CFA Volume 3 (Equity Investments)

1/421

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

422 Terms

Financial System

Includes markets and various financial intermediaries that help transfer financial assets, real assets, and financial risks in various forms from one entity to another, from one place to another, and from one point in time to another.

Six reasons why people use the financial system

1) To save money for the future

2) To borrow money for current use

3) To raise equity capital

4) To manage risks

5) To exchange assets for immediate and future deliveries

6) To trade on information

Three main functions of the financial system:

1) The achievement of the purposes for which people use the financial system (above)

2) The discovery of rates of return that equate aggregate savings with aggregate borrowings

3) The allocation of capital to the best uses

Equilibrium Interest Rate

The rate at which the amount individuals, businesses, and governments desire to borrow is equal to the amount that individuals, businesses, and governments desire to lend.

Equilibrium rates for different types of borrowing and lending will differ due to differences in risk, liquidity, and maturity.

The price for moving money through time.

Information-Motivated Traders (IMTs)

Trade to profit from information that they believe allows them to predict future prices. They expect to earn a return on their information in addition to the normal return expected for bearing risk through time (i.e., active portfolio management).

Primary Capital Markets

the markets in which companies and governments raise capital (funds).

Securities

Debt instruments, equities, and shares in pooled investment vehicles.

Contracts

Agreements to exchange securities, currencies, commodities, or other contracts in the future. The value of most contracts depends on the value of an underlying asset.

Includes the following:

1) Forward

2) Futures

3) Swap

4) Option

5) Insurance

Examples of financial assets

Securities, currencies, and contracts

Examples of physical assets

Commodities and real assets

Spot Market

Markets that trade for immediate delivery.

Two types of financial markets

1) Money markets

2) Capital markets

Money Markets

Trade debt securities or instruments with maturities of one year or less (e.g., repurchase agreements, certificates of deposit, government bills, and commercial papers).

Capital Markets

Trade instruments of longer duration (bonds and equities, whose value depends on the creditworthiness of the issuers and on payments of interest or dividends that will be made in the future and may be uncertain).

Corporations generally finance their operations in the capital markets.

Traditional Investments

All publicly traded debt and equities and shares in pooled investment vehicles that hold publicly traded debts and/or securities.

Alternative Investments

Hedge funds, private equities (including VC), commodities, real estate securities and properties, securitized debts, operating leases, machinery, collectibles, and precious gems.

Different classifications of securities

1) Fixed-income instruments

2) Equities

3) Shares in pooled investment vehicles

Fixed-income securities with shorter maturities are called ________, those with longer maturities are called ______________ (the cutoff is usually 10 years).

Notes, bonds

Pooled Investment Vehicles

Include mutual funds, trusts, depositories, and hedge funds, that issue securities that represent shared ownership in the assets that these entities hold.

People invest in them to benefit from the investment management services of their managers and from diversification opportunities.

Mutual Funds

Investment vehicles that pool money from many investors for investment in a portfolio of securities. Can either be open-ended or closed-ended.

Open-Ended Funds

Issue new shares and redeem existing shares on demand (usually on a daily basis). ETFs are open-ended funds that investors can trade among themselves in secondary markets.

Trade at NAV.

Closed-Ended Funds

Issue shares in primary market offerings that the fund or its investment bankers arrange. Generally trade in the secondary market at a discount to their net asset value.

Key characteristics of real assets

1) Heterogeneity

2) Illiquidity

3) Expensive (if directly owned due to maintenance costs)

Contract

Agreement among traders to do something in the future and includes forwards, futures, swap, option, and insurance contracts. The values of most contracts depend on the value of an underlying asset. Provide for some physical or cash settlement in the future. Classified as either being physical or financial.

Forward Contract

An agreement to trade the underlying asset in the future at a price agreed upon today (e.g., a contract for the sale of wheat after the harvest at a fixed price). Very illiquid because trading can only be done with the consent of the other party.

Counterparty Risk

Risk that the other party to a contract will fail to honor the terms of the contract.

Futures Contract

Standardized forward contract for which a clearinghouse guarantees the performance of all traders. The buyer of a futures contract is the side that will take physical delivery or its cash equivalent. The seller is the side that is liable for the delivery or its cash equivalent.

Clearinghouse

Organization that ensures that no trader is harmed if another trader fails to honor the contract (acts as the buyer for every seller and the seller for every buyer).

Initial Margin

Money paid to clearinghouse at time of entering a contract to protect against defaults. Clearinghouse settles margin accounts on a daily basis, losses from the day are deducted from a given player's account.

Maintenance Margin

Minimum amount needed to be maintained in buyers' accounts - if account drops below this threshold, players must replenish account via a margin call.

Applicable to leveraged positions for brokers to ensure margin buyers always have a minimum amount of equity in accounts in the event of significant drop in position's value.

Swap Contract

An agreement to exchange payments of periodic cash flows that depend on future asset prices or interest rates (e.g., interest rate swap, commodity swap, currency swap, equity swap).

Option Contract

Allows the holder (the purchaser) of the option to buy or sell, depending on the type of option, an underlying instrument at a specified price at or before a specified date in the future.

Those that buy or sell are said to exercise their option. An option to buy is a call option and an option to sell is a put option.

Credit Default Swaps

Insurance contracts that promise payment of principal in the event that a company defaults on its bonds.

Depository Institutions

Include commercial banks, savings and loan banks, credit unions, and similar institutions that raise funds from depositors and other investors and lend it to borrowers.

Insurance Companies

Create insurance contracts (policies) that provide a payment in the event that some loss occurs (e.g., auto, fire, life, liability). Transfers risk from those who buy the contracts to those who sell them.

Position

The quantity of the instrument that an entity owns or owes.

Long Positions

Owning assets or contracts (e.g., ownership of stocks, bonds, currencies, contracts). Benefit from an appreciation in the prices of the assets or contracts owned.

In general, for contracts, the long side is the one that benefits from an increase in the quoted price.

Short Positions

Selling assets or writing and selling contracts. Benefit from a decrease in the price of the assets or contracts sold. Short sellers profit by selling high prices and repurchasing at lower prices.

Long Side of a Forward or Futures Contract

The side that will take physical delivery or its cash equivalent.

Short Side of a Forward or Futures Contract

The side that is liable for the delivery.

Long Side of an Option Contract

The side that holds the right to exercise the option.

Short Side of an Option Contract

The side that must satisfy the obligation.

Long Side of a Swap Contract

The side that benefits from an increase in the quoted price.

Leverage Ratio

The ratio of the value of the position to the value of the equity investment in it — indicates how many times larger a position is than the equity that supports it.

Indicates how much riskier a leveraged position is relative to an unleveraged position.

= 1 / Initial Margin

Short Selling

Whereby an investor sells shares that he or she does not own by borrowing them from a broker and agreeing to replace them at a future date.

Causes for ROE to increase

1) If net income increases as a faster rate than shareholder's equity

2) If net income decreases at a slower rate than shareholder's equity

3) If the company sues debt and then uses the proceeds to repurchase some of its outstanding shares (i.e., will increase the company's leverage and make its equity riskier)

The book value of equity reflects

The historical operating and financing decisions of its management

Total Return of a Leveraged Position

Depends on the price change of the purchased security, the dividends or interest paid by the security, the interest paid on the margin loan, and the commissions paid to buy and sell the security.

Book Building

Process of investment bank identifying subscribers who will buy securities (by producing investment information and opinions about the issuer to their clients).

Underwritten Offer

Investment bank guarantees the sale of the issue at an offering price that it negotiates with the issuer (most common type of offering).

Private Placement

Corporations sell securities to a small group of qualified investors, usually with assistance of an investment bank.

Three main types of market structures

1) Quote-driven markets

2) Order-driven markets

3) Brokered markets

Quote-Driven Markets

Customers trade with dealers or at prices quoted by dealers (almost all bonds and currencies and most spot commodities trade in quote-driven markets).

Order-Driven Markets

An order matching system run by an exchange, a broker, or an alternative trading system uses rules to arrange trades based on the orders that traders submit.

Brokered Markets

Brokers arrange trades between their customers (common for transactions of unique instruments such as real estate).

Security Market Index

Represents a given security market, market segment, or asset class. The value of the index is calculated regularly using either the actual or estimated market prices of the individual securities (constituent securities) within the index.

Constructed and managed like a portfolio of securities.

Price Return

Measures only price appreciation or percentage change in price. Can be calculated in two ways: 1) either the percentage change in value of the price return index, or 2) the weighted average of price returns of the constituent securities.

Total Return

Measures price appreciation plus interest, dividends, and other distributions expressed as a percentage of the beginning value of the price return index.

There are two main sources of equity securities’ total return: price change (or capital gain) and dividend income. The price change represents the difference between the purchase price (Pt–1) and the sale price (Pt) of a share at the end of time t – 1 and t, respectively. Cash or stock dividends (Dt) represent distributions that the company makes to its shareholders during period t. Therefore, an equity security’s total return is calculated as:

Five approaches to index weighting

1) Price weighting

2) Equal weighting

3) Market-capitalization weighting

4) Float-adjusted market-capitalization weighting

5) Fundamental weighting

The weighting decision determines how much of each security to include in the index and has a substantial impact on an index's value.

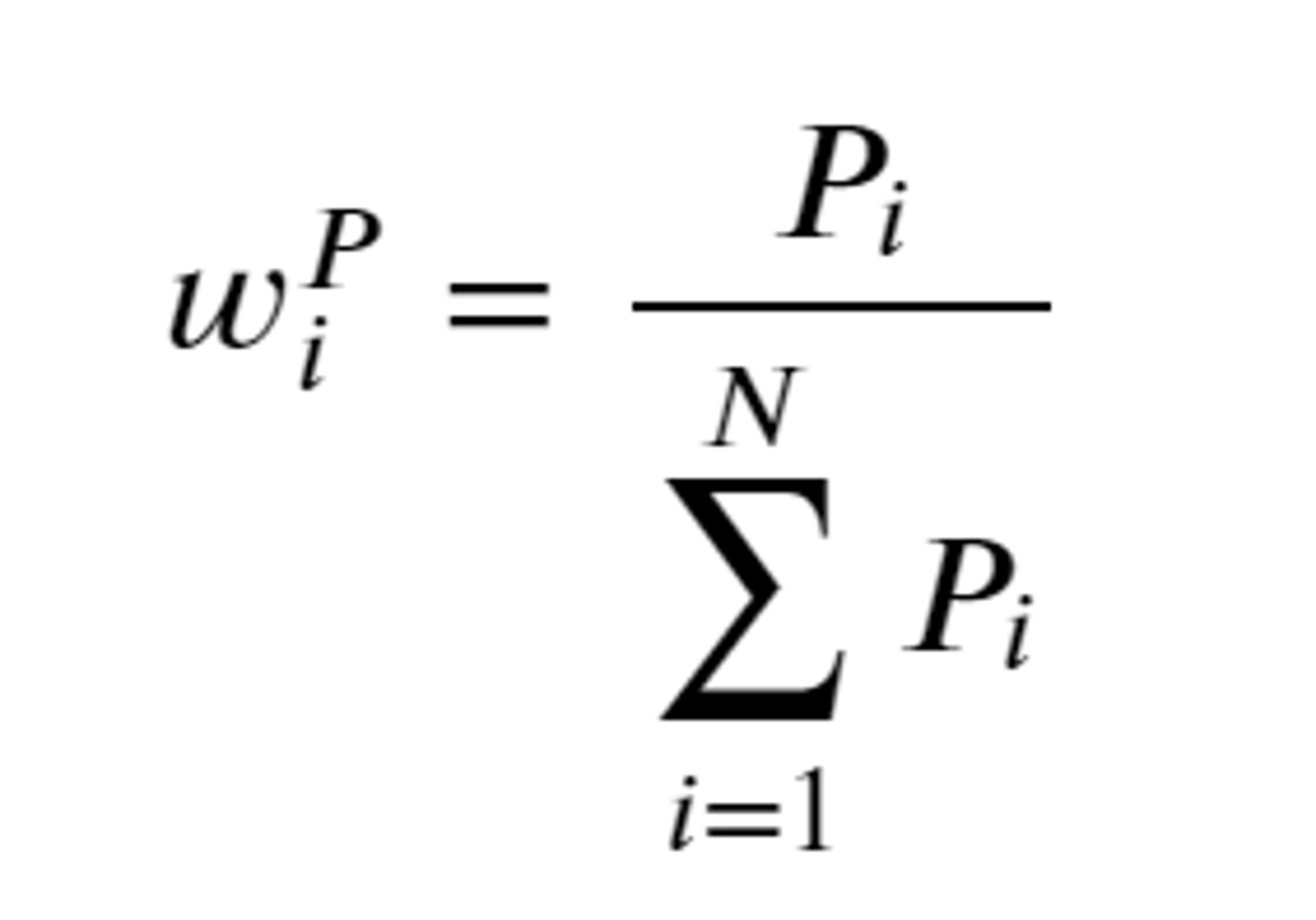

Price Weighting

An index weighting method in which the weight assigned to each constituent security is determined by dividing its price by the sum of all the prices of the constituent securities. Primary advantage is its simplicity, primary disadvantage is that it results in arbitrary weights for each security. Price returns mirror he returns on a portfolio with the same money amount invested in each security.

A property unique to price-weighted indexes is that a stock split on one constituent security changes the weights on all the securities in the index.

Not rebalanced as the weights of each constituent security is determined by its prices.

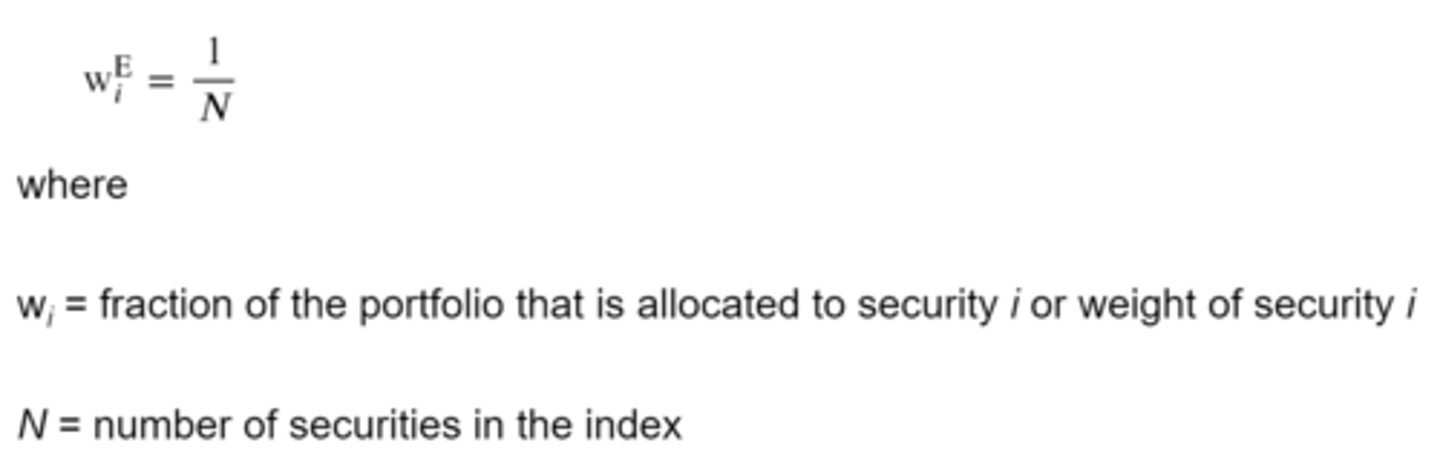

Equal Weighting

An index weighting method in which an equal weight is assigned to each constituent security at inception. Requires constant readjustments as prices of constituent securities change (i.e., most susceptible to rebalancing). Mirrors the returns on a portfolio with the same money amount invested in each security.

Assumed that an equal dollar investment is made in each stock in the index.

A disadvantage of an equal-weighted index is that securities that constitute the largest fraction of the target market value are underrepresented, and securities that constitute a small fraction of the target market value are overrepresented.

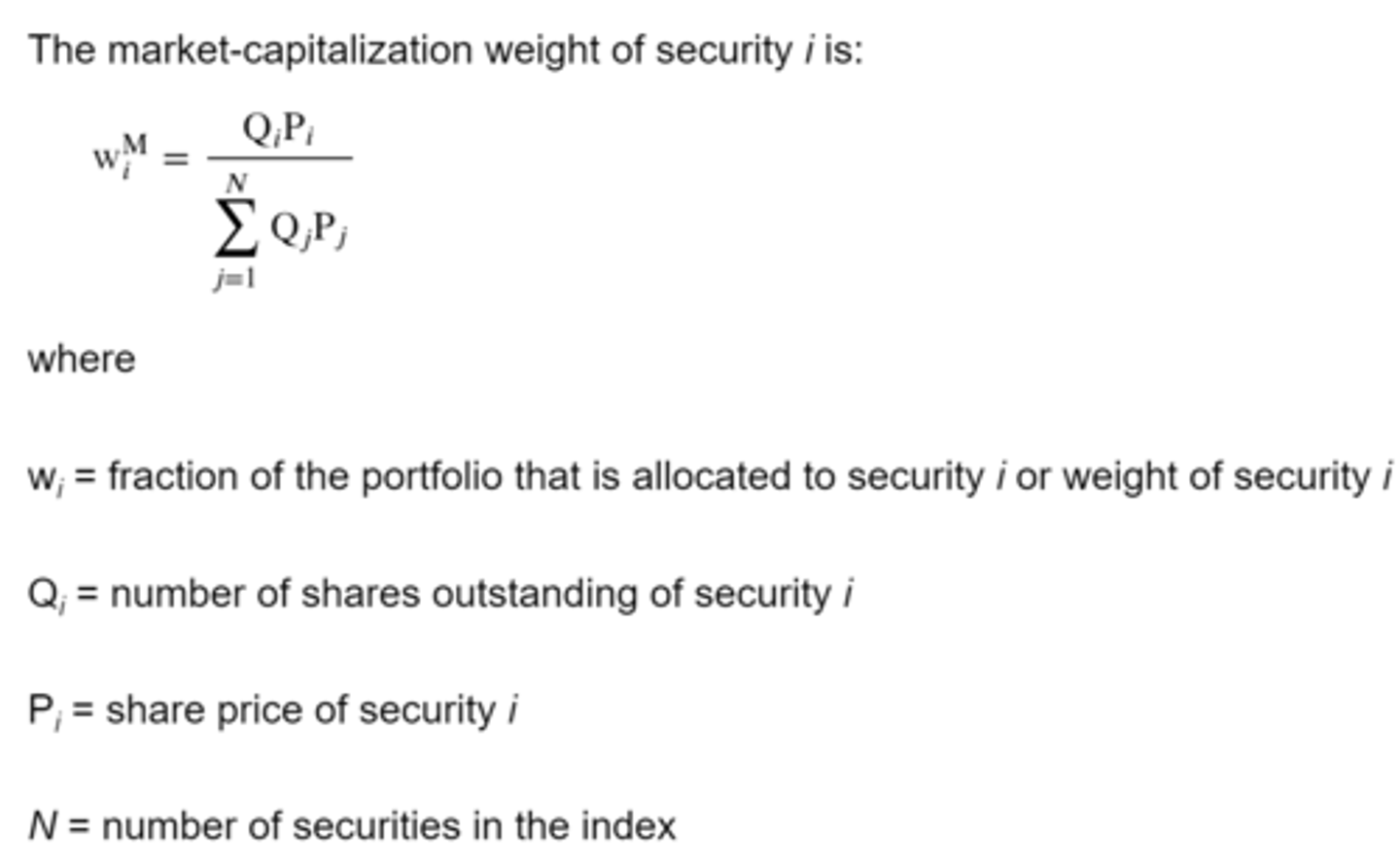

Market-Capitalization Weighting

An index weighting method in which the weight assigned to each constituent security is determined by dividing its market capitalization by the total market capitalization (sum of the market capitalization) of all securities in the index. Also called value weighting. Market capitalization calculated by multiplying the number of shares outstanding by the market price per share.

Biggest disadvantage is that constituent securities whose prices have risen the most (or fallen the most) have a greater (or lower) weight in the index.

Only rebalanced to reflect mergers, acquisitions, liquidations, and other corporate actions between rebalancing dates.

Equity and fixed income indexes are predominantly market cap-weighted.

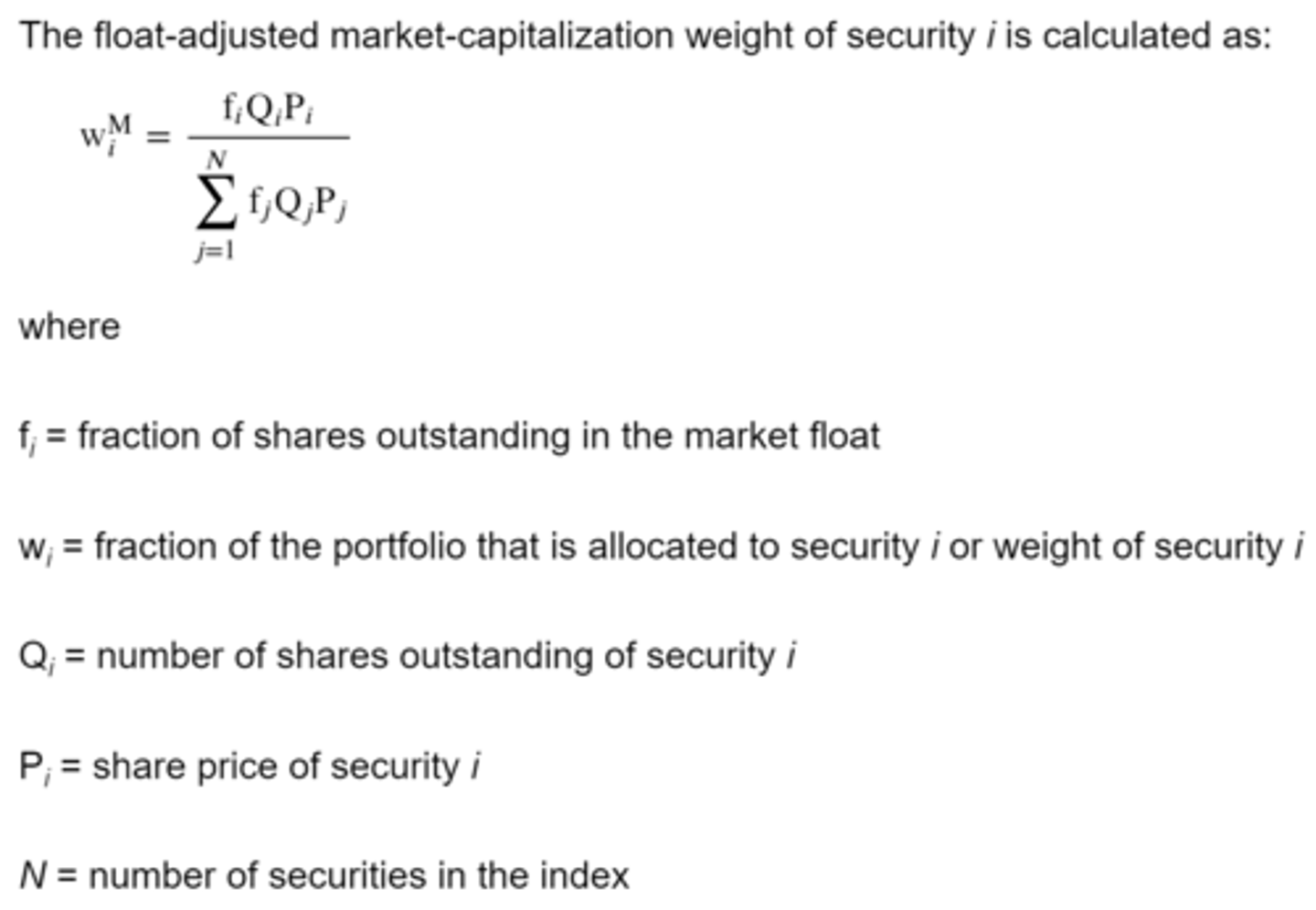

Float-Adjusted Market-Capitalization Weighting

An index weighting method in which the weight assigned to each constituent security is determined by adjusting its market capitalization for its market float. Market float is number of shares of the constituent security that are available to the investing public, rather than total number of shares outstanding. Leads to overweighting stocks that have risen in price.

Fundamental Weighting

An index weighting method in which the weight assigned to each constituent security is based on its underlying company's size. It attempts to address the disadvantages of market-capitalization weighting by using measures that are independent of the constituent security's price. Measures include book value, cash flow, revenues, earnings, dividends, and number of employees.

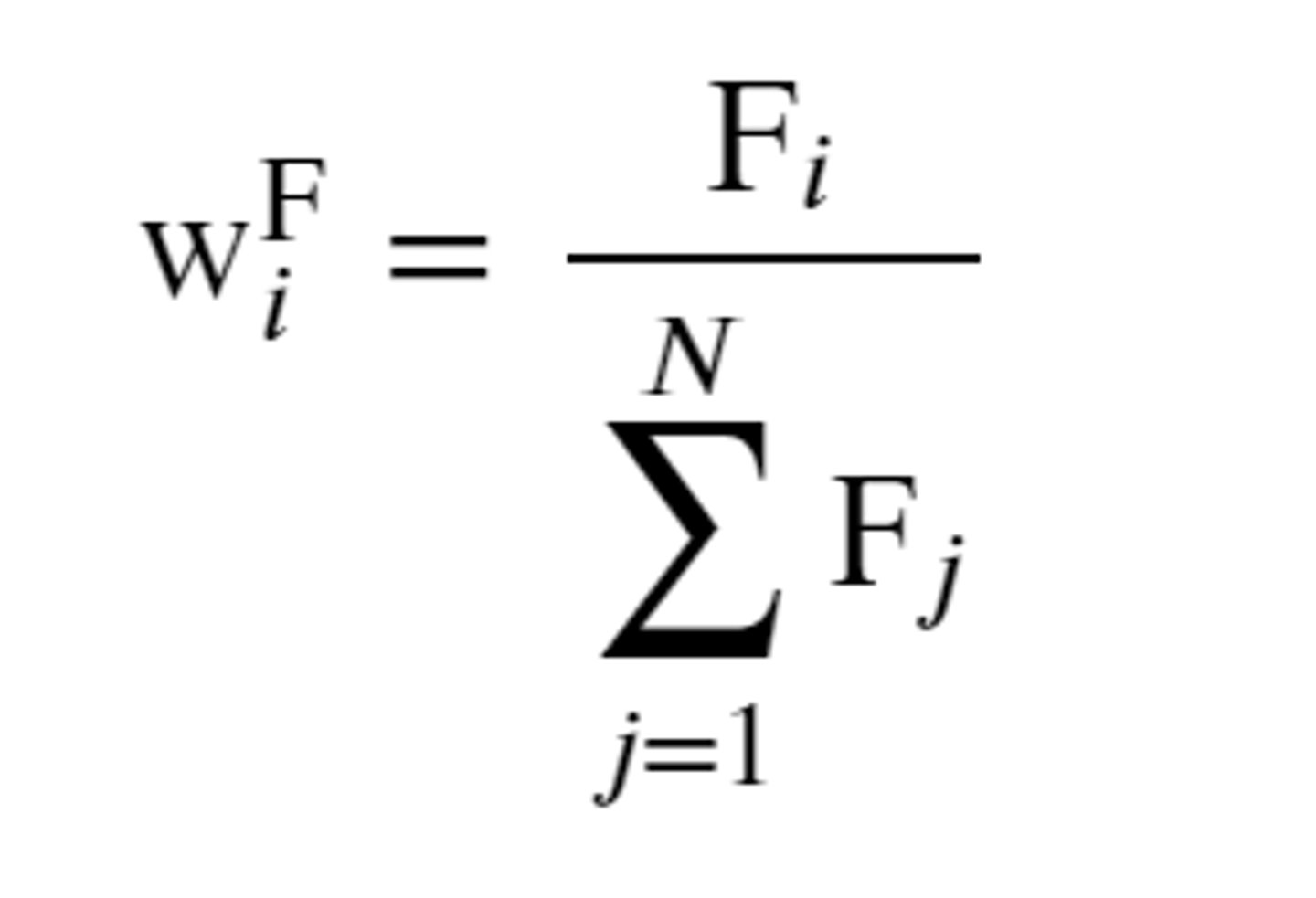

Letting Fi denote a given fundamental size measure of company i, the fundamental weight on security i is:

Most susceptible to a value tilt.

Questions to answer during index construction

1) Which target market should the index represent?

2) Which securities should be selected from the target market?

3) How much weight should be allocated to each security in the index?

4) When should the index be rebalanced?

5) When should the security selection and weighting decision be re-examined?

* Similar to portfolio construction

Rebalancing

Adjusting the weights of the constituent securities in an index — important becase weights of the constituents change as their market prices change.

Usually occurs on a regularly scheduled basis (quarterly).

Reconstitution

Process of changing the constituent securities in an index and is part of the rebalancing cycle.

Reconstitution date is the date on which index providers review the constituent securities, re-apply the initial criteria for inclusion in the index, and select which securities to retain, remove, or add.

Indexes are reconstituted to reflect changes in the target market (bankruptcies, de-listings, mergers, acquisitions, etc.) and/or to reflect the judgement of the selection committee.

Uses of Market Indexes

1) Gauge of market sentiment

2) Proxies for measuring and modeling returns, systematic risk, and risk-adjusted performance

3) Proxies for asset classes in asset allocation models

4) Benchmarks for actively managed portfolios

5) Model portfolios for such investment products as index funds and ETFs

Types of Equity Indexes

1) Broad market

2) Multi-market

3) Sector

4) Style

Style Indexes

Style indexes represent groups of securities classified according to market capitalization, value, growth, or a combination of these characteristics. They are intended to reflect the investing styles of certain investors, such as the growth investor, value investor, and small-cap investor.

Six basic style index categories

1) Large-cap value

2) Mid-cap value

3) Small-cap value

4) Large-cap growth

5) Mid-cap growth

6) Small-cap growth

Role of sector indexes

Sector indexes play an important role in performance analysis because they provide a means to determine whether a portfolio manager is more successful at stock selection or sector allocation. Sector indexes also serve as model portfolios for sector-specific ETFs and other investment products.

Commodity Indexes

Consist of futures contracts on one or more commodities, such as agricultural products (rice, wheat, sugar) livestock (cattle, hogs), precious and common metals (gold, silver, copper), and energy (crude oil, natural gas).

Performance of commodity indexes can be different from their underlying commodities because the indexes consist of futures contracts on the commodities rather than the actual commodities.

Real Estate Investment Trusts (REITs)

Consist of shares of publicly traded REITs (public or private corporations organized specifically to invest in real estate, either through ownership of properties or investment in mortgages).

Categories of Real Estate Indexes

1) Appraisal

2) Repeat Sales

3) REIT

Efficient Market Hypothesis

It is not possible to beat the market on a consistent basis by generating returns in excess of those expected for the level of risk of the investment.

In inefficient markets, an ____________ investment strategy may outperform a ____________ investment strategy on a risk-adjusted basis.

Active, passive

Efficient Market

Asset prices reflect new information quickly and rationally. Thus, a market in which asset prices reflect all past and present information.

The extent to which a market is efficient affects how many profitable trading opportunities (market inefficiencies) exist. Consistent, superior, risk-adjusted returns are not achievable in an efficient market.

In an efficient market, a passive investment strategy that does not seek superior risk-adjusted returns can be preferred to an active investment strategy because of lower costs.

Market Value

The price at which an asset can currently be bought or sold. Represents the intersection of supply and demand — the point that is low enough to induce at least one investor to buy while being high enough to induce at least one investor to sell.

Intrinsic Value (Fundamental Value)

The value that would be placed on it by investors if they had a complete understanding of the asset's investment characteristics (DCFs usually used to estimate this).

Factors that affect market efficiency

1) The number of market participants

2) Information availability and financial disclosure

3) Limits to trading

4) Transaction costs and information-acquisition costs

Market efficiency can be viewed as falling on a continuum.

Abnormal Returns

Returns in excess of those expected given a security's risk and the market's return (i.e., equals actual return less expected return).

Weak-Form Efficient Market Hypothesis

The belief that security prices fully reflect all past market data, which refers to all historical price and volume trading information.

If markets are weak-form efficient, past trading data is already reflected in current prices and investors cannot predict future price changes by extrapolating prices or patterns of prices from the past.

Semi-Strong-Form Efficient Market

Prices reflect all publicly known and available information (includes financial statement data and financial market data). In a semi-strong market, efforts to analyze publicly available information are futile.

If markets are semi-strong efficient, no single investor has access to information that is not already available to other market participants.

Strong-Form Efficient Market

Security prices fully reflect both public and private information. By definition, a market that is strong-form efficient is also semi-strong and weak-form efficient.

If a market is strong-form efficient, those with insider information cannot earn abnormal returns.

Fundamental Analysis

The examination of publicly available information and the formulation of forecasts to estimate the intrinsic value of assets. Involves the estimation of an asset's value using company data, such as earnings and sales forecasts, and risk estimates as well as industry and economic data, such as economic growth, inflation, and interest rates.

Facilitates a semi-strong efficient market by disseminating value-relevant information.

Technical Analysis

Attempts to profit by looking at patterns of prices and trading volume. Technically analysts argue that many movements in stock prices are based in large part on psychology.

Overall, the evidence indicates that investors cannot consistently earn abnormal profits using past prices or other technical analysis strategies in developed markets.

Market Anomaly

If a change in the price of an asset or security cannot directly be linked to current relevant information known in the market or to the release of new information into the market.

Size Effect

The observation that equities of small-cap companies tend to outperform equities of large-cap companies on a risk-adjusted basis.

Value Effect

Value stocks, stocks that have below-average price-to-earnings (P/E) and market-to-book (M/B) ratios, and above-average dividend yields, have consistently outperformed growth stocks over long periods of time.

Common Shares

Represent an ownership interest, a residual claim on the firm's assets in liquidation, and govern through voting rights.

No obligation for firm to pay a dividend.

Can proxy their votes to others.

Preference Shares

Rank above common shares with respect to the payment of dividends and the distribution of the company's net assets upon liquidation. The dividends on preference shares are fixed and generally higher than dividends on common shares.

Use of participating preference shares is much more common for smaller, riskier companies where the possibility of future liquidations is more of a concern to investors.

Private Equity Securities

Issued primarily to institutional investors via non-public offerings, such as private placements. There is no active secondary market for these securities because they are not listed on a public exchange.

Do not have "market determined" quoted prices, are highly illiquid, and require negotiations between investors in order to be traded.

Three types of private equity investments

1) Venture capital

2) Leveraged buyouts

3) Private Investment in Public Equity (PIPE)

Venture Capital

Provides "seed" or start-up capital, early-stage financing, or mezzanine financing to companies that are in the early stages of development and require additional capital for expansion.

Leveraged Buyouts (LBO)

Occurs when a group of investors uses a large amount of debt to purchase all of the outstanding common shares of a publicly traded company.

In cases where the group of investors acquiring the company is primarily comprised of the company's existing management, the transaction if referred to as a management buyout (MBO) — in which case the company is taken "private" or has been privatized.

Ultimate objective of a LBO or MBO is to restructure the company and later take it "public" again by issuing new shares to the public in the primary market.

Private Investment in Public Equity (PIPE)

Generally sought by a public company that is in need of additional capital quickly and is willing to sell a sizable ownership position to a private investor or investor group.

Depository Receipt (DR)

A security that trades like an ordinary share on a local exchange and represents an economic interest in a foreign company. Can be sponsored or unsponsored (sponsored is when the foreign company whose shares are held by the depository has a direct involvement in the issuance of the receipts).

Global Depository Receipt (GDR)

Issued outside the company's home country and outside the United States.

American Depository Receipt (ADR)

A US dollar-denominated security that trades like a common share on US exchanges.