Economics Module 1 definitions

1/33

Earn XP

Description and Tags

CAPE UNIT 1

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

34 Terms

Production Possibility Frontier

An economic model that illustrates the maximum possible outputs of two goods an economy can produce with its limited resources.

How does the Frontier illustrates scarcity?

The PPF illustrates the opportunity cost of producing one good over another, highlighting the concept of scarcity. Due to this, an economy must decide on what to produce, how to produce and who to produce it for.

Positive Statements

Objective, factual and can be tested and proven.

Normative Statements

Subjective and based on opinions, values and beliefs.

Cardinal Approach

Assumes that utility is quantifiable and can be measured numerically in units.

Ordinal Approach

Assumes that utility is a pschological phenomenon and cannot be measured but can be ranked in preference order.

Law of diminishing marginal utility

As an individual consumes an additional unit of a good/service, the marginal utility diminishes

Law of Equi Marginal Utility

States that a consumer will maximize their total satisfaction when the utility derived from the last dollar spent on each good is equal

Indifference curve

Shows all the different combinations of two goods that give a consumer the same level of satisfaction

Marginal rate of substitution

measures how much of one good a consumer is willing to give up in order to get one more unit of a another good while keep the overall satisfaction the same.

Budget Line

Shows all the combinations of two different goods a consumer can purchase with their limited income and the prices of those goods.

Consumer Equilibrium

Refers to the amount of goods a consumer can buy given his/her income and the prices of those goods.

A consumer is said to be in equilibrium when the budget line touches the highest possible indifference curve.

Normal Good

Products where demand increases when income increases

Eg: If you get a raise, you’ll purchase more steak and go to restaurants often.

Inferior Good

Goods where demand decreases when income increases

Eg: Instant ramen, instead of taking the bus you’ll purchase a car

Giffen good

A rare type of inferior good that defies the law of demand. When price goes up, demand increases.

This happens with absolute staples like bread or rice in very poor communities.

Substitute good

Pairs of goods that can be used in place of another. If the price of Good A goes up demand increases for Good B.

Eg: if the price for orange juice goes up the demand for apple juice increases.

Complementary goods

Products that are consumed together. if the price of good A goes up, demand for good B decreases

Eg: bun and cheese. if the price of bun goes up people will buy less cheese.

Movement along the demand curve

Result of a change in price of a good.

Fall in price ill result in an increase in QD, leading to an extension of the demand curve

Increase in price lead to a decrease in QD, causing the curve to contract.

Shift of the Demand Curve

A change in all other non price factor will cause a shift in the demand curve which ill result in a change in demand.

Factors that cause a shift to the right

An increase income

Increasing advertising

Improvement in product quality

Increase in population

Expectations of a price increase

Factors that cause a shift to the left

A decrease in income

Decrease in population

Decrease in advertisements

Expectation of price decrease

Decrease in product quality

Determinants of Demand

Price of good

Consumer income

Price of other good

Price Elasticity of Demand (PED)

Measures the responsiveness of quantity demanded to price.

Demand if elastic if the PED is greater than 1

Income Elasticity of Demand (YED)

Measures how quantity demanded for good changes in response to changes in consumer income

Cross Elasticity of demand (XED)

Measures how the quantity demanded of one good changes in response to a price change in another good.

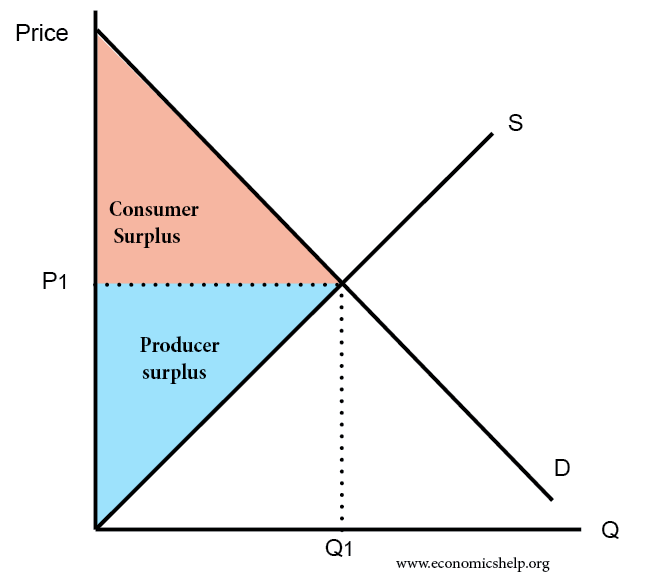

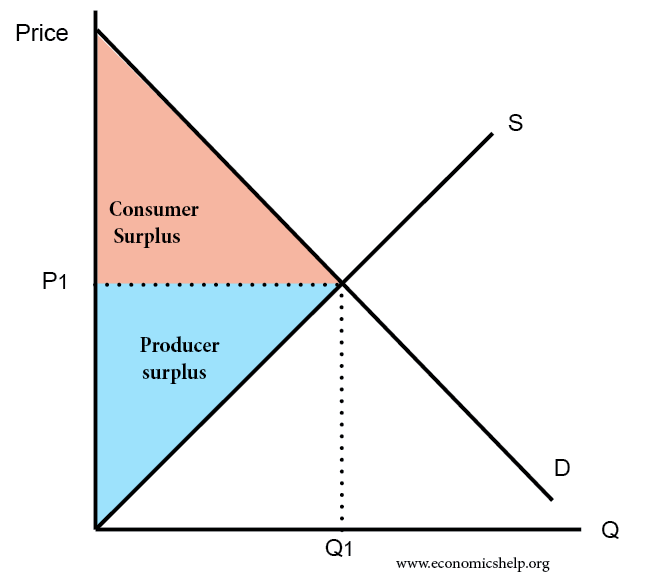

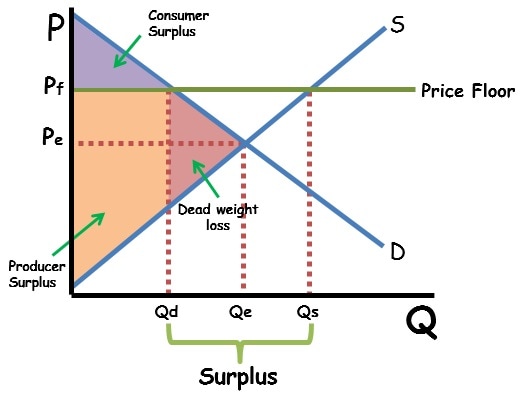

Producer Surplus

The difference between the price a producer actually receives for a product and the minimum amount they would have been willing to accept.

Consumer Surplus

The economic benefit consumers receive when they pay a price lower than the maximum they are willing to pay for a good or service

Market equilibrium

Refers to the state where quantity of goods or services demanded by consumers equal the quantity supplied by producers.

Price floor

A government imposed minimum price that can be charged on a good or service. It is set above market equilibrium. (minimum wage)

-Its purpose is to protect producers or workers by ensuring they receive stable income.

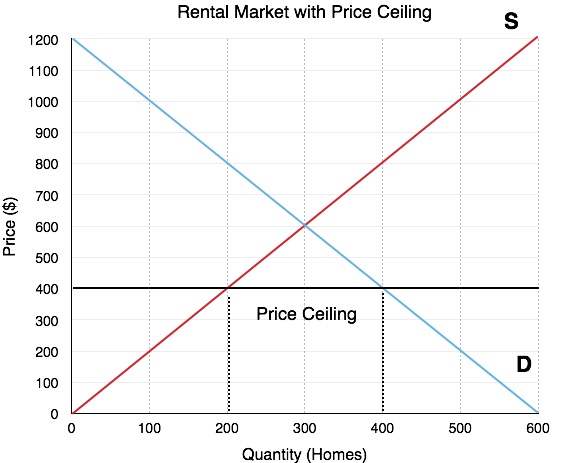

Price ceiling

A government imposed maximum price that can be charged on a good or service. It is set below market equilibrium.

Its purpose is to protect consumers by keeping essential goods and services affordable.