9 + 10. Money, ancient and modern

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

28 Terms

What are the functions of money?

It is a medium of exchange which allows for the transfer of goods

It is a unit of account for pricing; it allows one to price goods

It is a store of value for saving; traditionally this value has been asset-backed by things like gold or sheafs of wheat (cryptocurrencies are often excessively volatile and thus disadvantageous to hold as money)

What are the three types of money?

Commodity money (money backed by commodities like wheat, salt, or cows)

Can be debased (e.g., cutting chunks out of silver coins)

Representative money uses tokens which represent amounts of a specific asset — the best example of this is gold

Fiat money is a currency which isn’t backed by a physical asset; it has value simply because a government says it does

Since 1931, notes in Britain have been fiat money

What are the effects of paper (representative) money?

Allowed for a higher rate of growth and superseded commodity money, changing commerce and government finance

Avoided the problem of the coincidence of wants (arose under barter, where a sheep-owner wants shells when the potential buyer only is offering wheat); people can use this token to represent the goods they want

Resolves the problem of commodity money which can be debased (chunks can be cut out of silver coins, not all stores of value are easily transportable or findable — one might not be able to find gold)

Minimal history and effects of fiat money?

Venetian explorer Marco Polo wrote about money in the East and helped spread the idea to the West

From 1260-1308 paper representative money dominated in China

After Charles I in England, goldsmith’s storing merchant’s money and charging a fee realised they could lend this money and issue receipts promising to pay the receipt-bearer

Allows for fractional reserve banking; banks lend more than they have in their vaults by assuming not everyone will ask for their money at once

Issues with fiat money

It is created by Central Banks and divorced from any real value apart from that which we give it → money becomes a mere social institution

It holds value only due to trust: it is backed and created by trustworthy institutions and so trust is enabled in what could be a vacuous item

It will only fail if the economy fails or of there is sovereign debt default

What are the uses of fiat money?

It is a useful social institution which allows for exchange and stability of the financial system

It is acceptable because the CB is the sole issuer, meaning it can’t be forged, the institution is fiscally backed by the government

Thus, money only loses credibility if the economy fails, there is a sovereign debt default, or if a government takes over CB policymaking and money-printing functions

It also affords the CB stronger control over monetary policy

What is a CB digital currency (CBDC)?

Digital currency a central bank can issue and is an alternative to physical cash

It doesn’t have a physical form at all, and exists only electronically as a number on a screen

It is part of both banknotes and bank deposits/e-money; the digital pound is worth the exact same as a physical pound

It means that individuals have a direct claim on the CB itself rather than commercial banks

The difference between retail and wholesale CBDC’s

Retail CBDC’s are only used for retail transactions, whereas wholesale CBDC’s already exist in financial markets

Wholesale CBDC’s already exist and act similar to bank reserves; thus when referring to CBDC’s, it is primarily retail ones which are referred to

Why might a retail CBDC be useful?

Helps to maintain the ‘singleness’ of money in an increasingly digitalised landscape → important for CB to enact monetary policy

Allows for exchange between all forms of money, contributing to stability of the financial institutions — regulation involves ensuring that money is issued at par value across different currencies

Might help to solve the rise of other digital currencies and declining cash transactions

How might a CBDC work?

Could institute a centralised ledger who records transactions, but this has to try and maintain public confidence in it

Payment interface providers (PIPs) are regulated private sector intermediaries who facilitate such transactions between individuals and their accounts

What is a cryptocurrency?

A privately issued digital asset which are often unbacked by governments — they have generally performed poorly due to excess volatility

According to BitKE, more than 24,000 currencies have been issued since 2014 and in 2023, 65% of them had failed

Failure is being short-lived or abandoned, and this is often caused by lack of demand or fraud (rug-pulling)

What is a stablecoin?

Like Bitcoin, they’re run on distributed ledgers but they are different in that they are centralised because they are owned by a specific private company (no-one owns Bitcoin)

If a distributed ledger is the record-keeping system, native crypto assets are the currency intrinsic to this system (like Ether is to Ethereum)

They are often pegged to another currency, commodity, or financial instrument, like US Treasury Bonds which act as reserve assets

They are less volatile because they are centralised and collateralised → collateral is required to maintain the peg and this collateral is often liquid

An outline of Tether as a coin

Founded in 2014, it has several tokens, often denominated by a specific currency (UST, EURT, GBPT, XAUT) which aims to stabilise their value — these are EMT (e-money tokens), and it is pegged 1-1 to US $

Its current jurisdiction is El Salvador

It was fined $41m in 2021 for lying — it claimed it was fully backed by US dollars (a 1:1 mapping) but this only occurred for about ¼ of the 26-month period between 2016-2018

How does Tether work?

The company controls how many tokens are in circulation and is the only company that can do this (mint new coins)

They can be bought via cryptoexchanges or redeemed (turned back into Fiat currency); if redeemed, the Tether can be ‘burnt’ to reduce the currency in circulation or held by Tether, ready for future issuance

They are used as a medium of exchange and are a lot faster and cheaper than fiat currency (don’t need to make payments or engage with banks with different operating hours)

Used for cross border transactions for this reason — applying laws to regulate these transactions is challenging

How are Stablecoins regulated?

Dominate in the crypto-market: accommodate for 60% of on-chain transaction volume in 2023

IOSCO (International Organisation of Securities Commission) has long advocated for regulation of coins which are market dominant and therefore systemically important

In the EU, MiCA regulation exists which attempts to ensure stablecoins remain pegged to their assets and are backed by liquid assets which are separate from the issuers own assets

Only approved institutions can issue stablecoins and they must provide a white paper specifying rights, obligations, and expected risks

In the US, the GENIUS Act (2025) operates which requires coins to be backed 1-1 by US $ or other assets and prevents re-hypothecation (pledging stablecoins, which aren’t recognised as securities or national currency under Federal Law)

What are the consequences of Stablecoins?

Will become in-demand to the US government who need it to fund their plans

They facilitate decentralised finance, but it is not decentralised based on computer code/algorithm like Bitcoin, but there is centralised trust in the issuers

Dollar-backed stablecoins are market-dominant, which could lead to dollarisation

Poses an existential threat to smaller economies which have previously failed; it is tempting to use a stablecoin from a trusted company like Amazon rather than an untrustworthy local central bank currency — this is also pegged to the dominant global currency

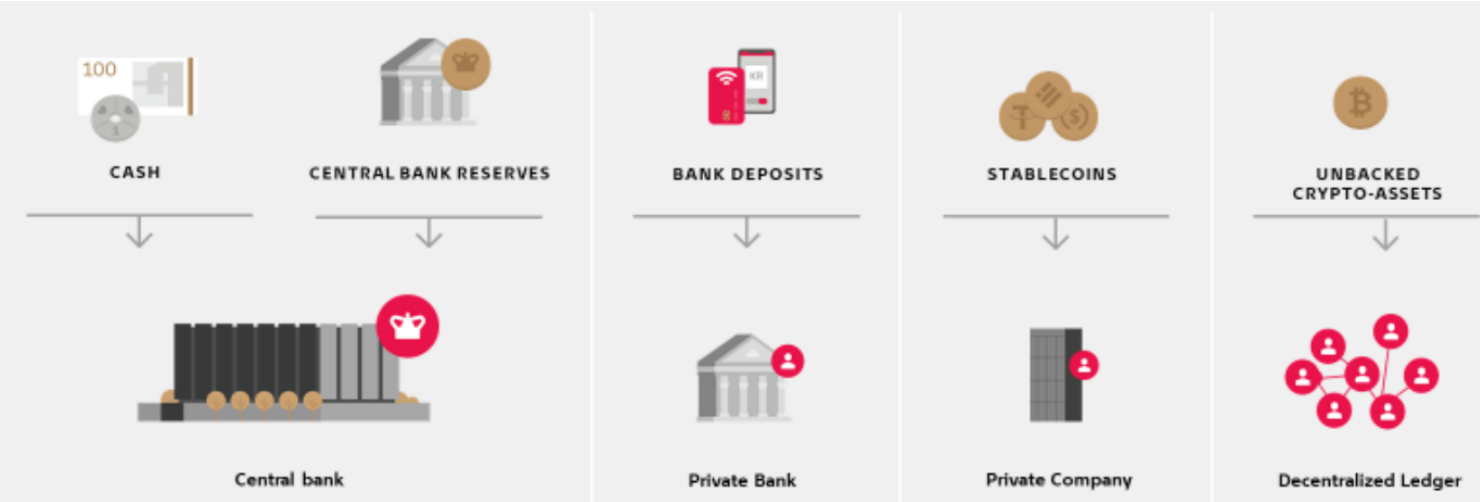

Traditional and new types of money

Why might Central Bank’s fear digital money?

The decline of use in cash reduces the effectiveness of Central Bank money as a monetary anchor — people just might not demand cash so the FED’s promise to supply it is ineffectual

People wouldn’t hold it if they aren’t able to exchange it for these other crypto assets

What are the benefits of a CBDC?

Backed by the CB and thus backed by fiat currency, meaning it is not volatile

It is the only currency whose face value is guaranteed; private coins rely on convertibility

It enables people to keep using the centralised bank in a time of digital primacy

Could a CBDC boost financial inclusion?

Inclusion refers to people without bank accounts or non-cash assets, particularly in developing and emerging countries

If accepted as payment, it could act as an entry point to financially excluded institutions

Fees for small transactions would be low or zero

Involvement of the CB aids adoption and confidence

CBDC Developments

130 governments and all of the G7 are looking into CBDC; a digital Euro is past the planning stage for a potential first issuance in 2029

The China E-CNY is in pilot and is encouraged by its compatibility with other institutions and potential features like ‘expiry dates’ to stimulate spending

The Bahamian Sand Dollar is the first digital currency (October 2020) which saw 25% population uptake (although volume of transactions < 1%)

Nigeria have introduced the eNaira but with low adoption (IMF)

Danish eKroner project cancelled in 2017 since efficiency gains didn’t outweigh administrative difficulties

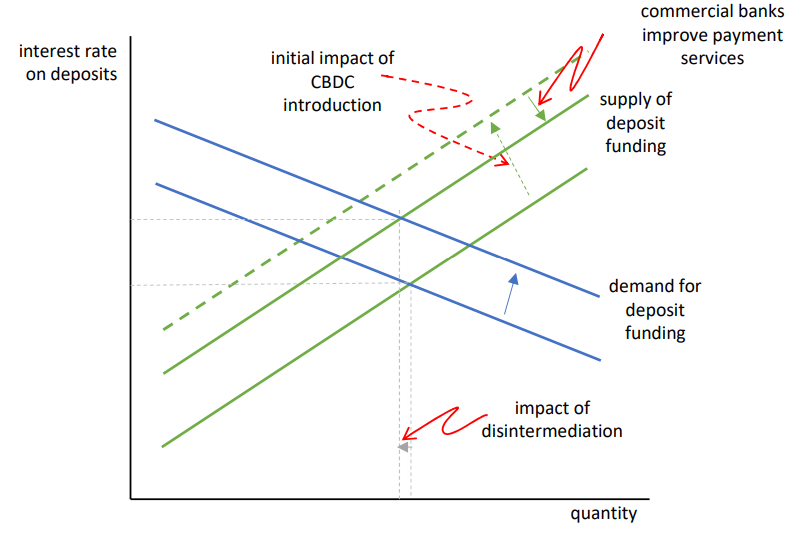

What are the impacts of a CBDC on the banking system?

There is higher competition for deposit funding, greater wholesale funding to replace deposits, central banks make lower profits due to squeezed margins

It could better financial inclusion if it addresses barriers to participation

Dollarisation is mitigated against because local CBDC are backed by the local currency of the CB

The BoE has even suggested that 20% of deposits to commercial banks would move to CBDC wallets, with assessors asking for greater research into this wider impact on the commercial banking system

Would a CBDC lead to a credit crunch?

A credit crunch is the financial systems lessened ability to lend (due to less deposits) leading to lower investment and economic downturn

Deposit flight might occur if people stop making deposits with commercial banks and move directly through the CB

Leads to disintermediation of the banking sector (investors can operate directly without the need for intermediaries)

Final impacts on commercial bank disintermediation (graphical analysis)

Problems with Tether

Over time, its collateral has fallen, it doesn’t have enough safe assets in reserves (only 64% in short-term T-bills),

It is making riskier investments in assets like corporate bonds, crypto, and gold (24% in higher-risk unaudited investments)

It has collected over $180 billion in deposits, which it can’t pay interest on (so is guaranteed profits)

It got ‘junked’ by the S&P, who rated it 5, as extremely weak and volatile

It also possesses 78% of stablecoin market share, making it vulnerable to systemic risk due to liquidity dominance

The political dimension of Tether

It is incredibly dominant with 78% of the Stablecoin market share; it is linked to the Trump administration via Howard Lutnick

It is also deemed the ‘go-to digital asset’ for criminals by many jurisdictions, used by drug cartels, paramilitary movements and it pops up in criminal cases

Disintermediation

People move from deposits at commercial banks and instead make direct claims on the CB instead

This would lead to more expensive credit and tighter lending criteria

It can be slow or fast: slower disintermediation refers to general commercial banking sector shrinkage, faster refers to a digital bank run → people flee the commercial banking sector for perceived financial instability

To stop this, commercial banks might raise their deposit rates. Alternatively, this could increase financial stability if there are less commercial banks/volume of transactions for runs to occur to

Commercial banks need to have sufficient reserves to accommodate for deposit outflows meaning they might need to reduce reserves or borrow

Disintermediation could also apply competitive pressure to commercial banks to retain users, forcing them to improve their services

Other stablecoin examples: DAI and USDC

DAI is an asset-referenced token (ART, backed by other cryptocurrencies) which was pegged 1-1 with US $ until March 2023

Since the collapse of Silicon Valley Bank in 2023, DAI had to unpeg since USDC was massively impacted

USDC has since recovered and is the first stablecoin to have complied with MiCA

It used to be largely collateralised with Ether and USDC, but now it is mainly US treasuries

DAI is generally overcollateralised (at around 150%)