Lecture 6 – Part 3 Financial v. Management Accounting: Cost -volume -profit analysis

1/86

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

87 Terms

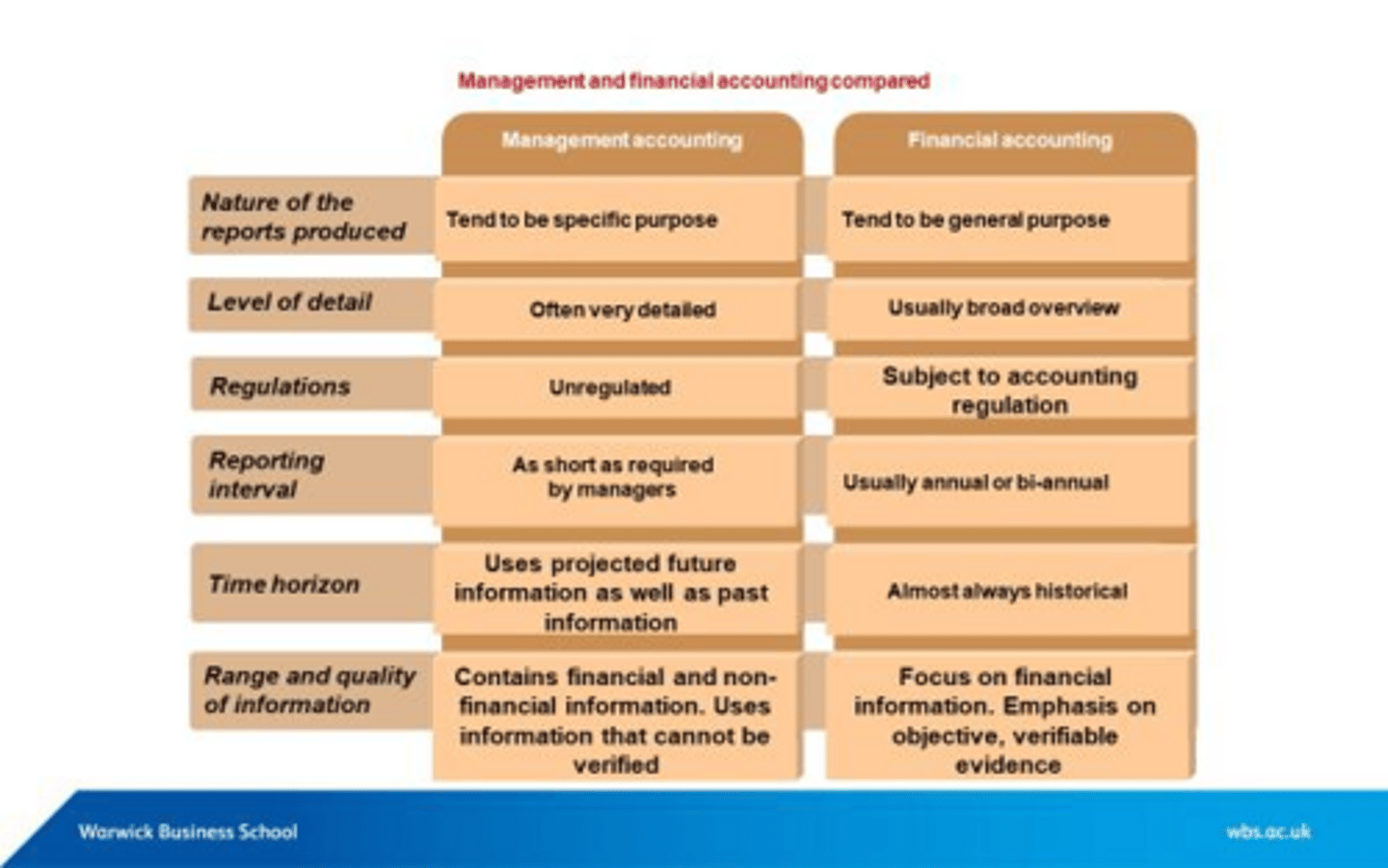

What is the primary focus of financial accounting?

To provide information about the financial position and performance of a business to external stakeholders.

What is the primary focus of management accounting?

To provide information for internal decision-making and management purposes.

Define fixed costs.

Costs that do not change with the level of production or sales, such as rent or salaries.

Define variable costs.

Costs that vary directly with the level of production, such as materials and labor.

What is the contribution margin?

Sales revenue minus variable costs.

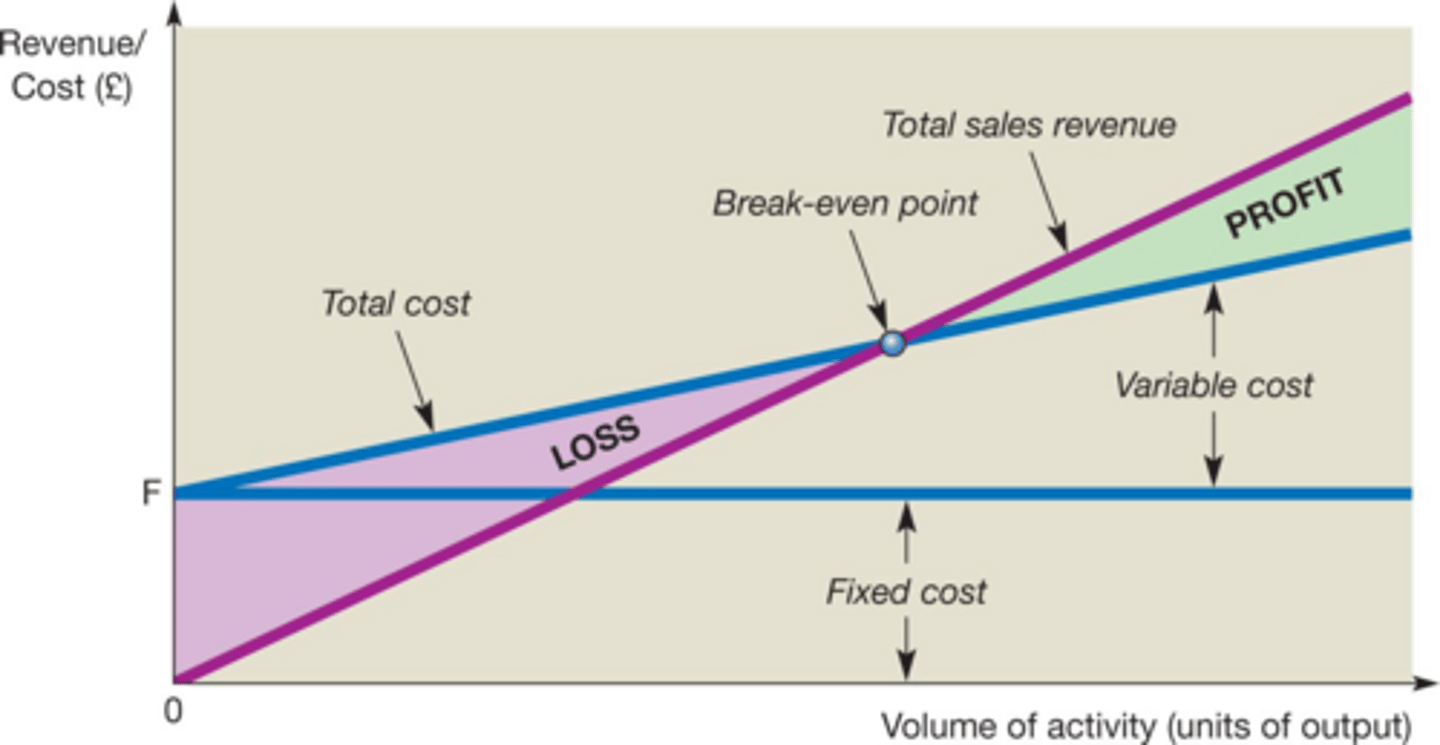

What does cost-volume-profit (CVP) analysis help determine?

The volume of sales needed to cover costs and achieve profit.

What is the formula for calculating profit?

Profit = Sales - Variable Costs - Fixed Costs.

What is the break-even point?

The level of sales at which total revenue equals total costs, resulting in no profit or loss.

How do you calculate the break-even point in units?

Break-even point (BEP) = Fixed Costs / Contribution per unit.

What is the contribution per unit for Greenoak Ltd's garden tables?

£80 per unit (calculated as £140 sales price minus £60 total variable costs).

What are the total variable costs per unit for Greenoak Ltd's garden tables?

£60 (composed of materials £35, labor £10, and variable overheads £15).

What is the fixed cost for Greenoak Ltd per annum?

£600,000.

How many garden tables must Greenoak Ltd sell to break even?

7,500 tables per annum.

What happens below the break-even point?

The company operates at a loss.

What happens above the break-even point?

The company generates profit.

What is the expected contribution for Greenoak Ltd if they sell 9,000 units?

£720,000 (calculated as £80 contribution per unit times 9,000 units).

What is the expected profit for Greenoak Ltd if they sell 9,000 units?

£120,000 (calculated as £720,000 contribution minus £600,000 fixed costs).

What is the relationship between fixed costs and contribution at the break-even point?

At the break-even point, fixed costs are equal to the total contribution from units sold.

What does a break-even chart illustrate?

The point where total revenue intersects with total costs, indicating break-even sales volume.

What is the significance of contribution in management accounting?

It helps in understanding how much revenue contributes to covering fixed costs and generating profit.

What is the primary purpose of financial accounting?

To meet the needs of external users, primarily investors and shareholders.

What is the primary purpose of management accounting?

To meet the accounting needs of managers for strategic planning and control.

What type of data does management accounting provide?

Detailed data that is flexible for managerial decision-making.

Define costs in accounting.

The amount of resources, usually measured in monetary terms, sacrificed to achieve a particular objective.

What are variable costs?

Costs that are related to the volume of activity, such as materials, labor, and variable overheads.

What are fixed costs?

Costs that are related to a period of time and do not change with the level of activity.

How do total variable costs behave with activity level?

Total variable costs change with the level of activity.

How do total fixed costs behave with activity level?

Total fixed costs do not change with the level of activity.

What happens to variable cost per unit as output changes?

Variable cost per unit remains the same.

What happens to fixed cost per unit as output changes?

Fixed cost per unit changes as output changes.

Give an example of a fixed cost in a car manufacturing business.

Rent for factory space or salaries for engineers paid annually.

Give an example of a variable cost in a car manufacturing business.

Raw materials such as steel, rubber, plastics, and aluminum.

What type of costs are assembly line workers paid on?

Hourly basis, which makes their cost a variable cost.

What is the variable cost per unit for a firm manufacturing wooden furniture?

£5 per unit.

What are the fixed costs for the furniture manufacturing firm?

£2000 per month.

What is the key difference between fixed and variable costs?

Variable costs change with activity level, while fixed costs remain constant.

In cost-volume-profit analysis, what does the term 'break-even' refer to?

The point at which total revenues equal total costs, resulting in no profit or loss.

What is contribution in cost-volume-profit analysis?

The difference between sales revenue and variable costs.

What is the significance of understanding cost behavior in management accounting?

It aids in decision-making and strategic planning.

How does management accounting differ from financial accounting in terms of data usage?

Management accounting uses detailed and flexible data for internal decision-making, while financial accounting focuses on standardized reports for external users.

What is the relationship between total costs and volume of activity?

Total costs are influenced by both fixed and variable costs, which change with the volume of activity.

What is the primary difference between financial and management accounting?

Financial accounting focuses on reporting financial information to external parties, while management accounting is concerned with providing information for internal decision-making.

What are fixed costs?

Costs that do not change with the level of production or sales, such as rent or salaries.

What are variable costs?

Costs that vary directly with the level of production, such as materials and labor.

What is the break-even point (BEP)?

The activity level at which a firm makes no profit or loss, where fixed costs equal contribution.

How is the break-even point calculated?

BEP = Fixed Costs / Contribution per unit.

What is contribution in cost-volume-profit analysis?

Contribution = Sales Revenue - Variable Costs.

In the example of Greenoak Ltd, what is the contribution per unit?

£80 per unit.

If Greenoak Ltd has fixed costs of £600,000, how many tables must they sell to break even?

7,500 tables per annum.

What is the expected contribution if Greenoak Ltd predicts sales of 9,000 units at £140 each?

£720,000.

How is profit calculated in the Greenoak Ltd example?

Profit = Contribution - Fixed Costs.

What happens to the profit if the selling price is reduced to £120 and variable costs increase by £10?

Profit decreases; specific calculations depend on the new contribution per unit.

What is the contribution margin ratio (CMR)?

CMR = (Contribution / Sales Revenue) x 100.

What are the variable costs per unit for Greenoak Ltd's garden tables?

Materials: £35, Labour: £10, Variable Overheads: £15.

What is the selling price of the garden tables produced by Greenoak Ltd?

£140 each.

If fixed costs increase to £650,000, what is the new break-even point if the contribution per unit is £80?

8,125 units.

What is the profit if the selling price is reduced to £120 and fixed costs are £650,000?

Profit would need to be calculated based on the new contribution and sales volume.

What is the effect on profit if all changes occur and demand is expected to be 11,500 units?

Profit would need to be calculated based on the new contribution and fixed costs.

What is the contribution per unit if variable costs increase to £50?

Contribution would be £80 - £50 = £30.

What is the break-even point in units if the contribution per unit is £60?

10,000 units.

What is the profit if the contribution is £70 and fixed costs are £650,000?

Profit = (Contribution x Sales Volume) - Fixed Costs.

What is the profit when the contribution is £80 and fixed costs are £600,000?

Profit = Contribution - Fixed Costs.

What does a negative profit indicate?

It indicates a loss, where total costs exceed total revenue.

What is the significance of the contribution margin ratio?

It indicates the proportion of sales revenue that exceeds variable costs, contributing to fixed costs and profit.

How do you calculate expected sales revenue?

Expected sales revenue = Number of units sold × Sales price per unit.

What is the formula for Margin of Safety?

Margin of Safety = Expected Sales - Break-even Sales.

What does a Margin of Safety percentage indicate?

It indicates how much sales can drop before the business reaches its break-even point.

What is the break-even point in units?

The break-even point is the number of units that must be sold to cover all fixed and variable costs.

How is the required number of units to achieve a target profit calculated?

Required units = (Fixed costs + Target profit) ÷ Contribution per unit.

What are limiting factors in a business context?

Limiting factors are resources that constrain a business's ability to produce goods, such as skilled labor or materials.

Why is contribution per limiting factor important?

It helps prioritize production based on the contribution generated per unit of scarce resource.

How do you calculate contribution per hour for a product?

Contribution per hour = Contribution per unit ÷ Labour hours per unit.

What is the opportunity cost in decision making?

Opportunity cost is the contribution foregone by using a scarce resource for an alternative purpose.

What is a relevant cost in decision making?

A relevant cost is a future cost that will change as a result of a decision.

What is the contribution margin for a product?

Contribution margin = Sales price - Variable cost.

What is the formula for calculating total profit?

Total profit = Total contribution - Fixed costs.

How do you determine the optimum production strategy when facing limiting factors?

By maximizing contribution per unit of limiting factor.

What is the expected unit demand for tables, benches, and chairs?

Tables: 9,000 units, Benches: 6,000 units, Chairs: 12,000 units.

What is the contribution per hour for chairs?

Contribution per hour for chairs is £15.

What is the total contribution from producing only chairs?

Total contribution from chairs = 12,000 units × £30 contribution per unit = £360,000.

What is the impact of fixed costs on contribution analysis?

Fixed costs are not relevant in contribution analysis as they do not change with production decisions.

How do you calculate the cost of a special order considering opportunity cost?

Cost = Variable cost + (Labour hours × Opportunity cost per hour).

What is the contribution from product Y2?

Contribution from product Y2 = Selling price - Variable cost = £1,000 - £600 = £400.

What is the additional contribution from accepting a special order for product Y5?

Additional contribution = Selling price of Y5 - Total cost of Y5.

What are the weaknesses of contribution/CVP analysis?

Weaknesses include non-linear relationships, stepped fixed costs, and complexities in multi-product businesses.

How does contribution analysis assist in pricing decisions?

It helps assess the impact of changes in sales price, variable costs, and sales volume on profitability.

What is the total fixed cost for Greenoak Ltd?

The total fixed cost for Greenoak Ltd is £600,000 per annum.