The Canadian Securities Industry

1/9

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

10 Terms

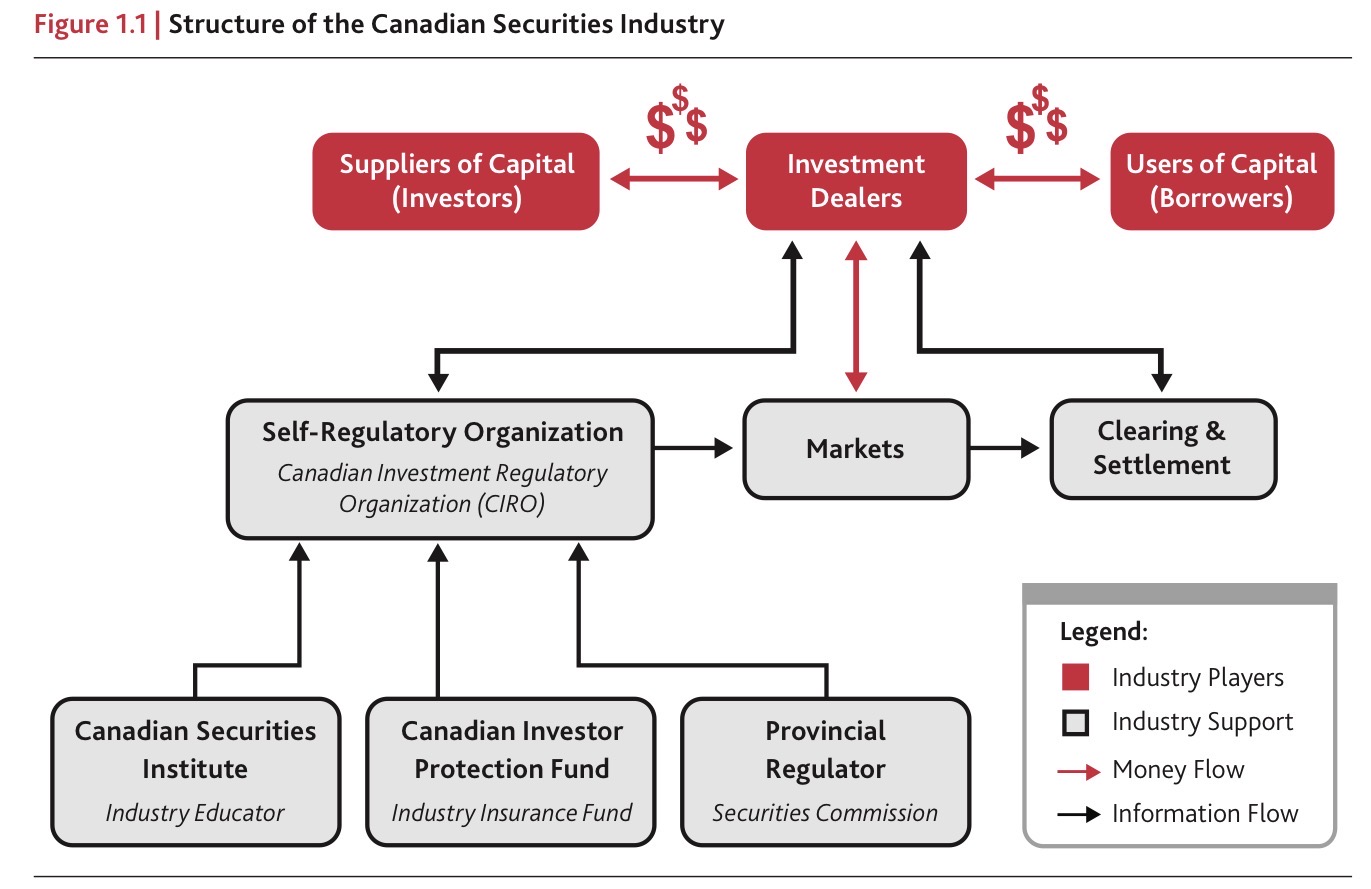

Who regulates the Canadian Securities Industry? What do they do?

Regulated by provinces through security commissions. They delegate some powers to the Canadian Investment Regulatory Org (CIRO), a self-regulated organization (SRO).

Provinces oversee the SRO. The SRO sets and enforces rules that govern and monitor market activity to ensure fairness and transparency.

Covers all investment dealers, mutual fund dealers, and trading activity over Canada’s debt, equity, and mutual fund marketplaces.

Who are investment dealers?

Intermediaries (brokers) that help match investors (suppliers of capital) to borrowers (users of capital). They operate directly with the market to create trades and transactions that clear and settle.

They are regulated by SROs.

What is CDS and netting?

Clearing and Depository Services, an organization that helps clear and settle trades and other transactions.

Clearing is the process of confirming and matching security trade details. Settlement is the irrevocable moment cash and securities are exchanged.

They use a process called netting, which is when they aggregate all the cash and securities positions for a single firm into a final debit or credit position for settlement. This reduces the amount of cash needed to close out.

What is CIPF?

Canadian Investor Protection Fund, they specifically provide insurance against investment dealer and mutual fund dealer insolvency.

Describe the three types of Investment Dealers.

Retail firms: full-service investment dealers and self-directed brokers that deal with regular people. Full-service = range and variety of products and services, including custom advice based on needs. Self-directed/discount = no advice, just help execute the trades; “do it yourself” and cheaper than full-service.

Institutional firms: investment dealers that work with only institutional clients and organizations that do large volumes of securities. Clients include pension funds, foreign institutional clients, and mutual funds.

Integrated firms: Deals in both retail and institutional markets. They also underwrite different types of government debt, corporate bonds, and equity issues. Active in both secondary markets, money market, foreign exchanges etc.

The above can become boutique if they specialize in a particular market segment.

How are Investment Dealer Firms organized?

Senior Management: Oversees all other departments. Directors, President, EVP.

Front Office: Client facing staff functions directly related to portfolio management activities. Portfolio Management, trading, sales, marketing.

Middle Office: Performs functions to ensure efficient operation of the firm. Compliance, Audits, Legal, Accounting.

Back office: Purely trade settlement of security transactions.

Describe the Principal and Agency transactions that an investment dealers will enter into

Principal: When dealers buy in the secondary market for their own inventory and when they underwrite a new issue. The key here is that they buy, hold, and then sell at a later time for a capital gain profit. They hold title.

Agency: When they help facilitate the matching of a buyer and seller. They don’t hold title and earn a commission on the trade. The principal is the clients.

What is the role of a Chartered Bank, and the differences between the Schedules?

Primary role is accept and safeguard deposits and then lend or transfer the funds to users.

Sch 1 = A Canadian owned bank, not a subsidiary of a foreign bank (even if they have foreign shareholders). For large Sch 1., Shareholders restricted to no more than 20%, medium = 65%, small = no restriction. Provides many services over lending and deposits, including financial planning and investment dealer services. Income comes from interest rate spread (margin put by the bank to cover expenses and create profit).

Sch 2 = Incorporated and operate in Canada as foreign bank subsidiary. May be eligible for coverage under CDIC and does the same thing as Sch 1 banks.

Sch 3 = Bank branches of foreign institutions that have been authorized to operate under the Bank Act. Tend to focus on specific areas like corporate finance and investment banking. Overall, this is like a tit for tat to help our banks operate abroad and then also promote FDI.

What are financial intermediaries exist other than banks? What role do they play?

Credit Unions - Similar to banks but cater to a specific group. Is regulated by the CCAA which limits their activities under the “prudent portfolio approach”. This prohibits them from acquiring substantial investments in entities and restricts exposure to real properties and equity securities.

Trust Companies - acts as a trustee in charge of corporate and individual assets such as property, stocks, and bonds. Services often overlap with chartered banks.

Insurance Companies - two lines of business: property/casualty insurance that covers real property and life insurance that also includes RRSPs, annuities, pension plans. The latter acts as a trustee so they have to be more careful with the funds.

Investment funds - Companies or trusts that sell shares or units to the public and then invest it into a diverse portfolio. Open ended (continually issue shares and can be redeemed on demand) and close-ended (only in the start up or infrequently).

Consumer finance companies - direct cash loans with higher interest rates.

Sales finance companies - purchase instalment sales contracts from retailers at a discount when payment plans are used by consumers.

What are the major trends in the financial services industry?

Fintech - online banks and banking services that have no brick and mortar. Think wise and neo.

Robo-advisors - “Self-directed” only investments that automatically rebalance portfolios using an algorithm.

Social and Economic Shifts - Trends in demographics (age and size of bucket moving from earning years), DBP and DCP (employers passing risk to employees through switch to DCP), Saving rates (how much people are saving, should aim for 10-20%, and where they get retirement income from), and debt levels (impact of rising interest rates and people’s ability to pay back loans).

Bitcoin - a digital currency that uses a public and private key to rises in value based on the concept of a deflationary market. Essentially, programmed to have a fixed number of coins which will eventually run out. There is a public ledger that then keeps track of who owns what.