Accounting for managers equations

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

28 Terms

High low method for calculating variable costing Cost volume per unit

Change in cost / change in units

high low method calculating fixed cost

Fixed cost = total cost - variable cost (variable cost per unit * number of units)

Contribution margin

Total sales revenue - variable costs

(So what is left to contribute to covering fixed costs)

How to decide whether a change in fixed costs bring greater sales volume is worth it?

INCREASED UNITS: (Increase in units * contribution margin) - (increase in costs)

INCREASED REVENUE: (Increase in revenue * CS RATIO!) - (increase in costs

if positive it’s worth it, if negative it’s not

what is break even point? Calculate it in units and sales:

Break even point is when fixed costs = contribution margin (so 0 profit is made as all contribution goes to fixed costs)

Break even units:

Fixed costs / unit contribution

Break even sales:

Fixed costs / CM ratio

How to find units needed for a target profit

Fixed costs + target profit / contribution margin

(Like break even equation which technically adds 0 to the numerator as the target profit)

What is margin of safety? calculate

in number of units: Excess sales over break even point

Total sales - break even sales

in £’s: Express as percentage: Margin of safety sales /total sales

Purpose of knowing direct and indirect costs

For traceability to trace costs to specific cost objects (aka a single product)

Purpose of knowing product and period costs

Needed for financial reporting so product costs are included within inventory? (CHECK THIS) and period costs are considered general expense

Purpose of knowing fixed and variable costs

Necessary to predict cost behaviour when activity changes (how will costs respond to increase activity, variable costs will rise with it but fixed costs remain the same)

Purpose of knowing controllable and uncontrollable costs

To assess performance

Purpose of knowing differential, sunk and opportunity costs

Aids decision making process

Calculation for costs of goods sold in income statement

Beginning inventory + addition to inventory (aka production of more goods or buying more goods) - ending inventory (what is left over )

price variance equation

AQ(AP-SP)

Quantity variance equation

SP(AQ-SQ)

pre-determined overhead rate

estimated overhead costs / estimated productive capacity/total units in allocation base for period e.g. direct labour hours, machine hours, direct labour costs

overhead applied

pre-determined rate * actual activity

present value

future value * discount factor (find in table using discount rate)

net present value and how to determine investment?

present value of cash outflow (cost —> the present value is the SAME as bought in present so say discount factor = 1 and * by 1) - (SUBRACT) present value of cash outflows

if NPV is POSITIVE make investment

if NEGATIVE don’t make investment

if NPV = 0 do invest and this means the present value of the return is the same as the initial cost (expected rate of return matches the discount rate)

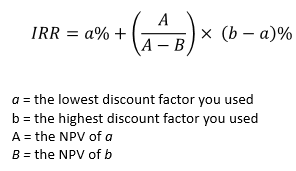

Internal rate of return, meaning and equations

meaning: the discount rate where net present value = 0, is the actual rate of return the project delivers

a discount rate GREATER than the IRR means NPV will be lower and should not do investment

a discount rate LOWER than the IRR means NPV will be higher and should invest

equation 1: investment required/net annual cash flows

equation 2: (see pic) lowest discount factor gives the positive NPV and highest discount factor gives NGEATIVE NPV

but NPV preferred to IRR when making investment decisions

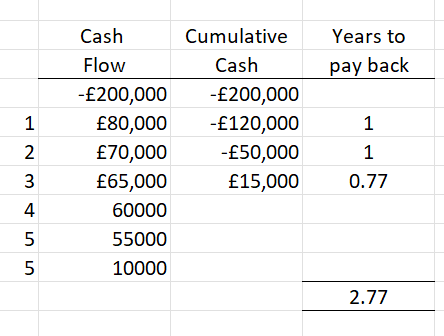

Payback period

the length of time it takes to recover its initial cost

= investment required/net annual cash flow (assuming cash flows are equal yearly)

if cash flows not equal work from top and work out cumulative cash - see in image (start from negative cost and add inflows till you get to positive number, figure out how many years to get to 0 - so if a positive number over 0 divide to find out how much into the year it is to get to 0)

DOESN’T CONSIDER TIME VALUE OF MONEY (doesn’t kook at present values)

Accounting rate of return

average profit / initial investment

for average profit work out yearly inflows - yearly expenses including depreciation and divide by number of years

What is a balanced scorecard?

its a strategic planning and management system used to align business incentives to the business strategy by monitoring performance against STRATEGIC goals (not just financial) —> so is specific to the firm and its long-term strategy

Components of Balanced Scorecard

4 PERSPECTIVES/performance measures:

Customer —> critical success factors of increased customer satisfaction, retention etc.

Financial —> net profit, sales growth, shareholders

Internal business —> improved operations, increased efficiency, delivery performance

Learning & growth —> improving employees via training etc. motivate and empower employees

critical success factors VS KPIs

CSF - Factors critical/vital to the success of the business, different for different businesses, if not met = failure, met directly leads to success or competitive advantage eg. customer satisfaction, Amazon speedy delivery

KPIs = key performance indicators. MEASUREMENTS that indicate how well critical success factors have been met e.g. Amazon average delivery time, average ratings from customer surveys (NEEDS TO BE ACTUALLY AND SPECIFICALLY MEASURABLE, may compare to a target KPI e.g. cant just be employee training but total hours on training)

Balanced scorecard benefits

clarifies vision and overall strategy

aligns daily operations with longer-term strategy

improves organisational performance by measuring what matters

increased focus on strategy

greater focus on the factors which are key to future performance

Balanced scorecard drawbacks

complex and time consuming to prepare

RELIES on a well defined strategy (small firms don’t have) - leads to poor implementation

focus on lagging measures

use of generic metrics (the 4 key things) instead firms should identify which are most relevant

self serving managers - may set easy goals to obtain rewards or look good

Management vs financial accounting

STAKEHOLDERS: management gives info to internal managers to help them direct and control operations, financial for EXTERNAL shareholders and creditors (giving loans)

TIME: Management forward looking —> helps inform for future, gives important data for daily operations, Financial backward looking to record and judge past financial performance,

legislation - Management doesnt have a prescribed format just ethical code of conduct, Financial follow a prescribed format e.g. IFRS reporting standards

Management emphasis on relevance for planning, timely data provided quickly, Financial emphasis on verifiable precise figures

management can focus on specific segments, financial focuses on the whole organisation