Market Structures in Edexcel Economics A-Level

1/178

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

179 Terms

Allocative efficiency

Allocative efficiency occurs when resources are distributed to the goods and services that consumers want, maximising utility, and exists at P = MC.

Productive efficiency

This is when firms produce at the lowest point on the short run or long run average cost curve, where MC = AC.

Static efficiency

Allocative and productive efficiency are forms of static efficiency.

Dynamic efficiency

Dynamic efficiency is when all resources are allocated efficiently over time, leading to falling long run average costs.

X-inefficiency

A firm is x-inefficient when it is producing within the AC boundary, resulting in higher costs than would occur with competition.

Characteristics of perfect competition

A perfectly competitive market has many buyers and sellers, sellers are price takers, free entry and exit, perfect knowledge, homogeneous goods, firms are short run profit maximisers, and factors of production are perfectly mobile.

Market power in perfect competition

In a competitive market, profits are likely to be lower than in a market with only a few large firms due to small market share.

Short run supernormal profits

In the short run, firms in perfect competition can make supernormal profits.

Long run normal profits

In the long run, profits in perfect competition are competed away, resulting in only normal profits.

Price determination in perfect competition

In a competitive market, price is determined by the interaction of demand and supply.

Entry of new firms

If firms make a profit in a competitive market, new firms will enter due to low barriers to entry.

Effect of new firms on supply

The entry of new firms increases supply in the market, which lowers the average price.

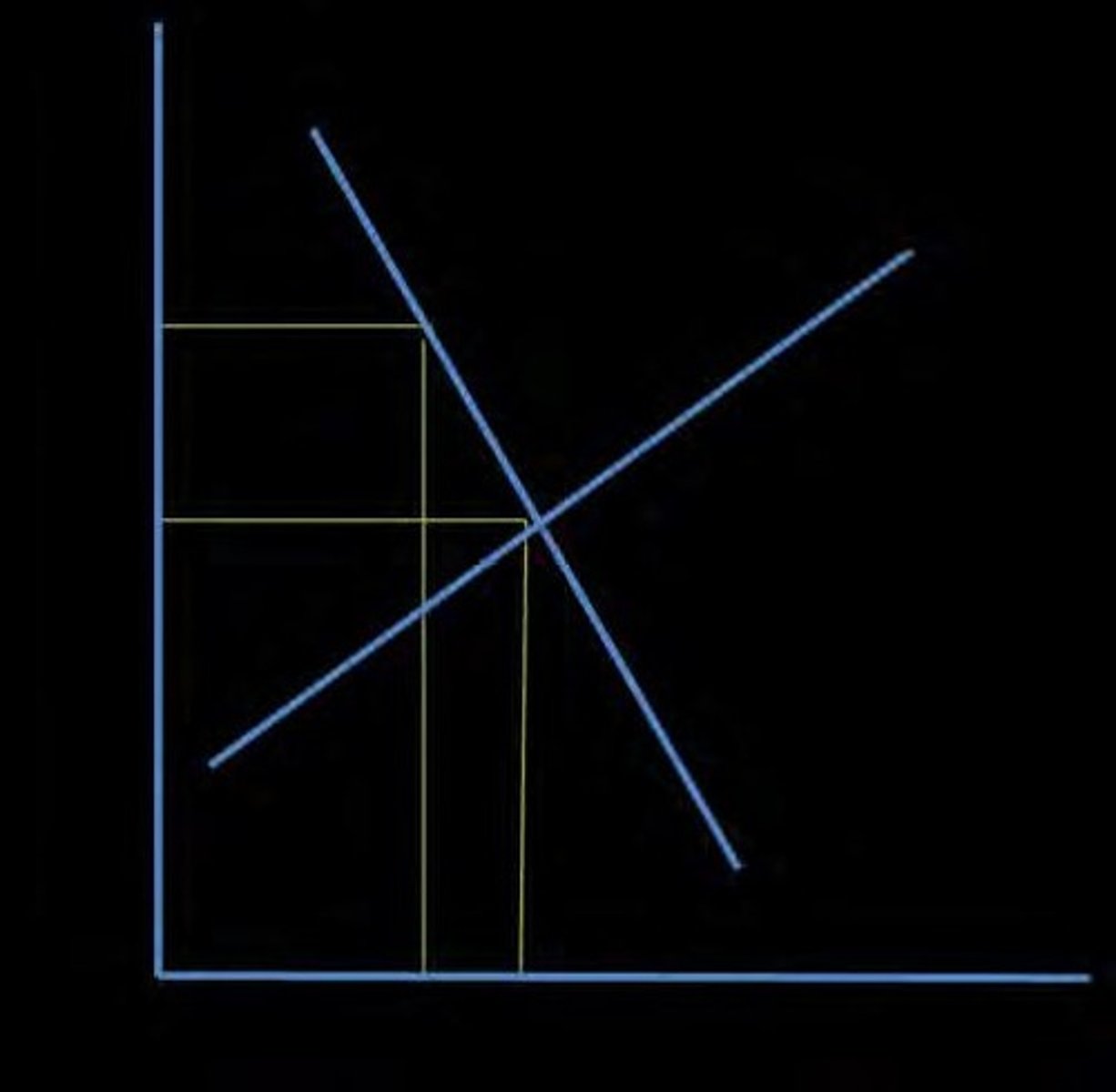

Short run equilibrium

In the short run equilibrium for a perfectly competitive market, the firm is a price taker and produces an output of Q1.

Supernormal profits area

The yellow shaded rectangle in the short run equilibrium diagram shows the area of supernormal profits earned.

Long run equilibrium

In the long run equilibrium, supernormal profits incentivise new firms to enter the industry.

Supply curve shift

The entry of new firms causes the supply curve to shift from S to S1, resulting in a lower price level.

Price acceptance

Since firms are price takers, they must accept the new, lower price after the supply curve shifts.

Free markets

Free markets are considered to be allocatively efficient.

MC curve and AC curve

The MC curve cuts the AC curve at the lowest point, indicating productive efficiency.

Trade-off in dynamic efficiency

Some firms face a trade-off between giving shareholders dividends and making an investment.

Factors affecting dynamic efficiency

Dynamic efficiency is affected by short run factors such as demand, interest rates, and past profitability.

Organisational slack

X-inefficiency could be due to organisational slack, a waste in the production process, poor management, or laziness.

Monopolies and x-inefficiency

Monopolies tend to be x-inefficient due to a lack of competition.

Investment lag

Dynamic efficiency can be evaluated by considering the long time lag between making an investment and achieving falling average costs.

Price Takers

Firms that must accept the market price.

Equilibrium

A state where supply equals demand, established in the long run.

Supernormal Profits

Profits exceeding normal profits, competed away in the long run.

Normal Profits

The minimum profit necessary for a firm to remain in the market.

Allocative Efficiency

Occurs when P = MC, leading to optimal resource allocation.

Dynamic Efficiency

Efficiency achieved through innovation and investment over time.

Economies of Scale

Cost advantages that firms experience as their scale of production increases.

Productive Efficiency

Occurs when firms produce at the lowest point on the AC curve.

Imperfect Competition

A market structure where firms have some control over prices.

Non-Homogeneous Products

Products that are differentiated by branding and features.

XED (Cross Elasticity of Demand)

Measures the responsiveness of the quantity demanded of one good to a change in the price of another good.

Market Power

The ability of a firm to influence the price of its product.

Downward Sloping Demand Curve

A demand curve that indicates that as price decreases, quantity demanded increases.

Imperfect Information

A situation where buyers and sellers do not have full knowledge of the market.

Short Run Profit Maximisation

Occurs at the point where MC = MR.

Price Elasticity of Demand

The degree to which the quantity demanded responds to a change in price.

Excess Capacity

When firms do not fully exploit their factors of production.

X-Inefficiency

Inefficiency that occurs when firms do not minimize their costs due to lack of competition.

High Barriers to Entry

Obstacles that make it difficult for new firms to enter a market.

High Concentration Ratio

A market structure where a small number of firms control a large market share.

Interdependence of Firms

A situation in an oligopoly where the actions of one firm affect the others.

Monopolistic Competition

A market structure characterized by many firms selling differentiated products.

Oligopoly

A market structure dominated by a small number of large firms.

Interdependence of firms

Firms are interdependent in an oligopoly, meaning that the actions of one firm affect another firm's behaviour.

Product differentiation

Firms differentiate their products from other firms using branding.

Concentration ratio

The concentration ratio of a market is the combined market share of the top few firms in a market.

4 firm concentration ratio

The market share of the 4 largest firms added together: 28.4% + 17.1% + 16.4% + 10.9% = 72.8%.

2 firm concentration ratio

The market share of the 2 largest firms added together: 28.4% + 17.1% = 45.5%.

Collusive behaviour

Collusive behaviour occurs if firms agree to work together on something, such as setting a price or fixing the quantity of output.

Effects of collusion

Collusion leads to a lower consumer surplus, higher prices, and greater profits for the firms colluding.

Incentives to collude

Firms in an oligopoly have a strong incentive to collude to maximise their own benefits and restrict output.

Conditions for collusion

Collusion is more likely to happen where there are only a few firms, they face similar costs, and there are high entry barriers.

Non-collusive behaviour

Non-collusive behaviour occurs when firms are competing, establishing a competitive oligopoly.

Overt collusion

Overt collusion is when a formal agreement is made between firms and is illegal in the EU, US, and several other countries.

Costs of collusion

There is a loss of consumer welfare, as prices are raised and output is reduced.

Benefits of collusion

Excess profits could be used for investment, which might improve efficiency in the long run.

Cartel

A cartel is a group of two or more firms which have agreed to control prices, limit output, or prevent the entrance of new firms into the market.

Example of a cartel

A famous example of a cartel is OPEC, which fixed their output of oil and controlled over 70% of the supply of oil in the world.

Consumer inertia

Consumer inertia refers to the tendency of consumers to continue purchasing from the same firms, contributing to market stability.

Market saturation

Market saturation occurs when a market is filled with products, making it difficult for firms to grow without taking market share from rivals.

Economies of scale

By increasing their size, firms can exploit economies of scale, which will lead to lower prices.

Allocative efficiency

A lower quantity supplied leads to a loss of allocative efficiency.

Inefficiency due to collusion

The absence of competition means efficiency falls, increasing the average cost of production.

Industry standards improvement

Industry standards could improve due to collaboration on technology, especially in the pharmaceutical industry and for car safety technology.

Duplicate research savings

Collusion saves on duplicate research and development.

Cartel

A group of firms that agree to control prices and limit output to increase profits.

Price leadership

A situation where one firm sets its prices and other firms follow suit.

Oligopoly

A market structure characterized by a small number of firms that have significant market power.

Game theory

A mathematical framework used to model strategic interactions between rational decision-makers.

Prisoner's Dilemma

A scenario in game theory illustrating how two individuals might not cooperate even if it is in their best interest.

Dominant strategy

The best option for a player regardless of what the other player chooses.

Nash equilibrium

A situation in game theory where no player can benefit by changing their strategy while the other players keep theirs unchanged.

Price war

A competitive situation where firms continuously lower prices to outdo each other.

Predatory pricing

An illegal strategy where a firm sets prices low to eliminate competition.

Limit pricing

A strategy where firms set prices low to deter new entrants into the market.

Non-price competition

Strategies that firms use to attract customers without changing prices.

Customer loyalty

The tendency of consumers to continue buying from a specific brand due to positive experiences.

Special offers

Promotions such as discounts or free gifts designed to attract customers.

Market share

The portion of a market controlled by a particular company or product.

Interdependence

A situation in which firms are affected by the actions of other firms in the market.

Price stability

A situation where prices remain relatively constant over time.

Consumer demand

The desire of consumers to purchase goods and services at given prices.

Average costs

The total cost of production divided by the number of goods produced.

Market conditions

The various factors that affect the supply and demand of goods and services.

Delivery times

The timeframes in which goods are delivered to consumers.

Loyalty cards

Cards issued by retailers that provide discounts or rewards to repeat customers.

Quality of customer service

The overall experience and satisfaction a customer receives when interacting with a company.

Dividing the market

A strategy where firms agree not to compete in each other's designated markets.

Uncertainty in oligopoly

The unpredictability of competitors' actions in a market dominated by a few firms.

Advertising and marketing

Used to make a brand more known and influence consumer preferences.

Sunk costs

Costs that are unrecoverable, which can be incurred if advertising spending is ineffective.

Brand loyalty

The tendency of consumers to remain committed to a brand, making demand more price inelastic.

Monopoly

A market structure characterized by a single seller dominating the market.

Profit maximisation

The goal of a monopolist to earn supernormal profits in both the short run and the long run.

Sole seller

A characteristic of a pure monopoly where one firm is the only seller in the market.

High barriers to entry

Obstacles that prevent new competitors from easily entering an industry or area of business.