Finance + Accounting

1/51

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

52 Terms

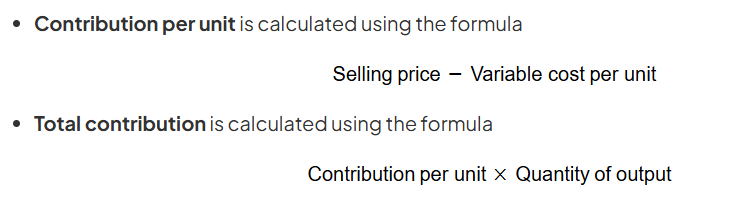

contribution

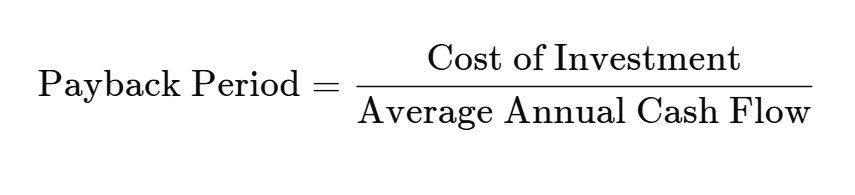

PBP

ARR

capital employed

total assets - current liabilities OR owner’s equity + noncurrent liabilities OR non-current liabilities + share capital + retained earnings

(total amount of capital a company uses to operate)

equity

total assets - total liabilities

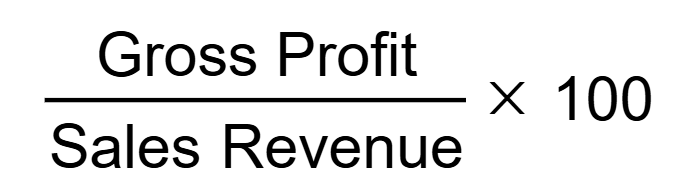

gross profit

revenue - COGS

variance

difference between figure budgeted and actual figure

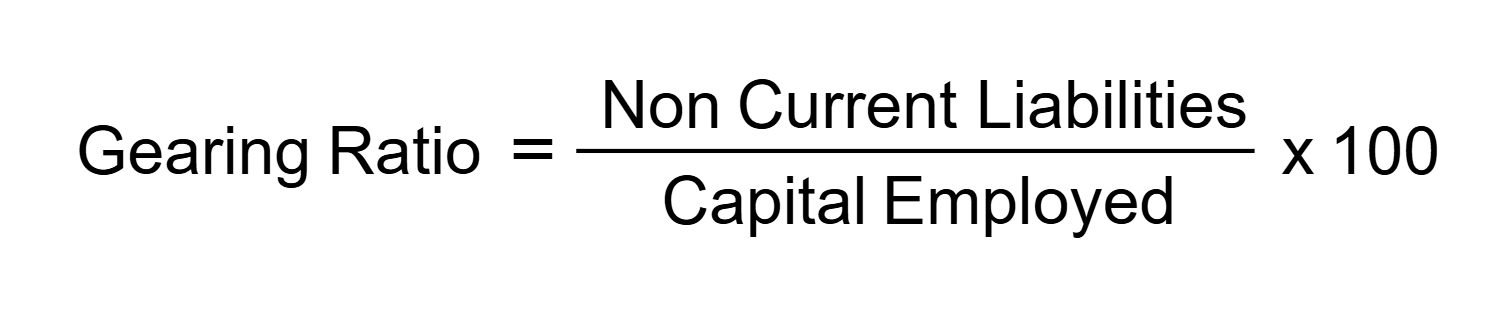

gearing ratio

how business funding is balanced between loans and equity — long-term financial structure;

if it is below 50% it is largely funded by shareholder capital, if above largely by loan capital

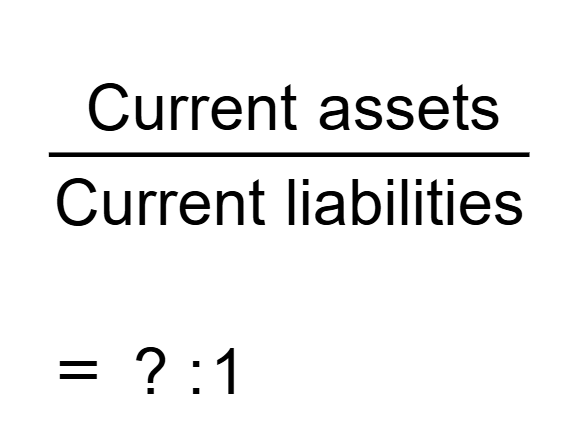

current ratio

liquidity measure for businesses that hold little stock

gross profit margin

the proportion of revenue that is turned into gross profit

return on capital employed (primary ratio)

how efficiently a business uses its capital to generate aprofit

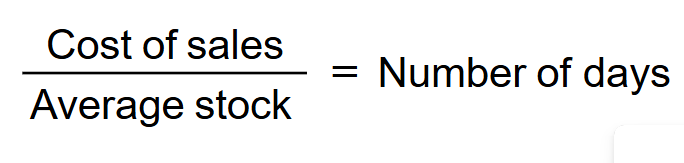

stock turnover ratio

how efficiently a business turns stocks into sales

average stock = (opening stock + closing stock)/2

net book value

cost - accumulated depreciation

straight-line depreciation method

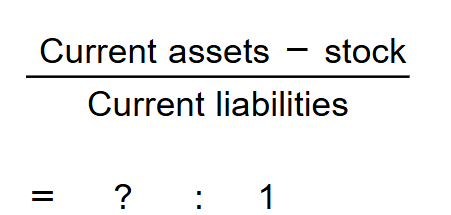

acid-test ratio

assess whether the firm has sufficient short-term assets to cover its immediate liabilities

variance

actual figure - budgeted figure

either favourable or adverse

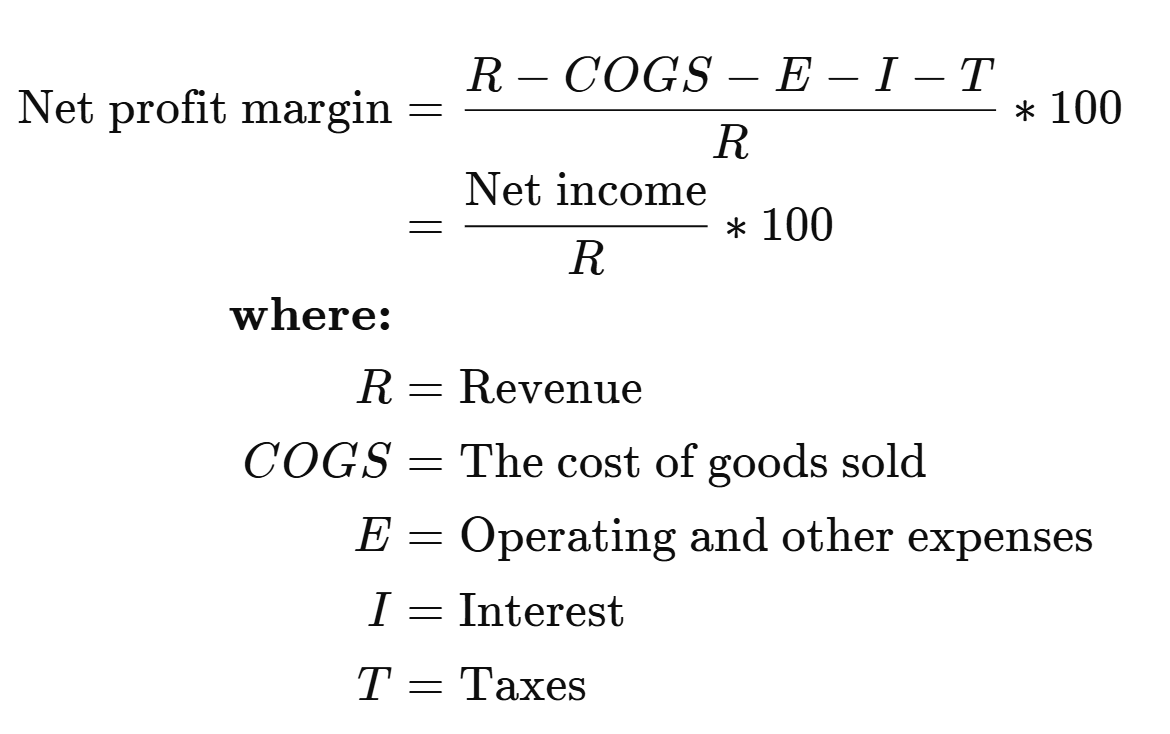

net profit margin

how much net profit a business earns as a percentage of its revenue

BEP

capital expenditure

(also called capex) is business spending on non-current assets that will be used multiple times over more than one year

revenue expenditure

spending on goods and services that a business uses in the short-term, as part of its normal trading activities (examples: raw materials, wages, rent, utility bills, insurance)

working capital

capital needed to manage day to day operations of a business, covering expenses such as inventory, supplier payments and overhead costs. including components such as inventory, cash, trade receivables, trade payables and trade deposits

liquid assets

assets that are cash or can be quickly converted into cash without significant loss of value. cash is the most liquid form of current asset

one advantage and one disadvantage of using retained profits

advantage: avoids incurring dept (no interest payments, preserving financial stability for future operations, no repayment schedules so steady cash flow)

disadvantage: reduces flexibility (retained profits used for one investment, cannot be allocated to other opportunties, potentially limiting ability to respond to unforseen expenses)

risks of a badly financed investment/expansion

cash flow shortages — struggle to cover daily operational costs like wages and utilities

project delays / delayed completion — struggle to meet customer demand, harmed image, harming market share, reducing customer trust

leasing advantages

reduced upfront costs (access to high-quality equipment without high upfront costs, preserving cash flow for other operatinal expenses)

flexibility — can upgrade to newer model frequently, giving competitive advantage

maintenance services — equipment reliability and reducing additional costs

often tax-deductible — finance operations effectively

retained profts

profit from previous years that has been kept within the business rather than paid out to shareholders

business angel

individual that invests their own money in a business in return for a share in the business often providing guidance and expertise

leasing

contractile arrangement where a business pays to rent an asset wihtout taking ownership of it

charactersitcs of overdraft

flexible borrowing up to agreed limit

interest is only paid on the amount overdrawn

can be withdrawn at a shrot notice

immediate access to funds

higher interest than a loan

variable interest rates

advantages of leasing

avoid large capital expenditure of purchasing

avoids tying up funds in fixed assets — capital can be used for expansion

operational flexibiliyt — e.g. scale up or down depending on seasonal demand

reduces the risk of ownership

advantages of a bank loan

immediate access to the (large) sum

spreading investment over several years can help maintain cash flow for day-to-day operations while using the loan for expansion

does not dilute ownership (especially important if the firm has a specific outlook mission whtvr like a socially responsible approach at the centre of activity)

disadvantages of loan

especially bad if the firm already has significant liabilites - increased debt can strain finances especially if interest rates rise

may require providing assets as collateral - increased risk in case the firm cannot repay the loan (especially in the face of unexpected challenges such as supply chain disruptions or slower than expected revenue growth)

highly competitive and time consuming to secure

overheads

indirect expenses that support overall business operations rather than specific products

revenue streams

dividents

donations (for not for profit orgs)

interest (from bank deposits)

subscription fees

merchendise

advertising revenue (for online media businesses)

sponsorship

paying another party to associate a brand or organization with the party, to provide a regular guaranteed source of income for a set period

current assets

items owned by a business that are expected to be converted into cash within one year

when is straight-line depreciation appropritate

when assets have predictable lifespans

when value decllines evenly over time

for small businesses with limitted accounting experitse

when assets have consistent usage patterns

when assets are maintained regularly

when a simple asset valuation is needed

how can u use a profit and loss account

analyse revenue trends to identify success in emerging markets and allocate resources to improve profitability in those regions

identify opportunities to reduce costs

monitor changes in operating expenses over time

advantages of using a profit and loss account to evaluate financial performance

identifying cost inefficiencies — shows higher operating expenses

tracking revenue trends — monitoring sales revenue (what works what doesn’t, e.g. markets, contracts)

transparency for managers

disadvantages of using a profit and loss account to assess financial performance

limited scope — no detailed insight into nonfinancial performance (e.g. staff productivity, customer satisfaction)

focuses on past performance and doesn’t forecast future profits that may resutl from further automation

advantages of selling off old inventory

improved cash flow - increas ability to meet short term liabilites and stabilise liquidity

free up warehouse space - reduce costs assoicated with inventory management

disadvantages of sellinf off old inventory

reduced profitability - may need to be sold at discount which may lower overall profit margins

offering discounts may harm a premium brand image potentially reducing customer trust in product quality

ways to make decisions using a statement of financial postion

assess solvency - review total liabilites and net assets to decide whether additional borrowing is feasible

analysing assets - assess value of non-current assets to see whether further investment in equipment is necessary

monitor current ratio - ensure business has enough liqudity to cover operational needs

adavntages of cheaper suppliers

improved gross profit margins - lower material costs reduce cost of sales, increasing percentage of revenue retained as profit

offer more competitive rpices thanks to reduced costs, attracting new customers which will increase revenue

disadvantages of cheaper suppliers

potential quality issues - image

possible late ddeliveries - project delays (may lead to increased expenses)

how workers can assess job security via a statement of profit and loss

evaluate profitability - evaluate net profit to determine whether the company generates enoguh earnings to sustain operations and payroll

assess solvency - review liabilities (if comapny more financially stabel, less likely to face cash flow problems that could cause business failure)

BUT: lack non-financial insight (ex: market challneges) and backward looking (do not predict future risks)

how to improve liquidity

reduce the credit period for customers (icreases cash inflows and amount of current assets)

sell excess inventory

negotiate extended supplier payment terms

arrange an overdraft facility

control business spending

reduce inventory levels

factors that can cause liquidity problems

high levels of inventory

slow customer payments

poor debt collection

overtrading

seasonal fluctuations

poor cash flow management

how to evaluate the success of investment in a warehouse or storage unit

analyse cost savings - does it reduce storage and transportation expenses

measure inventory turnover - faster trunover means improved stock management means reduced holding costs

does it lead to faster delivery times - enhanced customer experience

does the additional revenue generated by improved operations exceed the cost of investment

factors to cosider when renegotiating trade credit terms

supplier relationships - negotiations should not strain long-term relationships with key supplpiers as this could affect availability

ensure extended payment terms would free up sufficient cash flow to cover short-term obligations

suppliers may require strong payment track record before agrreing

assessing whether competitors have more favorable credit terms they themselves can replicate

advantages to becoming only online

reduce operating expenses

aligns wiht sustainable practices

disadvantages of going onlline only

reduced cusotmer reach

exclusion of those who lack digital reach