Long-Term Assets (11.1, 11.2, 11.3)

1/42

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

43 Terms

How are assets categorized?

Current and long-term

Tangible and intangible

What is a tangible asset?

An economic resource that has physical substance.

Can be short-term or long-term.

What is the useful life of an asset?

The time period over which an asset cost is allocated.

What are fixed assets?

Long-term tangible assets.

On a company’s balance sheet, what can long-term tangible assets be listed as?

They are typically listed as noncurrent assets, but they are also listed under the category of Property, Plant, and Equipment, as well as sometimes being called fixed or plant assets.

What are intangible assets?

Assets that neither have a physical substance nor will be sold, but still provide rights to the owner and provide it an economic benefit.

How are intangible assets valued?

Because their value is very subjective, they are typically not shown on the balance sheet unless an event indicates its value objectively, like the purchase of an intangible asset.

What are the four types of intangible assets and all of their useful lives?

Patents; twenty years

Trademarks; renewed every decade

Copyrights; seventy years beyond creator’s death

Goodwill; indefinite

What is a patent?

A contract that provides a company exclusive rights to produce and sell a unique product; granted to the inventory for twenty years. Common within the pharmaceutical industry. Granted by the federal government.

What is a trademark?

An exclusive right to the name, term, or symbol that a company uses to identify itself or its products. This helps prevent impersonators from selling a product similar to another or using its name.

What is copyright?

It provides the exclusive right to reproduce and sell artistic, literary, or musical compositions.

What is goodwill?

The value of certain favorable factors that a business possesses that allows it to generate a greater rate of return or profit, e.g. superior management, a skilled workforce, qualiy products, and so on.

When do companies record goodwill?

When they acquire another business in which the purchase price is in excess of the fair value of the identifiable net assets, the difference is recorded as goodwill.

What is capitalization?

The process of recording an expenditure as an asset on the balance sheet rather than as an immediate expense, with the cost allocated over the asset’s useful life.

If a long-term asset is not used in daily operations and it is not planned to be used, how is it classified?

It is classified as an investment.

What other costs of an asset might be included along with its total cost?

Its shipping costs, taxes, assembly, legal fees, and so on.

What are investments?

A short-term or long-term asset that is not used in the day-to-day operations of a business and is not expected to be used up overtime.

How are repair and maintenance costs of PP&E accounted for?

They may be capitalized or expensed depending on the cost’s nature.

If it prolongs the asset’s life or improves its economic benefit, it is capitalized; otherwise, if it does not extend its original length, then it is expensed.

What are examples of expensed versus capitalized costs?

Expensed — Maintenance costs, normal repairs, etc..

Capitalized — An upgrade to a machine’s circuit board.

What is an asset’s historical (initial) cost?

All costs to acquire an asset and put it into use.

What are the two steps of an asset’s initial recording?

Record its initial purchase at cost and record it as an N/P, A/P, or cash outflow.

At the period’s end, make an adjusting entry to recognize the depreciation expense.

What is the journal entry to record the purchase of a fixed asset?

What is book value?

The asset’s original cost less accumulated depreciation.

What is useful life?

The length of time the asset will be productively used within operations.

What is salvage (residual) value? Evaluate how it is determined.

The price an asset’s will sell for when its useful life expires. Valuing salvage value is difficult because it requires anticipating what will occur in the future.

What is depreciable base (cost)?

The total depreciation expense over the asset’s useful life.

What is the entry to record depreciation expense?

What type of account is accumulated depreciation?

It is a contra-account.

Which long-term assets are not depreciated and why?

Land is not depreciated because it has an unlimited useful life.

What are the three methods of allocating depreciation expense?

The straight-line method, the units-of-production method, and the double-declining balance.

What is straight-line depreciation?

A method of depreciation that evenly splits depreciable amount across an asset’s useful life by dividing the depreciable base by the asset’s useful life.

What is the units-of-production depreciation?

Depreciation is based on actual usage of asset, which is more appropriate when an asset’s life is a function of usage. To calculate, useful life is expressed in terms of usage and depreciable base is divided by it.

What is double-declining balance depreciation? How is it calculated?

It is the most complex of the three since it accounts for both time and usage.

It determines the percentage of depreciation expense that would exist under straight-line depreciation (e.g. a five-year asset depreciates 20% a year).

The aforementioned percentage of depreciation expense is then doubled, and depreciation expense is found by multiplying the book value by this doubled percentage.

However, the depreciation expense is prevented from going below the estimated salvage value.

What is partial-year depreciation?

Depreciable assets that ear only owned for a portion of a year. In this case, depreciation expense is based on the number of months the asset is owned in a year.

What are some special issues in depreciation?

In some cases, depreciable assets can be used beyond their useful life, so long as the asset’s original cost is not exceeded.

What is depletion and what is an example of when it would be used? And what method of allocating depreciation is most often used with it?

Depletion is when a company’s assets are converted into a product. It might be used for natural resources (e.g. coal, wood, lumber, mineral deposits) that are turned into products and thereafter accounted for as inventory. The units-of-production method is used the most.

What is amortization?

It is like depreciation expense but for intangible assets.

How is amortization different from depreciation?

Amortization is only done with the straight-line method.

There is no salvage value for amortized assets.

There is no “accumulated amortization” account, since intangible assets are written down each period instead.

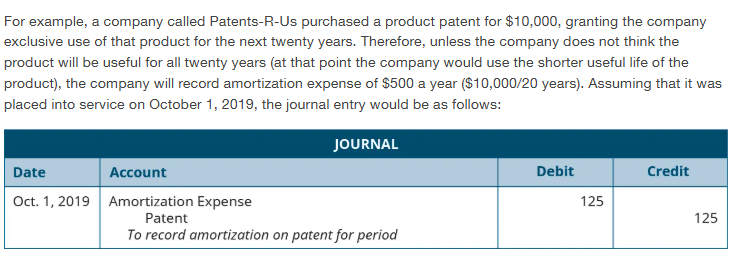

What would the entry for amortization be?

Explain how intangible assets are expensed.

Costs towards developing the assets are expensed, but anything that defends it (e.g. legal costs) are capitalized.

How is salvage value (or remaining life) revised?

Depreciation expense calculations must be recomputated.

What is functional obsolescence?

It is the reduction in use or value of an asset except those due to physical deteroriation. Useful life must be adjusted downwards, and an adjustment in salvage value may also be necessary.