Chapter 14: Operational performance measures

1/43

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

44 Terms

control

the set of procedures, tools, and systems organizations use to ensure that progress is being made toward accomplishing the goals and objectives of the organization

management accounting and control system

an organization's core performance measurement system, one that includes both planning and evaluation (feedback) components

-subdivided into management control systems and operational control systems

operational control

refers to the subset of an organization's overall management accounting and control system that focuses on short-term operational performance

-focuses on the control of basic business processes (or activities) that are performed to produce and deliver the orgs outputs (g/s) to customer

-two performance dimensions covered by operational control systems: financial and nonfinancial (effective system should have both types

Financial control

accomplished by comparing actual to budgeted financial amounts

-budgets are useful in the financial control process because they provide the standard against which actual financial results can be compared

variances

differences between budgeted amounts and actual financial results (can do this on any category on the income statement)

-favorable variances are those that increase short-term operating income, which unfavorable variances have the opposite effect

master budget variance

-an important short-term financial goal for a company is to achieve the budgeted operating income for the period

-at the end of a period, management wants to know whether the planned operating income was attained

-the difference between the actual operating income and the master budget operating income is called the master budget variance

-aka static budget because it is developed for only a single output level

-good for initial planning and coordination of activities, but operations seldom happen the way master budget plans

Flexible budget

a budget that adjusts revenues and expenses to the actual output level and sales mix achieved

-changes in output change the firms expected revenues and expenses.

-For financial control purposes, a firm prepares a flexible budget at the end of a period when the total work done for the actual output level for the period is known

-useful in assessing short-term financial performance

-preparing the flexible budget allows management to adjust the original budget to the actual output level and sales mix achieved, thereby allowing management to answer questions they might have about selling price, sales volume, sales mix, variable cost per unit, and total fixed costs

sales volume variance

the difference between the flexible budget operating income and master budget operating income

-the sales volume variance in terms of operating income is normally the same as the contribution margin sales volume variance because fixed expenses in the master and flexible budget are the same

the sales volume variance may be a result of one or more of the following:

1. The market for the product has changes. The total demand for the product grew (or declined) at a rate higher than expected

2. The firm lost market share to competitors

3. The firm failed to set a proper goal for the period

4. The firm set an inappropriate selling price for the product

5. the marketing and promotion programs were not effective

Flexible budget variance

the difference between the actual amount of that item and the flexible budget amount for that item

-= Actual results-flexible budget results

-there is a flexible budget variance for sales, VC, FC, and and operating income

total flexible budget variance

the difference between the actual operating income and the flexible budget operating income for the period

Selling price variance

reflects the effect on operating income of a difference between actual and budgeted selling prices

-take the difference between actual sales revenues for a period and the sales revenue in the flexible budget for the period

Total variable cost flexible budget

the difference between the total variable cost incurred during a period and the total variable cost in the flexible budget for the period

-reflects the deviation of the actual variable cost incurred during the period from the total standard variable cost for the output of the period

standard cost sheet

a listing of the standard costs and standard quantities of direct materials, direct labor, and overhead that should apply to a single product.

total variable cost flexible budget variance

= total direct materials flexible budget variance + total direct labor flexible budget variance + total variable overhead flexible budget variance + total variable selling and administrative expenses flexible budget variance

general model for analyzing variable cost variances

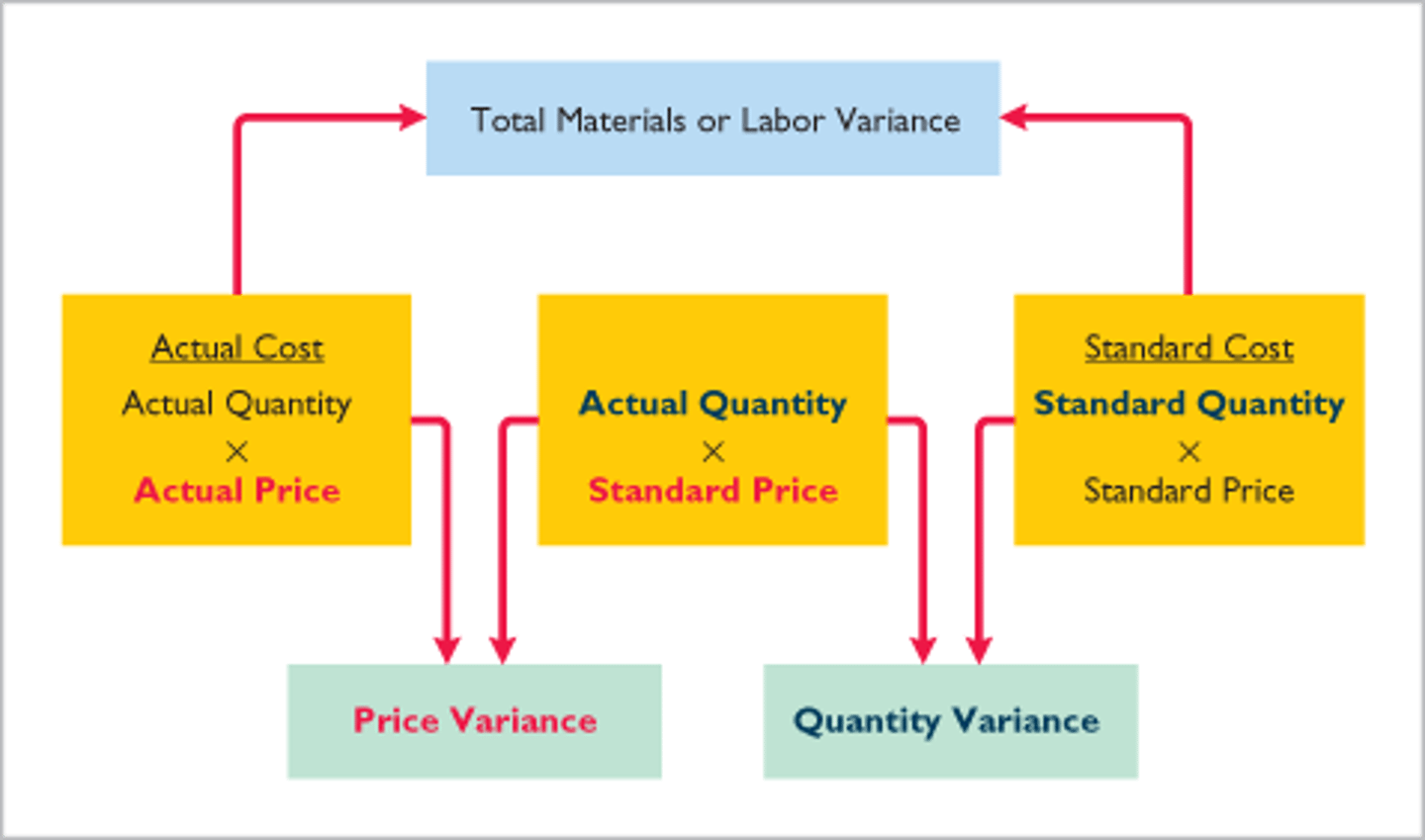

Direct materials variance

the direct materials flexible budget variance for each direct material is the difference between the actual direct materials cost and the total standard direct materials cost for a periods output

-reflects the efficiency in buying and using direct materials

direct materials flexible budget variance

For each material, the difference between the total direct materials cost incurred and the flexible budget amount for this period's output.

direct materials price variance

For each direct material, the difference between the actual and standard costs per unit of the material multiplied by the actual quantity of direct materials used (or purchased) during the period.

materials usage ratio

The ratio of the quantity used to the quantity purchased.

-a low materials usage ratio suggests that the purchasing department purchased for reasons other than the operational needs of the period

direct materials usage variance

the efficiency with which each raw material was used during the period

-for each raw material, this variance is calculated as the difference between the actual raw material units used during the period, multiplied by the standard cost per unit of the direct material

-aka efficiency or quantity variance

-a significant direct materials usage variance suggests that operations consumed a significantly different amount of direct materials than the amount specified for output of the period

-measures the efficiency in using direct materials and can result from the efforts of production personnel, substitutions of materials or production factors, variation in the quality of direct materials, inadequate training or inexperienced employees, poor supervision, or other factors

Direct labor variances

-a direct labor flexible budget variance is a result of the total direct labor cost of a period being different from the total standard direct labor cost for the output of the period

-can also be divided into a rate (price) variance and an effective (quantity) variance

direct labor rate variance

the difference between the actual and standard wage rates multiplied by the actual direct labor hrs worked during the period

-reflects the effect on operating income when the actual hourly wage rate during the period deviates from the standard hourly wage rate

-this could result from not using workers with the skill specified in the standard cost sheet for the work performed or from using an out-of-date standard

direct labor efficiency variance

occurs when the total direct labor hours worked deviate from the total standard direct labor hours allowed for the actual output of the period

-it is calculated by multiplying the difference between the actual and standard allowed hours by the standard hourly wage rate

-reflects the effect on operating income of using a number of direct labor hours during the period that differs from the standard hours allowed during the period

timing of variance recognition

for maximum control, managers should recognize variances at the earliest feasible time

standard cost

a carefully detrmined cost a firm or organization sets for an operation- the cost the firm or organization should incur for the operation under relatively efficient conditions

-usually expressed on a per-unit-of-output basis

-standard costs are incorporated into budgets and as such can be used to monitor and control operations and evaluate performance

standard costs vs. a standard cost system

a standard cost prescribes expected performance. A complete standard cost for a product or service includes carefully established standards for each cost element, including manufacturing, selling, and administrative expenses

standard cost system

an accounting system in which standard cost, and associated standard cost variances are recorded in the formal accounting system

-standard costs can also be sued for control purposes outside of the formal accounting system

-can be applied in either a job-order or process costing context

-because of the repetitive nature of operations, it is generally simpler to establish standards in conjunction with a process costing system. And the use of standard cost in a process costing system simplifies the determination of equivalent unit cots: The standard (predetermined) costs serve as the cost per eq units for dm, dl, and man oh

two basic types of standards

-ideal and currently attainable standards

Ideal standard

aka theoretical standard

-reflects maximum efficiency in every aspect of an operation

-difficult, but not impossible to achieve

-they assume peak operating efficiency and the absence of any production disruptions/ perfection across all operations

-the use of ideal standards can lead to undue stress on employees that may lead to decreases in morale and decreases in productivity. SO most orgs that use this will modify performance evals and reward structures so that employees are not frustrated by frequent failures to attain the standards

continuous improvement standards

such standards, as a function of time (eg months) become progressively tighter (ie more difficult to acheive)

-analogous to Kaizen costing

Currently attainable standards

aka practical standard

-sets the performance expectation at a level that a person with proper training and experience can attain most of the time without having to exert extraordinary effort

-emphasized normality and allows for some imperfections and inefficiencies

selection of standards

ideal standards are not effective if frequent failures in meeting the standards discourage employees or lead them to ignore the standards

-currently attainable standards may have built into them some degree of inefficacy

-a firm can use either an authoritative or a participative procedure when setting the standard

authoritative standard

determined solely or primarily by management

-used to ensure proper consideration of all operating factors, to incorporate managemenr;'s desires or expectations, or to expidite the standsard-setting process

-in a standard setting, the standard is useless if its ignored by employees

participative standard

calls for the active participation of employees affected by the standard

-require more time to create, yet they can have valuable behavioral effects

-participation also reduces the chance that employees will view a standard as unreasonable and increases the likelihood that they will buy into or adopt it as their own

establishing standard costs

joint effort

-managers, product design engineers, industrial engineers, management accountants, production supervisors, the purchasing dept, and employers

1. specify the quality of the direct materials (affects the quality of every other aspect of production and set the standard for the quantity of dm needed to manufacture the product

2. Industrial engineering, production, personnel, labor union reps, and management accountants jointly determine quantity standards for labor after considering the type of work, product complexity, employee skill level, nature of manuf process, and type and condition of the equipment to be used. Personnel dept determines standard wage rate, includes fringe benefits and payroll taxes. Overtime premium amts are treated as part of Factory OH (can be spread out over production in general or traced to a specific job)

3. When standard costs have been established, they are documented on the standard cost sheet for each product

recording cost flows and variances in a standard cost system

-standard cost systems use the same accounts for inventory and for recording manuf costs that actual or normal costing systems use and the costs flow in a similar way, but standard costs systems have standard costs flowing through the accounts

-firms that use a standard cost system have a separate ledger account for each variance. Favorable variances end in a credit balance while unfavorable will end in a debit balance

Standard cost variances: Direct material cost

To record purchase of DM:

DR direct materials inventory (total standard cost of the purchased materials)

DR Direct materials purchase price variance (if unfavorable; for amt of unfavorable variance)

CR cash or A/P (for purchase cost of materials)

CR Direct materials purchase price variance (if favorable; amount of favorable variance)

To record the issuance of DM, after the output of the month could be determined:

DR WIP Inv (total standard quality of materials, at standard cost, for the output of the period

DR Direct materials usage variance (if unfavorable; amt of unfavorable variance)

CR direct materials inv (total quantity of materials used, at standard cost)

CR Direct materials usage variance (If favorable; amt of favorable variance

Standard cost variances: Direct labor cost

The cost of manufactured units is increased by direct labor costs:

DR WIP Inv (The number of standard hrs, at the standard hrly rate, for the units manufactured)

DR Direct labor rate or efficiency variance (if unfavorable; for amt of unfavorable variance)

CR Accrued Payroll (for actual wage expense)

CR Direct labor rate or efficiency variance (if favorable; amount of favorable variance)

Application of standard factory overhead

DR WIP inv

CR Factory OH applied

Standard completion of production

Upon completion of production, the total standard cost of the units manuf is transferred out of the WIP inv account and into the FG inv account

DR finished goods inv

CR WIP inv

Limitations of short-term financial control

-backward looking measures, employees may not be able to act on measure to improve, may focus on local or short term goals at the expense of global or long term strat

-need to also focus on business processes and nonfinancilal meaures (operating processes, customer management processes, innovation processes, social/regulartoy processes

Business processes

-operating processes, customer management processes, innovation processes, social/regulatory processes

-an effective operational control would establish specific objectives for each of the four business processes and then monitor performance by developing one or more key performance measures for each specified objective

Operating processes

acquiring raw materials from suppliers, producing outputs, and delivering p/s to customers. Each has different weight depending on what strat the org is pursing