Chapter 16 Review Problems

1/23

Earn XP

Description and Tags

Pulled from MyBusinessCourse - not all problems are mentioned.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

24 Terms

Compute the selling price of the following bond issuance:

5M Corp. authorized and issued $120,000, 5%, 10 -year bonds payable on January 1.

Calculate the selling price of the bonds if the bonds pay cash interest semiannually on July 1 and January 1 and the market rate of interest on similar bonds is 7%.

$102,945

Compute the selling price of the following bond issuance:

5M Corp. authorized and issued $40,000, 6%, 10 -year bonds payable on January 1.

Calculate the selling price of the bonds if the bonds pay cash interest semiannually on July 1 and January 1 and the market rate of interest on similar bonds is 5%.

$43,118

Compute the selling price of the following bond issuance:

5M Corp. issued $40,000, 6%, 10 -year bonds payable on April 30 at 97. The bonds were authorized on January 1.

Calculate the selling price of the bonds (including interest) if the bonds pay cash interest semiannually on July 1 and January 1.

$39,600

5M Corp. authorized and issued $120,000, 5%, 10 -year bonds on January 1 at face value. Cash interest is paid annually on December 31:

Record the issuance of bonds on January 1.

Dr. Cash 120,000

Cr. Bonds Payable 120,000

5M Corp. authorized and issued $120,000, 5%, 10 -year bonds on January 1 at face value. Cash interest is paid annually on December 31:

Record the payment of interest (12/31/yr 1).

Dr. Interest Expense 60000

Cr. Cash 6000

5M Corp. authorized and issued $120,000, 5%, 10 -year bonds on January 1 at face value. Cash interest is paid annually on December 31:

Record the principal payment (12/31/yr 10).

Dr. Bonds Payable 120,000

Cr. Cash 120,000

5M Corp. authorized and issued $120,000, 5%, 10 -year bonds on January 1. The bonds pay cash interest semiannually on July 1 and January 1 and are issued to yield 7% - under the “effective interest method.”

Record issuance of bonds (January 1)

Dr. Cash 102,945

Dr. Discount on Bonds Payable 17,055

Cr. Bonds Payable 120,000

5M Corp. authorized and issued $120,000, 5%, 10 -year bonds on January 1. The bonds pay cash interest semiannually on July 1 and January 1 and are issued to yield 7% - under the “effective interest method.”

Record payment of interest on July 1.

Dr. Interest Expense 3,603

Cr. Discount on Bonds Payable 603

Cr. Cash 3,000

5M Corp. authorized and issued $120,000, 5%, 10 -year bonds on January 1. The bonds pay cash interest semiannually on July 1 and January 1 and are issued to yield 7% - under the “effective interest method.”

Record accrual of interest on December 31.

Dr. Interest Expense 3,624

Cr. Discount on Bonds Payable 624

Cr. Interest Payable 3,000

5M Corp. authorized and issued $120,000, 5%, 10 -year bonds on January 1. The bonds pay cash interest semiannually on July 1 and January 1 and are issued to yield 7% - under the “straight line method.”

Record issuance of bonds (January 1)

Dr. Cash 102,945

Dr. Discount on Bonds Payable 17,055

Cr. Bonds Payable 120,000

5M Corp. authorized and issued $120,000, 5%, 10 -year bonds on January 1. The bonds pay cash interest semiannually on July 1 and January 1 and are issued to yield 7% - under the “straight line method.”

Record payment of interest on July 1.

Dr. Interest Expense 3853

Cr. Discount on Bonds Payable 853

Cr. Cash 3000

5M Corp. authorized and issued $120,000, 5%, 10 -year bonds on January 1. The bonds pay cash interest semiannually on July 1 and January 1 and are issued to yield 7% - under the “straight line method.”

Record accrual of interest on December 31.

Dr. Interest Expense 3853

Cr. Discount on Bonds Payable 853

Cr. Bonds Payable 3000

On January 1, 5M Inc. issued $600,000 of bonds at 95. The bonds pay 5% cash interest semiannually on June 30 and December 31. The bonds are scheduled to mature in 5 years on December 31. The company retired $60,000 of the bonds on October 1, when the bonds were selling at 89 plus accrued interest. Assume the “straight-line interest method” is used to amortize the bond discount.

Record for the entry for the bond issuance on January 1.

Dr. Cash 570,000

Dr. Discount on Bonds Payable 30,000

Cr. Bonds Payable 600,000

On January 1, 5M Inc. issued $600,000 of bonds at 95. The bonds pay 5% cash interest semiannually on June 30 and December 31. The bonds are scheduled to mature in 5 years on December 31. The company retired $60,000 of the bonds on October 1, when the bonds were selling at 89 plus accrued interest. Assume the “straight-line interest method” is used to amortize the bond discount.

Record the entry for the interest payment on June 30.

Dr. Interest Expense 18,000

Cr. Discount on Bonds Payable 3,000

Cr. Cash 15,000

On January 1, 5M Inc. issued $600,000 of bonds at 95. The bonds pay 5% cash interest semiannually on June 30 and December 31. The bonds are scheduled to mature in 5 years on December 31. The company retired $60,000 of the bonds on October 1, when the bonds were selling at 89 plus accrued interest. Assume the “straight-line interest method” is used to amortize the bond discount.

Record the entry to recognize interest expense for the portion of the bond issue retired on October 1.

Dr. Interest Expense 900

Cr. Discount on Bonds Payable 150

Cr. Cash 750

On January 1, 5M Inc. issued $600,000 of bonds at 95. The bonds pay 5% cash interest semiannually on June 30 and December 31. The bonds are scheduled to mature in 5 years on December 31. The company retired $60,000 of the bonds on October 1, when the bonds were selling at 89 plus accrued interest. Assume the “straight-line interest method” is used to amortize the bond discount.

Record the entry for bond extinguishment on October 1.

Dr. Bonds Payable 60,000

Cr. Discount on Bonds Payable 2550

Cr. Cash 53,400

Cr. Gain on Extinguishment of Debt 4050

5M Corp. issued $240,000 of 5%, 5 -year convertible bonds. Each $1,000 bond is convertible into 5 shares of common stock ( $1 par value per share) of 5M Corp. The bonds were sold at 98 on January 1 of Year 1:

Provide the entry on 1/01/yr 1 for issuance of convertible bonds.

Dr. Cash 235,200

Dr. Discount on Bonds Payable 4800

Cr. Bonds Payable 240,000

5M Corp. issued $240,000 of 5%, 5 -year convertible bonds. Each $1,000 bond is convertible into 5 shares of common stock ( $1 par value per share) of 5M Corp. The bonds were sold at 98 on January 1 of Year 1:

The conversion privilege for 50% of the bonds is exercised on December 31 of Year 2. Assume that any discount or premium has been amortized through the date of conversion using the straight-line interest method and that the common stock is selling at $125 per share at the conversion date.

Provide the entry for conversion of the bonds to common stock, using the book value method.

Dr. Bonds Payable 120,000

Cr. Discount on Bonds Payable 1440

Cr. Common Stock 600

Cr. Paid-in Capital in Excess of Par - Common Stock 117,960

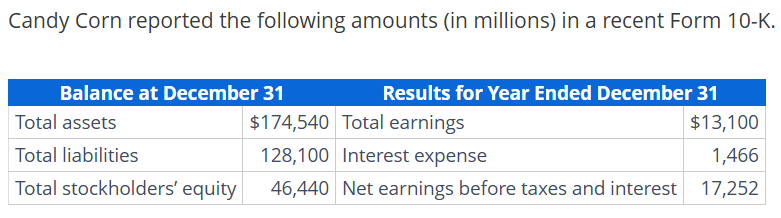

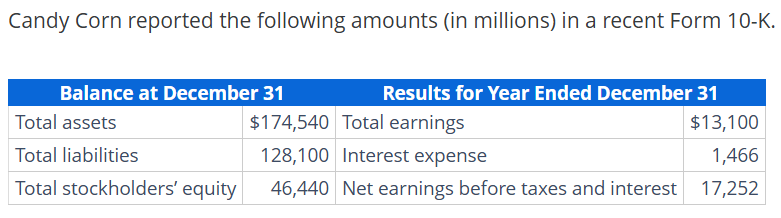

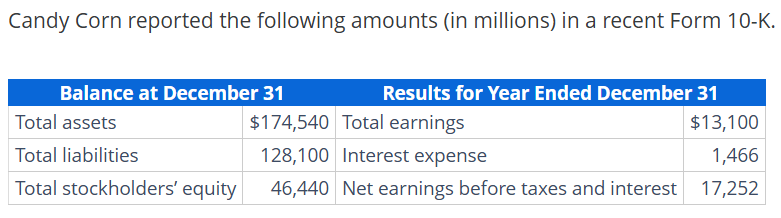

Use the attached screenshot to calculate “total liabilities-to-equity ratio”

128,100/46,440 = 2.76

Use the attached screenshot to calculate “total liabilities-to-total assets ratio.”

128,100/174,540 = 0.73

Use the attached screenshot to calculate “times interest earned.”

17,252/1466 = 11.77

On January 1, Frazier Inc. issued 3 -year bonds to Seattle Corp. at face value for $20,000, with cash interest payable annually on December 31 at 4%. On January 1, Frazier Inc. chooses to account for the bonds using the fair value option. The fair value of the bonds on December 31 is $16,000 because Frazier Inc. was in violation of a debt covenant.

Record the adjusting entry on December 31.

Dr. Fair Value Adjustment - Bonds Payable 4000

Cr. Unrealized Gain or Loss - OCI 4000

On January 1, CostKo Corporation issued $200,000 of 6%, 5 -year nonconvertible bonds with nondetachable stock purchase warrants. Each $1,000 bond carried 10 warrants, each of which was for one share of CostKo common stock, par value $1 , at a specified option price of $40 per share. The bonds (including the warrants) sold at 102. No bond price without warrants was available.

Provide the entry at the date of issuance of the nondetachable bonds.

Dr. Cash 204,000

Cr. Bonds Payable 200,000

Cr. Premium on Bonds Payable 4000

On January 1, CostKo Corporation issued $200,000 of 6%, 5 -year nonconvertible bonds with nondetachable stock purchase warrants. Each $1,000 bond carried 10 warrants, each of which was for one share of CostKo common stock, par value $1 , at a specified option price of $40 per share. The bonds (including the warrants) sold at 102. No bond price without warrants was available.

Provide the entry at the date of issuance of the detachable bonds.

Dr. Cash 204,000

Dr. Discount on Bonds Payable 6000

Cr. Bonds Payable 200,000

Cr. Paid In Capital - Stock Warrants 10,000