Economics of Money and Banking 270 Final

1/57

Earn XP

Description and Tags

Covers Chapter 9, 12, 15 which are Banking Management Principles, Financial Crises, and Tools of Monetary Policy

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

58 Terms

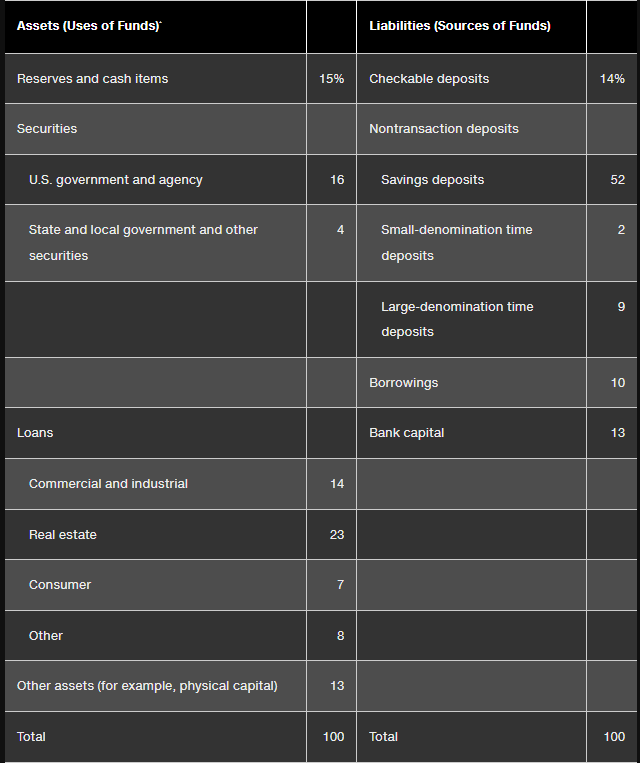

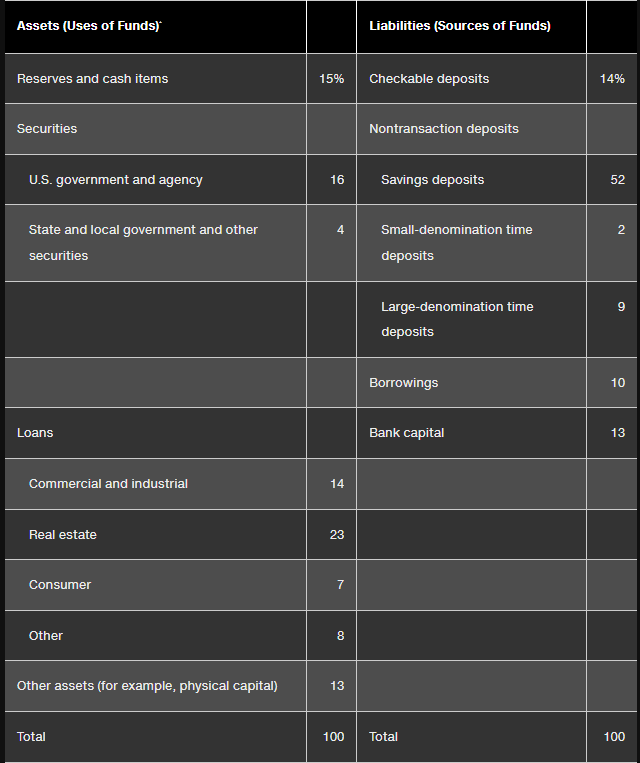

Assets (use of funds for banks)

RECALL total assets = total liabilities + capital

Banks make profits by earning interest on their asset holdings and securities and loans that is higher than the interest and other expenses on their liabilities

assets include loans* , securities, reserves and other cash assets

Liabilities (POV of a bank)

RECALL total assets = total liabilities + capital

banks acquire funds by issuing/selling liabilities. The funds are then used to buy income earning assets.

including deposits*, borrowings, other liabilities, and bank capital

NOW (Negotiable order of withdrawal) accounts

checking accounts that pay interests

Checkable deposits/transaction deposit

Bank accounts which allow the owner of the account to write checks.

They are a liability to banks therefore making it an asset to household and firms.

Nontransaction Funds

The primary source of bank funds. Owners CANT write these to third parties. In exchange for this the interest rate paid on these deposits are higher.

Saving Accounts

A type of nontransaction deposit acount

Funds can be added/withdrawn ANY time. Transaction/interest payments recorded in a monthly or passbook of the owner

Timed Deposits

Fixed maturity length months-5 years

Substantial penalties for early withdrawals

Small Timed Deposits (Less than $100,000)

Less liquid for the depositor than passbook savings, earn higher interest rates, and are a more costly source of funds for the banks.

Small Timed Deposits (More than/Equal $100,000)

-typically bought by corporations or other banks.

-negotiable; like bonds, can be resold in a secondary market before maturity.

-held by corporations, money market mutual funds, and other financial institutions as alternative assets to Treasury bills and other short-term bonds.

NOW accounts

Non Transaction Deposits

Saving Accounts

Money Market Deposit Accounts

Time Deposits

Borrowings

Federal Funds

Repurchase Agreements (REPOS)

Discount Loans

Loans from parent company

Bank Capital

Shareholders Equity

Bank Net Worth

Assets

Reserves

Vault Cash