ACCOUNTING (copy)

1/83

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

84 Terms

capital

The financial resources available to a company for investment and business operations.

loan

A sum of money borrowed to be paid back with interest, used for various purposes such as business investments or personal expenses.

issuing shares

Selling ownership in a company to raise capital through stock.

shareholders

Individuals or entities that own shares in a company.

share capital

Funds raised by issuing shares (Selling ownership in a company to raise capital through stock) in a company.

investors

Individuals or entities that provide capital to a company in exchange for financial returns

bonds

loans that pay interest and are repaid at a fixed future date

revenue

money received over a period of time, especially for selling goods and services

expenses

the money that individuals or entities spend on something

profit

the money you earn after paying expenses

earnings

the money you get from working or selling something

net income

= profit = earnings - revenue minus the operating costs, taxes and cost of sales - čistý príjem

dividend

the money a company shares with its owners

tax

the money you pay to the government

to retain some earnings

to keep, preserve

break-even point

the point at which profits are equal to costs, verb: to break even

to make a loss

to spend more money than you earn

consumer spending

the money people (consumers) spend on goods and services

to draw up a budget

to plan your money

to budget for (the costs)

to plan money for something you will need to pay

an actual expenditure

the real money spent

to go over budget

to spend more money than planned

to be under budget

to spend less money than planned

overspending

spending too much money

Management accounting

it involves the use of accounting data by managers in order to develop strategy, make plans and decisions

Financial accounting

it includes bookkeeping and preparing financial records for shareholders and creditors

Accounting

it involves recording, keeping and checking the financial records of an organization

financial statements

the reports that show a company’s money situation / documents showing the financial position of a company, usually a balance sheet and a profit and loss account (визначення людки)

the balance sheet

shows the company’s assets, its liabilities and its capital = suvaha

assets

the things that company owns

liabilities

the money that company owes

the profit and loss account

shows the company’s revenues and expenses during a particular period, such as three months or a year

accountants

people who keep track of money

accountancy

the work or profession of keeping and managing financial records

creative accounting

using of loopholes in a financial regulation in order to present figures in a misleadingly favorable light (OR it is when companies use clever or tricky methods to make their finances look better than they really are) = window dressing

window dressing

making financial statements look good just for a short time (like for reports or investors) = creative accounting

bookkeeping

deals with the day-to-day recording of transactions / recording daily credits and debits (vedenie účtovníctva)

bookkeepers

work under accountants / an accounts clerk

auditing

involves an official examination of financial records to see that they are true and correct

fraud

monkey business

internal audit

when a company checks its own money and processes to make sure everything is correct

controllers

people who check and manage a company’s financial records

internal auditors

people who check a company’s work to make sure everything is correct and honest

external audit

when outside experts check a company’s finances

independent auditors

the outside experts who check a company’s finances and are not part of the company

to give a true and fair view

to show the real financial situation honestly and correctly

cost cutting

reducing expenses (to save money)

tax accounting

dealing with how taxes are calculated and paid correctly

to plough back profits

to put company profits back into the business instead of taking them out (to reinvest profits)

to put up funds

to provide money / finance something

to wind up

to close down a company or business (to officially end a business) / force a company to stop trading (людка)

to wipe out

to completely destroy or remove (to make something disappear or be fully lost (money, debt, business))

to write off

to cancel a debt or loss in accounting (to accept that money cannot be recovered) / abandon debts as irrevocable - not able to be reversed (odpísať)

to go under

to go bankrupt / fail

to build up

accumulate (e.g. capital, reserves, energy)

to bring about

to cause something to happen

loss-leader

a product sold at a loss to attract customers

money-spinner, a cash cow

something very profitable

to work out

to calculate

current assets

assets that can be easily turned into cash (e.g. goods in shops or in warehouses, finished products, stocks/inventory, receivables (pohľadávky = accounts receivable) , raw-materials....)

intangible assets

it is difficult to turn these assets into cash and they are difficult to value , e.g. goodwill, trademarks , patents, copyrights

net assets

(owner's equity,or shareholders equity - vlastné imanie) = ASSETS MINUS LIABILITIES, = basic accounting equation. Net assets include: share capital (money from the issue of shares), share premium (money from selling shares above their nominal value), company reserves (retained profit)

overheads

(not related to particular products or services), e.g. rent, heating, lighting, electricity, gas, petrol, phone bills, etc.

funds flow statement

shows flow of cash in and out between balance sheet dates sources of funds: (money into a company) e.g. sales of assets, borrowings, trading profits, issuing of shares application of funds: (what you spend money on) e.g. purchasing of assets, payment of dividends, loans repayment

double-entry bookkeeping

all transactions are entered as a credit in one account and as a debit in another journals (- books of prime/first entr, day books= účtovné denníky)

ledgers

a book of final entry vouchers (hlavna kniha) - receipts - any documents proving that your accounts are correct trial balance - skúška podvojnostia way of checking that a set of accounts is correct, accurate

remuneration

journals

books of of prime/first entr, day books= účtovné denníky

day-to-day recording of transactions

equities

Ownership shares in a company, representing a claim on assets and earnings.

embezzlement

deceitful behavior in order to have some personal gains

tangible assets / tangibles

assets in a material, physical form and that can be turned into cash and easily valued : cash, cheques, securities..

debtors

accounts receivable

creditors

accounts payable

receivables

money that your clients / customers owe to you, they have to repay to you for the goods or services that have not been paid yet

payables

money that a business/company owes/has to pay

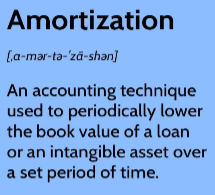

depreciation

amortization

overheads

operating costs, ongoing expenses on operating a business

stock

= inventory (US English) = finished products, value of raw materials, work in progress

debits

payments made are entered on the left hand side (debtors)

credits

payments received are entered on the right hand side (creditors)

trial balance

testing if both the sides (debit, credit) of an account book match

a voucher

evidence on financial transaction

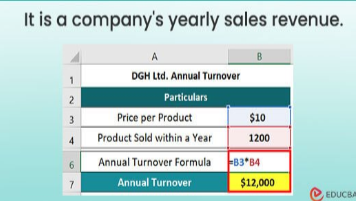

annual turnover