KTTC

1/286

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

287 Terms

Claims for which formal instruments of credit are issued as proof of the debt are

a. accounts receivable.

b. interest receivable.

c. notes receivable.

d. other receivables.

c

Interest is usually associated with

a. accounts receivable.

b. notes receivable.

c. doubtful accounts.

d. bad debts.

b

The receivable that is usually evidenced by a formal instrument of credit is a(n)

a. trade receivable.

b. notes receivable.

c. accounts receivable.

d. income tax receivable.

b

Which of the following receivables would not be classified as an "other receivable"?

a. Advance to an employee

b. Refundable income tax

c. Notes receivable

d. Interest receivable

c

Notes or accounts receivables that result from sales transactions are often called

a. sales receivables.

b. non-trade receivables.

c. trade receivables.

d. merchandise receivables.

c

The term "receivables" refers to

a. amounts due from individuals or companies.

b. merchandise to be collected from individuals or companies.

c. cash to be paid to creditors.

d. cash to be paid to debtors.

a

Among the types of receivables reported on the statement of financial position, which of the following is considered the most significant claim held by a company?

a. Others receivables (including loans to officers).

b. Notes receivable.

c. Accounts receivable.

d. Advances to employees.

c

Caps On Company manufactures sporting goods and clothing. Caps On sold

merchandise to Pro Sports Company on June 5, 2017 for $3,000, terms 2/10, n/30. On June 9, 2017 Pro Sports returns merchandise worth $200 to Caps On. On June 14, 2017 Caps On receives payment in full from Pro Sports. Which of the following is true regarding the transaction on June 14, 2017?

a. Caps On receives $2,800 from Pro Sports.

b. Caps On receives $2,744 from Pro Sports.

c. Pro Sports will pay $2,940 to Caps On.

d. All of these answer choices are correct.

b

The entry to record merchandise returned to the seller includes a

a. debit to Sales Returns and Allowances.

b. debit to Sales Revenue.

c. credit to Inventory.

d. debit to either Sales Returns and Allowances or Sales Revenue.

a

Which one of the following is not a primary problem associated with accounts receivable?

a. Depreciating accounts receivable

b. Recognizing accounts receivable

c. Valuing accounts receivable

d. Disposing of accounts receivablea

a

Trade accounts receivable are valued and reported on the statement of financial position

a. in the investment section.

b. at gross amounts less sales returns and allowances.

c. at cash realizable value.

d. only if they are not past due.

c

Three accounting issues associated with accounts receivable are

a. depreciating, returns, and valuing.

b. depreciating, valuing, and collecting.

c. recognizing, valuing, and disposing.

d. accrual, bad debts, and disposing.

c

Which of the following would require a compound journal entry?

a. To record merchandise returned that was previously purchased on account.

b. To record sales on account.

c. To record purchases of inventory when a discount is offered for prompt payment.

d. To record collection of accounts receivable when a cash discount is taken.

d

The adjusting entry a retailer makes to record interest on customer amounts due includes

a debit to

a. Notes Receivable.

b. Interest Receivable.

c. Accounts Receivable.

d. Interest Revenue.

c

A customer charges a treadmill at Mike’s Sport Shop. The price is €800 and the financing charge is 9% per annum if the bill is not paid in 30 days. The customer fails to pay the bill within 30 days and a finance charge is added to the customer’s account.

What is the amount of the finance charge?

a. €24

b. €6

c. €72

d. €2

b

A customer charges a treadmill at Mike’s Sport Shop. The price is €2,000 and the financing charge is 9% per annum if the bill is not paid in 30 days. The customer fails to pay the bill within 30 days and a finance charge is added to the customer’s account.

The accounts affected by the journal entry made by Mike’s Sport Shop to record the finance charge are

a. Accounts Receivable

Cash

b. Cash

Finance Receivable

c. Accounts Receivable

Interest Payable

d. Accounts Receivable

Interest Revenue

d

The net amount expected to be received in cash from receivables is termed the

a. cash realizable value.

b. cash-good value.

c. gross cash value.

d. cash-equivalent value.

a

If a department store fails to make the entry to accrue the finance charges due from customers,

a. accounts receivable will be overstated.

b. interest revenue will be understated.

c. interest expense will be overstated.

d. interest expense will be understated.

b

Under the allowance method, writing off an uncollectible account

a. affects only statement of financial position accounts.

b. affects both statement of financial position and income statement accounts.

c. affects only income statement accounts.

d. is not acceptable practice.

a

When a company determines a particular account to be uncollectible, it charges the loss to Bad Debt Expense under

a. the allowance method.

b. the direct writeoff method.

c. both the allowance method and the direct write–off method.

d. None of these answer choices are correct.

b

If a company fails to record estimated bad debts expense,

a. cash realizable value is understated.

b. expenses are understated.

c. revenues are understated.

d. receivables are understated.

b

Wright sells softball equipment. On November 14, they shipped $2,000 worth of softball uniforms to Paola Middle School, terms 2/10, n/30. On November 21, they received an order from Paola Middle School for $1,500 worth of custom printed bats to be produced in December. On November 30, Paola Middle School returned $250 of defective merchandise.

Wright has received no payments from either school as of month end. What amount will be recognized as net accounts receivable on the statement of financial position as of November 30?

a. $3,500

b. $3,250

c. $2,000

d. $1,750

d

Fowler Company on July 15 sells merchandise on account to Coffey Co. for $3,000, terms 2/10, n/30. On July 20, Coffey Co. returns merchandise worth $1,200 to Fowler Company. On July 24, payment is received from Coffey Co. for the balance due. What is the amount of cash received?

a. $1,800

b. $1,764

c. $1,740

d. $3,000

b

The existing balance in Allowance for Doubtful Accounts is considered in computing bad debts expense in the

a. direct write-off method.

b. percentage of receivables basis.

c. percentage of sales basis.

d. percentage of receivables and percentage of sales basis.

b

When the allowance method is used to account for uncollectible accounts, Bad Debt Expense is debited when

a. a sale is made.

b. an account becomes bad and is written off.

c. management estimates the amount of uncollectibles.

d. a customer’s account becomes past-due.

c

When an account becomes uncollectible and must be written off,

a. Allowance for Doubtful Accounts should be credited.

b. Accounts Receivable should be credited.

c. Bad Debt Expense should be credited.

d. Sales should be debited.

b

The collection of an account that had been previously written off under the allowance method of accounting for uncollectibles

a. will increase income in the period it is collected.

b. will decrease income in the period it is collected.

c. requires a correcting entry for the period in which the account was written off.

d. does not affect income in the period it is collected.

d

The percentage of sales basis of estimating expected uncollectibles

a. emphasizes the matching of expenses with revenues.

b. emphasizes statement of financial position relationships.

c. emphasizes cash realizable value.

d. is not generally accepted as a basis for estimating bad debts.

a

An aging of a company’s accounts receivable indicates that $7,500 are estimated to be uncollectible. If Allowance for Doubtful Accounts has a $1,100 credit balance, the adjustment to record bad debts for the period will require a

a. debit to Bad Debt Expense for $7,500.

b. debit to Allowance for Doubtful Accounts for $6,400.

c. debit to Bad Debt Expense for $6,400.

d. credit to Allowance for Doubtful Accounts for $7,500.

c

A debit balance in the Allowance for Doubtful Accounts

a. is the normal balance for that account.

b. indicates that actual bad debt write-offs have exceeded previous provisions for bad debts.

c. indicates that actual bad debt write-offs have been less than what was estimated.

d. cannot occur if the percentage of sales method of estimating bad debts is used.

b

Under the direct write-off method of accounting for uncollectible accounts, Bad Debts Expense is debited

a. when a credit sale is past due.

b. at the end of each accounting period.

c. whenever a pre-determined amount of credit sales have been made.

d. when an account is determined to be uncollectible.

d

An alternative name for Bad Debt Expense is

a. Deadbeat Expense.

b. Uncollectible Accounts Expense.

c. Collection Expense.

d. Credit Loss Expense.

b

A reasonable amount of uncollectible accounts is evidence

a. that the credit policy is too strict.

b. that the credit policy is too lenient.

c. of a sound credit policy.

d. of poor judgments on the part of the credit manager.

c

Bad Debt Expense is considered

a. an avoidable cost in doing business on a credit basis.

b. an internal control weakness.

c. a necessary risk of doing business on a credit basis.

d. avoidable unless there is a recession.

c

The best managed companies will have

a. no uncollectible accounts.

b. a very strict credit policy.

c. a very lenient credit policy.

d. some accounts that will prove to be uncollectible.

d

Two methods of accounting for uncollectible accounts are the

a. allowance method and the accrual method.

b. allowance method and the net realizable method.

c. direct write-off method and the accrual method.

d. direct write-off method and the allowance method.

d

The allowance method of accounting for uncollectible accounts is required if

a. the company makes any credit sales.

b. bad debts are significant in amount.

c. the company is a retailer.

d. the company charges interest on accounts receivable.

b

Bad Debt Expense is sometimes called

a. Allowance for Doubtful Accounts.

b. Loss from Default.

c. Uncollectible Accounts Expense.

d. None of these answer choices are correct.

c

When the allowance method of accounting for uncollectible accounts is used, Bad Debts Expense is recorded

a. in the year after the credit sale is made.

b. in the same year as the credit sale.

c. as each credit sale is made.

d. when an account is written off as uncollectible.

b

The method of accounting for uncollectible accounts that results in a better matching of expenses with revenues is the

a. aging accounts receivable method.

b. direct write-off method.

c. percentage of receivables method.

d. percentage of sales method.

d

To record estimated uncollectible accounts using the allowance method, the adjusting entry would be a

debit to Accounts Receivable and a credit to Allowance for Doubtful Accounts.

debit to Bad Debt Expense and a credit to Allowance for Doubtful Accounts.

debit to Allowance for Doubtful Accounts and a credit to Accounts Receivable.

debit to Loss on Credit Sales and a credit to Accounts Receivable.

b

Under the allowance method of accounting for uncollectible accounts,

a. the cash realizable value of accounts receivable is greater before an account is written off than after it is written off.

b. Bad Debt Expense is debited when a specific account is written off as uncollectible.

c. the cash realizable value of accounts receivable in the statement of financial position is the same before and after an account is written off.

d. Allowance for Doubtful Accounts is closed each year to Income Summary.

c

Allowance for Doubtful Accounts on the statement of financial position

is offset against total current assets.

increases the cash realizable value of accounts receivable.

appears under the heading "Other Assets."

is offset against accounts receivable.

d

When an account is written off using the allowance method, the

a. cash realizable value of total accounts receivable will increase.

b. total accounts receivable will decrease.

c. allowance account will increase.

d. total accounts receivable will stay the same.

b

If an account is collected after having been previously written off,

the allowance account should be debited.

only the control account needs to be credited.

both income statement and statement of financial position accounts will be affected.

there will be both a debit and a credit to accounts receivable.

d

When an account is written off using the allowance method, accounts receivable

is unchanged and the allowance account increases.

increases and the allowance account increases.

decreases and the allowance account decreases.

decreases and the allowance account increases.

c

Two bases for estimating uncollectible accounts are:

percentage of assets and percentage of sales.

percentage of receivables and percentage of total revenue.

percentage of current assets and percentage of sales.

percentage of receivables and percentage of sales.

d

The percentage of receivables basis for estimating uncollectible accounts emphasizes

a. cash realizable value.

b. the relationship between accounts receivable and bad debt expense.

c. income statement relationships.

d. the relationship between sales and accounts receivable.

a

Hahn Company uses the percentage of sales method for recording bad debt expense. For the year, cash sales are $300,000 and credit sales are $1,500,000. Management estimates that 1% is the sales percentage to use. What adjusting entry will Hahn Company make to record the bad debt expense?

a. Bad Debt Expense ....................................................... 18,000

Allowance for Doubtful Accounts ......................... 18,000

b. Bad Debt Expense ....................................................... 15,000

Allowance for Doubtful Accounts ......................... 15,000

c. Bad Debt Expense ....................................................... 15,000

Accounts Receivable ........................................... 15,000

d. Bad Debt Expense ....................................................... 18,000

Accounts Receivable ........................................... 18,000

b

The balance of Allowance for Doubtful Accounts prior to making the adjusting entry to record estimated uncollectible accounts

is relevant when using the percentage of receivables basis.

is relevant when using the percentage of sales basis.

is relevant to both bases of adjusting for uncollectible accounts.

will never show a debit balance at this stage in the accounting cycle.

a

The direct write-off method of accounting for bad debts

a. uses an allowance account.

b. uses a contra-asset account.

c. does not require estimates of bad debt losses.

d. is the preferred method under IFRS.

c

Under the direct write-off method of accounting for uncollectible accounts

a. the allowance account is increased for the actual amount of bad debt at the time of write-off.

b. a specific account receivable is decreased for the actual amount of bad debt at the time of write-off.

c. balance sheet relationships are emphasized.

d. bad debts expense is always recorded in the period in which the revenue was recorded.

b

An aging of a company’s accounts receivable indicates that $10,000 are estimated to be uncollectible. If Allowance for Doubtful Accounts has a $2,400 credit balance, the adjustment to record bad debts for the period will require a

a. debit to Bad Debt Expense for $10,000.

b. debit to Allowance for Doubtful Accounts for $7,600.

c. debit to Bad Debt Expense for $7,600.

d. credit to Allowance for Doubtful Accounts for $10,000.

c

An aging of a company’s accounts receivable indicates that $21,000 are estimated to be uncollectible. If Allowance for Doubtful Accounts has a $6,000 debit balance, the adjustment to record bad debts for the period will require a

a. debit to Bad Debt Expense for $21,000.

b. debit to Bad Debt Expense for $27,000.

c. debit to Bad Debt Expense for $15,000.

d. credit to Allowance for Doubtful Accounts for $6,000.

b

Using the percentage of receivables method for recording bad debts expense, estimated uncollectible accounts are ¥500,000. If the balance of the Allowance for Doubtful Accounts is ¥120,000 debit before adjustment, what is the amount of bad debts expense for that period?

a. ¥500,000

b. ¥120,000

c. ¥620,000

d. ¥380,000

c

Using the percentage of receivables method for recording bad debts expense, estimated uncollectible accounts are ¥500,000. If the balance of the Allowance for Doubtful Accounts is ¥100,000 credit before adjustment, what is the amount of bad debts expense for that period?

a. ¥500,000

b. ¥400,000

c. ¥600,000

d. ¥100,000

b

Using the percentage of receivables method for recording bad debts expense, estimated uncollectible accounts are ¥500,000. If the balance of the Allowance for Doubtful Accounts is ¥100,000 debit before adjustment, what is the balance after adjustment?

a. ¥500,000

b. ¥600,000

c. ¥400,000

d. ¥100,000

a

Using the allowance method, the uncollectible accounts for the year is estimated to be $84,000. If the balance for the Allowance for Doubtful Accounts is a $21,000 credit before adjustment, what is the amount of bad debts expense for the period?

a. $21,000

b. $63,000

c. $84,000

d. $105,000

b

Using the allowance method, the uncollectible accounts for the year is estimated to be $84,000. If the balance for the Allowance for Doubtful Accounts is a $21,000 debit before adjustment, what is the amount of bad debts expense for the period?

a. $21,000

b. $63,000

c. $84,000

d. $105,000

d

In reviewing the accounts receivable, the cash realizable value is $33,000 before the write-off of a $2,000 account. What is the cash realizable value after the write-off?

a. $33,000

b. $2,000

c. $35,000

d. $31,000

a

In 2017, the Dugan Co. had net credit sales of $1,500,000. On January 1, 2017, Allowance for Doubtful Accounts had a credit balance of $32,000. During 2017, $60,000 of uncollectible accounts receivable were written off. Past experience indicates that the allowance should be 10% of the balance in receivables (percentage of receivable basis).

If the accounts receivable balance at December 31 was $400,000, what is the required adjustment to the Allowance for Doubtful Accounts at December 31, 2017?

a. $40,000

b. $68,000

c. $72,000

d. $60,000

b

A company has net credit sales of $800,000 for the year and it estimates that uncollectible accounts will be 2% of sales. If Allowance for Doubtful Accounts has a credit balance of $1,000 prior to adjustment, its balance after adjustment will be a credit of

a. $16,000.

b. $17,000.

c. $15,980.

d. $15,000.

b

In 2017, Garrison Company had net credit sales of $2,250,000. On January 1, 2017, Allowance for Doubtful Accounts had a credit balance of $54,000. During 2017, $90,000 of uncollectible accounts receivable were written off. Past experience indicates that the allowance should be 10% of the balance in receivables (percentage of receivables basis). If the accounts receivable balance at December 31 was $700,000, what is the required adjustment to the Allowance for Doubtful Accounts at December 31, 2017?

a. $60,000

b. $225,000

c. $106,000

d. $90,000

c

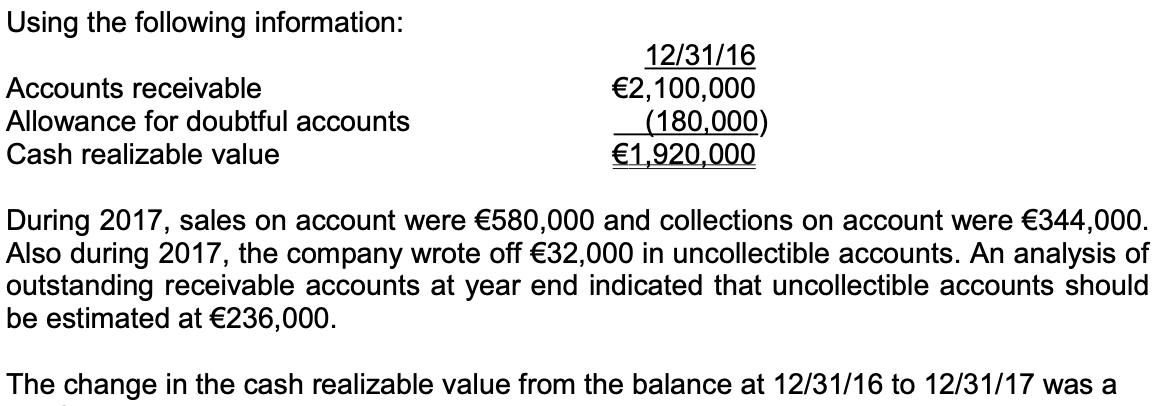

a. €268,000 increase.

b. €236,000 increase.

c. €148,000 increase.

d. €204,000 increase.

c

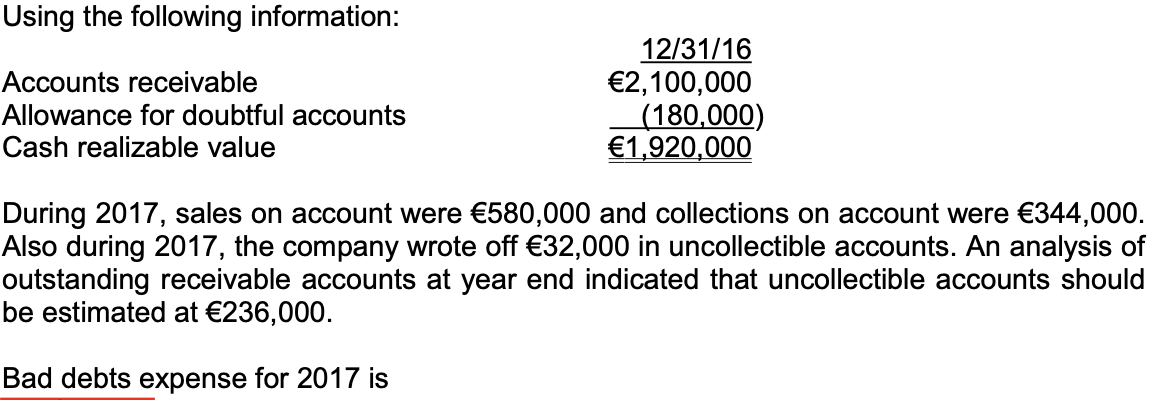

a. €88,000.

b. €56,000.

c. €236,000

d. €4,000.

a

During 2017, Hitchcock Inc. had sales on account of $528,000, cash sales of $216,000, and collections on account of $336,000. In addition, they collected $5,850 which had been written off as uncollectible in 2016. As a result of these transactions, the change in the accounts receivable balance indicates a

a. $402,150 increase.

b. $192,000 increase.

c. $186,150 increase.

d. $408,000 increase.

b

Klosterman CorporationÜs unadjusted trial balance includes the following balances (assume normal balances):

Accounts Receivable $373,000

Allowance for Doubtful Accounts 5,325

Bad debts are estimated to be 3% of outstanding receivables. What amount of bad debts expense will the company record?

a. $11,190

b. $5,865

c. $11,403

d. $10,977

b

Black Company provides for bad debts expense at the rate of 2% of credit sales. The following data are available for 2017:

Allowance for doubtful accounts, 1/1/17 (Cr.)........................ $ 21,000

Accounts written off as uncollectible during 2017.................. 13,000

Credit sales in 2017 .............................................................. 3,500,000

The Allowance for Doubtful Accounts balance at December 31, 2017, should be

a. $78,000

b. $70,000

c. $62,000

d. $13,000

a

In 2017, Freeze Company had credit sales of $1,800,000 and granted sales discounts of $36,000. On January 1, 2017, Allowance for Doubtful Accounts had a credit balance of $45,000. During 2017, $75,000 of uncollectible accounts receivable were written off. Past experience indicates that 3% of net credit sales become uncollectible. What should be the adjusted balance of Allowance for Doubtful Accounts at December 31, 2017?

a. $22,920

b. $24,000

c. $52,920

d. $99,000

a

An analysis and aging of the accounts receivable of Downs Company at December 31 revealed the following data:

Accounts Receivable............................................................ ₤980,000

Allowance for Doubtful Accounts per books before adjustment (Cr.)....................................................... 100,000

Amounts expected to become uncollectible........................... 109,000

The cash realizable value of the accounts receivable at December 31, after adjustment, is:

a. ₤971,000

b. ₤880,000

c. ₤871,000

d. ₤771,000

c

Franks Company has a debit balance of $4,000 in its Allowance for Doubtful Accounts before any adjustments are made at the end of the year. Based on review and aging of its accounts receivable at the end of the year, Franks estimates that $80,000 of its receivables are uncollectible. The amount of bad debts expense which should be reported for the year is:

a. $4,000

b. $76,000

c. $80,000

d. $84,000

d

Which of the following methods is not acceptable for financial reporting purposes?

Percentage of sales (emphasis on income statement).

Percentage of receivables (emphasis on statement of financial position).

Direct write-off.

All of these answer choices are acceptable.

c

Which of the following is false regarding the Allowance for Doubtful Accounts?

The Allowance for Doubtful Accounts is closed at the end of the fiscal year.

Cash realizable value reduces receivables in the statement of financial position by the amount of estimated uncollectible receivables.

Cash realizable value is also referred to as "amortized cost" by the International Accounting Standards Board.

Cash realizable value is also referred to as "cash (net) realizable value.”

a

Which of the following relationships best describes the percentage of receivables basis of valuing accounts receivable?

Matching, emphasis on income statement relationships.

Cash realizable value emphasis on income statement relationships.

Matching, emphasis on statement of financial position relationships.

Cash realizable value, emphasis on statement of financial position relationships.

d

Which of the following transactions affects only statement of financial position accounts?

Recovery of a bad debt using the allowance method.

Recording bad debt expense using the allowance method.

Writing off a bad debt using the direct write-off method.

Recording bad debt expense using the percentage of sales basis.

a

Which of the following statements is false regarding the different bases used for the allowance method?

a. Three bases are generally accepted, the percentage of sales, the percentage of receivables, and the direct write-off.

b. Management can choose whichever basis it prefers.

c. If management wishes to emphasize the cash realizable value of receivables it will select the percentage of receivables basis.

d. The company must determine its past experience with bad debt losses regardless of which basis it selects.

a

The_______________ produces the better estimate of cash realizable value and reflects a statement of financial position viewpoint.

a. Direct write-off method.

b. Factoring of accounts receivable.

c. Percentage of receivable basis.

d. Expense recognition principle.

c

Gowns, Inc. uses the percentage of receivables basis to estimate its bad debts. At December 31, 2017, Gowns estimates total bad debts that will become uncollectible in the future as €6,608. The existing balance in the Allowance for Doubtful Accounts is a credit balance of €1,408. The Accounts Receivable balance at December 31, 2017 is €105,600.

The amount of the bad debt adjusting entry at December 31, 2017 will impact the statement of financial position accounts by

a. Increasing expenses by €6,608.

b. Increasing the Allowance for Doubtful Accounts by €6,608.

c. Increasing Accounts Receivable by €5,200.

d. Increasing the Allowance for Doubtful Accounts by €5,200.

d

Gowns, Inc. uses the percentage of receivables basis to estimate its bad debts. At December 31, 2017, Gowns estimates total bad debts that will become uncollectible in the future as €11,140. The existing balance in the Allowance for Doubtful Accounts is a credit balance of €2,640. The Accounts Receivable balance at December 31, 2017 is €198,000.

The cash realizable value of Accounts Receivable reported on the statement of financial position at December 31, 2017 is

a. €195,360.

b. €209,140.

c. €186,860.

d. €189,500

c

Gowns, Inc. uses the percentage of receivables basis to estimate its bad debts. At December 31, 2017, Gowns estimates total bad debts that will become uncollectible in the future as €11,140. The existing balance in the Allowance for Doubtful Accounts is a debit balance of €2,640. The Accounts Receivable balance at December 31, 2017 is €198,000.

The amount of the bad debts adjusting entry at December 31, 2017 will impact the statement of financial position by

a. Increasing expenses by €11,140.

b. Increasing the Allowance for Doubtful Accounts by €13,780.

c. Increasing the Allowance for Doubtful Accounts by €11,140.

d. Increasing the Allowance for Doubtful Accounts by €8,500.

b

Gowns, Inc. uses the percentage of receivables basis to estimate its bad debts. At December 31, 2017, Gowns estimates total bad debts that will become uncollectible in the future as €11,140. The existing balance in the Allowance for Doubtful Accounts is a debit balance of €2,640. The Accounts Receivable balance at December 31, 2017 is €198,000.

The cash realizable value of Accounts Receivable reported on the statement of financial position at December 31, 2017 is

a. €184,220.

b. €209,140.

c. €186,860.

d. €189,500.

c

Gowns, Inc. uses the percentage of sales basis to estimate its bad debts. For the year ended December 31, 2017, Gowns’ total credit sales are €2,500,000. Management of the company estimates that 1% of credit sales will become uncollectible. The existing balance in the Allowance for Doubtful Accounts is a debit balance of €3,000. The Accounts Receivable balance at December 31, 2017 is €220,000.

The entry to record bad debt expense at December 31, 2017 will impact the statement of financial position by

a. Increasing expenses by €22,000.

b. Increasing the Allowance for Doubtful Accounts by €22,000.

c. Increasing the Allowance for Doubtful Accounts by €25,000.

d. Increasing the Allowance for Doubtful Accounts by €28,000.

c

Gowns, Inc. uses the percentage of sales basis to estimate its bad debts. For the year ended December 31, 2017, Gowns’ total credit sales are €2,500,000. Management of the company estimates that 1% of credit sales will become uncollectible. The existing balance in the Allowances for Doubtful Accounts is a debit balance of €3,000. The Accounts Receivable balance at December 31, 2017 is €220,000.

The cash realizable value of Accounts Receivable reported on the statement of financial position at December 31, 2017 is

a. €195,000.

b. €198,000.

c. €192,000.

d. €242,000.

b

Gowns, Inc. uses the percentage of sales basis to estimate its bad debts. For the year ended December 31, 2017, Gowns’ total credit sales are €2,500,000. Management of the company estimates that 1% of credit sales will become uncollectible. The existing balance in the Allowances for Doubtful Accounts is a credit balance of €3,000. The Accounts Receivable balance at December 31, 2017 is €220,000.

The cash realizable value of Accounts Receivable reported on the statement of financial position at December 31, 2017 is

a. €195,000.

b. €198,000.

c. €192,000.

d. €242,000.

c

Miles to Go is a travel agency specializing in tours to Africa and Australia. Miles to Go has $2,000,000 in accounts receivable and factors these receivables with Fox Factors. The agreement with Fox calls for a service charge of 2% of the amount of receivables sold.

The net effects on the statement of financial position for Miles to Go of factoring its receivables is a(n)

a. Increase in assets of $40,000.

b. Increase in assets of $1,960,000.

c. Increase in equity of $1,960,000.

d. Decrease in equity of $40,000.

d

Miles to Go is a travel agency specializing in tours to Africa and Australia. Miles to Go has $4,000,000 in accounts receivable. During 2017, Miles to Go enters into a factoring arrangement with Fox Factors to factor 75% of their receivables. The agreement with Fox calls for a services charge of 2% of the amount of receivables sold.

The effects on the statement of financial position for Miles to Go of factoring its receivables includes a(n)

a. Increase in cash of $2,940,000.

b. Increase in assets of $4,000,000.

c. Increase in cash of $3,920,000.

d. Increase in equity of $80,000.

a

On October 1, 2017, Brosnan Company sells (factors) $800,000 of receivables to Nation Factors, Inc. Nation assesses a service charge of 3% of the amount of receivables sold.

The journal entry to record the sale by Brosnan will include:

a. a debit of $800,000 to Accounts Receivable.

b. a credit of $824,000 to Cash.

c. a debit of $824,000 to Cash.

d. a debit of $24,000 to Service Charge Expense.

d

On March 1, 2017, Joe Miles purchased a suit at Calvin’s Fine Apparel Store. The suit cost $400 and Joe used his Calvin credit card. Calvin charges 2% per month interest if payment on credit charges is not made within 30 days. On April 30, 2017, Joe had not yet made his payment. What entry should Calvin make on April 30th?

a. Uncollectible Account ................................................... 400

Accounts Receivable............................................ 400

b. Bad Debt Expense........................................................ 392

Interest Expense........................................................... 8

Accounts Receivable............................................ 400

c. Accounts Receivable .................................................... 408

Interest Revenue.................................................. 8

Sales Revenue..................................................... 400

d. Accounts Receivable .................................................... 8

Interest Revenue.................................................. 8

d

Newland Retailers accepted $80,000 of Citibank Visa credit card charges for merchandise sold on July 1. Citibank charges 4% for its credit card use. The entry to record this transaction by Newland Retailers will include a credit to Sales Revenue of $80,000 and a debit(s) to

a. Cash $76,800 and Service Charge Expense $3,200.

b. Accounts Receivable $86,400 and Service Charge Expense $3,200.

c. Cash $76,800 and Interest Expense $3,200.

d. Accounts Receivable $80,000.

a

ABC Company accepted a national credit card for a €12,500 purchase. The cost of the goods sold is €10,000. The credit card company charges a 3% fee. What is the impact of this transaction on net operating income?

a. Increase by €2,425

b. Increase by €2,500

c. Increase by €2,125

d. Increase by €12,125

c

Major advantages of credit cards to the retailer include all of the following except the

issuer does the credit investigation of customers.

issuer undertakes the collection process.

retailer receives more cash from the credit card issuer.

All of these answer choices are correct.

c

The sale of receivables by a business

indicates that the business is in financial difficulty.

is generally the major revenue item on its income statement.

is an indication that the business is owned by a factor.

can be a quick way to generate cash for operating needs.

d

If a retailer regularly sells its receivables to a factor, the service charge of the factor should be classified as a(n)

a. selling expense.

b. interest expense.

c. other expense.

d. contra asset.

a

If a company sells its accounts receivables to a factor,

the seller pays a commission to the factor.

the factor pays a commission to the seller.

there is a gain on the sale of the receivables.

the seller defers recognition of sales revenue until the account is collected.

a

Retailers generally consider sales from the use of national credit card sales as a

credit sale.

cash sale.

collection of an accounts receivable.

collection of a note receivable.

b

Receivables might be sold to

a. lengthen the cash-to-cash operating cycle.

b. take advantage of deep discounts on the cash realizable value of receivables.

c. generate cash quickly.

d. finance companies at an amount greater than cash realizable value.

c

A company regularly sells its receivables to a factor who assesses a 2% service charge on the amount of receivables purchased. Which of the following statements is true for the seller of the receivables?

a. The loss section of the income statement will increase each time receivables are sold.

b. The credit to Accounts Receivable is less than the debit to Cash when the accounts are sold.

c. Selling expenses will increase each time accounts are sold.

d. The other income

c

Oliver Furniture factors $800,000 of receivables to Kwik Factors, Inc. Kwik Factors assesses a 2% service charge on the amount of receivables sold. Oliver Furniture factors its receivables regularly with Kwik Factors. What journal entry does Oliver make when factoring these receivables?

a. Cash............................................................................. 784,000

Loss on Sale of Receivables......................................... 16,000

Accounts Receivable............................................ 800,000

b. Cash............................................................................. 784,000

Accounts Receivable............................................ 784,000

c. Cash............................................................................. 800,000

Accounts Receivable............................................ 784,000

Gain on Sale of Receivables................................ 16,000

d. Cash............................................................................. 784,000

Service Charge Expense .............................................. 16,000

Accounts Receivable............................................ 800,000

d

When customers make purchases with a national credit card, the retailer

a. is responsible for maintaining customer accounts.

b. is not involved in the collection process.

c. absorbs any losses from uncollectible accounts.

d. receives cash equal to the full price of the merchandise sold from the credit card company.

b

The retailer considers Visa and MasterCard sales as

a. cash sales.

b. promissory sales.

c. credit sales.

d. contingent sales.

a