Derivate Securities

1/191

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

192 Terms

Stochastic Processes

Describes how variables like stock prices, exchange rates, or interest rates change through time, incorporating uncertainties

Markov Processes

A process where future movements depend only on the current state, not the history of how that state was reached

Weak-Form Market Efficiency

The assertion that technical analysis (using past price history) cannot produce consistently superior returns

Stationary Process

A process where the parameters do not change over time

Continuous Stochastic Process

A process defined by taking the limits of time intervals as they tend toward zero.

Wiener Process

A specific type of Markov stochastic process with a mean change of 0 and a variance rate of 1 per year

Generalized Wiener Process

A Wiener process where the drift rate and variance rate can be set to chosen constants

Drift Rate

The average change per unit of time

Variance Rate

The variance of the change per unit of time

Itô Process

A generalized Wiener process where the drift and variance rates are functions of both the variable and time

Itô’s Lemma

A mathematical theorem used to find the stochastic process followed by a function of a variable that itself follows an Itô process

Geometric Brownian Motion

A specific Itô process used for stock prices where the expected percentage change (not actual dollar change) is constant.

Lognormal Distribution

The distribution followed by stock prices, derived from the assumption that stock returns are normally distributed

Continuously Compounded Return

The realized annual return when compounding occurs constantly

Volatility (σ)

The standard deviation of the continuously compounded rate of return in one year

Historical Volatility

An estimate of volatility calculated from historical stock price observations

Trading Days

The days a market is open for trading; options are usually valued assuming 252 trading days per year

Call Option

An option to buy an asset

Put Option

An option to sell an asset

European Option

Can be exercised only at the end of its life

American Option

Can be exercised at any time during its life

Strike Price (K)

The price at which the option holder can buy or sell the underlying asset

Option Positions

Including Long Call, Long Put, Short Call (writing a call), and Short Put (writing a put)

Moneyness

Categorized as At-the-money, In-the-money, or Out-of-the-money

Intrinsic Value

The value an option would have if it were exercised immediately

Time Value

The part of an option's price not accounted for by its intrinsic value

Option Class

All options of the same type (calls or puts) on the same stock

Option Series

All options of a certain class with the same expiration date and strike price.

Warrants

Options issued by a corporation or financial institution, representing a Primary Market Action

Black-Scholes-Merton (BSM) Differential Equation

The fundamental equation used to price options based on a riskless portfolio of the stock and the derivative

Arbitrage

The practice of selling a "rich" portfolio and buying a "cheap" portfolio to lock in a riskless profit

Law of One Price

Two portfolios paying the same amount in every state of the world must have the same price

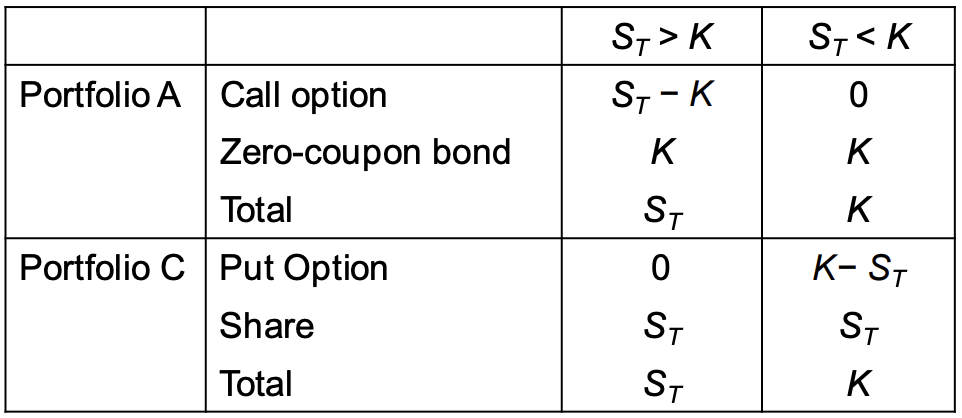

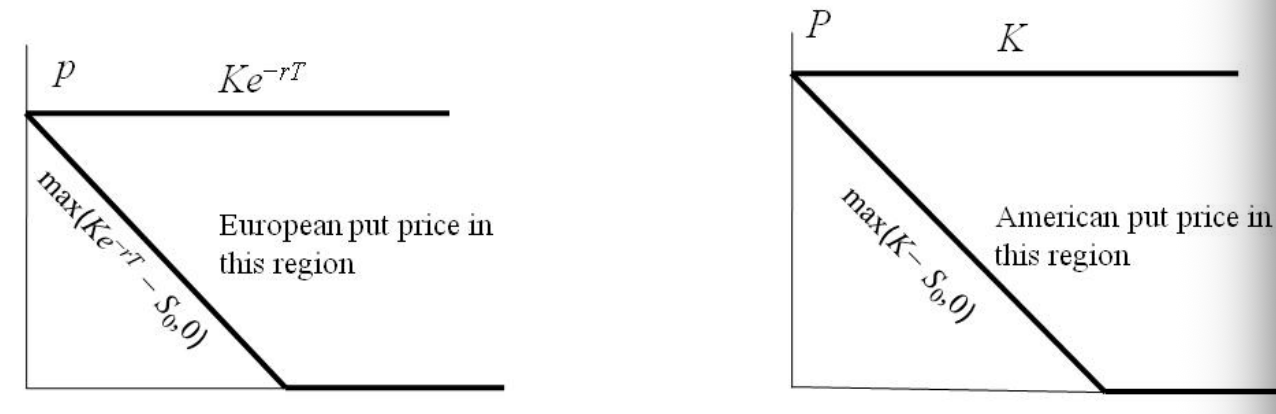

Lower Bound

The minimum theoretical price for an option

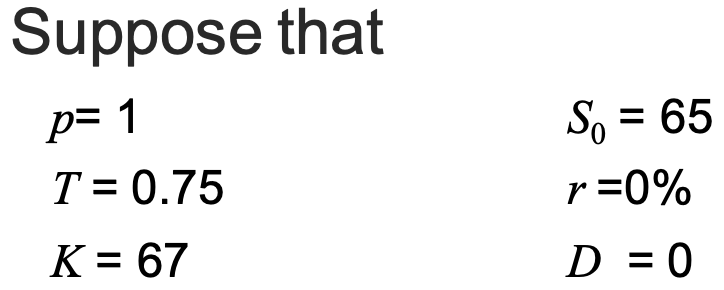

Put-Call Parity

The relationship between the price of a European call, a European put, the underlying stock, and a risk-free bond

Early Exercise

Exercising an American option before its expiration date

Principal Protected Note

A strategy combining a zero-coupon bond and an option to take a risky position without risking the original principal

Spread

A strategy involving two or more options of the same type (e.g., Bull Spread, Bear Spread, or Butterfly Spread)

Combination

A strategy involving options of different types (e.g., Straddle or Strangle)

Binomial Model / Binomial Trees

A model for valuing derivatives by assuming stock prices move to one of two possible values over discrete time steps

Risk-Neutral Valuation

The principle that derivatives can be valued by assuming the expected return on all assets is the risk-free rate

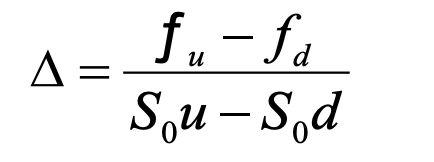

Delta (Δ)

The ratio of the change in the price of an option to the change in the price of the underlying stock

put-call parity formula

c: European call option price

p: European put option price

S0: Stock price today

K: Strike price

r: Risk-free rate for maturity T with continuous compounding

T: Life of the option

e−rT: The discount factor used to find the present value of the strike price

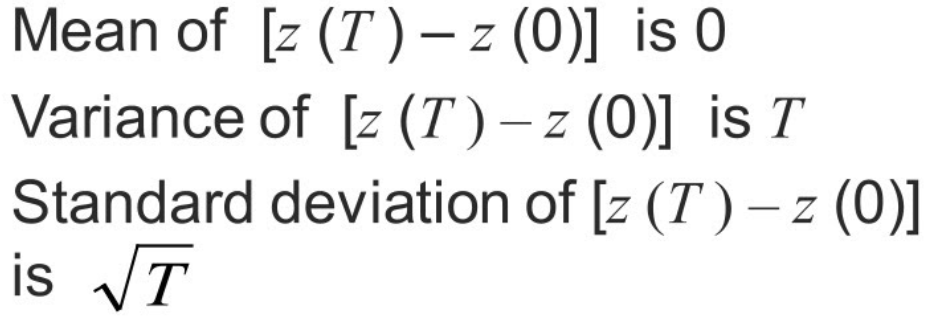

the std and variances in the Markov process

the variances are additive

Standard deviations are not additive

because the Markov process changes in successive periods of time are independent

Stochastic and Markov Processes

variables change through time with uncertainty

future price movements depend only on the current price, not the historical path. This assumption is consistent with weak-form market efficiency

Wiener and Itô Processes

Wiener process as a specific Markov process with a mean change of zero and a variance rate of one.

An Itô process generalizes this by making drift and variance functions of time and the underlying variable.

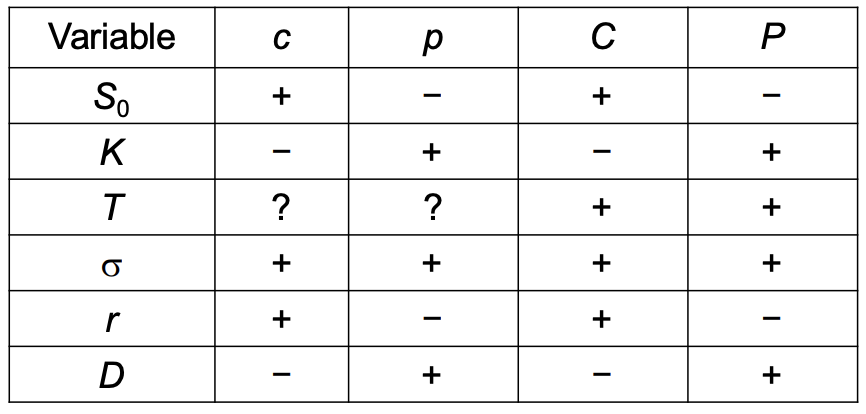

Pricing Variables

the current stock price (S0),

strike price (K),

time to maturity (T),

volatility (σ),

the risk-free interest rate (r),

and dividends (D

Call Options: In-the-Money

A call option is in-the-money when the stock price is greater than the strike price (S>K). In this state, the option holder can buy the stock for less than its current market value, resulting in a positive payoff

Call Options: Out-of-the-Money

A call option is out-of-the-money when the stock price is less than the strike price (S<K). In this scenario, the option has no immediate payoff because the holder would not choose to buy the stock at a strike price that is higher than the current market price

Put Options: In-the-Money

A put option is in-the-money when the stock price is less than the strike price (S<K). This allows the holder to sell the stock for more than its current market value, creating a positive payoff

Put Options: Out-of-the-Money

A put option is out-of-the-money when the stock price is greater than the strike price (S>K). The option has no intrinsic value because the holder could sell the stock on the open market for a higher price than the strike price

At-the-Money

An option is at-the-money when the current stock price is equal to the strike price (S=K). For example, if a stock portfolio is currently worth $1,000, an "at-the-money" call option would also have a strike price of $1,000

Early Exercise Logic

An American call option on a non-dividend-paying stock should never be exercised early

his is because exercising early sacrifices the insurance against the stock price falling and loses the time value of money on the strike price

American puts may be exercised early under certain conditions

The Law of One Price

Arbitrage is the practice of buying a "cheap" portfolio and selling a "rich" one to lock in riskless profit; if two portfolios provide the same payoff in all future states, they must have the same price today

Put-Call Parity

For European options, there is a fixed relationship between call and put prices: c+Ke−rT=p+S0. If this equality does not hold, an arbitrage opportunity exists

The Differential Equation

By assuming this riskless portfolio must earn the risk-free rate, the BSM differential equation is derived, which is used to value derivatives based on the price of the underlying asset and time

Principal Protected Notes structure

Typically combines a zero-coupon bond (which pays the original principal at maturity) with an at-the-money call option.

Performance Factors: The viability of this note depends on interest rates, the volat

ility of the portfolio, and dividend levels

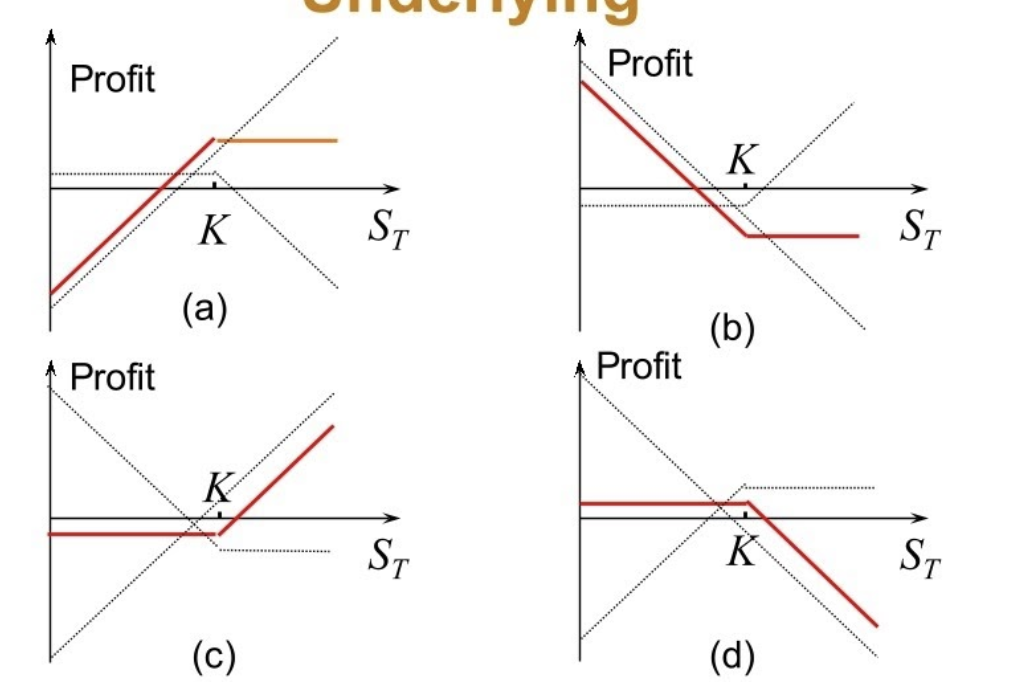

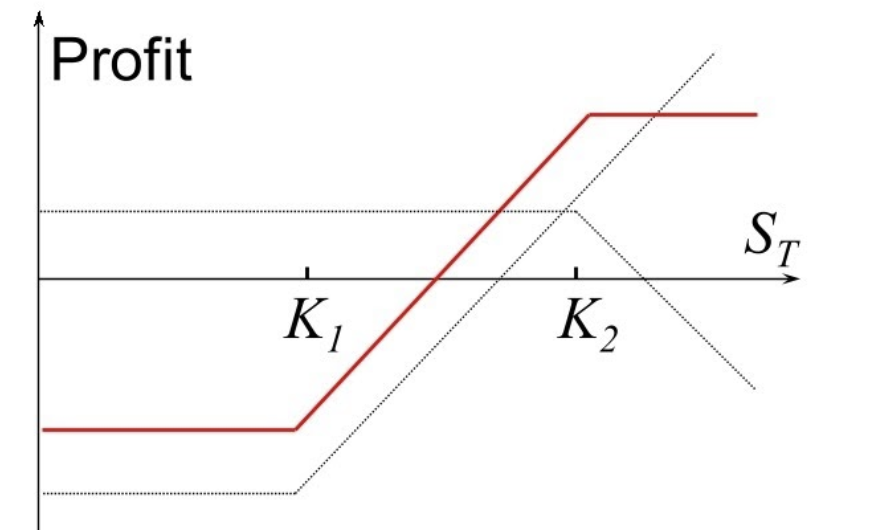

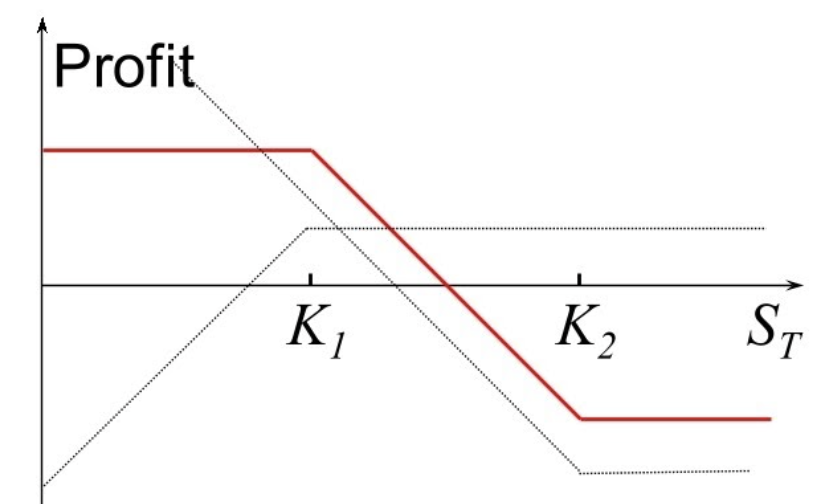

Bull Spreads

Created using either calls or puts. involves being long a call with a lower strike price (K1) and short a call with a higher strike price (K2)

Bear Spreads

Designed to profit from falling prices, these can also be created using either calls or puts

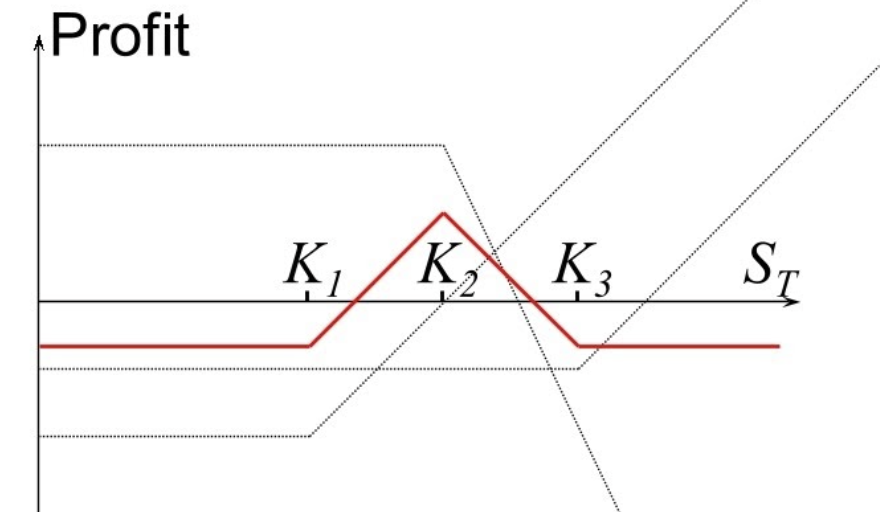

Butterfly Spreads

These utilize three different strike prices (K1,K2,K3) and can be constructed using either all calls or all puts

Combinations

involves taking positions in two or more options of different types (mixing calls and puts)

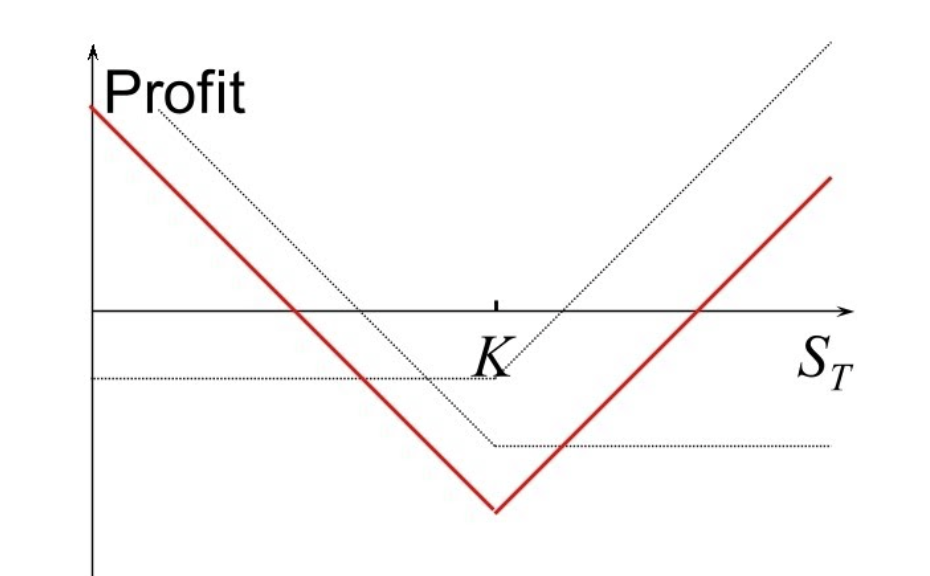

Straddle combination

Involves being long both a call and a put with the same strike price (K) and expiration date

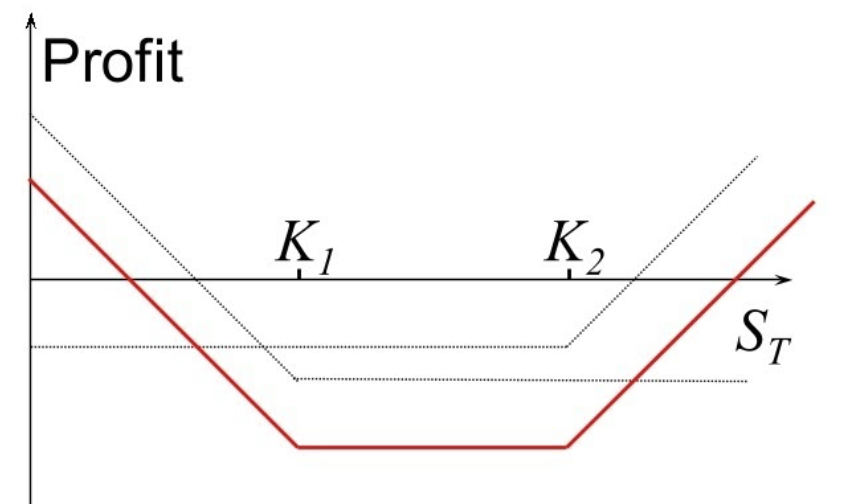

Strangle Combination

Similar to a straddle, but the call and put have different strike prices (K1 and K2)

Arbitrage

This is the core strategy of identifying and exploiting price discrepancies. It involves selling a "rich" (overpriced) portfolio and buying a "cheap" (underpriced) portfolio to lock in a riskless profit

Riskless Hedging

Used in the derivation of the Black-Scholes-Merton model and Binomial Trees, this strategy involves forming a portfolio of a stock and its derivative (like shorting a call and buying Δ shares) to eliminate uncertainty and earn the risk-free rate

why do options have value?

They allow you to delay a decision until you have better information

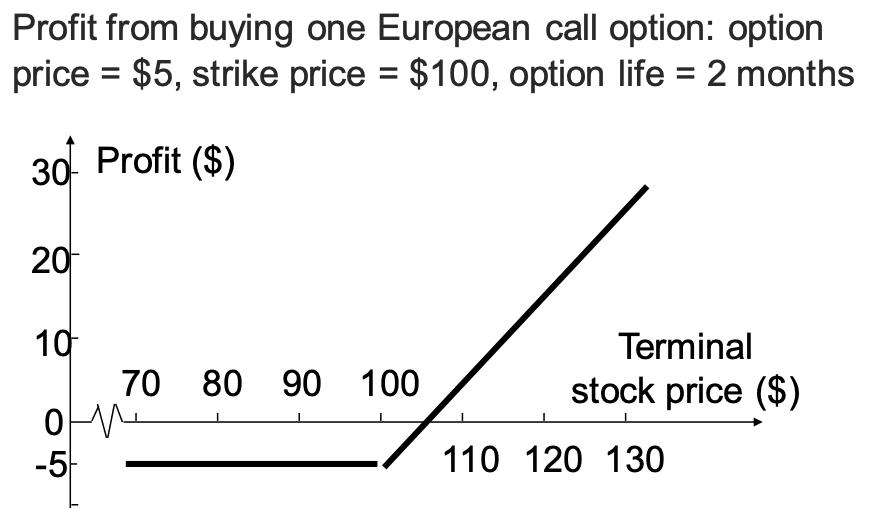

Long call

Payoff moves one-for-one if S>K

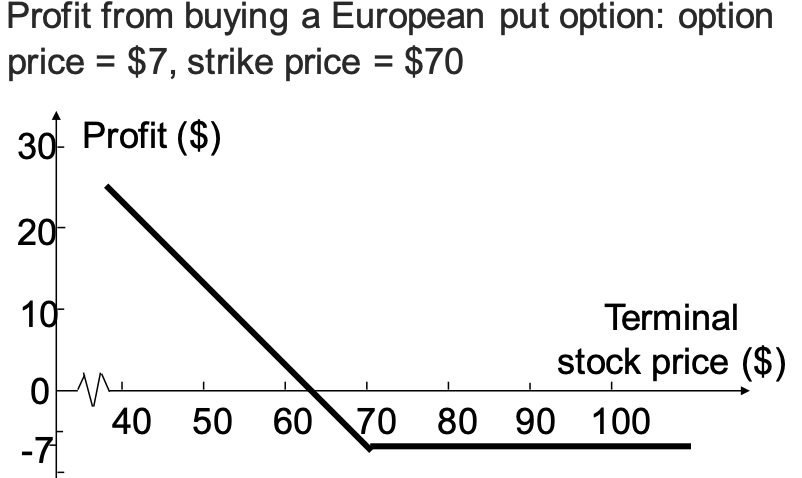

Long put

Payoff moves minus one-for-one if S

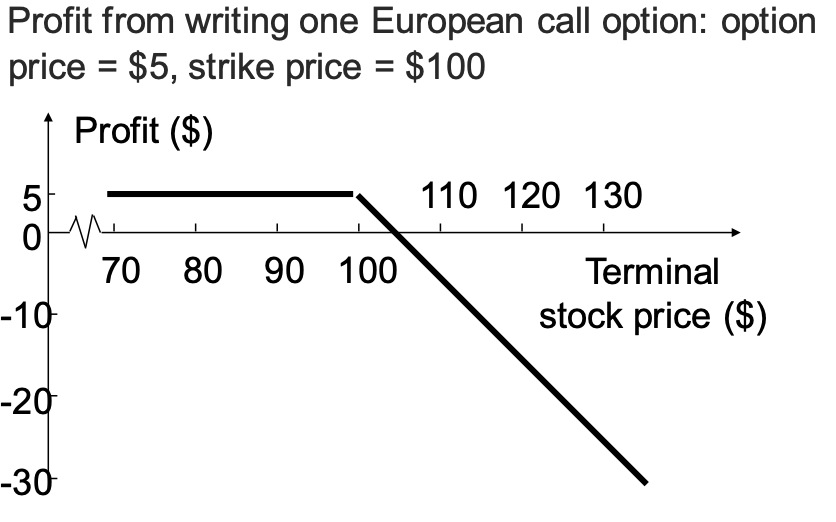

Short call

Opposite of long call S>K

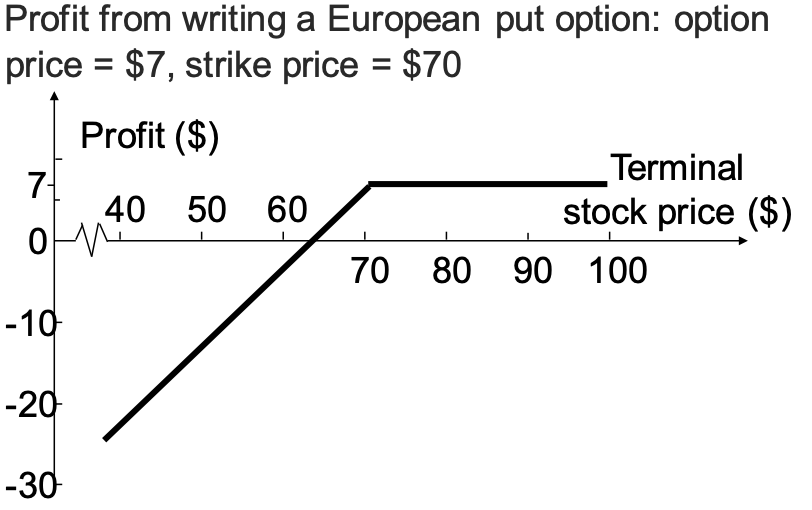

Short put

Opposite of long put S<K

Suppose you own N options with a strike price of K : When there is an n-for-m stock split,

the strike price is reduced to mK/n

the no. of options is increased to nN/m

effect of variables on option pricing

If the stock price decreases, the value of a call option will:

Decrease

Two portfolios that pay the same amount in each state of the world should have

the same price

Barring other financial market frictions

Law of One Price

An American option is worth

at least as much as the corresponding European option C ≥ c P ≥ p

Arbitrage opportunity of at least $1

values of portfolios

early exercise exception

is an American call on a non-dividend paying stock • This should never be exercised early!

No income is sacrificed

You delay paying the strike price

Holding the call provides insurance against the stock price falling below the strike price

Bounds for European and American Put Options (No Dividends)

Extensions of Put-Call Parity American options; D = 0

S0 − K < C − P < S0 − Ke−rT

Extensions of Put-Call Parity European options; D > 0

c + D + Ke −rT = p + S0

Extensions of Put-Call Parity American options; D > 0

S0 − D − K < C − P < S0 − Ke −rT

Strategies to be Considered

Bond plus option to create principal protected note

Stock plus option

Two or more options of the same type (a spread)

Two or more options of different types (a combination)

Principal Protected Notes: Viability depends on

Level of dividends

Level of interest rates

Volatility of the portfolio

Principal Protected Notes: Variations on standard product

Out of the money strike price

Caps on investor return

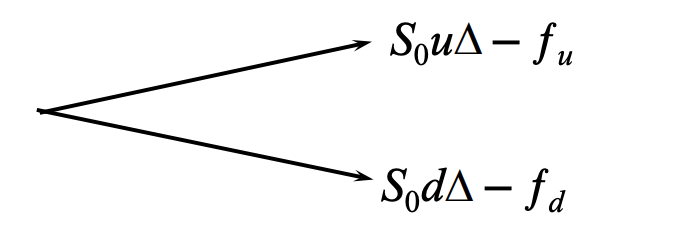

Value of a portfolio that is long ∆ shares and short 1 derivative:

The portfolio is riskless when

Value of the portfolio at time T is

S0u∆ – ƒu

Value of the portfolio today is

(S0u∆ – ƒu)e–rT or S0∆ – f

When we are valuing an option in terms of the price of the underlying asset, the probability of up and down movements in the real world are

irrelevant

Delta (∆)

the ratio of the change in the price of a stock option to the change in the price of the underlying stock

The value of ∆ varies from node to node

A variable z follows a Wiener process if

∆z = ε ∆t where ε is φ(0,1)

The change in z in a small interval of time ∆t is ∆z

The values of ∆z for any 2 different (non-overlapping) periods of time are independent

What does an expression involving dz and dt mean?

It should be interpreted as meaning that the corresponding expression involving ∆z and ∆t is true in the limit as ∆t tends to zero

The expected value of the stock price is

S0e^µT

The expected return on the stock is

µ – σ 2/2 not µ

because ln[E(ST/S0)]E[ln(ST/S0)]

μ

the expected return in a very short time, ∆t, expressed with a compounding frequency of ∆t

μ −σ2 /2

the expected return in a long period of time expressed with continuous compounding (or, to a good approximation, with a compounding frequency of ∆t)

The volatility

the standard deviation of the continuously compounded rate of return in 1 year

The standard deviation of the return in a short time period time ∆t is

The option price and the stock price depend on

the same underlying source of uncertainty