Investments

1/118

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

119 Terms

firm commitment agreement

best effort

syndicate offering

green shoe

investment banker purchases the entire securities issue from the issuer at a negotiated price and bears the risk of reselling the securities to the public.

underwriter agrees only to sell as much of the issue as possible, with any unsold securities returned to the issuer.

involves a group of brokerage firms working together to underwrite and sell a securities issue, not a single commitment to purchase.

an overallotment option that allows underwriters to sell additional shares if demand exceeds supply; it is a standby provision, not the primary underwriting commitment.

A client purchased 1,000 shares of stock at $23 per share using 50% initial margin. The maintenance margin requirement is 35%. At what stock price will a margin call be triggered?

The margin call trigger price is calculated as: Loan ÷ (1 − Maintenance Margin). The loan per share equals $23 × 0.50 = $11.50. Therefore: $11.50 ÷ (1 − 0.35) = $11.50 ÷ 0.65 = $17.69.

An investor purchases 200 shares at $100 per share using full initial margin of 50%. The maintenance margin is 25%. Share prices subsequently fall to $50 per share. What is the margin call amount?

The loan per share is $100 × 0.50 = $50. At the new price of $50, actual equity per share = $50 − $50 = $0. Required equity per share = $50 × 0.25 = $12.50. The investor must deposit $12.50 per share × 200 shares = $2,500 to meet the maintenance margin requirement

Who establishes initial margin requirements for security transactions

Fed

In securities law, what is a "red herring"?

preliminary prospectus issued by the managing underwriter prior to SEC approval

nominal rate is composed of

the risk-free rate plus recognized risk premiums that compensate investors for specific risks, including the default (credit) premium, the liquidity premium, and the maturity (term) premium

An investor is comparing four fixed-income options. Which bond carries the greatest reinvestment rate risk?

A.A U.S. Treasury bond with an 11.625% coupon, maturing in five years, priced at $1,225.39 with a yield to maturity of 6.3%.

B.A U.S. Treasury strip (zero-coupon bond), maturing in five years, priced at $735.12 with a yield to maturity of 6.25%.

C.A corporate B-rated bond with a 9.75% coupon, maturing in five years, priced at $1,038.18 with a yield to maturity of 8.79%.

D.A corporate zero-coupon bond, maturing in five years, priced at $750 with a yield to maturity of 5.9%.

Reinvestment rate risk is greatest for bonds with high coupon payments, because a larger proportion of total return depends on reinvesting those coupons. The Treasury bond in Choice A has the highest coupon (11.625%) and is trading at a significant premium, reflecting that current market rates (6.3% YTM) are far below the coupon rate. Investors must reinvest the large coupons at the much-lower prevailing rate.

A client owns two stocks in equal dollar amounts with the following characteristics:

Stock | Expected Return | Standard Deviation | Beta |

|---|---|---|---|

ABC | 9.5% | 13% | 0.93 |

XYZ | 12.0% | 18% | 1.12 |

The correlation of returns between the two stocks is -0.89. Which of the following statements is correct regarding the portfolio formed by combining these two stocks?

With a correlation of -0.89, the two stocks move largely in opposite directions. Portfolio theory demonstrates that combining negatively correlated assets reduces the portfolio standard deviation below that of either individual stock.

A portfolio is invested 60% in Stock A with a standard deviation of 17.5% and 40% in Stock B with a standard deviation of 16.75%. The correlation between the two securities is 0.29. What is the portfolio standard deviation?

First calculate the covariance: COV = 0.175 × 0.1675 × 0.29 = 0.00850. Then apply the two-asset formula: √[(.60)²(.175)² + (.40)²(.1675)² + 2(.60)(.40)(.00850)] = √[.011 + .0045 + .0041] = √.0196 = 14.0%.

The optimal portfolio in the Markowitz model occurs at the point of tangency between which two measures?

The indifference curve and the efficient frontier.

What is the standard deviation of a stock with the following annual returns?

Year | Return |

1 | 5.75% |

2 | 12.23% |

3 | 11.16% |

4 | -3.94% |

5 | 9.37% |

Enter the five returns (5.75, 12.23, 11.16, -3.94, 9.37) into your financial calculator using the statistics function and solve for the sample standard deviation (Sx). The result is approximately 6.55%

For which type of portfolio is standard deviation the most appropriate measure of risk

Standard deviation measures total risk, which includes both systematic (market) risk and unsystematic (company-specific) risk. For a portfolio that is not well diversified, unsystematic risk has not been eliminated, making standard deviation the appropriate total risk measure.

Mutual fund XYZ has a beta of 1.5, a standard deviation of 12%, and a correlation to the S&P 500 of 0.80. What percentage of the fund's return is explained by the S&P 500?

R-squared is calculated by squaring the correlation coefficient: R² = (0.80)² = 0.64, or 64%. R-squared measures the percentage of a portfolio's return that can be explained by movements in the benchmark (the S&P 500 in this case).

A security has a beta of 1.2, the overall market has returned 10.93%, and U.S. Treasury issues are currently yielding 3.56%. Using the Capital Asset Pricing Model (CAPM), what expected return should your client anticipate from this security?

Using CAPM: Expected Return = Rf + β(Rm − Rf) = 3.56% + 1.2 × (10.93% − 3.56%) = 3.56% + 1.2 × 7.37% = 3.56% + 8.84% = 12.40%.

Neal is willing to invest in above-average-risk securities only if he is rewarded for doing so. A stock he is considering dropped 8% when the S&P 500 dropped 6%. The current market risk premium is 7% and the Treasury bill rate is 6.5%. Beta for this stock is 1.3. Using the Capital Asset Pricing Model (CAPM), what is the required rate of return for this stock, and does it meet Neal's criteria?

The market return equals the risk-free rate plus the market risk premium: 6.5% + 7% = 13.5%. Using CAPM: r = 6.5% + 1.3 × 7% = 6.5% + 9.1% = 15.6%. Because 15.6% exceeds the market return of 13.5%, the stock compensates Neal for taking on above-average systematic risk, satisfying his criterion. The stock's price drop relative to the S&P 500 is context only and is not used in the CAPM formula.

When reviewing Morningstar reports for mutual fund selection, a CFP® Professional focuses on each fund’s alpha. Which of the following most accurately describes what alpha measures?

The difference between a fund’s actual return and its risk-adjusted expected return

Which portfolio evaluation method allows a comparison of a portfolio manager’s performance to the overall market using only one calculation?

The Jensen model

When computing portfolio performance, the Sharpe index uses __________ as its risk measure, while the Treynor index uses __________ as its risk measure.

Standard deviation; beta

The Performance Fund returned 19% over the evaluation period with a standard deviation of 23%. The risk-free rate was 8% during the same period. What is the Sharpe index of performance for the Fund?

Sharpe index = (Portfolio Return − Risk-Free Rate) ÷ Standard Deviation = (0.19 − 0.08) ÷ 0.23 = 0.11 ÷ 0.23 = 0.4783.

An investor in the 32% marginal tax bracket purchased a bond for $980, received $75 in interest, and sold the bond for $950 after a seven-month holding period. The long-term capital gains rate is 15%. What are the investor's pre-tax and after-tax holding period returns, respectively?

Pre-tax HPR = ($950 − $980 + $75) ÷ $980 = $45 ÷ $980 = 4.59% ≈ 4.6%. Because the holding period is less than 12 months, the loss and interest are both short-term. After-tax HPR = [($950 − $980) × (1 − 0.32) + ($75 × (1 − 0.32))] ÷ $980 = [<20.40> + 51.00] ÷ $980 = 30.60 ÷ $980 ≈ 3.1%.

Michael's investment had the following annual returns: Year 1: 12%, Year 2: -5%, Year 3: 8%, Year 4: 18%. What are the arithmetic mean (AM) and geometric mean (GM) of these returns?

AM = (0.12 + (-0.05) + 0.08 + 0.18) / 4 = 0.33 / 4 = 8.25%. For the geometric mean: GM = [(1.12)(0.95)(1.08)(1.18)]⁽⁄⁴ - 1 = (1.3562)⁽⁄⁴ - 1 = 7.91%.

Of the following market indexes, which is the only one that uses the geometric average to compute its daily value?

Value Line Average

A portfolio contains four stocks with the following characteristics:

Stock L: beta = 1.45, value = $60,000 Stock M: beta = 0.93, value = $125,000

Stock N: beta = 0.65, value = $240,000 Stock O: beta = 2.20, value = $175,000

What is the weighted average beta of this portfolio?

Total portfolio value = $60,000 + $125,000 + $240,000 + $175,000 = $600,000. Stock L: ($60,000 ÷ $600,000) × 1.45 = 0.1450. Stock M: ($125,000 ÷ $600,000) × 0.93 = 0.1938. Stock N: ($240,000 ÷ $600,000) × 0.65 = 0.2600. Stock O: ($175,000 ÷ $600,000) × 2.20 = 0.6417. Weighted beta = 0.1450 + 0.1938 + 0.2600 + 0.6417 = 1.24

Bill holds three stocks with the following market values and betas:

ACE: market value = $5,000, beta = 1.10 BDF: market value = $8,000, beta = 0.70 GIK: market value = $10,000, beta = 1.50

What is the weighted beta coefficient for Bill’s portfolio?

Total portfolio value = $5,000 + $8,000 + $10,000 = $23,000. ACE: ($5,000 ÷ $23,000) × 1.10 = 0.2391. BDF: ($8,000 ÷ $23,000) × 0.70 = 0.2435. GIK: ($10,000 ÷ $23,000) × 1.50 = 0.6522. Weighted beta = 0.2391 + 0.2435 + 0.6522 = 1.13

Which combination of information is the minimum needed to calculate the weighted average rate of return for a portfolio?

Current market price of each security, number of shares held, and percent return of each security

A portfolio contains three stocks with the following data:

Stock | Beta | Expected Return | Amount Invested |

|---|---|---|---|

A | 1.4 | 15% | $10,000 |

B | 1.2 | 12% | $15,000 |

C | 0.9 | 9% | $11,000 |

What is the weighted average expected return of this portfolio (rounded to the nearest full percent)?

Total portfolio value = $10,000 + $15,000 + $11,000 = $36,000. Stock A: ($10,000 ÷ $36,000) × 0.15 = 0.0417. Stock B: ($15,000 ÷ $36,000) × 0.12 = 0.0500. Stock C: ($11,000 ÷ $36,000) × 0.09 = 0.0275. Weighted average = 0.0417 + 0.0500 + 0.0275 = 0.1192, or approximately 12%.

When comparing the performance of two investment managers, which return measurement approach is generally used?

Time-weighted return

An investor buys one share of stock for $55. At the end of year one, the stock pays a $2 dividend and the investor purchases a second share for $58. At the end of year two, each share is worth $65 and another $2 dividend per share is paid, at which point the investor sells both shares. What is the time-weighted rate of return on this investment?

Time-weighted return focuses on the security's own cash flows and excludes the effect of additional investor contributions. Using the single-share cash flows: CF0 = −$55; CF1 = $2; CF2 = $67 ($65 price + $2 dividend). Solving for IRR yields 12.20%. The second share purchase at $58 is excluded because time-weighted return measures the security's performance, not the investor's additional capital decisions.

An investor has a 20% required rate of return. A stock pays an annual dividend of $0.64 and is projected to grow dividends by 17% annually. The current market price is $36.50. Using the constant growth dividend model, what is the intrinsic value of this stock per share?

D&sub1; = $0.64 × 1.17 = $0.7488. Intrinsic Value = D&sub1; / (r − g) = $0.7488 / (0.20 − 0.17) = $0.7488 / 0.03 = $24.96.

Question

A company's current annual dividend is $2.00 per share. Five years ago, the dividend was $1.36 per share. The firm expects dividends to grow at the same compound annual rate as the past five years. The required rate of return on the stock is 12%. Using the constant dividend growth model, what is the value of one share of common stock? (Round to the nearest dollar.)

Step 1: Solve for the historical growth rate using a financial calculator: N = 5, PV = <1.36>, FV = 2.00, PMT = 0; solve for I = 8%. Step 2: D&sub1; = $2.00 × 1.08 = $2.16. Step 3: V = D&sub1; / (r − g) = $2.16 / (0.12 − 0.08) = $2.16 / 0.04 = $54.

A stock pays a current dividend of $2.00 and is expected to grow at 6%. The stock has a beta of 1.5, the risk-free rate is 3%, and the market return is 12%. Using the constant growth dividend valuation model, what is the intrinsic value of this stock?

First, use the Capital Asset Pricing Model (CAPM) to find the required return: R = 3% + 1.5(12% − 3%) = 3% + 13.5% = 16.5%. Then apply the constant growth dividend model: V = D&sub1; / (r − g) = $2.00 × 1.06 / (0.165 − 0.06) = $2.12 / 0.105 = $20.19.

To determine whether a stock is overvalued or undervalued relative to its fair price, a financial planner would use which formula

Intrinsic Value

Question

Camping the US, Inc. will pay dividends of $1, $0, and $2 at the end of each of the next three years, respectively. After Year 3, dividends are expected to grow at a constant rate of 3% per year. Using a required rate of return of 7%, what is the intrinsic value per share of Camping the US, Inc. using the dividend growth model?

Step 1: Calculate terminal value at end of Year 3 using D4 as the next dividend: V3 = $2.00 × 1.03 ÷ (0.07 − 0.03) = $2.06 ÷ 0.04 = $51.50. Step 2: CF0 = 0; CF1 = $1; CF2 = $0; CF3 = $2 + $51.50 = $53.50; I = 7%; NPV = $44.61.

XYZ Company anticipates paying the following dividends starting next year: Year 1: $2.25; Year 2: $2.75; Year 3: $3.01. After Year 3, dividends are expected to grow at a constant rate of 6% per year. If an investor requires a 12% rate of return, what is the maximum price the investor should pay for this stock today?

Step 1: Calculate terminal value at end of Year 3 using the constant growth model: V3 = $3.01 × 1.06 ÷ (0.12 − 0.06) = $3.1906 ÷ 0.06 = $53.18. Step 2: Discount all cash flows at 12% using the cash flow function: CF0 = 0; CF1 = $2.25; CF2 = $2.75; CF3 = $3.01 + $53.18 = $56.19; I = 12%; NPV = $44.20.

Question

Which of the following accurately describes American Depositary Receipts (ADRs)?

They allow U.S. investors to purchase foreign company stock denominated in U.S. dollars.

Bristol-Buyers Company trades at $36.00 per share with current earnings of $3.00 per share. Earnings for next year are projected to increase by 25%, and the retention ratio is projected to remain at 60%. Using the price-to-earnings (P/E) multiplier, to what level might the market price move in one year, assuming the P/E ratio remains constant?

Current P/E = $36.00 ÷ $3.00 = 12. Projected earnings = $3.00 × 1.25 = $3.75. Projected price = $3.75 × 12 = $45.00.

According to fundamental analysis, which of the following best defines the intrinsic value of a share of common stock?

According to fundamental analysis, which of the following best defines the intrinsic value of a share of common stock?

An analyst researches and selects individual companies based on their outstanding investment potential before considering industry and macroeconomic factors. This analyst is practicing:

Bottom-up analysts begin their research at the company level, seeking overlooked or undervalued individual securities based on company-specific fundamentals

The dividend payout ratio is best described as which of the following?

The percentage of net income distributed to shareholders as dividends, calculated as dividends per share divided by earnings per share

A client asks why callable bonds are generally considered less attractive to investors than otherwise identical non-callable bonds. Which answer correctly identifies the primary risks callable bonds create from the investor's perspective?

Callable bonds expose investors to two primary disadvantages. First, reinvestment risk arises because issuers are most likely to call bonds when interest rates have fallen, forcing investors to reinvest their returned principal at the lower prevailing rates — precisely the worst time to do so. Second, price risk (negative convexity) limits price appreciation: as rates decline, the call feature acts as a ceiling on the bond's market price near the call price, preventing investors from fully benefiting from the rate drop.

Which of the following statements about U.S. Treasury bills (T-bills) is correct?

T-bills are issued at a discount and redeemed at face value at maturity

Commercial paper.

Short-term debt securities issued by corporations with maturities generally under 270 days, which allows issuers to avoid Securities and Exchange Commission (SEC) registration requirements, are known

A client will only invest in securities backed by the full faith, credit, and taxing power of the U.S. government. Which of the following securities meets this requirement?

Which of the following statements accurately describes a characteristic of Government National Mortgage Association (GNMA) securities?

Government National Mortgage Association (GNMA) certificates.

If mortgage rates decrease, prepayments on the underlying mortgages may increase.

Question

Which of the following organizations provides insurance against municipal bond defaults?

Municipal Bond Insurance Association (MBIA)

Which pair of investment characteristics best describes a high-quality, long-term municipal bond?

High inflation risk; low default risk

David has $20,000 earmarked for a down payment on a house in two years. David is in the 32% marginal tax bracket. Which investment is most appropriate for this goal?

The taxable equivalent yield (TEY) of the 4% tax-free money market fund = 4% ÷ (1 − 0.32) = 5.88%. This exceeds the 5.4% taxable corporate bond, making the tax-free fund more advantageous on an after-tax basis. TEY = Tax-Exempt Rate ÷ (1 − Marginal Tax Rate).

Jan is interested in purchasing a municipal bond that pays $35 in interest on a semiannual basis. The bond is selling at par of $1,000 and Jan is in the 35% marginal tax bracket. What pre-tax yield must a comparable taxable corporate bond offer to equal the after-tax return of this municipal bond?

First, calculate the municipal bond's annual coupon rate: $35 × 2 = $70 annual interest; $70 ÷ $1,000 par = 7.0% tax-exempt yield. Then apply the TEY formula: TEY = Tax-Exempt Rate ÷ (1 − Marginal Tax Rate) = 7.0% ÷ (1 − 0.35) = 7.0% ÷ 0.65 = 10.77%

A CFP® Professional is comparing four option-free bonds for a client concerned about interest rate risk. The bonds have identical credit quality but differ in their other characteristics. Which bond will exhibit the highest convexity?

A.5-year bond with a 7% coupon trading at a 6% yield

B.A 10-year bond with a 5% coupon trading at a 4% yield

C.A 20-year bond with a 3% coupon trading at a 4% yield

D.A 30-year bond with a 2% coupon trading at a 3% yield

Convexity increases with longer maturity, lower coupon rates, and lower yields. The 30-year bond combines the longest maturity, lowest coupon, and lowest yield, making it the most convex of the four option-free bonds.

To calculate the Yield to Maturity (YTM) of a bond, which of the following is an essential input?

The present value, par value, and time to maturity of the bond

Barbara owns an LMN, Inc. AA-rated bond with a par value of $1,000 that matures in 7 years. She receives $55 of interest income semiannually. Comparable AA-rated, 7-year bonds currently yield 12%. What is the intrinsic value of Barbara's bond?

The intrinsic value is the present value of all future cash flows: N = 7 × 2 = 14 periods; i = 12% ÷ 2 = 6% per period; PMT = $55; FV = $1,000; solve for PV = $953.53

A CFP® Professional is explaining to a client why duration alone may understate the price change of a long-term bond when interest rates move significantly. Which statement best describes the role of convexity in the price-yield relationship of an option-free bond?

Convexity causes prices to rise more than duration predicts when yields fall and fall less than duration predicts when yields rise

The bond investment strategy of "riding the yield curve" involves which of the following?

Riding the yield curve involves purchasing debt instruments in anticipation of changes in both short- and long-term interest rates, repositioning the portfolio as rates change to capture price appreciation

Using the following information, what is the duration of the bond? Maturity: 11 years; Par value: $1,000; Coupon rate: 8.25%; Current market price: $1,094; Interest paid annually.

Step 1 – Calculate YTM: N = 11; PV = −1,094; PMT = 82.50; FV = 1,000; Solve for i ≈ 7%. Step 2 – Apply the Macaulay Duration formula using an annual coupon rate of 8.25% and YTM of 7% over 11 years, which yields a duration of approximately 7.8 years. Using annual rather than semiannual periods does not materially change the result.

To immunize a bond portfolio over a specific investment horizon, an investor should:

Match the average weighted duration of the bond portfolio to the investment horizon.

Which measure best evaluates a bond's sensitivity to interest rate risk?

Duration, because it accounts for both interest rate changes and reinvestment rate risk.

Which of the following bond characteristics directly influence its duration

Current price, time to maturity, yield to maturity, and coupon rate.

Immunization

matches a portfolio's duration to the investment horizon

A $1,000 par bond originally issued at par has a 8% coupon (semi-annual), 10 years to maturity, callable in 5 years at $1,050, and a current market price of $1,147.20. Which set of calculations and conclusions is correct?

A.YTM ≈ 6.0%, YTC ≈ 5.5%, and the bond is selling at a premium because market rates have fallen since issuance.

B.YTM ≈ 6.0% and YTC ≈ 5.5%, but the bond is selling at a discount.

C.YTM ≈ 5.5% and YTC ≈ 6.0%, and the bond is selling at a premium.

D.YTM > YTC, meaning the bond is more likely to be called than held to maturity.

YTM: N = 20, PV = <1,147.20>, PMT = 40, FV = 1,000; I = 3.01% per period × 2 = 6.02% ≈ 6.0%. YTC: N = 10, PV = <1,147.20>, PMT = 40, FV = 1,050; I = 2.74% per period × 2 = 5.48% ≈ 5.5%. The bond is priced above par ($1,147.20 > $1,000), indicating market rates have fallen since issuance, as investors are willing to pay a premium for the above-market 8% coupon.

A convertible bond has an 8% coupon rate, pays interest semiannually, has a par value of $1,000, matures in 20 years, and converts into 100 shares of common stock. Current market rates on similar bonds are 12%. The current stock price is $8.50 per share. What price should a client expect to pay for this bond?

A convertible bond will trade at the higher of its debt value or its conversion value. Debt value: N = 40, i = 6, PMT = 40, FV = 1,000; PV = $699.07. Conversion value = 100 shares × $8.50 = $850. Since the conversion value ($850) exceeds the debt value ($699.07), the bond will trade at its conversion value of $850.

A client owns a convertible bond with a par value of $1,000 that is convertible into 22 shares of common stock. The current market price of the underlying stock is $52. What is the conversion value of this bond?

Conversion value = Conversion ratio × Stock price = 22 × $52 = $1,144. The conversion ratio is the number of shares received upon conversion, which is given directly as 22 shares. The conversion price (PAR ÷ conversion ratio = $1,000 ÷ 22 = $45.45) is used to derive the ratio when not given, but here the ratio is provided.

A convertible bond has a maturity value of $1,000 and an exercise (conversion) price of $10 per share. How many shares of stock will the bondholder receive upon conversion?

The conversion ratio equals par value divided by the conversion price: $1,000 ÷ $10 = 100 shares. This is the number of common shares the bondholder receives if they choose to convert the bond.

Which of the following is an accurate characteristic of a municipal bond unit investment trust (UIT)?

The portfolio is self-liquidating as the underlying bonds mature or are called

Which of the following statements accurately describes a unit investment trust (UIT)?

UITs typically hold a fixed portfolio of bonds or securities until maturity and are self-liquidating

coefficient of determination by r^2

If r^2 is >= .7. We use BETA

If r^2 is < .7. We use SD

At What Price Does an Investor Receive a Margin Call Price?

Loan/(1-maintenance margin)

Research Reports

Value Line

• Ranks stocks on a scale of 1 to 5 for timeliness and safety.

• 1 is highest rank

• Morningstar

• Ranks mutual funds, stocks, bonds and Exchange Traded Funds (ETFs) using 1 to 5 stars.

• 1 star represents the lowest performing, 5 stars represents the highest performing.

qualified dividend

Paid by an American company or qualifying foreign company

• Not listed as a dividend that doesn't qualify by IRS

• Held the stock for more than 60 days during the 121 day period that begins 60 days

before the ex-dividend date

If Tuesday, June 4 is the date of record, when must Joe purchase the stock in order to receive the

dividend

june 3

IPS Statement

clients objectives, limitations on investment manager

standard deviation

• Measures the total risk of an undiversified portfolio.

• Measures how much something “flip flops” around an average.

• The bigger the standard deviation, the more risky.

SD area under the curve

• 68% of the time +/- 1 Standard Deviation

• 95% of the time +/- 2 Standard Deviations

• 99% of the time +/- 3 Standard Deviations

Coefficient of Variation

Useful when comparing two assets with different average returns

Exam Tip: The asset with lower CV (risk/return) has the higher Risk Adjusted Return

(return/risk)

Covariance

The covariance is the measure of two securities combined and their interactive risk.

Correlation/Correlation Coefficient

Correlation and the covariance measure movement of one security relative to that of another

Correlation ranges from +1 to -1 and provides the investor with insight as to the strength and

direction two assets move relative to each other.

• A correlation of +1 denotes that two assets are perfectly positively correlated.

• A correlation of 0 denotes that assets are completely uncorrelated.

• A correlation of -1 denotes a perfectly negative correlation.

beta

Beta is a measure of systematic risk or market risk, whereas standard deviation is a measure of

total risk.

• Beta is an appropriate measure of risk for a well diversified portfolio.

Coefficient of Determination

Coefficient of Determination or R-Squared

Systematic risk

P - purchasing power

R - reinvestment rate risk

I - Interest rate risk

M - market risk

E - exchange rate risk

Cannot diversify away

Modern Portfolio Theory (1 of 2) - Harry markowitz

Modern Portfolio Theory is the acceptance by an investor of a given level of risk while

maximizing their expected return objectives.

• The Efficient Frontier is the curve which illustrates the best possible returns that could be

expected from all possible portfolios.

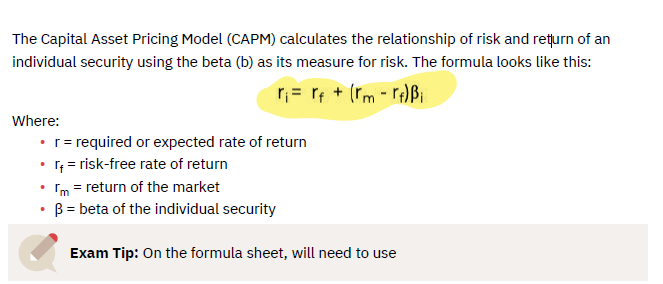

Capital Asset Pricing Model

Portfolio Performance Measures: Jensen’s Alpha

Treynor and Sharpe are calculations for providing a measure and ranking of

relativeperformance, Jensen’s model attempts to construct a measure of absolute

performance on arisk-adjusted basis.

• Jensen tells you something all by itself:

• + alpha = good =

The alpha is indicative of the level of a manager’s performance.

• The higher the alpha, the better the performance.

Holding period return

selling price-purchase price +-cahs flow / (Initial equity)

Weighted Average Portfolio Return

1. The current market value of the securities held (CMV)

2. The total portfolio value (TPV)

3. The return of each security throughout the period in question

NPV

NPV is deterministic.

• A positive NPV: the investor would make the investment.

• A negative NPV: the investor would not make the investment.

• NPV = PV of Cash Flows – Initial Cost

Exam Tip: If NPV = 0, then “yes” make the investment

Internal Rate of Return

the discount rate that sets the NPV formula equal to zero.

PE Ratio

(Earnings Per Share) x (P/E multiplier) = Expected Price Per Share

Dividend payout ratio

Common stock dividend/earning per share

ROE

Dividend Yield

EPS/Stockholders equity per share

(Dividend Per Share/Stock Price)

Dividend Discount Model

The dividend discount model values a company’s stock by discounting the future stream of cash

flows.

Dividend Discount Model - Important Exam Tips:

• If the required rate of return decreases, the stock price will increase

• If the dividend is expected to increase, the stock price will increase

• If the required rate of return increases, the stock price will decrease

• If the dividend is expected to decrease, the stock price will decrease

Efficient Market Hypothesis - picture on phone to explain it better

Weak: Historical information will not help investors achieve above average market returns.

Essentially rejects technical analysis

• Semi-Strong: Historical and public information will not help investors achieve above average

market returns. Rejects technical and fundamental analysis

• Strong: Historical, public and private information will not help investors achieve above average

market returns. Rejects technical & fundamental analysis, and also inside information. So,

diversify stocks randomly or merely go with an Index

Series E Bonds and Series EE Bond

Sold at face value

• Non marketable, nontransferable

• Do not pay interest periodically

Series H Bonds and Series HH Bonds

They pay interest semiannually – different than EE bonds

Series I Bonds

Inflation protection via fixed rate + variable rate (see TIPS on next slide)

Tax equivalent yield

r/(1 – t)

Where:

r = tax exempt yield

t = marginal tax rate

TIPS

Principal adjusts for inflation, apply coupon rate to new principal amount.

• Provides inflation and purchasing power protection

• Coupon rate does not change as is the case with I Bonds - important

STRIPS

Separate trading of coupon payments and principal amount

• Essentially creates many zero coupon bonds

Federal Agency Securities NOT BACKED BY FEDERAL GOV

• Federal National Mortgage Association (FNMA - Fannie Mae)

• Federal Home Loan Mortgage Corporation (FHLMC - Freddie

Mac)

• Student Loan Marketing Association (SLMA - Sallie Mae)

• Federal Farm Credit Banks (FFCB)

• Federal Intermediate Credit Banks (FICB)

Federal Home Loan Bank

Secured Bonds

Mortgage Bonds

• Backed by a pool of mortgages

• Payment consists of both principal and interest

• Biggest risks: Default and Prepayment Risk

• Collateral Trust Bonds

• Backed by an asset that the company owns