ch3: employment income

1/77

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

78 Terms

employment income

Income received from holding an office or employment.

non-saving income

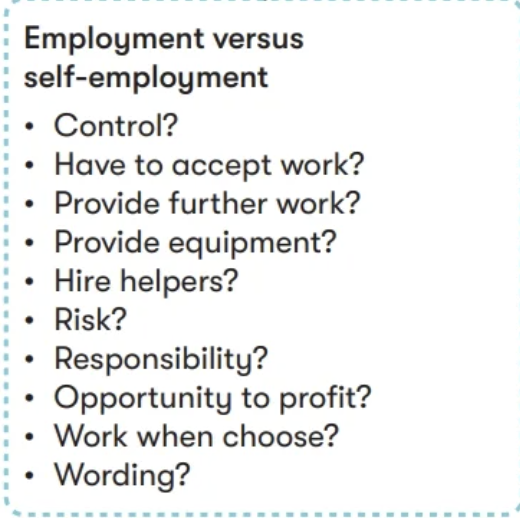

how to tell someone is employed, and not self-employed

have contract of service

relationship is ongoing

how to tell someone is self employed, and not employed

have a contract for services

task based

how to determine between self employed and employed

control = employed

who provides equipment? Employer → employment

who has the financial risk

can they hire their own helpers = self-employed

Main types of employment income?

Salary

Bonuses

commisions

non-cash Benefits (e.g. company car)

payments made on termination of income

Employment income taxed on what basis - normal tax rules

Earlier of received or entitled

What is PAYE?

Tax deducted at source from salary.

Employment income taxed on what basis for directors?

earliest of:

time payment made

entitled

amount credited in the company’s accounts

end of the company’s period of account

time the amount is determined

In exam questions, are salaries usually given gross or net?

gross

Main trap in bonus timing questions?

Confusing the accounting period the bonus relates to with the tax year in which it is taxed

tax year?

6 Apr 2025–5 Apr 2026

What are taxable benefits?

Perks provided by employers that are taxable on employees.

If no specific rule exists for a benefit, how is it valued?

Cost to the employer.

When is there NO taxable benefit?

When there is no private benefit to the employee.

What happens if a benefit is not available for the full tax year?

time apportion

If not available for full tax year OR unavailable for ≥30 days

What happens if the employee contributes towards the benefit?

Deduct the contribution.

exception of fuel benefit

When does a car give rise to a taxable benefit?

When provided by employer and available for private use.

Does commuting in the company car count as private use?

yes

(different for vans)

Exception to car benefit rule?

Pool car

(stays at the office)

Car benefit formula?

(List price – employee capital contribution [max £5,000]) × CO₂ %

What is included in list price?

Price when new

Optional extras (£100+)

Are discounts deducted from list price?

No (IGNORE discounts)

How does % increase above 55g/km?

+1% per 5g/km (rounded down)

pool cars

Used by more than one employee

Private use is incidental

Not kept overnight at employee’s home

Does partial employee contribution reduce fuel benefit?

no

When is fuel benefit NIL?

Only if employee pays for ALL private fuel

Does commuting count as private use for vans?

no

Van benefit for private use?

£4020

Van fuel benefit?

£769

Steps to calculate car benefit?

Find list price

Deduct employee capital contribution (max £5k)

Apply CO₂ %

Time apportion

Deduct employee usage contributions

Steps to calculate van fuel benefit?

Take £28,200

Apply same CO₂ %

Time apportion

DO NOT deduct contributions (unless full reimbursement)

Use of asset benefit formula?

Higher of:

20% × market value when first provided

Rent paid by employer

Gift of asset – if asset already used by employee?

Higher of:

Market value when given

Original value - benefits already taxed

Gift of NEW asset (not previously used)?

Cost to employer

gift of asset: Special rule for computers?

Always use market value

What happens to employee payments for asset?

Deduct from benefit

When does a beneficial loan arise?

Interest-free OR low-interest loan from employer

beneficial loan benefit calculation

Interest at official rate – interest actually paid

Official rate of interest (2025/26)?

3.75

Two methods for loan benefit calculation?

Average method

Strict (monthly) method

Average loan formula?

Interest = 3.75% × (Opening loan + Closing loan) ÷ 2

Strict method approach?

Calculate interest month-by-month on actual balances

When is NO loan benefit charged?

If total loans ≤ £10,000

If loan exceeds £10,000?

Entire loan taxed (not just excess)

What if loan is written off?

FULL amount is taxable

Final taxable benefit for loans?

LOWER of average vs strict method

When is accommodation NOT taxable and exempt?

When it is job-related

What counts as job-related accommodation?

Security reasons e.g. prime minister

Necessary for job e.g. caretaker

Customary for job

Basic accommodation benefit =

Greater of:

Annual value

Rent paid by employer - (if employer doesnt own property) doesn't

What happens to employee contributions to accomodation?

Deduct from benefit

accommodation: when does additional charges apply

employer owns the building

if property cost greater than £75,000

accommodation: Additional charge formula?

(Cost – 75,000) × official interest rate

accommodation: If property owned > 6 years before use?

Use market value at start, not cost

at the start of the financial year the employee moves in

If employer rents property, do we do additional charge?

❌ No (only basic charge)

If employer owns property?

✅ Basic + possible additional charge

When does a living expenses benefit arise?

When employer pays household costs

Job-related living expenses benefit =

Lower of:

Cost to employer

10% × net earnings

Non-job-related living expenses benefit =

Full cost to employer

Examples of living expenses?

Heating

Lighting

Cleaning

Maintenance

Furniture (follows use of asset rule - 20%)

is Workplace nursery exempt?

✅ Exempt (if employer-run)

What is an exempt benefit?

A benefit not taxable → NOT included in employment income

are Staff parties limit exempt?

£150 per head

❌ If exceeded → FULL amount taxable

When is an expense allowable?

Must be:

Wholly

Exclusively

Necessarily

for the job

specific allowable deductions

professional subscriptions

business travelling and other expenses incurred

Mixed (private + business) expense?

Only business portion allowed

When is commuting allowed?

Temporary workplace (< 24 months)

Approved mileage rates?

45p (first 10,000 miles)

25p (after)

Approved mileage rates

If employer pays MORE?

If employer pays LESS?

Excess = taxable

Employee claims deduction

EXEMPT = “CRAP MESS BUS” trick

Canteen

Removal (£8k)

Accommodation (job-related)

Parking

Mobile

Events (£150)

Sports

Subsidised buses

Bicycles

Under £6 home working

Service awards

contributing to a pension, max contribution tax relief

higher of

£3,600

earnings of the year

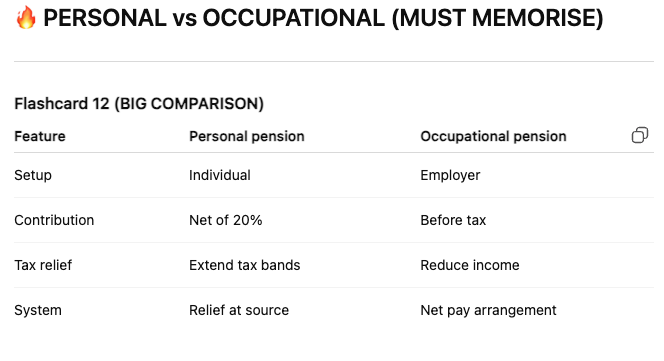

PERSONAL vs OCCUPATIONAL pension

How to spot which pension type in exam?

“Paid net of tax / relief at source” → Personal

“Deducted from salary before tax” → Occupational

How can an employee legally reduce taxable income?

Choose exempt benefits over taxable ones

Select benefits with lower cash equivalent

Contribute towards company car (not fuel)

Pay into a pension scheme

Use payroll giving (charity)

Claim all allowable deductions (e.g. business travel)

Keep income below £100,000 (avoid PA loss)

Prefer benefits over cash (no employee NIC)

EMPLOYMENT BASICS

Employment = salary + bonuses + benefits

Taxed at earlier of receipt or entitlement

Must distinguish employment vs self-employment

BENEFITS IN KIND

Most benefits = taxable

Car benefit = % × list price (based on CO₂)

Fuel benefit = additional charge

Van benefit = fixed (£4,020 + fuel £769)

Assets = 20% of value

Loans = interest saving

Accommodation = annual value + possible extra (>£75k)

EXEMPT BENEFITS

Job-related accommodation

Canteen, parking, childcare, pensions

Staff events (£150), home working (£6/week)

Mileage, bicycles, mobile phone

ALLOWABLE DEDUCTIONS

Must be wholly, exclusively, necessarily

Business travel ✔ | Commuting ❌

Temporary workplace (<24 months) ✔

Mileage: 45p / 25p

Reimbursed expenses → exempt

PENSIONS & CHARITY

Occupational pension → reduces income

Personal pension → extends tax bands

Employer contributions → exempt

Payroll giving → reduces taxable income