Finance Exam 2

1/127

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

128 Terms

what are the 2 important sources of funding?

debt and equity

you can borrow from the bank (private) or issue a bond (public), what’s the main differences?

bank:

senior term, subordinate term, revolver

cheaper, floating, pre-payment, heavy covenants

bonds:

more expensive, fixed, no pre-payment, covenant-lite

options for convertible and callable

investment bank issues

what is a senior term?

less risky for the bank

lower interest rate

what is a relevant cash flow for a project?

change in the firm’s overall future cash flow that comes about as a direct consequence of the decision to take that project

also called incremental cash flows

what is an incremental cash flow?

the difference between a firm’s future cash flows with a project and those without the project

consist of any and all changes in the firm’s future cash flows that are a direct consequence of taking the project

what is not considered an incremental cash flow?

any cash flow that exists regardless of whether or not a project is undertaken is NOT relevant

ex: sunk costs

what is the stand-alone principle

the assumption that evaluation of a project may be based on the project’s incremental cash flows

sunk cost

cost that has already been incurred and cannot be removed and therefore should NOT be considered in an investment decision

opportunity costs

the most valuable alternative that is given up if a particular investment is undertaken

erosion

the cash flows of a new project that come at the expense of a firm’s existing projects

basically if the addition of the new product causes other projects in the company to be less successful for whatever reason

when a corporation or gov wants to borrow money on a long-term basis what happens?

issues or sells debt securities that are called bonds

what does it mean when it is said that bonds are interest-only loans?

borrowers pay the interest every period but none of the principal is repaid until the end of the loan

coupon

the stated interest payment made on a bond

constant

paid every year

face value or par value

the amount that will be repaid at the end of the loan

coupon rate

annual coupon divided by the face value of a bond

maturity

number of years until the face value is paid

why does the value of the bond fluctuate over time?

interest rates may change in the market but the cash flows of the bond stay the same

as the interest rates change, how does the PV of the bond change? (valued more or less)

as interest rates rise, PV of bond’s remaining cash flows decline, so bond is worth less

as interest rates fall, PV of bond’s remaining cash flows increase, so bond is worth more

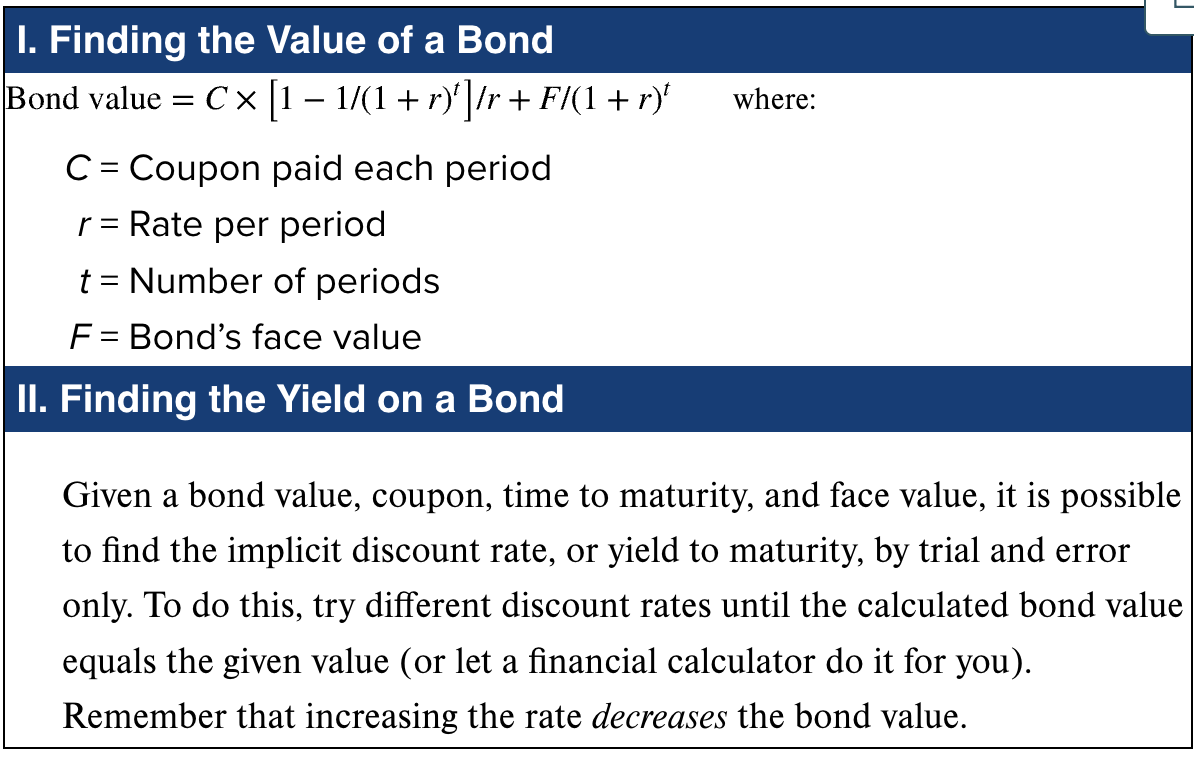

yield to maturity (YTM)

rate required in the market on a bond

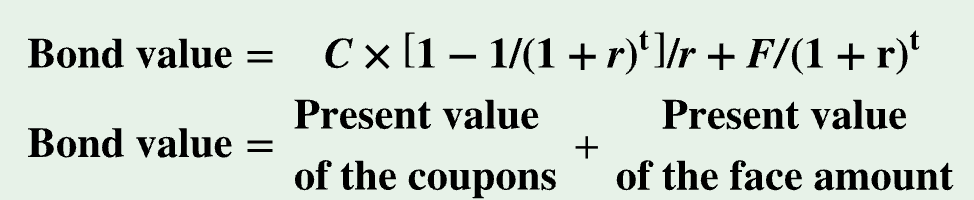

what do you need to determine value of bond at certain point in time?

number of periods remaining until maturity, face value, coupon, market interest rate for bonds (YTM)

estimate market value of bond by?

calculating PV of the lump sum and the coupons separately and then adding the components together

discount bond

when bond sells for less than face value

premium bond

when bond sells for more than face value

what is the difference in value to the bondholder vs bond issuer as market rates rise and fall?

bondholder:

if the market rates rise, this is bad because it means that new buyers of the bond have a better return then you do because they bought at a higher interest rate and you are locked into the lower one

for example they bought a $1000 bond and the interest was 5% then they would get $50 coupons for the life of the bond

but if interest rates rise to say 7% then that is bad because they could’ve bought the same bond for $1000 but be making $70 instead so if they were to have to resell the bond they would have to sell it at a discounted rate

vice versa if interest rates fall

bond issuer:

if market rates rise, this is great for them bc they essentially locked in cheap debt

they should have had to pay $70 in the current market but they only have to pay $50 back and they are protected on the already issued bonds

in this sense it’s great for them because they are basically “saving money”

and vice versa if interest rates fall

bond value equation

bond yields are quotes like APRs, what does this mean?

quoted rate is equal to the actual rate per period multiplied by number of periods

interest rate risk

risk that arises for bond owners from fluctuating interest rates

how much interest rate risk a bond has depends on _____

how sensitive its price is to interest rate changes

what does the sensitivity of a bond to interest rate changes depend on?

time to maturity and the coupon rate

what are the two things you should keep in mind about interest rate risk?

all other things being equal, the longer the time to maturity, the greater the interest rate risk

all other things being equal, the lower the coupon rate, the greater the interest rate risk

why does a bond have a greater interest rate risk the longer the time to maturity?

the longer you hold the bond, the more likely it is that the interest rates in the market will fluctuate for the better or for worse (opportunity cost issue)

additionally tho and more importantly!!, the present value of the face value drops bc a large portion of the bond’s value comes from the face amount and we know that from the time value of money, it is worth much less in the future than today

interest rate risk increases at a decreasing rate, what does this mean?

the risk of a 1yr bond vs 10 yr is significant (10 yr has much higher risk) but difference in risk between 20yr and 30yr bond is fairly small

why does a bond have a greater interest rate risk the lower the coupon rates?

for the same reason as the longer time to maturity

the value of a bond depends on the PV of its coupons and the PV of the face amount

if two bonds with different coupon rates have same maturity, then the one with lower coupons is more dependent on the face amount (and that fluctuates more as interest rates change so the risk is primarily on the component that brings the majority of the value of the bond)

aka: the bond with the higher coupon has a larger cash flow early in its life, so its value is less sensitive to changes in the discount rate

current yield

bond’s annual coupon divided by its price

NOT THE SAME AS YTM

how to do bond valuation?

differences between debt and equity

debt is not an ownership interest in the firm. creditors generally do not have voting power

corporation’s payment of interest on debt is considered cost of doing business and is tax deductible. dividends paid are not tax deductible

unpaid debt is a liability of firm. could cause financial failure whereas issuing equity does not have this possibility

indenture

written agreement between corporation and the lender detailing terms of debt issue

debenture

unsecured debt, usually with maturity of 10 years or more

sinking fund

account managed by bond trustee for early bond redemption

call provision

allows the company to repurchase a bond at a specified price prior to maturity

corporate bonds usually are callable

call premium

amount by which the call price exceeds the par value of a bond

deferred call provision

a call provision prohibiting the company from redeeming a bond prior to a certain date

call protected

a bond that, during a certain period, cannot be redeemed by the issuer

protective covenant

part of indenture limiting certain actions that might be taken during the time of the loan, usually to protect the lender’s interest

negative and positive

negative covenant

type of protective covenant

limits or prohibits actions company might take

positive covenant

type of protective covenant

specifies an action the company agrees to take or a condition the company must abide by

bond rating

assessment of creditworthiness of corporate issuer

based on how likely the firm is to default and the protection that creditors have in the event of a default

zero coupon bond

bond that makes no coupon payments and is thus initially priced at a deep discount

price of stock today is equal to ________

PV of all of the future dividends

what are the assumptions that we make to value a stock?

dividend has a zero growth rate (perpetuity)

dividend grows at a constant rate (growing perpetuity)

dividend grows at a constant rate after some length of time

dividend yield

stock’s expected cash dividend divided by price you bought it for

capital gains yield

dividend growth rate, or the rate at which the value of an investment grows

total rate of return equation

capital gains yield + dividend yield OR (price the stock is worth now + dividend - price you bought stock at) / price you bought stock at

net present value

measure of how much value is created or added today by undertaking an investment

based on NPV, what do different values indicate?

positive NPV = good project! accept

negative NPV = bad project! reject

zero NPV= still profitable, but kind of indifferent between taking and leaving it depending on what other projects are available and how much funds you have

who do covenants protect?

protect the bondholders from losing money

convertible bonds

Allow bondholder to exchange bond for specified number of common stock shares

little more expensive bc bondholders have the advantage over bond issuers

callable bonds

May be repurchased by issuer at specified call price during call period

little cheaper because bond issuers have the advantage

protects bond issuers

when a bond is trading at a discount, would you expect the YTM to be greater or less than the coupon rate?

when the bond is priced lower, the rate of return should be higher (greater than coupon rate)

if you buy a bond partway through the original life, how do you price it?

use the new values and price like normal, IGNORE WHAT ALREADY HAPPENED (just price what is left)

credit risk

the person you lend to might not pay you back

inflation risk

investment needs to earn your money back and cover inflation

interest rate risk

the interest rate rises and falls without easy prediction

which kind of bond is affected most by interest rate risk?

zero coupon bonds (bc the entirety of their value depends on the face value and that is at the end) MOST

long term bonds (they are more heavily affected bc of the timeline)

lower coupon bonds (bc again their value comes majority from the face value of the bond)

what is the holding period yield?

if an investor holds the bond for the entire maturity then HPY = YTM

but oftentimes, investors sell early and then HPY is a different value

If sold before maturity and rates change (interest rate risk)

Or if borrower doesn’t make promised payments (default risk)

how do you calculate HPY?

determine the sale price of the bond at the sale date based on the remaining cash flows and current YTM

calculate IRR for cash flows actually received

what do you have to remember about a problem like this? Three years ago you bought a bond at par value. It has face value of $1000, an 8% coupon rate paid semi-annually, and maturity of 10 years.What was the expected rate of return on the bond at the time you bought it if you held it to maturity?

you need to remember that the YTM is calculated not on an annual basis but based on the periods so you need to remember to multiply by 2 in this problem bc it is semi-annual (4% *2 compounds per year)

default risk typically means that investors pay (more/less) for bonds with high credit risk and that the yield of these bonds would be (higher/lower) than normal

investors pay less to offset the risk

higher yield to incentivize people to buy a risky bond in the first place

the safest bonds have a really (high/low) YTM and the really risky bonds have a very (high/low) YTM

safe have low YTM

risky have high YTM

main risk of owning treasury bonds is the risk of…

changing market interest rates

default

changing coupon rates

decreased liquidity

changing market interest rates

(if market interest rates rise, price of bond falls) no risk of default bc issued by the gov and coupon rates are fixed, additionally they are the most liquid security of all

corporate bonds have higher yields than comparable treasury bonds because of the higher

default risk

corporation can default on its obligation to repay interest and principal while fed gov can always just print more money

what is a bond’s yield to maturity?

the return that you’ll earn if you hold the bond to maturity and the bond delivers all promised cash flows

does a BBB or an AA rated bond have a higher YTM?

BBB is considered a riskier bond and therefore it must have a higher YTM (or lower price) in order to compensate the investors for the additional risk

does a callable bond have a higher or lower YTM?

callable bonds give issuer the option to call the bond before the maturity date

the issuer benefits from this

therefore, callable bonds have a higher YTM to compensate the bondholder for this

does a convertible bond have a higher or lower YTM?

convertible bonds give bondholders the option to convert bond to number of shares

this is valuable to the bondholder

therefore, convertible bonds have a lower YTM to compensate the bond issuer for this

does coupon rate affect the YTM?

similar bonds (same time to maturity, bond rating, etc) have same YTM independent of coupon rate

does having a longer time to maturity have a higher or lower YTM?

because longer time to maturity indicates a higher interest rate risk, this is offset by the higher YTM as a result

what is the normal par or face value of bonds?

$1000

how many times per year does a normal bond pay interest?

2

how is the coupon rate and yield to maturity expressed?

as an annual percentage rate (APR) with semiannual compounding

eq for market cap

stock price * shares outstanding

what does market cap represent?

value of all of the total common equity

eq for dividend yield

annual dividends per share/price per share *100

eq for capital gains yield

(current market price/original purchase price) -1

what are the 3 accepted ways to value a stock

dividend discount model (kinda terrible)

discounted cash flows (DCF) model - BEST

multiples - this one is ok but not great

equity cost to capital

rate of return that investors are expected to receive

what is the basic definition of the dividend-discount model?

the price of any stock is equal to the PV of the expected future dividends it will pay

investor’s time horizon is irrelevant

basically you just value all of the dividends produced

what is the basic definition of the DCF model?

PV of all the cash flows that the firm will ever produce (core operations aka enterprise value)

BEST ONE

what are free cash flows?

cash flow generated from continuing operations

available for distribution to ALL suppliers of capital, such as shareholders, bondholders, etc

independent of leverage and other non-operating investments

the discount rate used is the WACC (weighted average cost to capital)

what is the equation for FCF

FCF = EBIT (1-tax rate) + depr - Capex - change in NWC

equation for EBIT

rev - COGS - SG&A - Depr

change in NWC

sales - op costs - capex - taxes

what is the forecast period in terms of the DCF model

non-constant growth period

what is the horizon period in terms of the DCF model

constant growth period

what is the terminal value in terms of the DCF model

impractical to forecast the FCFs forever

terminal value is the PV of the infinite stream of remaining cash flows as of the final estimation period

how do i value a firm using the DCF method?

find the PV of the FCFs discounted by the WACC to get the enterprise value

subtract net debt

divide by shares outstanding if firm is public

valuation multiple

a ratio of firm’s value to some measure of the firm’s scale or cash flow

P/E ratio

share price divided by earnings per share

what is the go-to multiple

enterprise value multiple

According to the Dividend Discount Model, if you are pricing a stock and plan to hold it for only a few weeks, how should you price the stock?

Price all of the dividends you believe the stock will ever pay. (doesn’t matter what you plan on doing with it, the value is based on what it is actually worth)