engineering econ final: effective interest, debt management

1/87

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

88 Terms

What is a nominal interest rate?

The quoted annual interest rate (APR), not accounting for compounding effects.

What is another name for nominal interest rate?

Annual Percentage Rate (APR).

Does the nominal rate include compounding effects?

No, it is simply a stated or “advertised” rate.

What is an effective interest rate?

The actual interest earned or paid after accounting for compounding.

What is another name for effective interest rate?

Annual Percentage Yield (APY).

Which rate is usually larger, nominal or effective?

Effective rate (when compounding occurs more than once per year).

When are nominal and effective rates equal?

When compounding occurs annually.

What is compounding?

The process of earning interest on both principal and previously earned interest.

Why does more frequent compounding increase interest?

Because interest is earned more often on smaller time intervals.

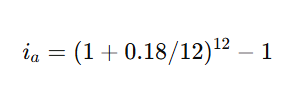

What does “18% APR compounded monthly” mean?

The 18% annual rate is divided into 12 monthly rates.

How do you convert APR to periodic interest rate?

i=APR/m

where m = number of compounding periods per year.

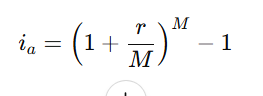

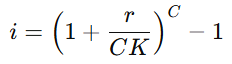

What is the formula for effective annual interest rate?

m: number of interest compounding periods per year

r: nominal interest rate (APR)

What does m represent in the effective rate formula?

Number of compounding periods per year.

Why does effective interest rate use exponentiation?

Because interest compounds over multiple periods.

In an 18% APR compounded monthly, what is the monthly interest rate?

18%/12=1.5% per month

Why is credit card interest expensive even if APR seems moderate?

Because compounding happens monthly, increasing total interest paid.

What does effective interest rate tell you in real terms?

The actual yearly cost of borrowing or return on investment.

What is the key difference between APR and APY?

APR ignores compounding; APY includes compounding.

When does borrowing become more expensive than expected?

When compounding occurs more frequently than annually.

What is the correct APY formula setup for 18% monthly compounding?

Why do we calculate effective interest per payment period? not annually!

Because payments may not occur annually (e.g., monthly or quarterly).

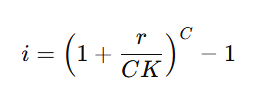

What is the formula for effective interest per payment period?

What does CCC represent?

Number of compounding periods per payment period.

What does K represent?

Number of payment periods per year.

What does CK represent?

Total number of compounding periods per year (M).

What is the relationship between M, C, and K?

M=C*K

Why do we sometimes use two different formulas for effective interest?

One is for annual rate (APY), the other for non-annual payment periods.

What is the key idea behind effective interest per payment period?

Matching interest calculation to actual timing of cash flows.

A payment period is the

length of time between consecutive payments in a cash flow problem.

If a loan has:

Monthly payments → payment period =

Quarterly payments → payment period =

Annual payments → payment period =

1 month

3 months

1 year

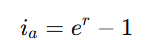

What is continuous compounding?

Interest that compounds an infinite number of times per year (as compounding frequency → ∞).

What happens mathematically as compounding frequency increases without limit?

The discrete compounding formula approaches an exponential function.

What is the formula for annual effective interest rate under continuous compounding?

What does r represent in continuous compounding?

The nominal interest rate (APR in decimal form).

What is the formula for non-annual effective interest rate under continuous compounding?

i= (e^r)^1/K -1

What is the effective annual rate for 8% compounded continuously?

ia=e^0.08−1≈8.3287%

Find APY for 8% compounded monthly.

ia=(1+0.08/12)^12−1=8.3000%

Find APY for 8% compounded weekly.

ia=(1+0.08/52)^52−1=8.3220%

For 8% compounded monthly, what are values of C and K (quarterly)?

C = 3 (3 months per quarter)

K = 4 (quarters per year)

Effective quarterly rate for 8% compounded monthly?

i=(1+0.08/12)^3−1=2.0134%

For 8% compounded weekly, what is C and K (quarterly)?

C = 13 weeks per quarter

K = 4 quarters per year

Effective quarterly rate for 8% compounded weekly?

i=(1+0.08/52)^13−1=2.0186%

What is C for daily compounding (quarterly rate)?

C = 365/4 = 91.25 days per quarter

Effective quarterly rate for 8% compounded daily?

i=(1+0.08/365)^91.25−1=2.0199%

What are the two main types of interest equivalence problems?

Same compounding and payment periods

Different compounding and payment periods

Step 1 when compounding = payment periods?

Identify number of periods per year (M = K).

Step 2 when compounding = payment periods?

Compute per-period interest:

i=r/M

Step 3 in same-period problems?

Compute total periods:

N=M×(years)

Step 4 in same-period problems?

Use i and N in cash flow equivalence formulas.

When do we use the unequal compounding & payment period method?

When interest compounding periods and payment periods are different.

What is the main goal when compounding ≠ payment periods?

Convert everything into a consistent effective interest rate per payment period.

What are the three key quantities you must identify first?

M = compounding periods per year

K = payment periods per year

C = compounding periods per payment period

What is Step 1 in solving unequal period problems?

Identify M, K, and C.

What is Step 2 in the solution method?

Compute effective interest rate per payment period.

General formula for effective interest per payment period?

What is Step 3 in the method?

Compute total number of payment periods.

Formula for total number of payment periods?

N=K×(years)

What does N represent?

Total number of cash flow periods.

What is Step 4 in solving these problems?

Use i and N in engineering economy equivalence formulas.

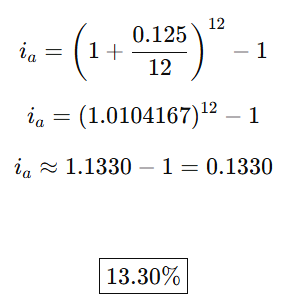

if your credit card calculates interest based on a 12.5% APR compounded monthly, what is your monthly interest rate and annual effective interest rate?

Your current outstanding balance is $2000. You are allowed to skip

payments for 2 months; what would your balance be two months from

now?

monthly interest rate: 12.5/12 = 1.0417%

annual effective interest rate:

balance two months from now:

F=P(1+i)^n

F=2000(1+.0104167)² = 2041.88

Suppose your savings account pays 9% Compounded Quarterly. If you deposit $10,000, how much will you have in one year?

i= .09/4= .0225

N=4 quarters in one year

F=10,000(1.0225)^4

=10,931

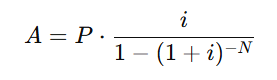

given: P=20000, r=8.5% per year, K=12 payments per year, N=48 payment periods, find A

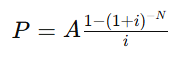

assume monthly compounding from this data

C=1

i=.085/12=.0070833

solve using formula

solve quarterly

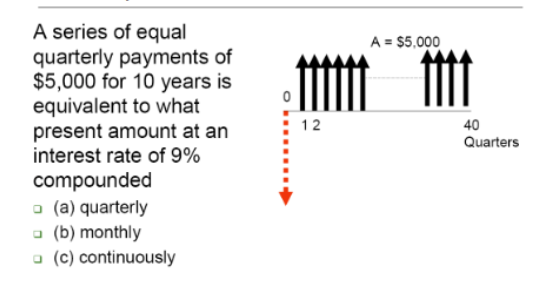

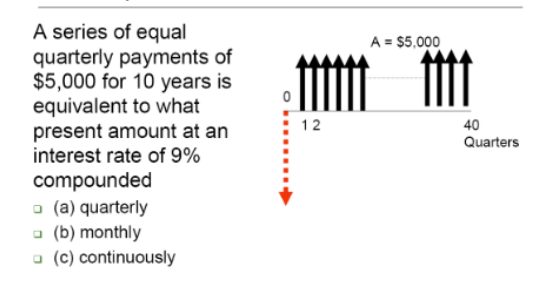

equal quarterly payments compounded quarterly : C=1

quarterly: N=10×4=40 quarters

i=.09/4 = .0225

solve for P

solve monthly

equal quarterly payments compounded monthly: C=3 (3 months in a quarter)

N=10×12=120 months

i=.09/12 = .0075

iq=(1.0075)³-1 = .02257

solve for P

solve continuously

iq= e^.09/4 -1 = .02275

solve for P

when can you use i=r/M?

when C=1

what would be P?

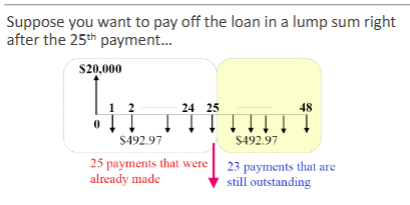

after calculating A=$492.97, use P=$492.97(P/A, .7083%, 23)

23 months is what is remaining

=$10,428.96

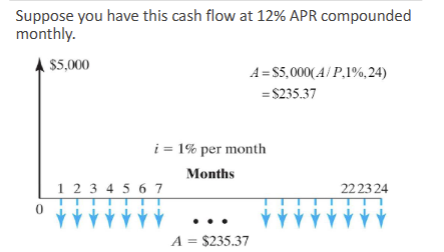

considering the 7th payment: how much goes to interest and how much goes to principal?

A=5000(A/P,1%,24)

=$235.37 = equal monthly payment

calculate outstanding balance after previous month (month 6)

P6= 235.37(P/A,1%,18) because 18 periods are left = $3859.66

using the outstanding balance, calculate interest charged on that balance in the next period

IP7= 3859.66(.01)= 38.60

calculate the principal payment by subtracting the interest from the total monthly payment

235.37-38.60 = $196.77

Suppose you have received a credit card offer from a bank that charges interest at 1.3% per month, compounded monthly.

What is the nominal interest (annual percentage) rate for this credit card? What is the effective annual interest rate?

Find the effective interest rate per payment period for an interest rate of

6% compounded monthly for each of the given payment schedule:

(a) Monthly

(b) Quarterly

(c) Semiannually

(d) Annually

do monthly

Find the effective interest rate per payment period for an interest rate of

6% compounded monthly for each of the given payment schedule:

(a) Monthly

(b) Quarterly

(c) Semiannually

(d) Annually

do quarterly

Find the effective interest rate per payment period for an interest rate of

6% compounded monthly for each of the given payment schedule:

(a) Monthly

(b) Quarterly

(c) Semiannually

(d) Annually

do semiannually

Find the effective interest rate per payment period for an interest rate of

6% compounded monthly for each of the given payment schedule:

(a) Monthly

(b) Quarterly

(c) Semiannually

(d) Annually

do annually

What is the future worth of each of the given series of payments?

(a) $10,000 at the end of each six-month period for 10 years at 8% compounded semiannually.

What is the future worth of each of the given series of payments?

(b) $9,000 at the end of each quarter for six years at 8% compounded quarterly.

What is the future worth of each of the given series of payments?

(c) $5,000 at the end of each month for 14 years at 9% compounded monthly.

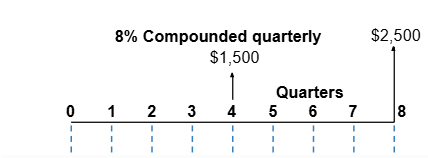

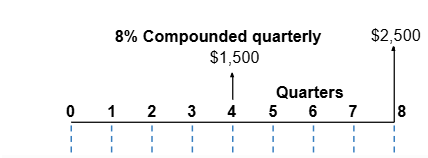

What is the amount of the quarterly deposits A such that you will be able to withdraw the amounts shown in the cash flow diagram if the interest rate is 8% compounded quarterly?

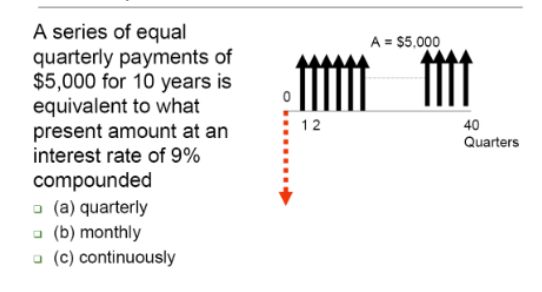

Suppose that $4,000 is placed in a bank account at the end of each quarter over the next 10 years. What is the future worth at the end of 10 years when the interest rate is 9% compounded at the given intervals?

(a) Quarterly

Suppose that $4,000 is placed in a bank account at the end of each quarter over the next 10 years. What is the future worth at the end of 10 years when the interest rate is 9% compounded at the given intervals?

b) monthly

Suppose that $4,000 is placed in a bank account at the end of each quarter over the next 10 years. What is the future worth at the end of 10 years when the interest rate is 9% compounded at the given intervals?

c) continuously

Suppose you take out a car loan of $10,000 with an interest rate of

12% compounded monthly. You will pay off the loan over 48 months with equal monthly payments.

what is the monthly interest rate?

Suppose you take out a car loan of $10,000 with an interest rate of

12% compounded monthly. You will pay off the loan over 48 months with equal monthly payments.

what is the amount of the equal monthly payment?

Suppose you take out a car loan of $10,000 with an interest rate of

12% compounded monthly. You will pay off the loan over 48 months with equal monthly payments.

what is the interest payment for the 20th payment?

Suppose you take out a car loan of $10,000 with an interest rate of

12% compounded monthly. You will pay off the loan over 48 months with equal monthly payments.

what is the total interest paid over the life of the loan?

Clay Harden borrowed $25,000 from a bank at an interest rate of 9% compounded monthly. The loan will be repaid in 36 equal monthly installments over three years. Immediately after his 20th payment, Clay desires to pay the remainder of the loan in a single payment. Compute the total amount he must pay.

Emily Wang financed her office furniture from a furniture dealer. The dealer's terms allowed her to defer payments (including interest) for six months and to make 36 equal end-of-month payments thereafter. The original note was for $15,000,with interest at 9% compounded monthly. After 26 monthly payments, Emily found herself in a financial bind and went to a loan company for assistance. The loan company offered to pay her debts in one lump sum if she would pay the company $186.00 per month for the next 30 months.

determine the original monthly payment made to the furniture store.

Emily Wang financed her office furniture from a furniture dealer. The dealer's terms allowed her to defer payments (including interest) for six months and to make 36 equal end-of-month payments thereafter. The original note was for $15,000,with interest at 9% compounded monthly. After 26 monthly payments, Emily found herself in a financial bind and went to a loan company for assistance. The loan company offered to pay her debts in one lump sum if she would pay the company $186.00 per month for the next 30 months.

determine the lump-sum payoff amount the loan company will make.

Emily Wang financed her office furniture from a furniture dealer. The dealer's terms allowed her to defer payments (including interest) for six months and to make 36 equal end-of-month payments thereafter. The original note was for $15,000,with interest at 9% compounded monthly. After 26 monthly payments, Emily found herself in a financial bind and went to a loan company for assistance. The loan company offered to pay her debts in one lump sum if she would pay the company $186.00 per month for the next 30 months.

what monthly rate of interest is the loan company charging on this loan?