income approach

1/33

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

34 Terms

valuing equity directly (dividend discount model)

the value of equity is just the present value of the future dividends

- forecast the dividends and discount them back by the cost of equity capital

- not a popular approach, good if you have dividends

why is dividend discount model not a popular approach?

Because we need to first solve for the optimal dynamic dividend policy (1) and get managers to stick to it (2)

- Figure out the optimal mix of dividends and RE from now to infinity

- Assumes that the only cash flows to shareholders are dividends and share repurchases

no growth (dividend model)

PV = CF / k

non constant growth (dividend model)

- Forecast out CF until growth is constant

- Get terminal value

- Take PV of finite cash flows

PV = CF_t+1 / (k-g)

indirect method of valuing equity (DCF)

Solving for the Enterprise Value and taking out the Net Debt

enterprise value is NOT

the market value of the assets of the firm

enterprise value

is the market value of the financial claims against the firm; the cost of buying a company

EV = common equity value + preferred + market value debt - excess cash

who has a claim on enterprise value

debt holders, preferred stock holders, equity holders

- so we need a cash flow that goes to all these ppl and has to be before interest since interest goes to debt holders

- if it was just equity, we would only need dividends

calculating equity value

Equity Value = EV − Debt − Preferred + Cash

calculating enterprise value (DCF)

• Project future cash flows to capital providers (UFCF)

• Convert each cash flow to a present value (use wacc)

• Sum these present value cash flows

unlevered free cash flow

Total cash available for distribution to owners and creditors after funding worthwhile investment activities

- goes to all 3 holders, so has to be before ebit

- UFCF = EBITDA - tax on EBIT - capex - changes in WC

- UFCF = EBIT - tax on EBIT + dep + amort - capex - changes in WC

why tax on EBIT not EBITDA?

because the tax shield from interest is already captured in WACC, avoiding double counting.

- WACC uses: Cost of debt × (1 − tax rate) where the 1-tax rate is the tax shield

required rate of return (on capital)

the appropriate discount rate is the return that can be earned on an investment of comparable risk

- What would investors expect to earn on a similar-risk investment?

- The riskier an investment, the higher the expected return needs to be

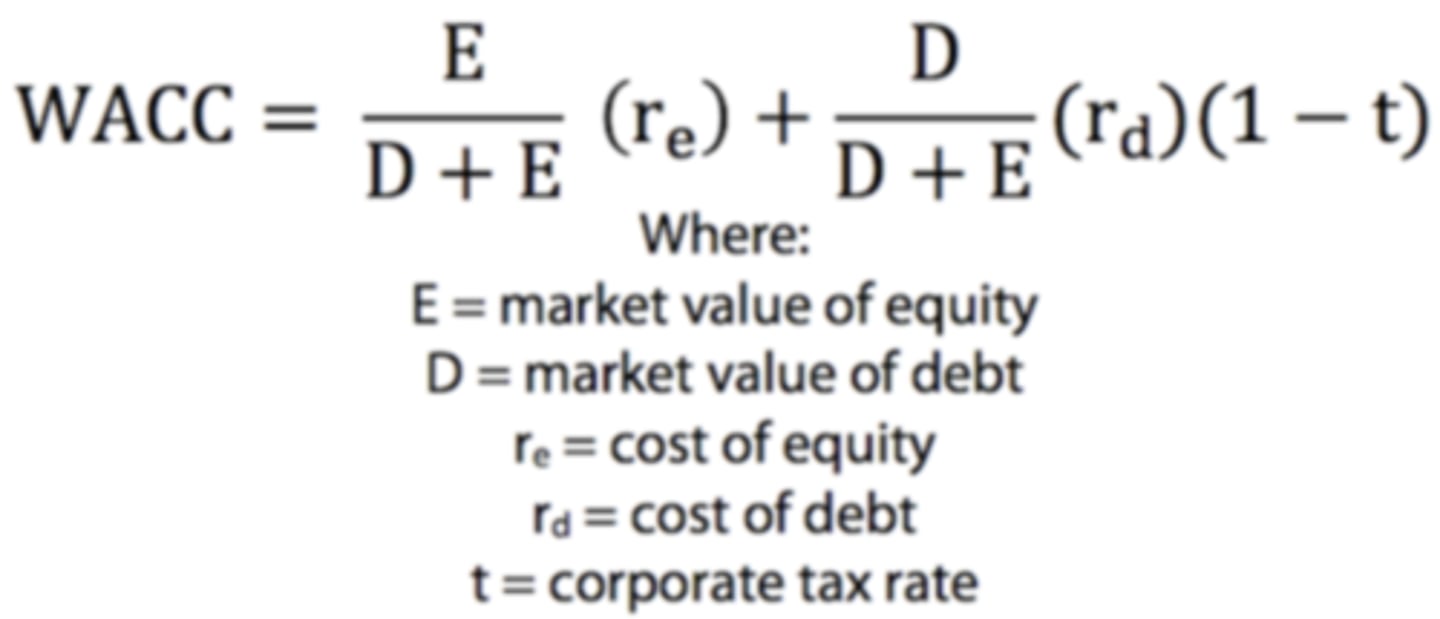

WACC

A weighted average of the component costs of debt, preferred stock, and common equity.

-forward looking

market value vs book value (WACC)

Use market value for the debt and equity bc we want to reflect the current risk and current required return

- MV of debt is hard to obtain so we often use book value (close enough to mv if firm is stable)

actual or target weights?

- We are interested in the required rate of return in the future, so today's ratios are irrelevant

- what matters is our expectation of the future, TARGET

short-term debt

Only include if:

It's permanent

Shows up consistently on balance sheet (both 10Q and 10K)

MV of equity

number of shares * price per share

- more difficult for private firms because equity doesn't have a "price"

- instead, we use the industry P/E multiple

cost of debt (Rd)

The current interest rate the company would pay if it borrowed today

ways to calculate:

1. calculate YTM using bond market prices: expected yield over the life of the bond

2. Use similar companies' bond yields if your bonds dont trade

3. Infer credit rating yourself using TIE, D/A, liquidity ratios

4. look in footnotes to annual report

debt > equity bc

Lenders get paid first → less risk

Interest is tax deductible (1-t)

converting to annual rate (Rd)

Bonds usually pay semi-annually, but WACC needs an annual rate so we use the effective annual rate; to calc:

(1 + semiannual/2)^2 - 1

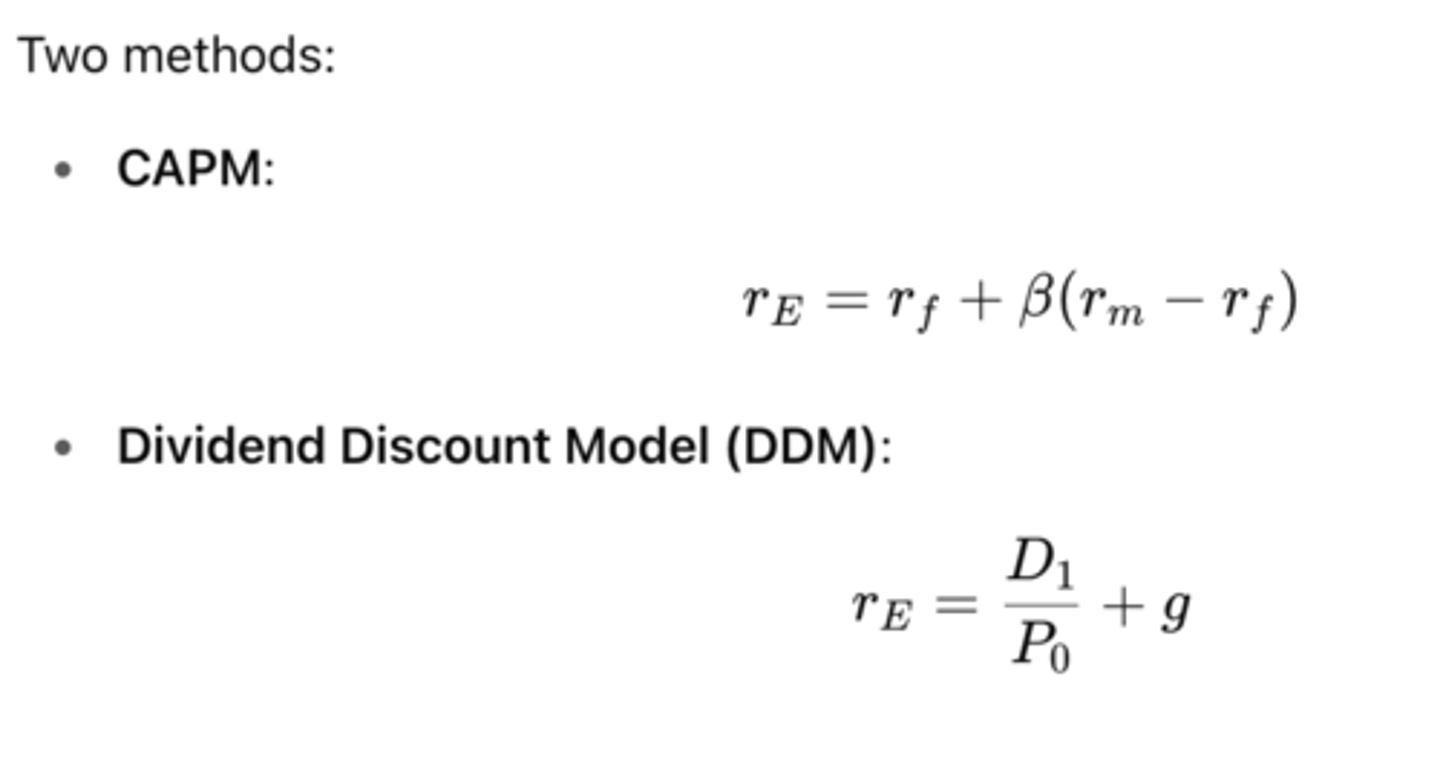

cost of equity (Re)

the return shareholders require for investing in the company

- to find Re we take the risk free return and add some risk to it

- use CAPM

Risk-Free Rate (Rf)

Return on an investment with zero risk.

- baseline; based on government bonds

- Match maturity to firm → use 30-year Treasury

Market Risk Premium (Rm - Rf)

Extra return investors demand for investing in the market instead of risk-free assets

- reflects Investor expectations & Risk aversion

- current premium is 5.45%

- NOT the diff between the CURRENT market rate of return and CURRENT risk free rate

beta

Measures how risky the stock is relative to the market

- reflects both business and financial risk

- B > 1 = more risky than market, B < 1 = less risky

- adjusts the risk premium: Higher beta → bigger premium → higher required return

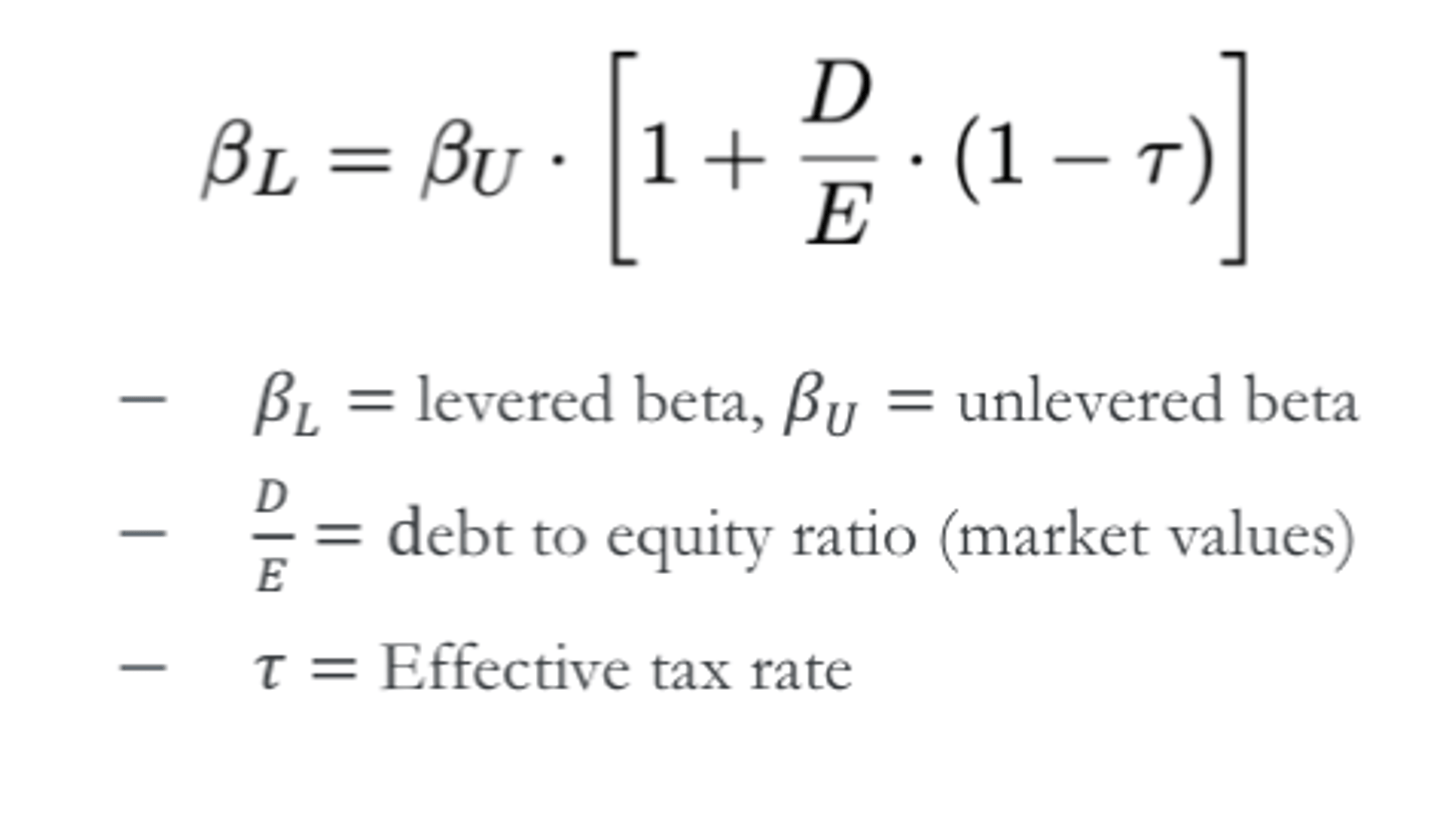

unlevered beta

The firm's beta coefficient if it has no debt, only business risk

levered beta

business risk + financial risk (debt)

- More debt → more risk to equity holders

- So: β increases & Re increases

equity

Equity = EV - Net debt - preferred stock

where net debt is Debt + Capital Leases + Minority Interest - Excess cash

undervalues

traditional DCF _________ companies

- because it assumes CFs occur at the end of the year

mid-year convention

Assumes that the cash flows happens smoothly over the course of the year

- Rather than using cash flows at T= 1, 2, 3... etc, we use T= 0.5, 1.5, 2.5... etc.

- PV(mid-year) > PV(end of year)

--> under what condition not true? if the discount rate is 0. as long as there is risk aversion, it is true

when to use mid-year convention

if valuing A firm that does most of its business in the summer months, like a restaurant at the shore.

- A firm whose revenues are relatively stable over the course of the year

- Any firm that doesn't have a major concentration of revenues in Q4

seller prefers

mid-year convention

buyer prefers

traditional end of year convention

false (needs to be discounted at WACC)

PV of UFCF discounted at cost of equity = EV?

- UFCF goes to debt + equity

- So discount rate must reflect both not just Re