Financial Accounting Chapter 1 John Wild

1/55

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

56 Terms

Accounting

is an information and measurement system that identifies, records, and communicates information about and organization's business activities

record keeping/ bookkeeping

the recording of transactions and events

accounting is called the ?

the language of business because it communicates data that help people make better decisions

External Users

do not directly run the organization and have limited access to its accounting information

Financial accounting

The field of accounting that focuses on providing information for external decision makers.

general-purpose financial statements

refers to the broad range of purposes for which external users rely on these statements

Examples of external users

Lenders(creditors), shareholders, board of directors, external (independent auditors), non-executive employees and labor unions, regulators, voters, legislators, government officials, contributors, suppliers, and customers

internal users

directly manage and operate the organization

Managerial Accounting

serves the decision making needs of internal users

Examples of Internal users

Research and development managers

Purchasing managers

Human resource managers

Production managers

Distribution managers

Marketing managers

Service managers

Ethics

are beliefs that separate right from wrong. They are accepted standards of good and bad behavior. identifying the ethical path is a course of action that avoids casting doubt on one's decisions.

Fraud Triangle

opportunity- a person must be able to commit fraud with a low risk of getting caught , pressure- a person must feel pressure or have incentive to commit fraud, rationalization- a person justifies fraud or does not see its criminal nature.

Internal Control

are procedures to protect assets, ensure reliable accounting, promote efficiency, and uphold company policies, physical controls(locks), and independent reviews.

Sarbanes-Oxley Act

GAAP (generally accepted accounting practices)

The standard guidelines used in financial accounting. Aims to make information relevant, reliable, and comparable.

SEC

U.S. government agency that has the legal authority to set GAAP. The SEC oversees proper use of GAAP by companies that raise money from the public through the issuance of stock and debt. The SEC has largely given the task of setting U.S GAAP to the Financial Accounting Standards Board.

FASB (Financial Accounting Standards Board)

sets accounting standards in the U.S.

IASB (International Accounting Standards Board)

Group that identifies preferred accounting practices & encourages global acceptance; issues IFRS

conceptual framework

A written framework to guide the development, preparation, and interpretation of financial accounting information. Consists of objectives, qualitative characteristics, elements, and recognition and measurement.

Objective of Conceptual Framework

... to provide info about the entity that is useful to investors or lenders/creditors

Qualitative Characteristics of conceptual framework

To require information that has Relevance and Faithful representation

elements of conceptual framework

to define elements in financial statement

Recognition and Measurement

to set criteria for an item to be recognized as an element; and how to measure it.

What are the four Accounting principles?

-Measurement principle (cost principle)

-Revenue recognition principle

-Expense recognition principle (matching principle)

- Full disclosure principle

Measurement Principle (Cost Principle)

Accounting information is based on actual cost. Cost is measured on a cash or equal-to-cash basis. cash value of what was giving up or received.

Revenue Recognition Principle

revenue is recognized when goods or services are provided to customers and at the amount expected to be received from the customer

Expense recognition principle (matching principle)

A company records the expenses it incurred to generate the revenue reported.

Full Disclosure Principle

A company reports the details behind financial statements that would impact users' decisions. Those disclosures are often in footnotes to the statements.

Recognize

Means to record

Revenue

is the amount received from selling products or services.

What are the four accounting assumptions?

going concern, monetary unit, time period, business entity

Going Concern Assumption

Accounting information presumes that the business will continue operating instead of being closed or sold. This means, for example, that property is reported at cost instead of liquidation value.

Monetary Unit Assumption

Transactions and events are expressed in monetary, or money, units. Examples of monetary units are the U.S. dollar and the Mexican peso

Time Period Assumption

The life of a company can be divided into time periods, such as months and years, and useful reports can be prepared for those periods.

Business Entity Assumption

A business is accounted for separately from other business entities and its owner.

Cost Benefit Constraint

Says that information disclosed by and entity must have benefits to the user that are greater than the costs of providing it

Materiality

Ability of information to influence decisions.

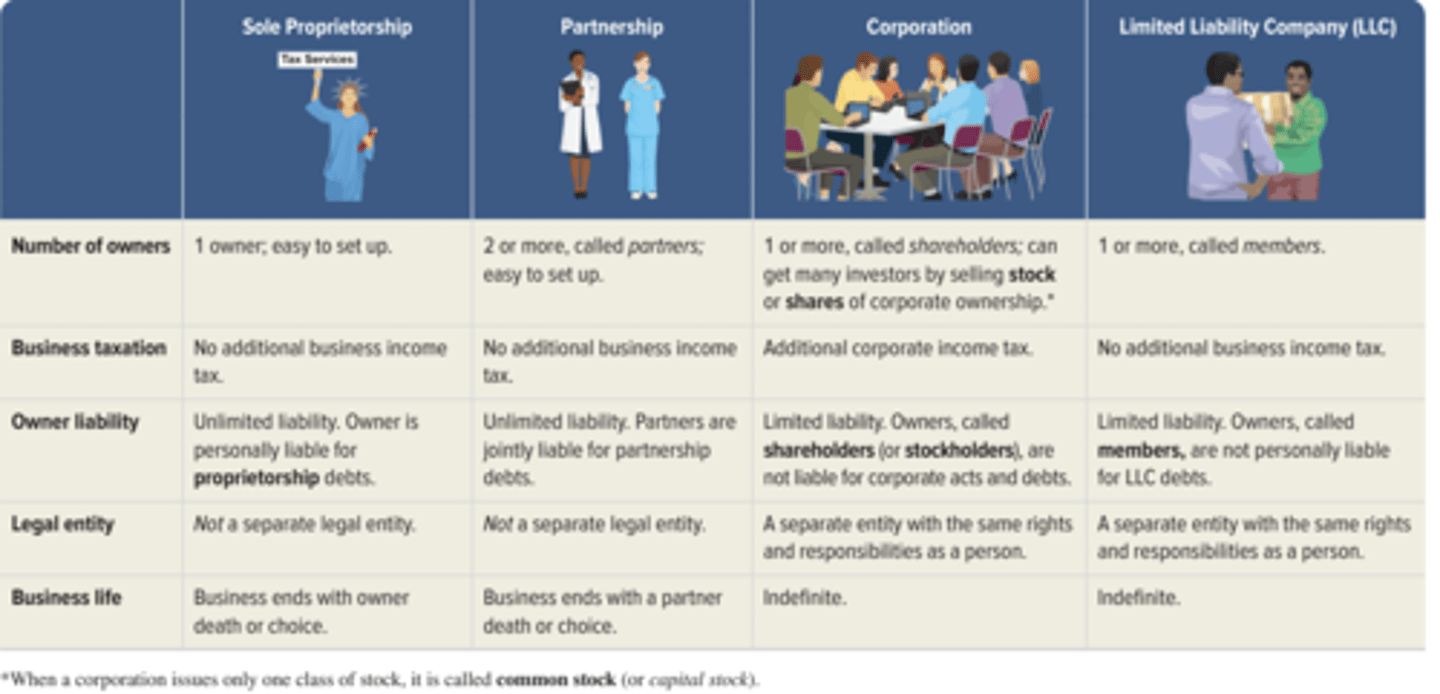

Describe the four Common Business Entities.

What is the order in which Financial Statements are prepared?

Income statement, Statement of retained earnings, Balance sheet, Statement of cash flows

Income statement

Describes a company's revenues and expenses and computes net income or loss over a period of time. Revenues-Expenses=Net Income

Statement of Retained Earnings

explains changes in retained earnings from net incomes (or loss) and any dividends over a period of time. Beg retained earnings + Net income- Dividends=End Retained Earnings

Balance Sheet

Describes a company's financial position (Types and amounts of assets, liabilities, and equity) at a point in time. Assets=Liabilities + Equity

Statement of cash flows

Identifies cash inflows (receipts) and cash outflows (payments over a period of time. Operating activities-

investing activities-involve buying and selling assets such as land and equipment that held for long term use( typically more than one year)

Financing activities-include long-term borrowing and repaying of cash from lenders and the cash investments from, and dividends to, shareholders.

Net Income

Occurs when revenues exceed expenses

Net Loss

Occurs when expenses exceeds revenues

Shareholder's investments and dividends

are not part of income

Four areas on financial statement analysis

liquidity and efficiency, solvency, profitability, market prospects

Return on Assets / Return on Invetment

Profitability measure that helps evaluate if management is effectively using assets to generate net income.

Net income/Average Total assets

Asset

Resources a company owns or controls that are expected to yield future benefits

Liabilities

Creditors' claims on assets. These are obligations to provide

assets, products, or services to others.

Equity

Shareholders' claim on assets. It consists of:

+ Common Stock- reflects inflows of cash and other net assets from shareholders in exchange for stock.

-Dividends-are outflows of cash and other assets to shareholders that reduce equity

+Revenues- increase equity(via net income) from sales of products and services to customers; examples are sales of products, consulting services provided, facilities rented to others, and commissions from services.

-Expenses decrease equity(via net income) from cost of providing products and services to customers; example are cost of employee time, use of supplies, advertising, utilities, and insurance fees.

Receivable

is an asset that promises a future inflow of

resources.

payable

is a liability that promises a future outflow

of resources

External Transactions

are exchanges of value between two entities, which cause changes in the accounting equation.

Internal transactions

are exchanges within an entity, which may or may not affect the accounting equation

Events

happenings that affect the accounting equation and are reliably measured. They include business events such as changes in the market value of certain assets and liabilities and natural events such as fires that destroy assets and create losses.