 300 units, 400 units - 750)

Variable or Fixed: Rubber used in bike tires

Variable

Variable or Fixed: Recycled aluminum used to make the bike frame

Variable

Variable or Fixed: Lubricant used on clipless pedal springs

variable

Variable or Fixed: Quality inspector’s salary

Fixed

Variable or Fixed: Depreciation on equipment used to make the aluminum in the bike frame

fixed

Variable or Fixed: renewable cork used to make the saddle

variable

Variable or Fixed: patent on belt drive (used instead of a chain)

fixed

When choosing the high point for the high-low method, how is the high point selected?

The point w the highest volume of activity is chosen

Regression analysis

A statistical procedure for determining the line, and association cost, that best fits all of the data points in the data set

what’s the advantage of using regression analysis:

A. The method is objective

B. All data points are used to calculate the terms for the cost equation.

C. Regression analysis will generally be more accurate than the high-low method.

• D. All of the listed statements are true about regression analysis.

D. All

The only difference between variable costing and absorption costing is in the treatment of

• A. variable manufacturing overhead costs.

• B. fixed manufacturing overhead costs.

• C. direct materials and direct labor costs.

• D. variable nonmanufacturing costs.

fixed MOH

Fixed or Variable: finance charges on car loan

fixed

Fixed or Variable: Car washes (one per week)

fixed

Fixed or Variable: traffic violation ticked

fixed???