Lecture 3: Capital Markets & Risk Pricing: risk premium, expected return, variance, standard deviation, volatility, annual return, standard error, Beta

1/18

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

19 Terms

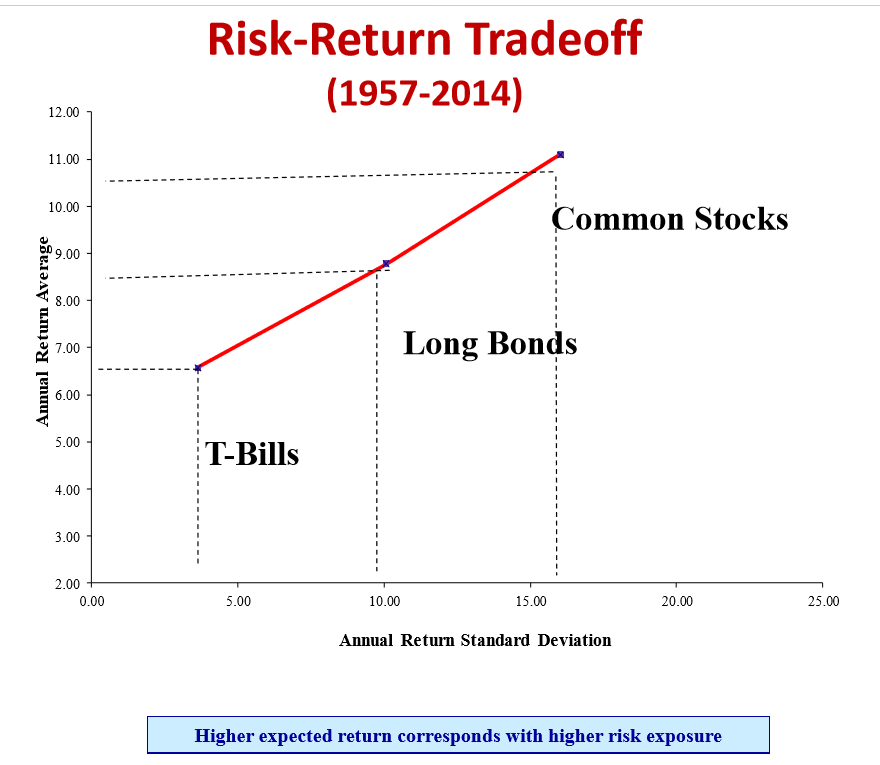

What is the risk-return tradeoff?

In order to gain higher returns, you have to have more risk

What is a risk premium & the required rate of return on risky investments?

The extra return as compensation for more risk

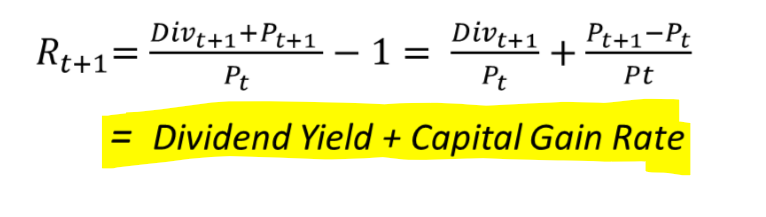

r = risk-free rate + risk premium

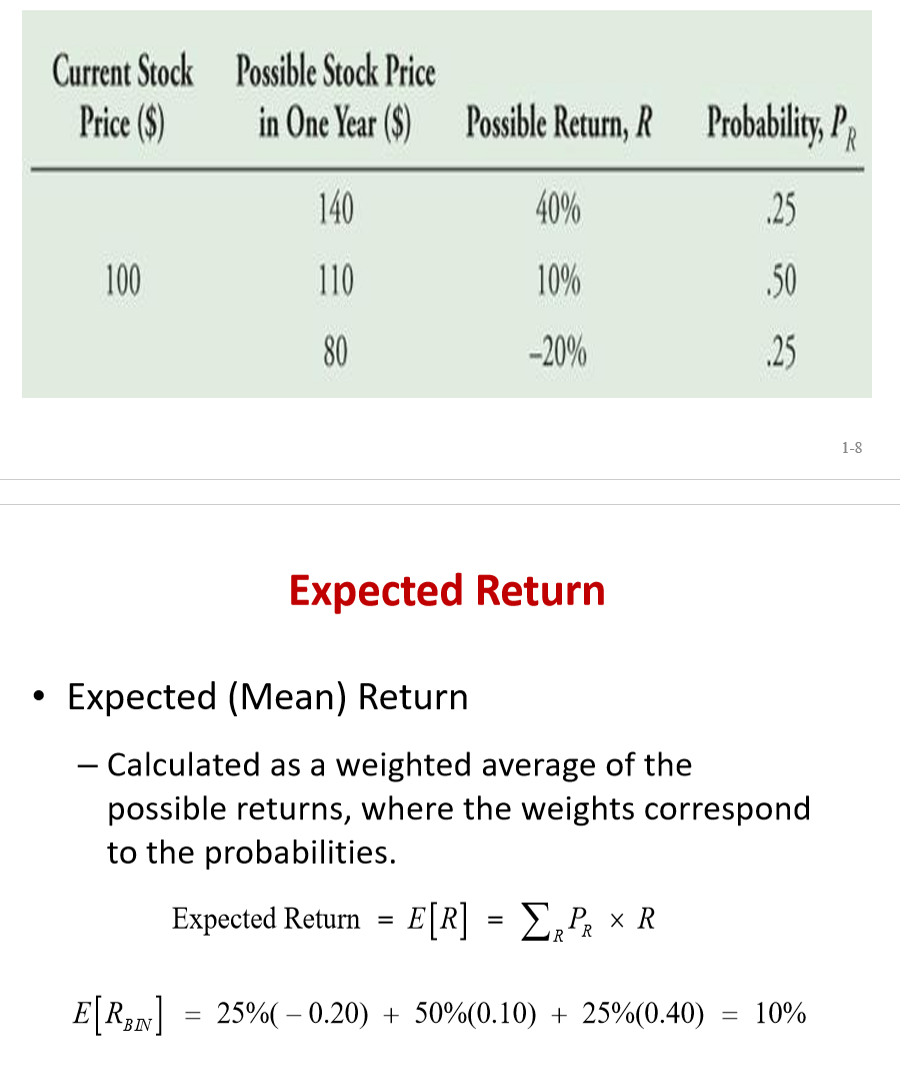

What is expected return & its formula?

The mean return → weighted average of the possible returns

weights correspond to the probabilities

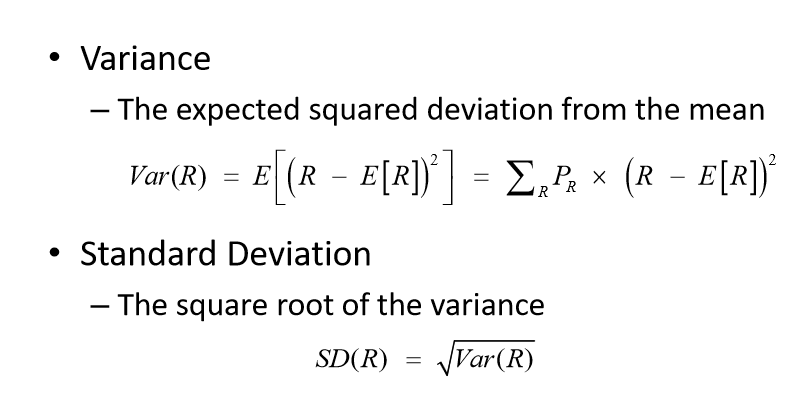

What is variance and standard deviation?

Both measures risk of a probability distribution

Variance - expected squared deviation from the mean

Standard deviation - square root of variance

What is volatility?

Measure of total risk → systematic + diversifiable risk

another term for standard deviation (square root of variance)

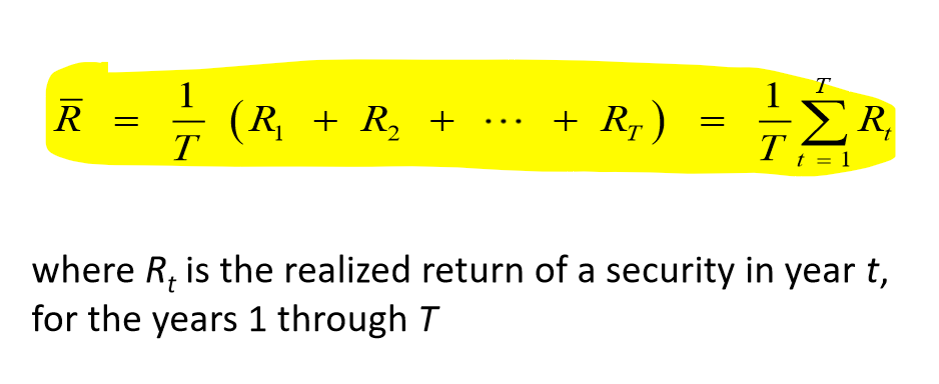

What are historical returns of stocks & bonds (realized annual returns)?

Realized return → actually occurs over a particular time period

What is the average annual return formula?

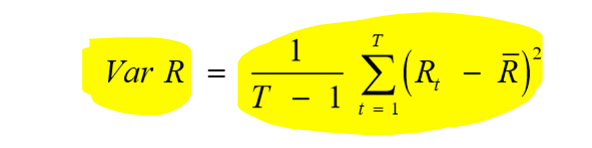

What is the variance and volatility of returns?

The variance estimate using realized returns

the standard deviation is the square root of the variance

What are 2 issues with using past returns to predict the future (estimation error)?

2 Issues:

Don’t know what investors expected in the past, only know the realized actual returns

Average return is just an estimate of the true expected return

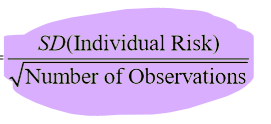

How can we measure the estimation error (standard error)?

Standard error: A statistical measure of the degree of the estimation error

the estimate of the expected return

How does risk and return differ for large portfolios and individual stocks?

Large: more risk, more return

Individual: more risk, less return

Why is total risk (volatility) a bad measure of risk?

Because volatility measures = systematic/market risk + firm-specific risk

but firm-specific risk can be diversified and averaged out → and is eliminated!

systematic risk can’t be diversified → need a new measure

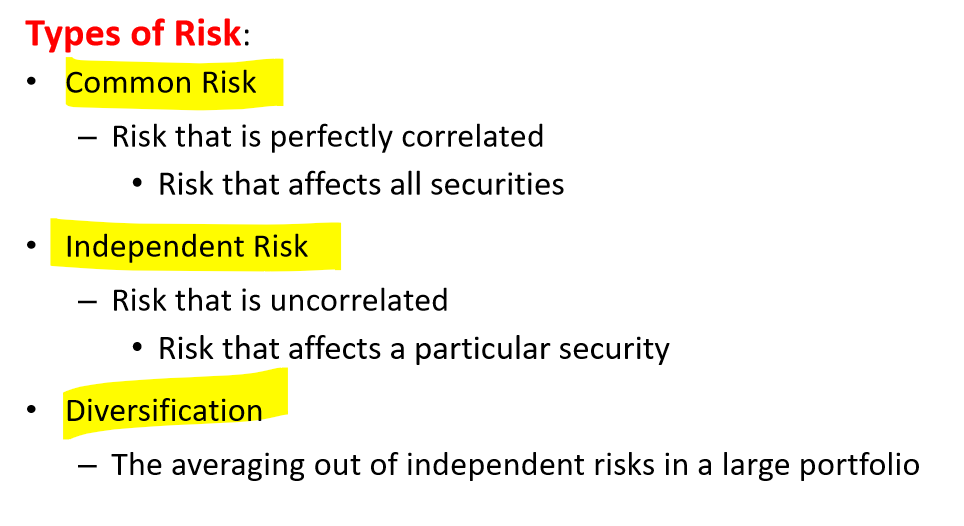

What is common & independent risk and diversification?

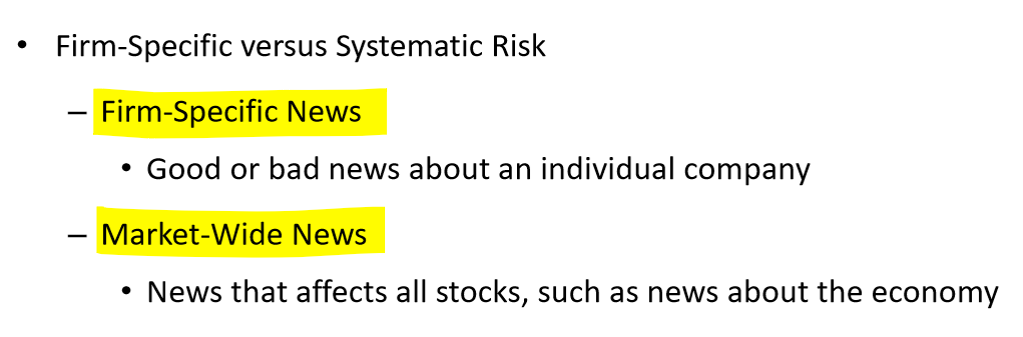

What is firm specific and market-wide news?

Firm-specific vs. systematic

What is the risk premium for market and firm-specific risks?

Market → reward for bearing market risk, can’t be diversified out

Firm-specific → can eliminate through diversification (no risk premium from holding firm-specific risky stocks, no reward because it can easily eliminate for free)

How do you measure systematic risk?

Beta → measures ONLY systematic risk

Measure investment’s systematic risk

determine risk premium require to compensate for that amount of systematic risk

(volatility measures systematic risk + firm-specific risk)

What is an efficient and market portfolio?

Efficient → only systematic risk (no firm-specific), can’t reduce volatility (total risk, standard deivation) without reducing expected return

Market → efficient portfolio has all shares & securities in market

What is Beta?

How sensitive its underlying revenues & cash flows are to general economic conditions

How we move with the market

Measures only systematic risk

→ 1% change in return of market, leads to a x change in s firm’s return on average

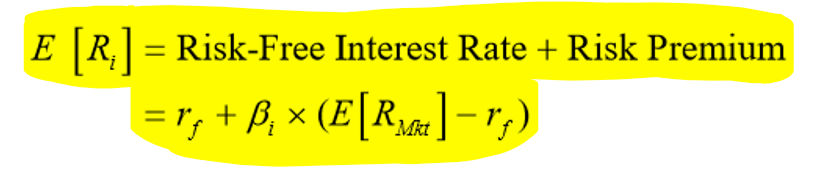

How do you find the cost of capital?

Capital Asset Pricing Model → used to find the return of any security

risk free interest rate + B x market risk premium