Microeconomics: Profit Maximization, Market Equilibrium, and Consumer/Producer Surplus

1/12

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

13 Terms

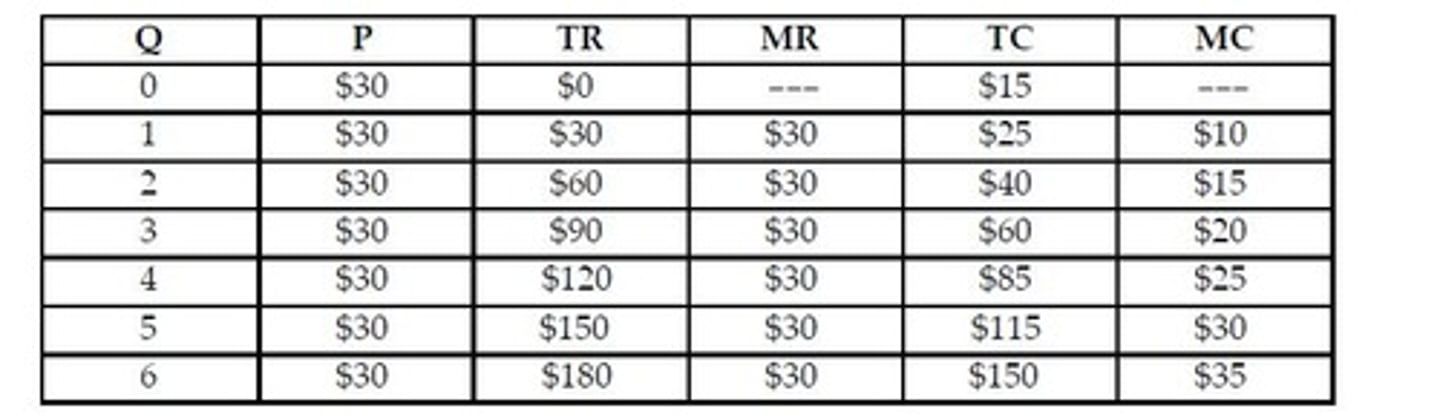

What is true of Total Revenue (TR) and Total Cost (TC) curves at the profit maximizing level of output?

They must have the same slope

What can be concluded if a profit maximizing monopolist is producing a quantity where marginal revenue exceeds marginal cost?

The firm's output is smaller than the profit maximizing quantity.

What is the economic profit if a monopolist sets output such that marginal revenue, marginal cost, and average total costs are equal?

Economic profit must be positive.

If current output is less than profit maximizing output for a perfectly competitive firm, what must be true?

Marginal revenue is greater than marginal cost.

What indicates that a firm is perfectly competitive?

Constant Marginal Revenue.

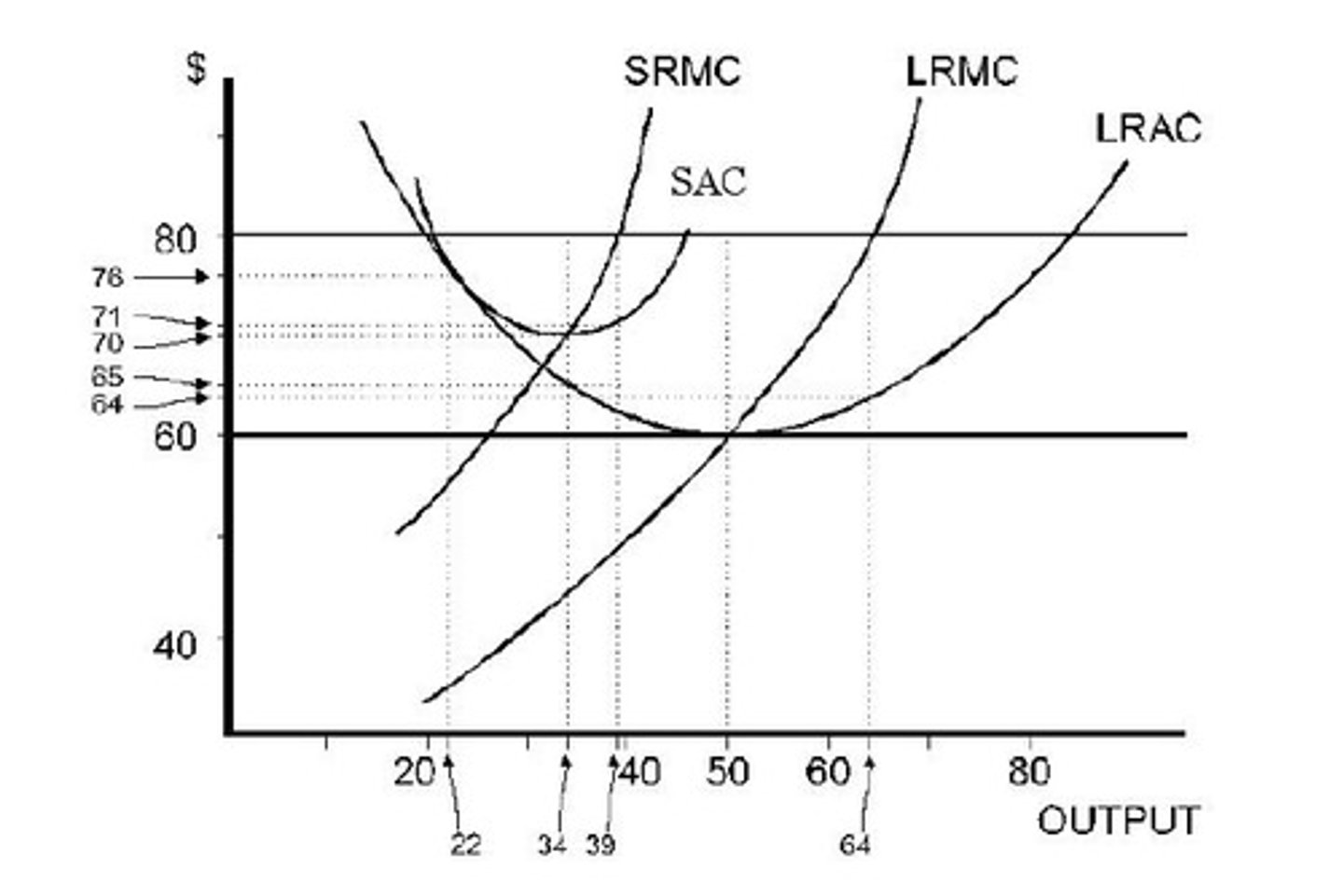

At P = $80, what is the profit maximizing output in the short run?

39.

At P = $80, how much is profit in the short run?

351.

Why does producer surplus exist in an unregulated competitive market?

Producers are willing to sell at less than equilibrium price.

Why does consumer surplus exist in an unregulated competitive market?

Consumers are willing to pay more than equilibrium price

What conditions must hold in the equilibrium of a competitive market with a specific tax on consumers?

The quantity sold and the price paid by the buyer must lie on the demand curve, the quantity sold and the sellers prices must lie on the supply curve, the quantity demanded must equal the quantity supplied, and the difference between the price the buyer pays and the price the seller receives must equal the specific tax.

If the government establishes a price floor of $50, how many widgets will be sold?

20.

If the government establishes a price floor of $40, how will consumer surplus change?

Fall by $350.

If the government establishes a price floor of $40 and purchases the surplus over quantity demanded, how will producer surplus change?

Rise by $500.