6.2 Other investment types REITs, ETFs, and ETNs

1/16

Earn XP

Description and Tags

REITs, ETFs, and ETNs

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

17 Terms

Real estate investment trusts (REITs)

are trusts that invest in real estate and mortgages.

structured much like a closed-end fund but are not considered an investment company as the portfolio does not hold other securities

not open or close investment company.

Shareholders receive dividends from investment income or capital gains distributions.

Many REITs are registered with the SEC and, therefore, are subject to all disclosure requirements, known as public REITs and are subject to greater risk.

there are REITs that are not registered with the SEC, known as private REITs.

Nonlisted REITs are difficult to price and have far less liquidity than a listed REIT.

RITS

Offer the ability to participate in pooled investment focused on real estate purchases and mortgages

similar to mutual funds as they follow conduit tax theory, but are not investment companies

may be registered or non registered

pay dividends and pass gains through to investors but do not pass through losses like limited partnerships do

equity REIT.

A real estate investment trust that owns properties but does not hold mortgages

mortgage REIT

A REIT. One that holds mortgages but not the property

hybrid REIT

One that does both, mortgage and equity

leasing REIT.

There is no such thing

Exchange-traded funds (ETFs)

the fastest growing investments in the U.S. market.

These investments are organized as open-end investment companies but have significant differences.

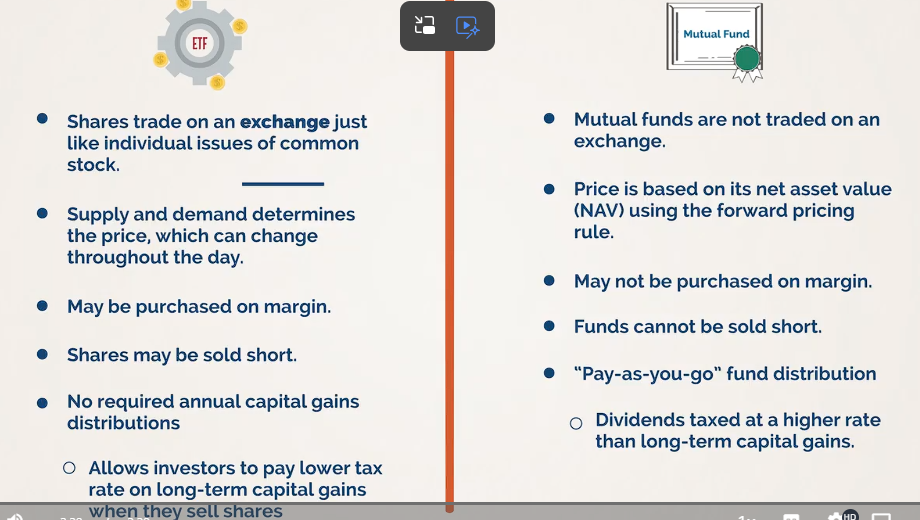

The most obvious is that the shares trade in the secondary markets.

Many are listed on one or more exchanges.

ETFs

Because they trade in the secondary market, an investor can take advantage of intraday (within one day) price changes.

ETFs can be purchased on margin (with borrowed money) and sold short.

Expenses tend to be lower than those of mutual funds, and the management fee is also low.

Like an index fund, most ETFs do not actively trade within the fund. This generally results in greater tax efficiency for the investor, since the index fund realizes less taxable capital gains.

Every time a person purchases or sells shares, there is a commission, and those charges can add up over time.

All of the following are concerns regarding private, nontraded, REITS

lack of liquidity,

transparency in operations

difficulty of valuing the programs.

Nontraded REITs and public (traded) REITs

are taxed the same way

A prospectus must be delivered to customers following a transaction in all of the following except

advantages of ETFs when compared with open-end mutual funds:

Pricing and ease of trading. Because individual ETF shares are traded on exchanges, they can be bought or sold anytime during the trading day at the price they are currently trading at, as opposed to mutual funds, which use forward pricing and are generally priced once at the end of the trading day.

Margin. ETFs can be bought and sold short on margin like other exchange-traded products (ETPs). Mutual funds cannot be bought on margin, nor can they be sold short.

Operating costs. ETFs traditionally have operating costs and expenses that are lower than most mutual funds.

Tax efficiency. ETFs can and sometimes do distribute capital gains to shareholders like mutual funds do, but this is rare. Because these capital gains distributions are not likely, there are usually no further tax consequences with ETF shares until investors sell their shares. This may be the single greatest advantage associated with ETFs.

disadvantages of ETFs when compared to open-end mutual funds:

Commissions. The purchase or sale of ETF shares is a commissionable transaction. The commissions paid can erode the low-expense advantage of ETFs. This would have the greatest impact when trading in and out of ETF shares frequently or when investing smaller sums of money.

Market influences on price. Because ETFs trade on exchanges, share prices can be influenced by market forces such as supply and demand, like any other investment that trades in the secondary market. Investors need to recognize that they might receive less than NAV per share when selling ETF shares.

ETFs vs Mutual funds

Exchange-traded notes (ETNs)

unsecured debt securities issued by a bank or financial institution, they are backed only by the good faith and credit of the issuer

ETNs are bond-like instruments with a stated maturity date, but they do not pay interest and they offer no principal protection.

ETN investors receive a cash payment linked to the performance of the underlying index, minus management fees, when the note matures.

The notes track the performance of a particular market index but do not represent ownership in a pool of securities the way share ownership of a fund does.

If the credit of the underwriting bank should falter, the note might lose value in the same way any other senior debt of the issuer would. Additionally, there are limits to the size of ETN issues.

Though these are called exchange-traded notes, very few of these trade in the secondary markets. These investments can be illiquid.

What is The primary risk associated with ETNs

default risk. Liquidity risk is also a common concern. Even though they are called exchange traded, very few of them have ever actually been listed on an exchange.

Which of the following best describes an Exchange-Traded Note (ETN)?

A debt security issued by a financial institution with returns linked to a market index or benchmark