Risk and Insurance

1/29

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

30 Terms

Expected Income E(I)

E(I) = pW + (1-p)L

Why does insurance exist?

Because most people dislike risk

Win state

W

Loss state

L

Expected income meaning

The average income you would get if the gamble happened many times

Insurance meaning

Insurance converts uncertain income into certain income

Utility

Used to describe how much satisfaction people get from income

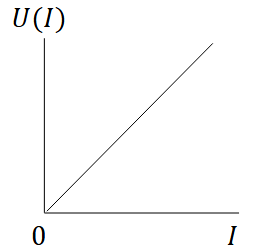

Risk neutral individual characteristics + graph

The utility function is linear

Constant marginal utility

Only cares about average income

Indifferent between certainty and risk

U(I) = Ia where a = 1

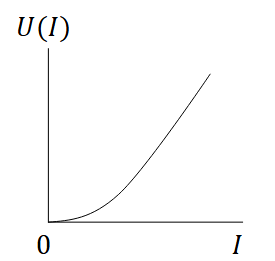

Risk Loving

Utility function is convex

Enjoys gambling

Prefers risky outcomes

EU(I) > U(E(I))

U(I) = Ia where a > 1

Risk averse

Concave utility function

Diminishing marginal utility

Dislike uncertainty

EU(I) > U(E(I))

U(I) = Ia where 0 < a < 1

Expected Utility Formula

EU(I) = pU(W) + (1 - p)U(L)

Certainty equivalent

when a guaranteed amount of money gives the SAME utility as a risky gamble (x)

Certainty equivalent formula

U(x) = EU(I)

Fair premium formula

σc = (1-p)(W - L)

Fair premium meaning

Expected loss

What type of profit is made by insurance firms in the comopetitive market?

E(π) = 0

Normal profit, hence why they care about expected profit

Risk Premium meaning

The extra amount of risk a risk-averse person will pay to eliminate risk

Risk premium formula

E(I) - CE (CE stands for certainty equivalent)

Interpretation of the risk premium calculation

The more risk averse someone is the larger their risk premium and the more they value certainty

Why are insurance firms less risk averse than individuals?

Because they diversify their risk by selling insurance to a lot of customers some of which will not actually suffer the loss

What does concave mean economically?

Diminishing marginal utility

An extra pound gives POSITIVE utility but less additional utility than the PREVIOUS pound

What does convex mean economically?

Increasing marginal utility

Each extra pound gives more extra utility than the previous pound

How is price decided in competitive markets?

Price is pushed down to fair premium price

Unless the firm has market power then the firms can charge above fair premium using this formula

σMP=σC+θED where 0 ≤ 𝜃 ≤ 1

𝜃 = 0 gives the competitive outcome

• 𝜃 = 1 gives the most uncompetitive outcome (where the insurer charges the highest

price the individual will pay)

Market failure meaning

The market doesn’t produce the efficient outcome

Asymmetric information meaning

One side of the market has more information than the other

Who tends to have more information?

The customer tends to have more information than thre insurer

Types of asymmetric information

Adverse Selection

Moral Hazard

Adverse Selection - THE PROBLE

Occurs before the insurance is bought

Issue is : Insurers cannot tell who is high risk and who is low risk

Adverse selection - What happens

Insurer is forced to charge based on average risk

this is decided using the pooled insurance premium formula

Adverse Selection - Final conclusion

for low risk people this premium is too high - they then leave the market

Only the high risk people are insured

Becomes inefficient because due to the asymmetric info there is no way of the insurer being able to specify premium charges based on the risk each individual has