OM Week 11

1/73

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

74 Terms

What does every operations decision start with?

A forecast

What happens in OM if we get the forecast wrong?

Everything downstream becomes “wrong” too

What are the three main pairings that get forecasted in OM?

Demand and Sales

Unit sales by product, by region, by channel

Used for production planning, inventory, and staffing

Prices and Costs

Raw material prices, energy costs

Affects procurement and budgeting

Supply and Lead Times

Supplier delivery reliability

Affects safety stock and reorder points

Right Censoring

If you sell out, sales undercount true demand

You only observe a demand up to available supply

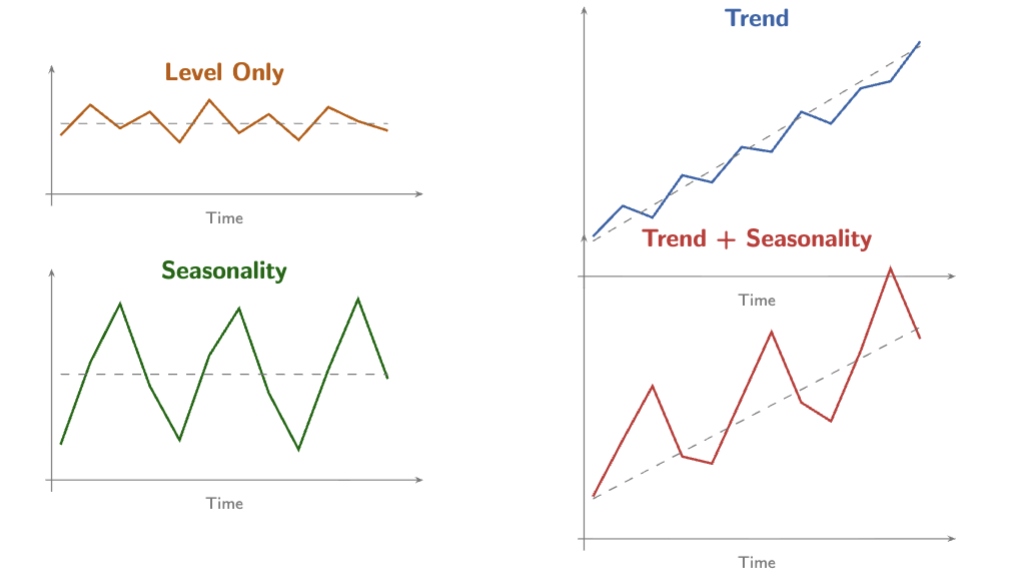

Four Properties of Forecasts

Forecasts are always wrong

Never report just a point estimate

Always include an error measure

Short term > Long term

Next week’s forecast is more accurate than next year’s

Uncertainty compounds over time

Aggregate > disaggregate

Total company sales easier to forecast than one SKU

Individual errors cancel out when aggregated

Upstream direction

Forecast error amplify as you move up the supply chain

Small retail fluctuation → lrge manufacturer swing

Bullwhip effect

A forecast without an error estimate is

Just a guess

What happens when we over forecast (4 points)?

Excess inventory sitting in warehouses

Spoilage and waste (especially perishables)

Holding costs eat into margins

Markdowns to clear unsold stock

What happens when we under forecast?

Lost sales and empty shelves

Customers switch to competitors

Expediting costs to rush orders

Backorder management overhead

Random Variation Demand Fluctuation

Unpredictable, short term fluctuations

Cannot be forecasted → only measured

Trend Demand Fluctuation

Sustained upward or downward movement

Driven by market growth, technology shifts

Seasonality

Predictable, repeating pattern within a fixed cycle

Weekly, monthly quarterly, annually

Business Cycles Demand Fluctuations

Long term economic expansions and contractions

Hard to predict timing, easier to recognize

What is the forecaster’s job within OM?

Separate what is systematic (trend, seasonality) from what is random (noise)

Forecast the systematic part, measure the random part

Four Demand Patterns

What are the two components of an observation?

Systematic Component (What we can forecast)

Noise

What are the three elements of the Systematic Component?

Level (L): the baseline demand

Trend (T): the rate of change per period

Seasonal Factor (St): periodic multiplier

Multiplicative Model Formula

Ft = (L + T x t) x St

Multiplicative Model

Level and trend set the baseline; seasonality scales it up or down

Most common

Additive Model Formula

Ft = L + T x t + St

Additive Model

Use when seasonal swings are constant regardless of level

What is the rule of thumb for using the multiplicative model?

If seasonal peaks grow as demand grows

What is the rule of thumb for using the additive model?

If peaks stay the same size

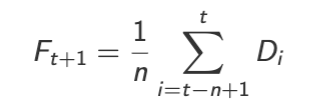

Simple Moving Average Formula

Simple Moving Average (SMA)

Forecast next period’s demand as the average of the last n observations

Each of the last n periods gets equal weight

Periods before that get zero weight

The “window” slides forward each period

What are the implications of choosing a small n for SMA (4 points)?

Reacts quickly to changes

Picks up real shifts faster

But also amplifies noise

Forecast is volatile

What are the implications of choosing a large n for SMA (4 points)?

Smooths out noise effectively

Stable, less jumpy forecasts

But slow to detect real shifts

Forecast is sluggish

A Small n for SMA is [BLANK1] while a Large n is [BLANK2]

Responsive/Stable

Responsive/Stable

Responsive

Stable

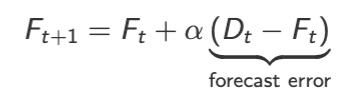

Exponential Soothing Formula

a E (0,1) is the smoothing constant

What are the two equivalent interpretations of Exponential Smoothing?

Weighted blend:

New forecast = blend of latest observation and previous forecast

a controls how much weight goes to new data

Error correction:

Start with previous forecast

Adjust by a fraction a of the error

If you under forecast, nudge up

If you over forecast, nudge down

Error Correction Formula

What is the advantage of ES over SMA?

Each step back in time multiplies the weight by (1-a)

The forecast is a weighted sum where recent data gets the most weight

Weights decay

Exponentially

What are the implications of choosing a Small a for ES?

Heavy weight on history

Very smooth, stable forecast

Slow to react to real changes

Like a large-n moving average

What are the implications of choosing a Large a for ES?

Heavy weight on recent data

Responsive, catches shifts quickly

But amplifies noise

Like a small-n moving average

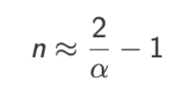

An ES with smoothing constant a behaves roughly like an SMA with:

What level of a should you first try for stable demand?

a = 0.1-0.3

What level of a should you first try for volatile/level-shifting demand?

a = 0.3-0.5

Attributes of SMA pertaining to the following factors:

Weights

Data storage

Tuning parameter

Drops old data

Responds to shifts

Best for

Equal weight on last n periods

Must store n past observations

n (window size)

Completely, after n periods

After n periods, fully

Stable demand, no trend

Attributes of ES pertaining to the following factors:

Weights

Data storage

Tuning parameter

Drops old data

Responds to shifts

Best for

Exponentially decaying weights

Only last forecast + last demand

a (smoothing constant)

Gradually, never fully

Immediately (partially)

Stable demand, no trend

What is a limitation of both SMA and ES?

Neither handle trend or seasonality

Both will systematically under forecast trending demand and miss seasonal patterns

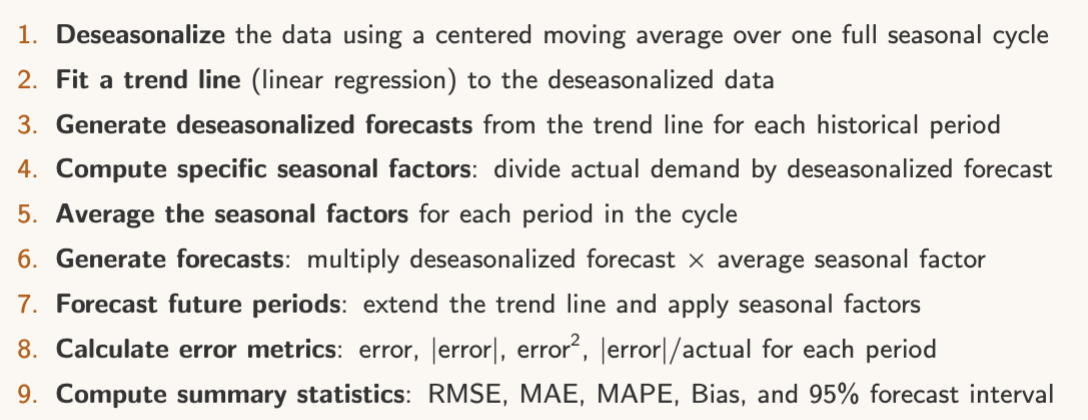

Static Decomposition Approach

What is the goal of the Static Decomposition Approach?

To separate demand into Level, Trend, and Seasonality, then recombine to forecast

Step-by-step Method for the Static Decomposition Approach

Remove seasonality to reveal the trend

Fit a line through the trend

Measure how each season deviates from the trend

Put it back together: trend x seasonal factor

A p-period moving average includes every season exactly once, so

Seasonal highs and lows cancel out

To deseasonalize we average over

One full cycle (p periods)

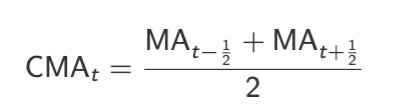

Where does an Odd average land after deseasonalizing ?

The middle one

Where does an Even average land after deseasonalizing ?

Falls between periods

Average two consecutive MAs to “center” at an actual period

Even Average Formula

Averages two offset windows to land on period t

Centering the Moving Average Formula

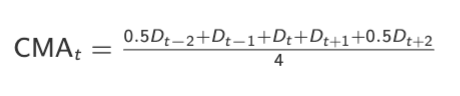

Shortcut formula for computing CMA

Step-by-step CMA Calculation

Compute the CMA

Find the trend

Use the CMA values from Step 1 to estimate a trend line via linear regression

=SLOPE(CMA, periods) and = INTERCEPT(CMA, periods)

What is a seasonal factor? What are the specific seasonal factors?

For each period, divide actual demand by the trend value [PICTURE]

Average the seasonal factors

Put it all together

![<ol><li><p>Compute the CMA</p></li><li><p>Find the trend</p></li></ol><ul><li><p>Use the CMA values from Step 1 to estimate a trend line via linear regression</p></li><li><p>=SLOPE(CMA, periods) and = INTERCEPT(CMA, periods)</p></li></ul><ol><li><p>What is a seasonal factor? What are the specific seasonal factors?</p></li></ol><ul><li><p>For each period, divide actual demand by the trend value [PICTURE]</p></li></ul><ol start="4"><li><p>Average the seasonal factors</p></li><li><p>Put it all together</p></li></ol><p></p><p></p>](https://assets.knowt.com/user-attachments/68e2f6ba-7a4c-4bcc-8e01-cf5de161a8f5.png)

When S>1

Demand is above trend (peak)

When S<1

Demand is below trend

Seasonal factor

Ratio of actual demand to trend

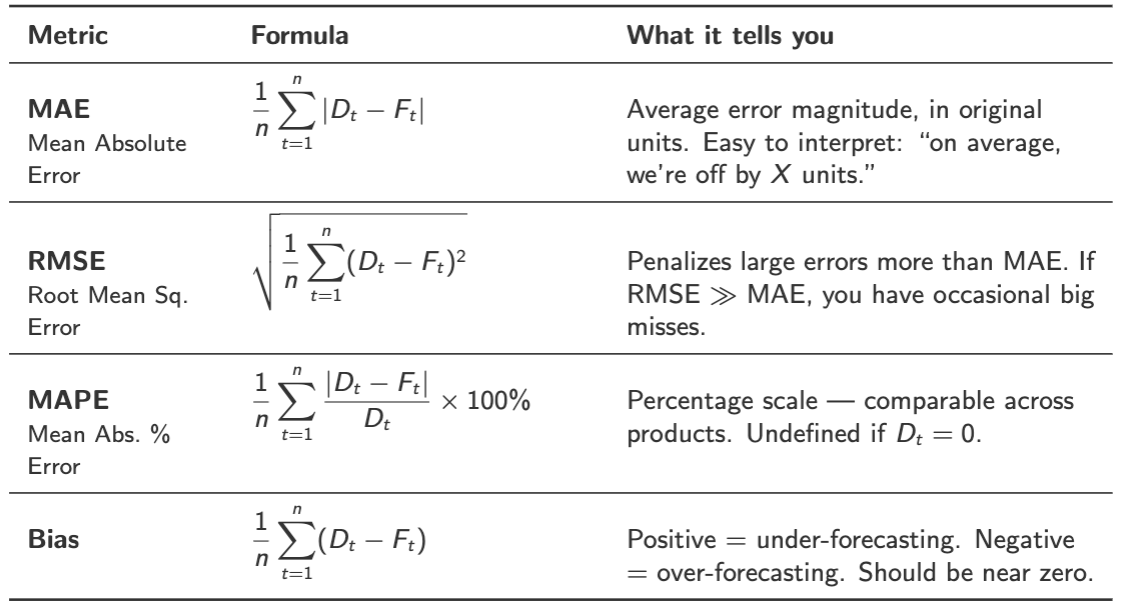

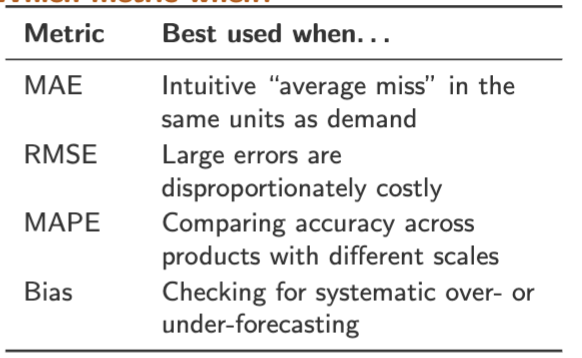

What are the four error metrics you needs and what do they tell you?

What are the four error metrics and when is each best put to use?

RMSE >= MAE always (True/False)

True

The bigger the gap, the more your errors are “spiky” rather than uniform

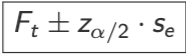

Forecast Interval

Gives a plausible range for demand

Forecast Interval Formula

Tracking Signal

Monitors whether errors are becoming systematically biased

Tracking Signal Formula

What does it mean if the TS ~= 0?

Errors show little cumulative signed bias

What does it mean if the TS > 0 and increasing?

Systematically under forecasting

What does it mean if the TS > 0 and decreasing?

Systematically overforecasting

If |TSt| exceeds a threshold (typically +- 6)

The forecast method needs attention

The tracking signal is a control chart for

Your forecast

It triggers an alarm when something systematic goes wrong

9 Step Process of Static Decomposition

Steps 1-7 build the forecast

Steps 8-9 tell you how much to trust it

Never skip steps 8-9

What are the 3 limitations of Static Decomposition?

Parameters are estimated once from all data

Doesn’t adapt as new data arrives

If the trend shifts or seasonal pattern changes, the forecast becomes stale

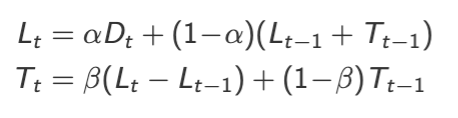

Holt’s Method Formula

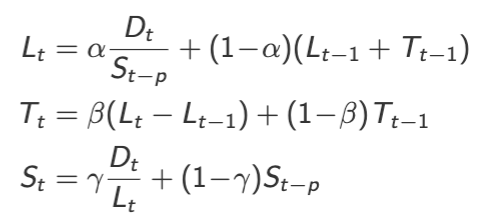

Holt’s Winters Formula

Under Holt’s Method, each component

Updates every period

Forecasts are always wrong (True/False)

True