Insurance Exam 3

1/30

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

31 Terms

Tort

A legal wrong for which the law allows a remedy in the form of money damages. The person who is injured or harmed by the actions of another party can sue for damages.

Three Category’s:

Intentional torts

Strict liability (absolute liability) - Does not matter what happened because you took that risk.

Negligence

Negligence

As the failure to exercise the standard of care required by law to protect others from an unreasonable risk of harm.

Proving Negligence

•No duty, no breach, no causation, no harm

(1) Prove that the plaintiff assumed the risk of injury

Assumption of risk

(2) Prove negligence on the part of injured party

Contributory:

•bar to recovery by plaintiff since plaintiff helped cause the accident

Comparative:

•Pure Rule: allocate damages based on fault. If 95% at fault, the defendant pays 95% of the damages

49 Percent Rule: plaintiff can only recover if his fault is <= 49%

•50 Percent Rule: plaintiff can only recover if his fault is <= 50%

Last clear chance rule

Elements of Proving Negligence

1.Proof of legal duty by defendants

2.Proof that duty was breached

3.Proof that breach of duty was proximate cause of harm

4.Proof of injury, damage, harm

Joint and Several Liability Rule

Several people may be responsible for the injury, but a defendant who is only slightly responsible may be required to pay the full amount of damages.

Personal Auto Policy Coverages

Part A: Liability Coverage

Part B: Medical Payments Coverage

Part C: Uninsured Motorists Coverage

Part D: Coverage for Damage to Your Auto

Part E: Duties after an Accident or Loss

Part F: General Provisions

Uninsured Motorist Coverage

Pays for bodily injury (and property damage in some states) caused by an uninsured motorist, by a hit-and-run driver, or by a negligent driver whose insurance company is insolvent.

Compulsory Insurance Law

Requires motorists to carry at least a minimum amount of liability insurance before the vehicle can be licensed or registered.

Cons:

In general, there is no correlation between __________ and the number of uninsured vehicles on the highway.

requires motorists to carry at least a minimum amount of liability insurance before the vehicle can be licensed or registered.

Pure No-fault

Accident victims could not sue at all, regardless of the amount of the claim, and no payments would be made for pain and suffering.

Modified No Fault

Injured person has the right to sue a negligent driver only if the bodily injury claim exceeds the dollar or verbal threshold.

Add on Plan

Pays benefits to an accident victim without regard to fault, and the injured person still has the right to sue the negligent driver who caused the accident.

Choice No Fault

Pays benefits to an accident victim without regard to fault, and the injured person still has the right to sue the negligent driver who caused the accident.

Arguments for No-Fault Laws

Inequity in claim payments

High transaction costs and attorney fees

Fraudulent and inflated claims

Delay in payments

Arguments Against No-Fault Laws

Defects of the negligence system are exaggerated

Claims of efficiency and premium savings are exaggerated

Court delays are not universal

Safe drivers may be penalized

There is no payment for pain and suffering

The tort liability system needs only to be reformed

Financial Responsibility Law

Does not require proof of financial responsibility until after the driver has his or her first accident or until after conviction for certain offenses, such as driving under the influence of alcohol.

Joint Underwriting Association

An organization of auto insurers operating in the state in which high-risk business is placed in a common pool, and each company pays its pro rata share of pool losses and expenses. The ______ influences the design of the high-risk auto policy and sets the rates that are charged.

Reforming tort (civil) justice system

Capping noneconomic damages, such as pain and suffering

Reinstating the state-of-the-art defense

Restricting punitive damages

Modifying the collateral source rule

Modifying the joint and several liability rule

Alternative dispute resolution (ADR) techniques

Reinsurance Facility Pool

Under this arrangement, the insurance company must accept all applicants for insurance, both good and bad drivers. If the applicant is considered a high-risk driver, the insurer has the option of placing the driver in the reinsurance pool. Although the high-risk driver is in the reinsurance pool, the original insurer services the policy.

Maryland Automobile Insurance

A state entity that makes auto insurance available to motorists who are unable to obtain insurance in the voluntary market.

Specialty Insurers

Specialize in insuring motorists with poor driving records. These insurers typically insure drivers who have been canceled or refused insurance, teenage drivers, and drivers convicted of drunk driving. The premiums are substantially higher than premiums charged in the standard market

Homeowners (HO)-8

Is a modified coverage form that covers loss to the dwelling and other structures on the basis of repair cost, which is the amount required to repair or replace damaged property using common construction materials and methods.

Homeowners HO-4

Is designed for tenants who rent apartments, houses, or rooms. ______ covers the tenant’s personal property against loss or damage and also provides personal liability insurance.

Homeowners 3

Persons insured:

Named insured and residents of the household who are your relatives.

Other persons under age 21

Full-time student away from home

Coverage A: Dwelling

Coverage B: Other structures

Coverage C: Personal property

Coverage D: Loss of use

Factors that Effect Homeowners' Insurance

Construction

Location

Fire-protection class

Construction costs

Age of the home

Type of policy

Deductible amount

Insurance score

Loss history report

Personal Umbrella Policy

Provides protection against a catastrophic lawsuit or judgment. Most insurers write this coverage in amounts ranging from $1 million to $10 million.

Characteristics:

Excess liability insurance

Broad coverage

Self-insured retention or deductible

Reasonable cost

Coverage HO-2 (broad form), HO-3 (special form), HO-4 (contents broad form)

Section I Coverages

A. Dwelling

Minimum varies by company. Minimum varies by company.

Not applicable

B. Other structures

10% of A , 10% of A , Not applicable

C. Personal property

50% of A, 50% of A, Minimum amount varies.

D. Loss of use

30% of A, 30% of A, 30% of C

Covered perils

Fire or lightning, Windstorm or hail, Explosion, Riot or civil commotion, Aircraft, Vehicles, Smoke, Vandalism or malicious mischief, Theft, Falling objects, Weight of ice, snow, or sleet, Accidental discharge or overflow of water or steam, Sudden and accidental tearing apart, cracking, burning, or bulging of a steam, hot water, air conditioning, or automatic fire protective sprinkler system, or from within a household appliance, Freezing of a plumbing, heating, air conditioning, or automatic fire sprinkler system, or of a household appliance, Sudden and accidental damage from artificially generated electrical current, Volcanic eruption

Dwelling and other structures are covered against direct physical loss to property, All direct physical losses are covered except those losses specifically excluded, Personal property is covered for the same perils as HO-2, Same perils as HO-2 for personal property

E. Personal liability

$100,000, $100,000, $100,000

F. Medical payments to others

$1,000 per person, $1,000 per person, $1,000 per person

HO-5 (comprehensive form), HO-6 (unit-owners form), HO-8 (modified coverage form) Section 1 Coverage

Minimum varies by company, $5,000 minimum, Minimum varies by company.

10% of A, Included in Coverage A, 10% of A

50% of A, Minimum amount varies, 50% of A

30% of A, 50% of C, 10% of A

Dwelling and other structures are covered against direct physical loss to property. All direct physical losses are covered except those losses specifically excluded, Personal property is covered against direct physical loss to property. All direct physical losses are covered except those losses specifically excluded.

Same perils as HO-2 for personal property.

Fire or lightning, Windstorm or hail, Explosion, Riot or civil commotion, Aircraft, Vehicles, Smoke, Vandalism or malicious mischief, Theft (applies only to loss on the residence premises up to a maximum of $1,000), Volcanic eruption

Section II Coverages

$100,000, $100,000, $100,000

$1,000 per person, $1,000 per person, $1,000 per person

a Minimum amounts can be increased.

Homeowners Exclusions

Ordinance or Law

Earth Movement

Water Damage

Power Failure

Neglect

War

Nuclear Hazard

Intentional Loss

Governmental Action

Weather Conditions

Acts or Decisions

Faulty, Inadequate, or Defective Planning and Design

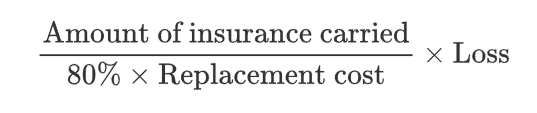

Replacement Cost Coverage

Is the amount necessary to repair or replace the dwelling with material of like kind and quality at current prices.