Purchase Order Processing

1/8

Earn XP

Description and Tags

MGTP 422

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

9 Terms

Authorization Controls (3)

purchase inventory based on actual inventory needs

need to have a purchase requisition before preparing a purchase order

authorize a department to look into inventory needs

non-inventory purchases (and purchase requisitions) must be approved by your department manager

use an approved vendor list when purchases

only buy from vendors on the list

if looking to purchase from diff vendor, must go through approval process to get them added

Segregation of Duties Controls (3)

authorization of inventory purchases is separate from purchase order processing

custody of inventory (receiving) is separate from recordkeeping (inventory control)

access to different accounting records should be separate

purchases journal, inventory subsidiary ledger and general ledger

purchases journal and AP journal can be updated by the same department bc we are not making and sending invoices

Supervision Controls (3)

authorization of payments (AP dept) is separate from payment of bills (cash disbursements dept)

custody of checks (cash disbursement group) is separate from recordkeeping (AP group)

when items are received, department supervisors take the packing slip and the receiving department takes the blind PO (shows what items were ordered and expected to be delivered; must count the goods received)

supervisor is to reconcile the packing slip and blind PO

Accounting Records Controls (2)

use prenumbered source documents w unique identifiers

maintain an adequate record of transactions

source documents

journals

purchases

cash disbursements

subsidiary ledgers

inventory

AP (if someone is paying on credit)

general ledger

files

supplier master

open/close PO

AP pending

open/close AP

Physical Access Controls (2)

physical access controls

access to inventory (direct) physically restricted

access to accounting records (indirect) is physically and logically restricted

access to cash/checks (indirect) is physically and logically restricted

computer based access controls

electronic records to be protected against un/authorized exposure

have logical and physical access controls

data and programs to be monitored and safeguarded

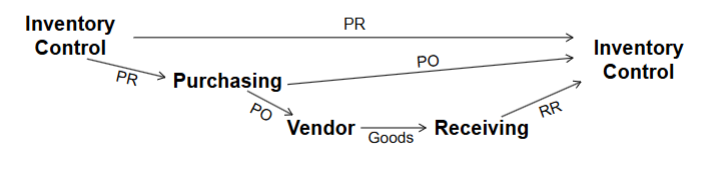

Independent Verification Controls - Inventory Control

reconcile purchase requisition, purchase order and receiving report

PR from inventory control

PO from purchasing (who got RP from inventory control)

RR from receiving (who got goods from vendor that got PO from receiving)

validation performed to ensure we ordered and received what was initially requested before recording an increase in inventory

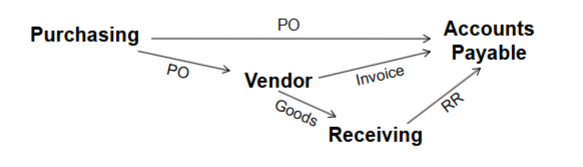

Independent Verification Controls - Accounts Payable

reconcile purchase order, invoice, and receiving report

PO from purchasing

invoice from vendor (who got PO from purchasing)

RR from receiving (who got PO from purchasing)

example of a 3 way match; checking that you are only paying for what you ordered/things received

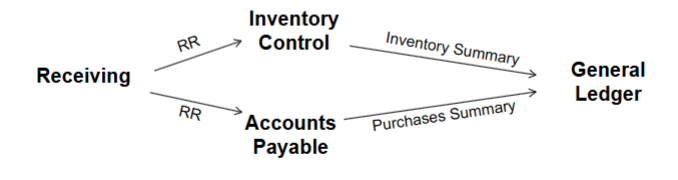

Independent Verification Controls - General Ledger

reconcile purchase summary and inventory summary

PS from AP (who got RR from receiving)

IS from inventory control (who got RR from receiving)

performed to validate that the total obligations recorded equal the total inventories received (+ control over inventory control and AP)

What is a voucher package and how is it used in purchase order controls?

voucher package: set of documents (purchase order, receiving report, and invoice) that are to be reconciled for a 3 way match

use this match when authorizing payment of bills

making sure you are only paying for what you received and what you ordered