Study guide for Exam #3 Microeconomics

1/76

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

77 Terms

Test 3

...

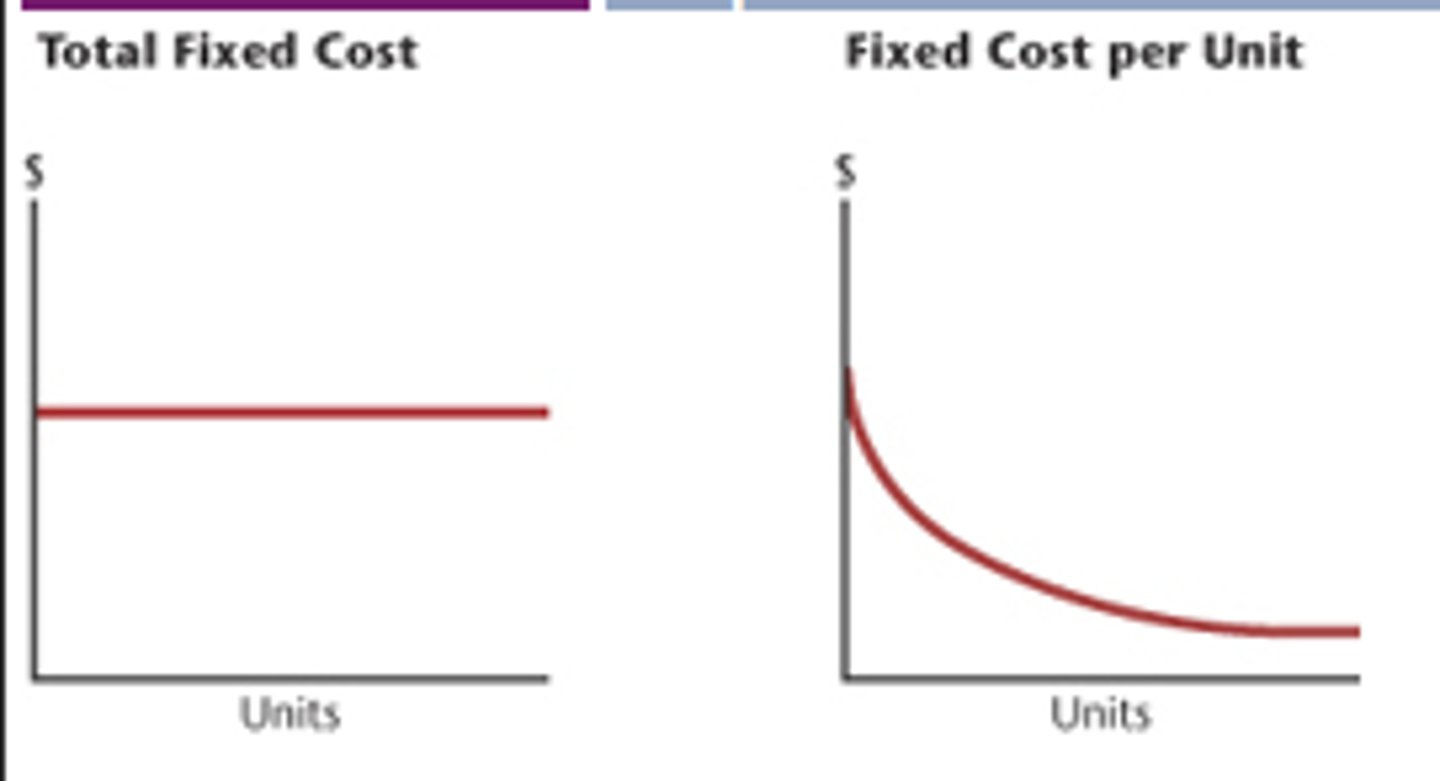

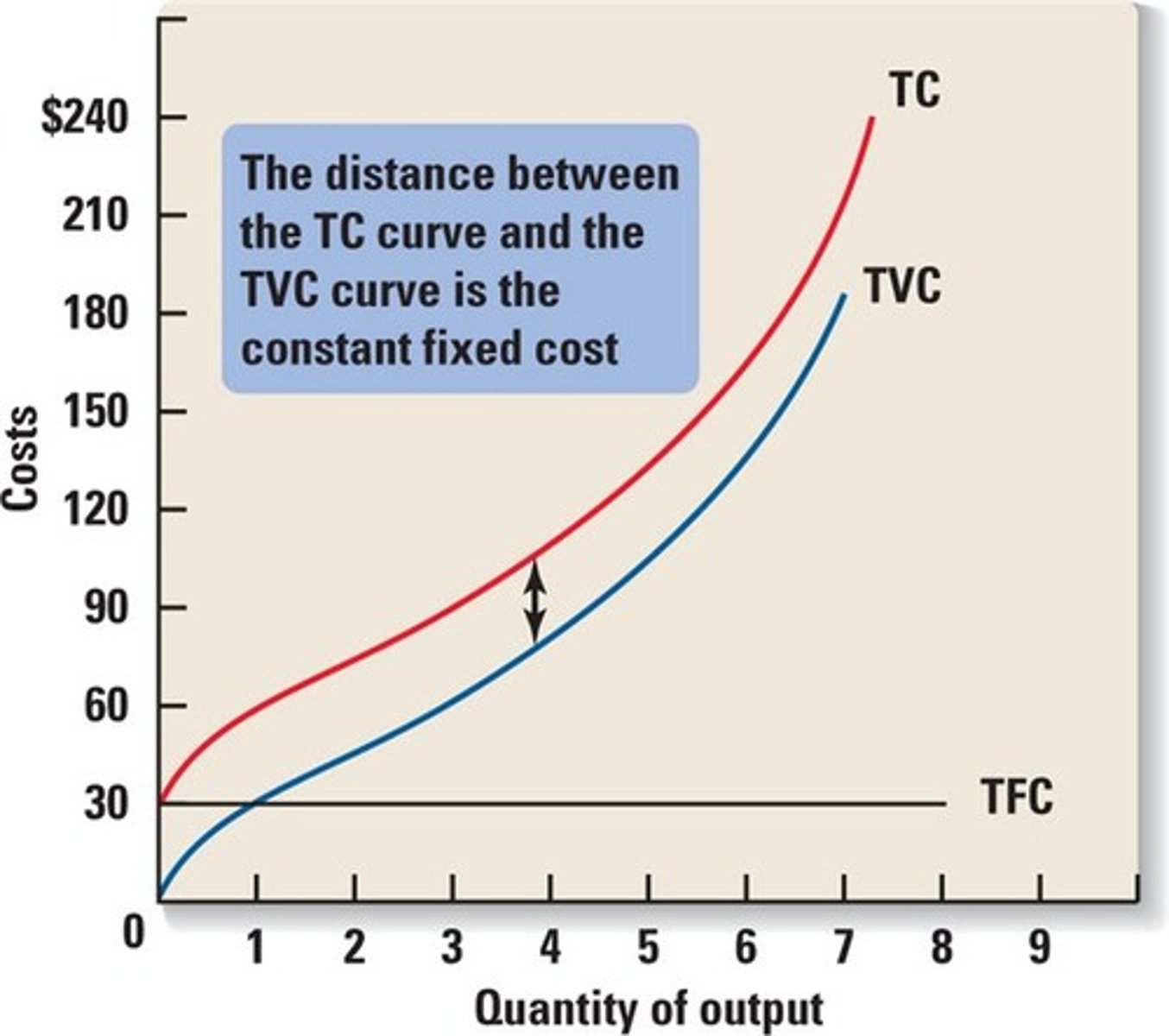

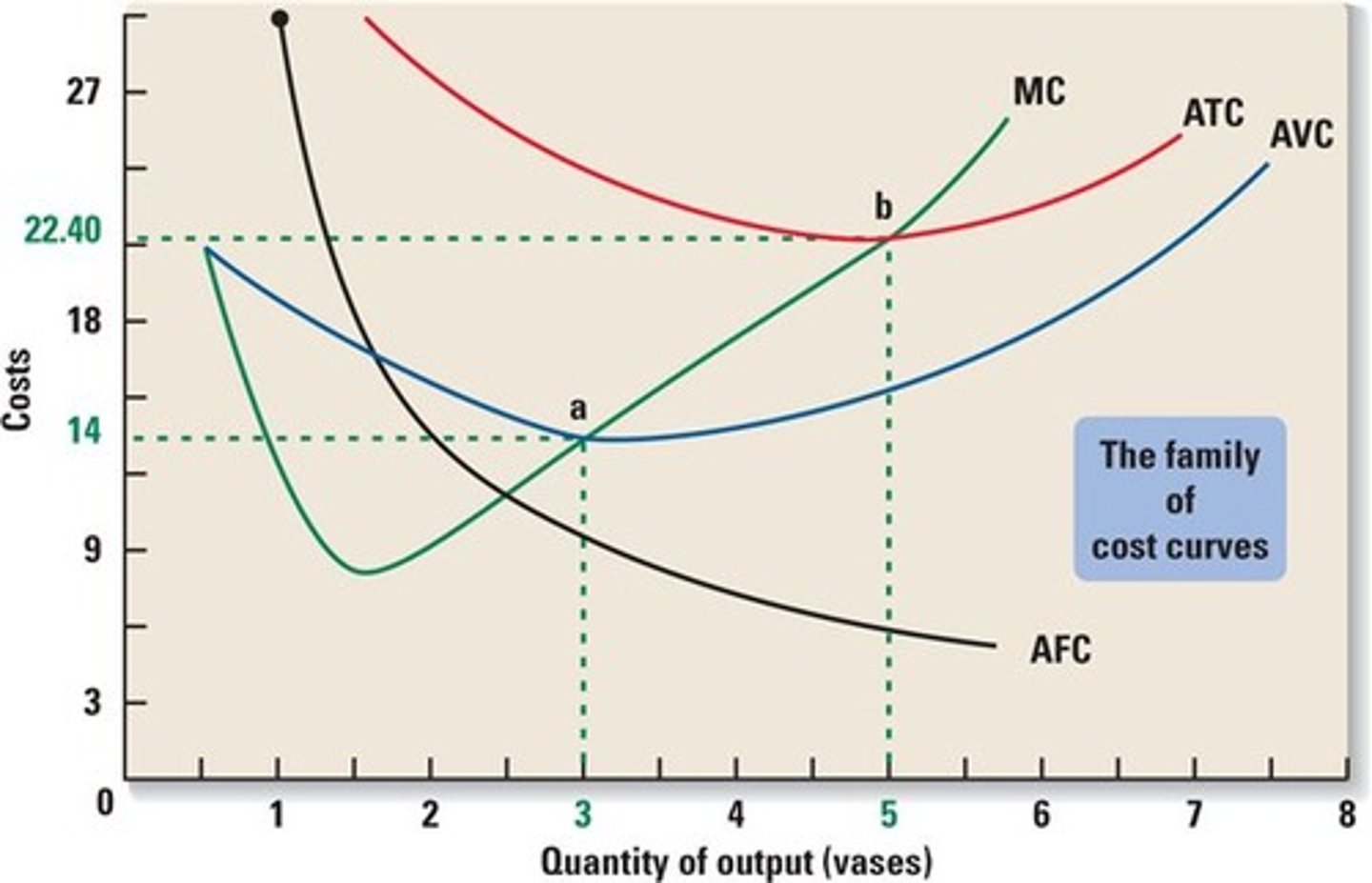

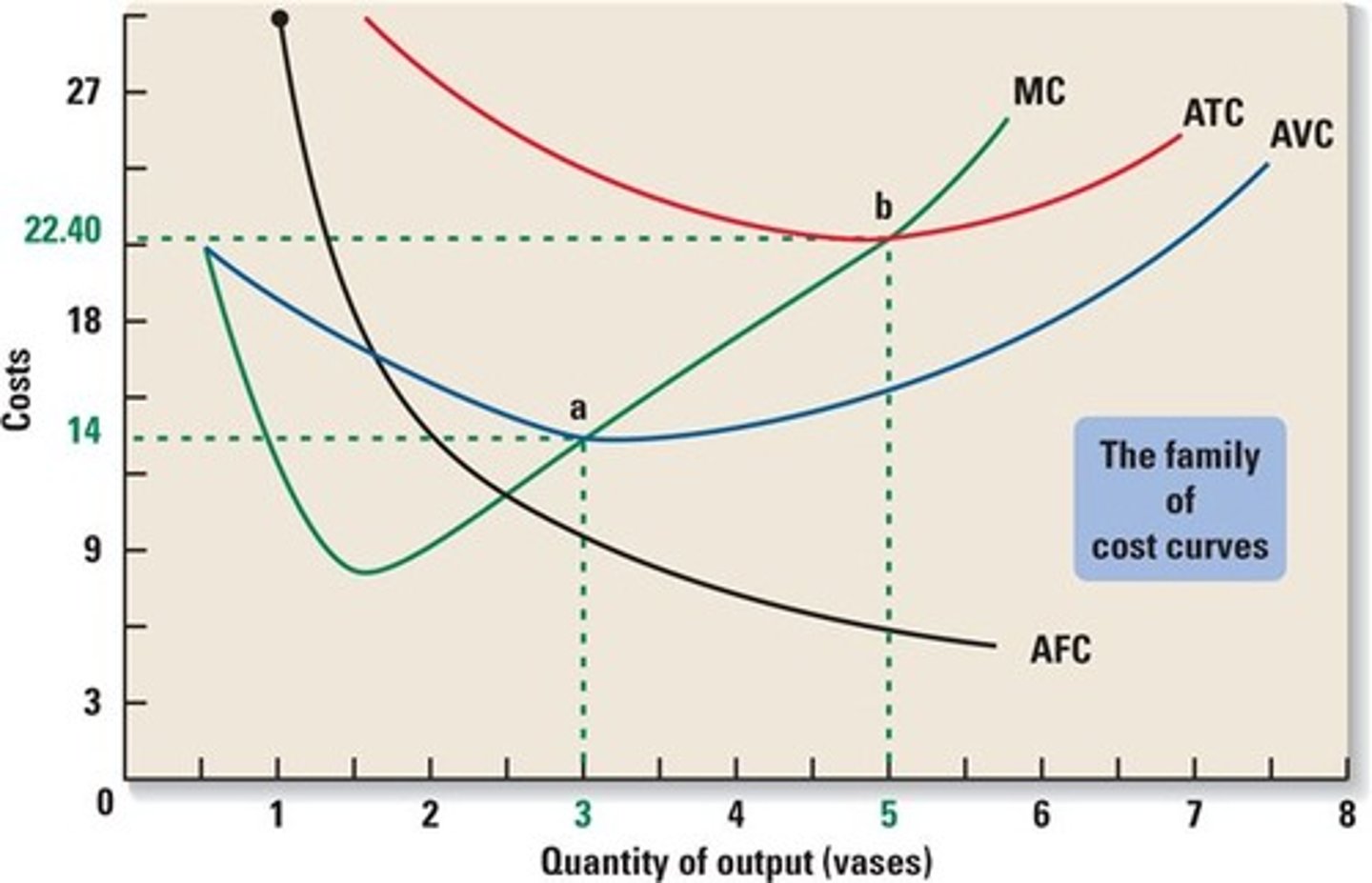

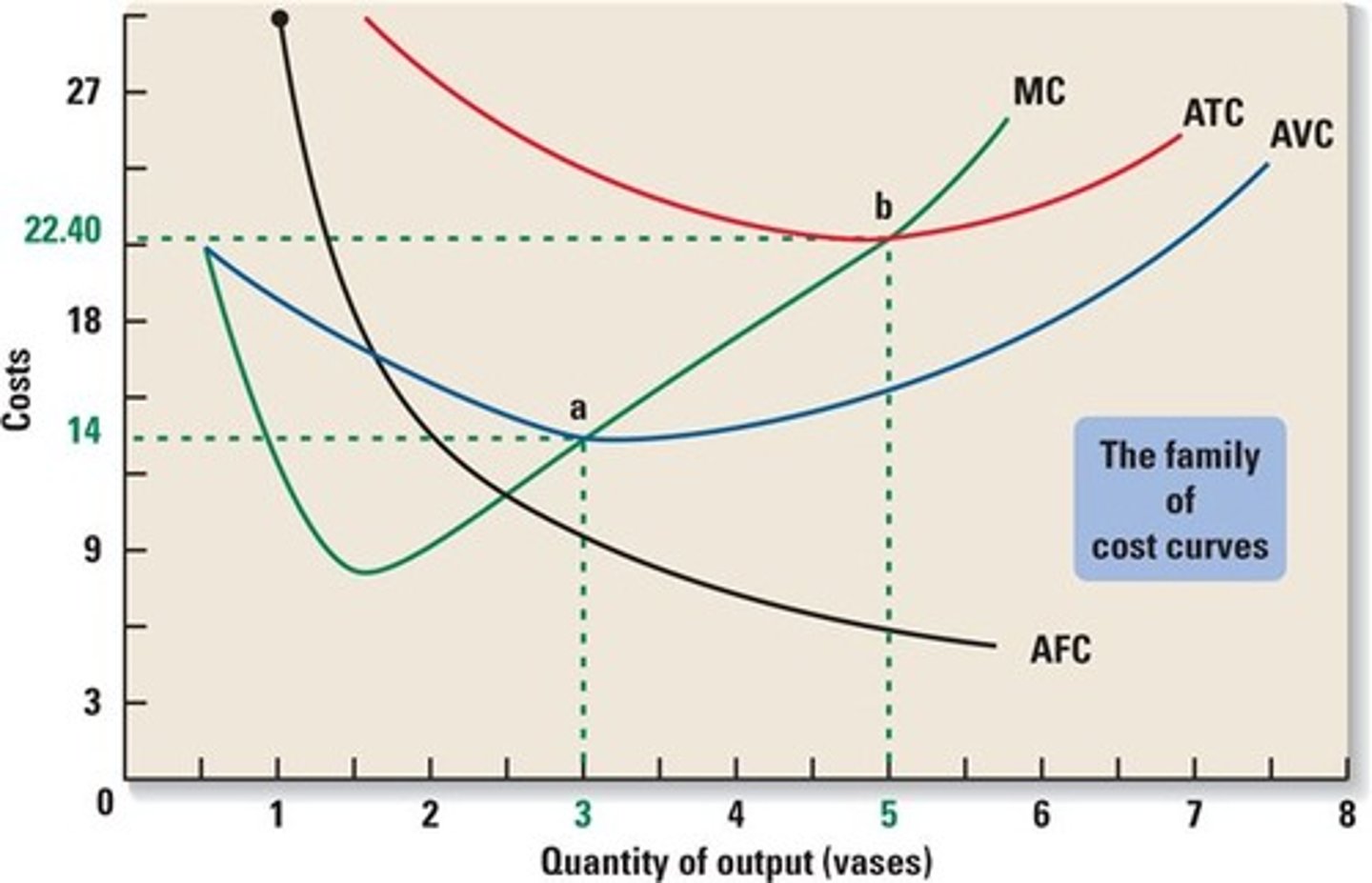

Total Fixed Costs (TFC)

All the expenses that remain the same no matter how many products are made or sold

- TC (Total Cost) - TVC (Total Variable Costs)

Total Variable Costs (TVC)

Costs that vary with the level of production or sales

- TC (Total Cost) - TFC (Total Fixed Cost)

Total Cost (TC)

Total fixed costs + Total variable costs

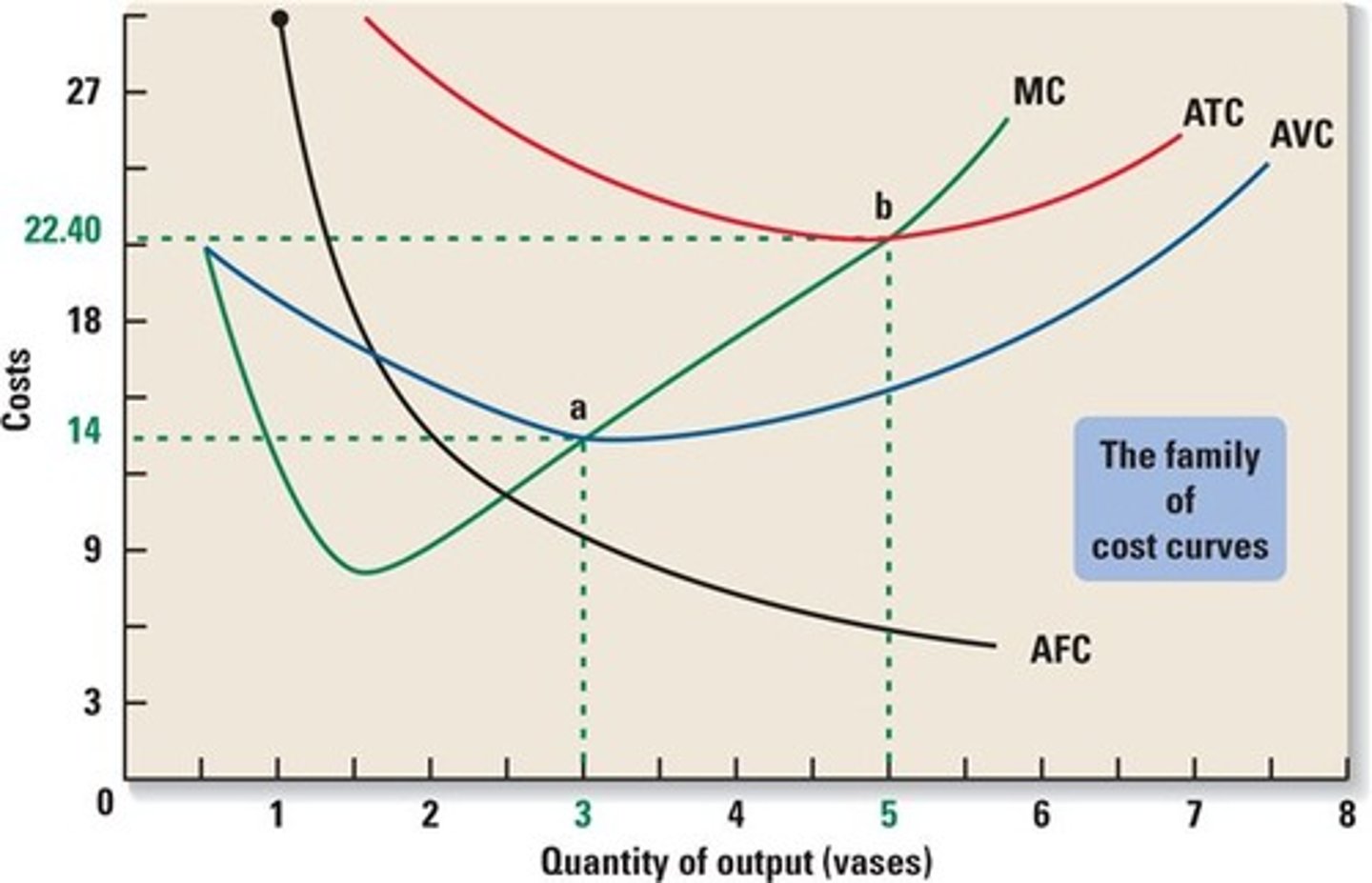

Average Fixed Costs (AFC)

TFC/Q

- These average fixed costs will decrease as production increases

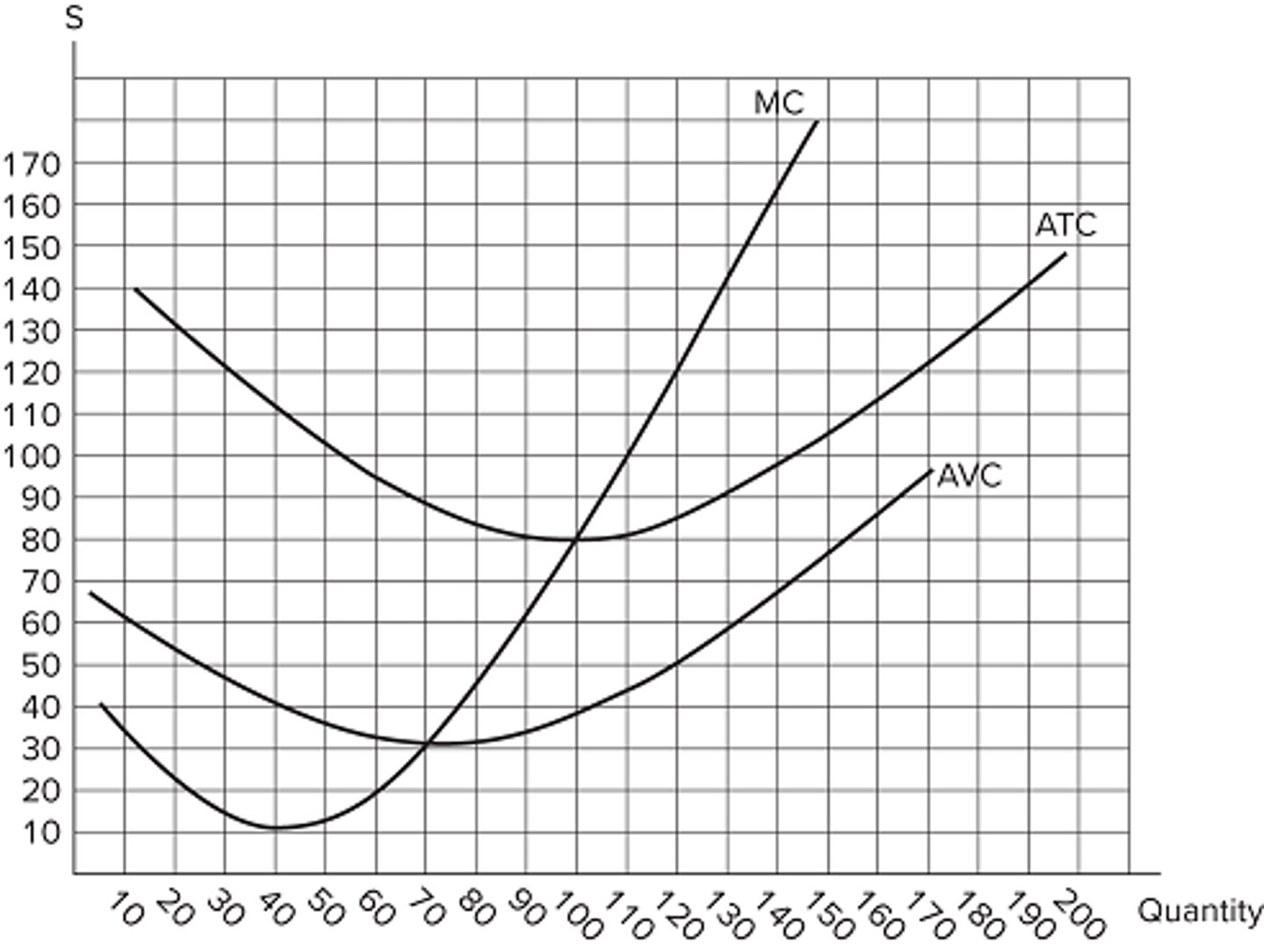

Average Variable Cost (AVC)

TVC/Q

- Decreases to start and then increases almost touching the ATC curve

Average Total Cost (ATC)

TC/Q

- AFC + AVC

Four types of firms in Microeconomics

1. Perfectly Competitive (extreme to the left)

2. Monopolistic Competition

3. Oligopoly

4. Monopoly (extreme to the right)

Which of the four types of microeconomics firms are most efficient?

Perfectly Competitive Firms

- Because goods are being produced and sold at the lowest Average Cost (Price = min of LRAC)

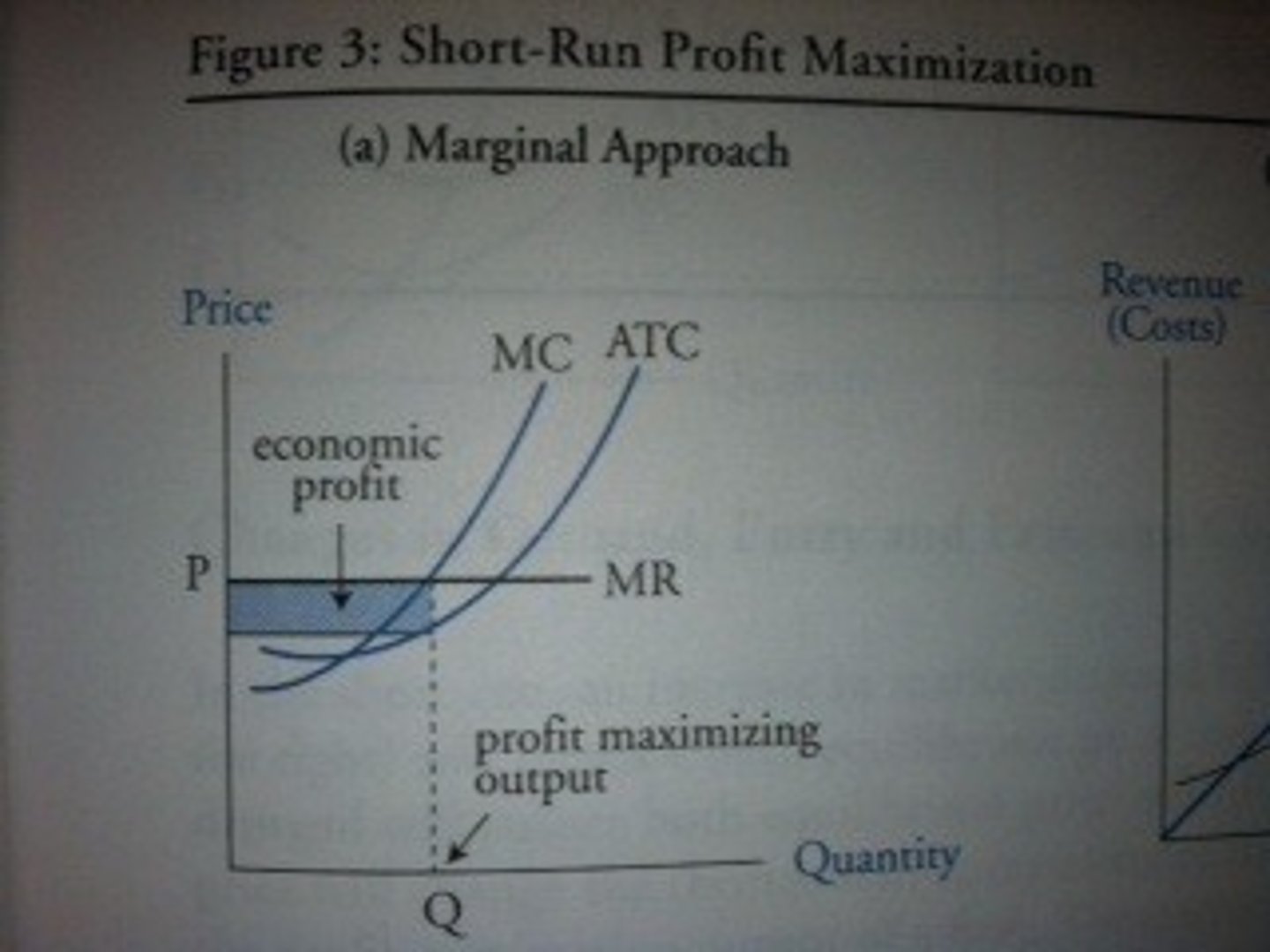

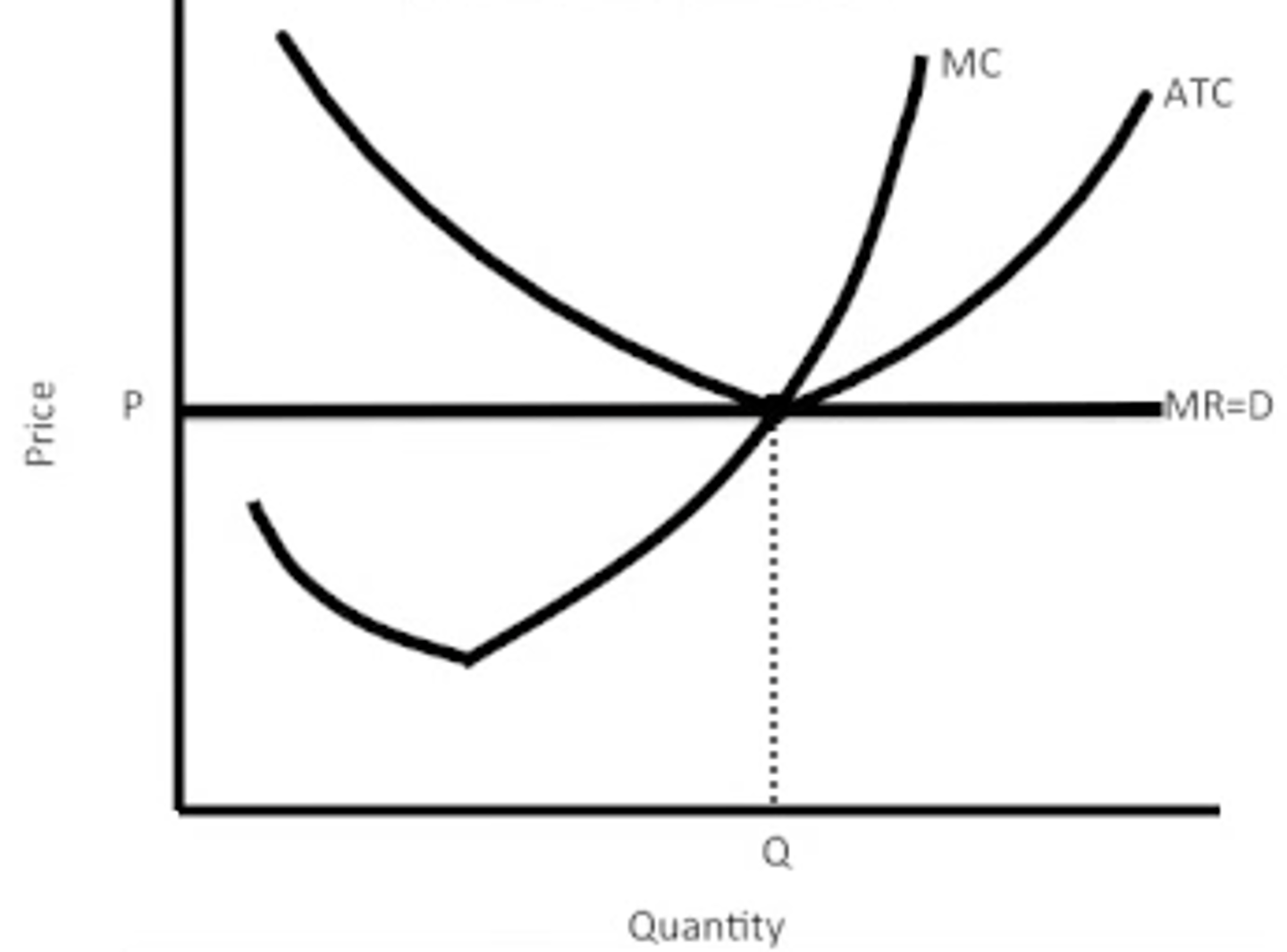

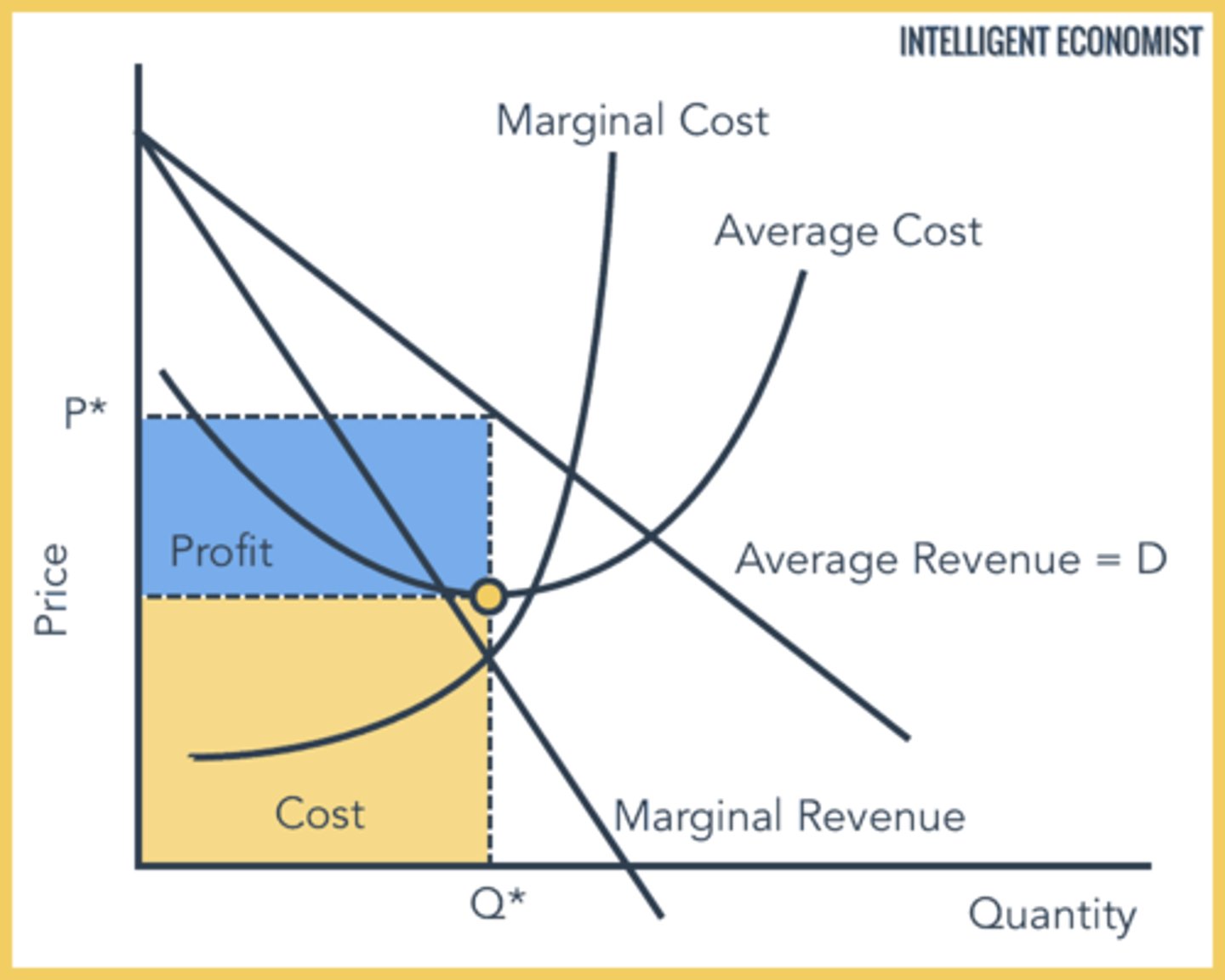

Marginal Cost (MC)

The extra cost incurred by producing one more unit of a product

- The Marginal Cost decreases at first and then increases

Total Revenue (TR)

The total amount of money a firm receives by selling goods or services

- Price * Quantity

Marginal Revenue (MR)

The extra revenue associated with selling an extra unit of output or the change in total revenue with a one-unit change in output

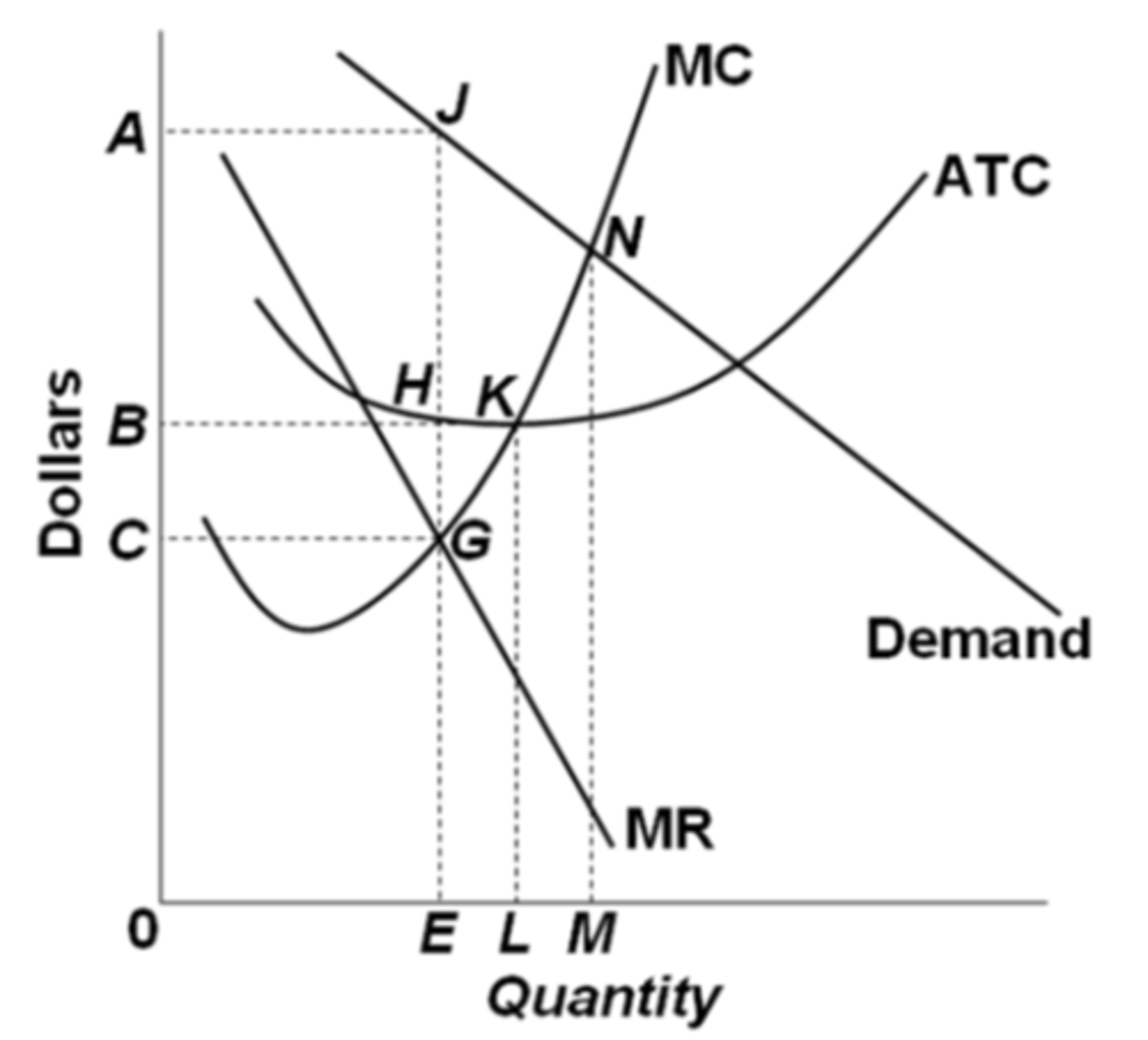

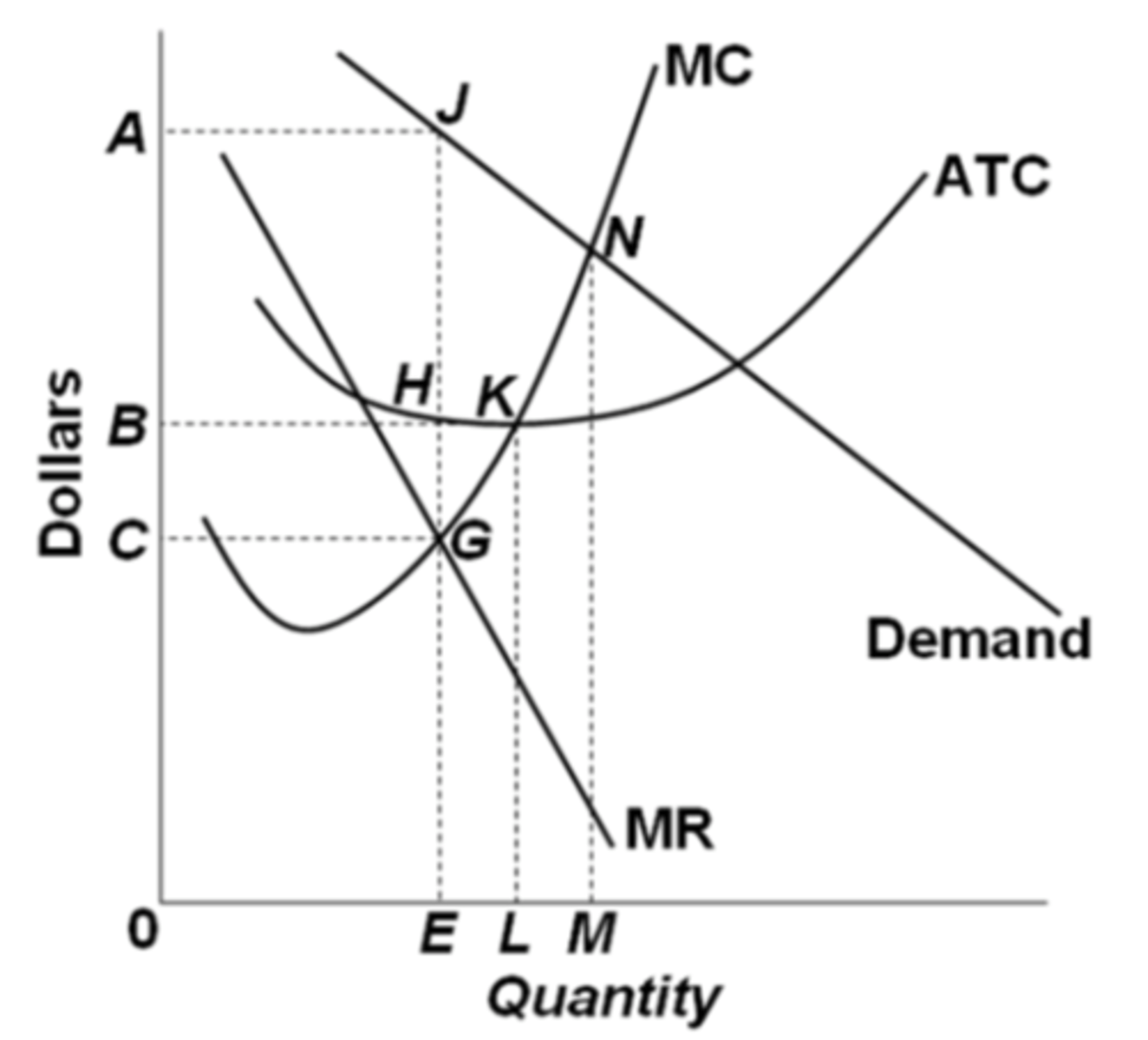

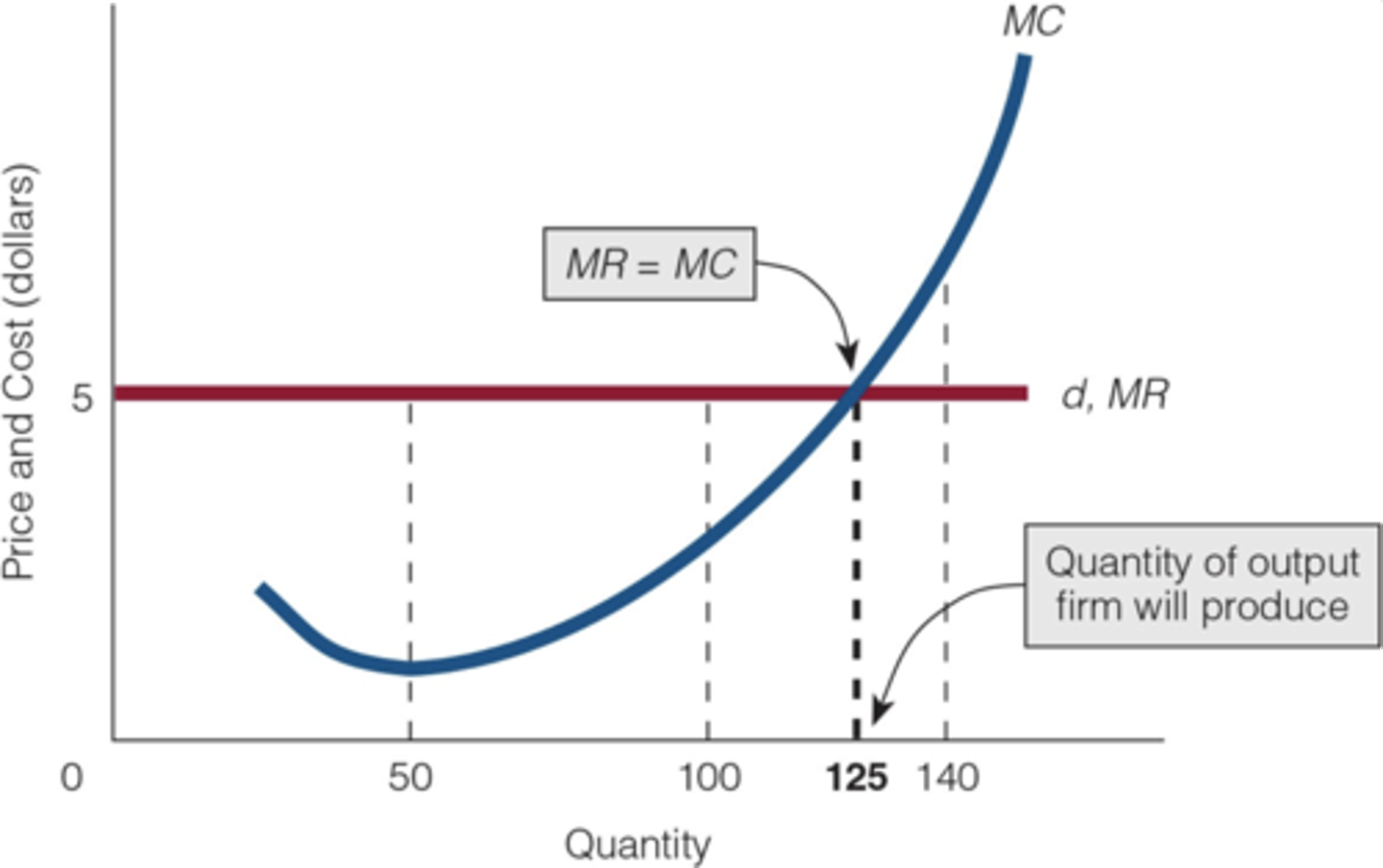

Profit maximizing level of output

- The firm knows what the best output is to be produced

- Means that the firm will produce the BEST output

- DOESN'T guarantee profits

Where do firms need to produce in order to be a "profit-maximizing firm"?

Where Marginal Cost (MC) "extra cost" = Marginal Revenue (MR)

"extra benefit revenue"

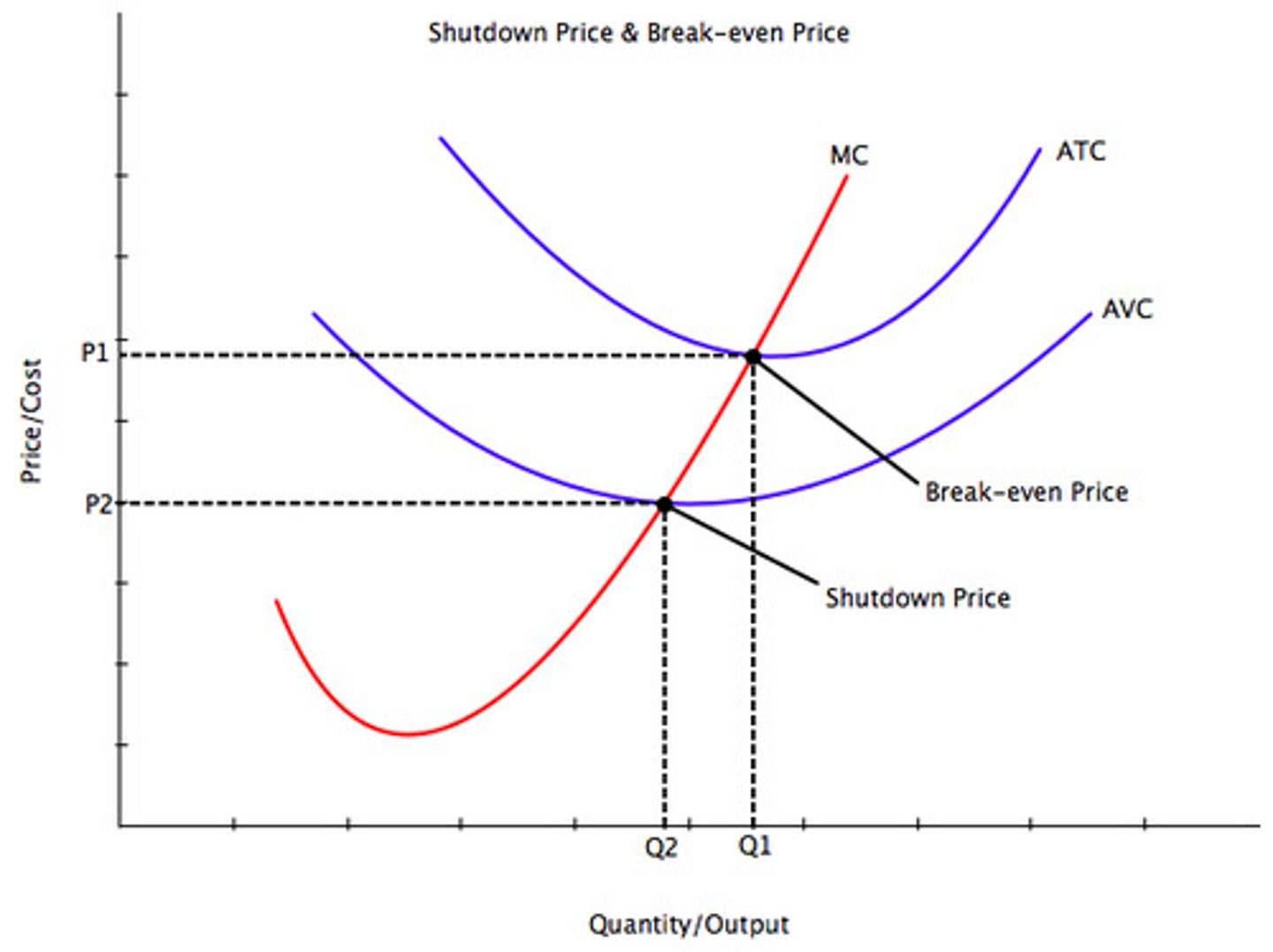

Shut Down Price (short-run)

Price < minimum of AVC

If the Price > AVC do you stay in business?

Yes, because the minimum of the AVC intersecting with the Price is the shutdown price

*If you are making economic losses that are less than the Total Fixed Cost (TFC)

Stay in business because the losses are less than the Fixed Costs (rent, insurance, building space) that you're already paying for no matter what

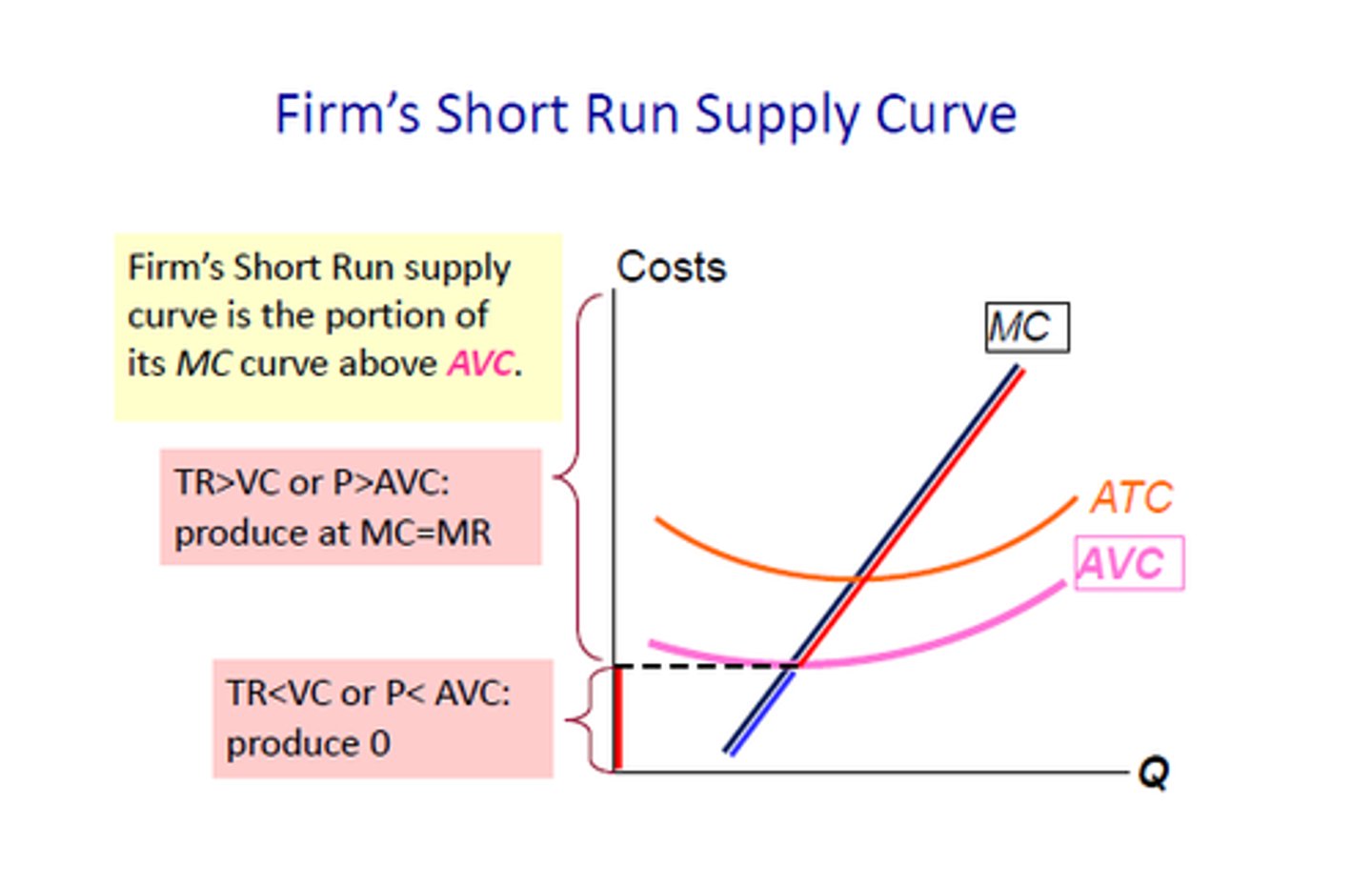

Short-Run Firm Supply Curve

The portion of the firm's marginal cost curve that lies above the average variable cost curve.

An Industry's Supply Curve

The horizontal sum of all existing firms' short-run supply curves in that industry.

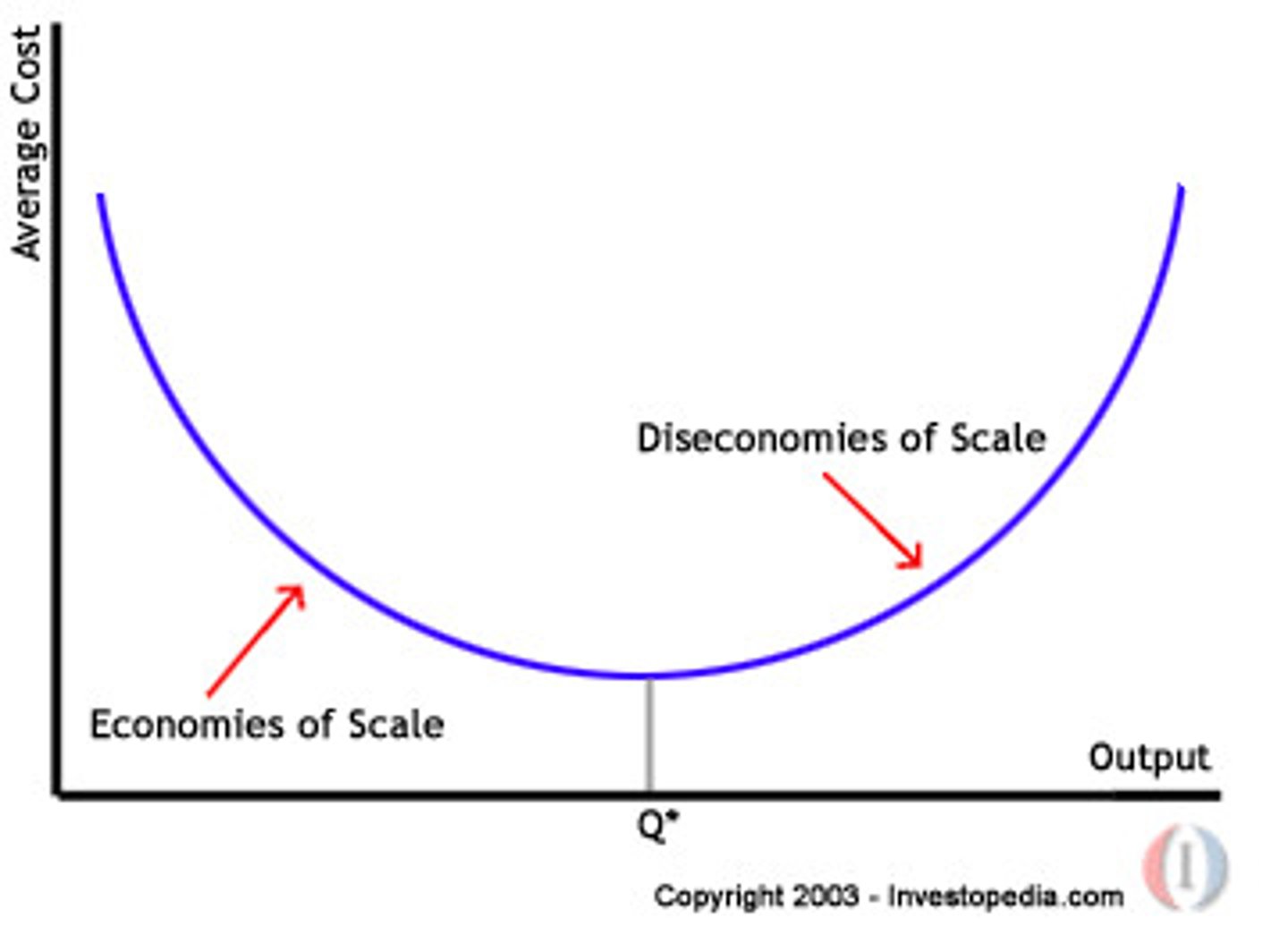

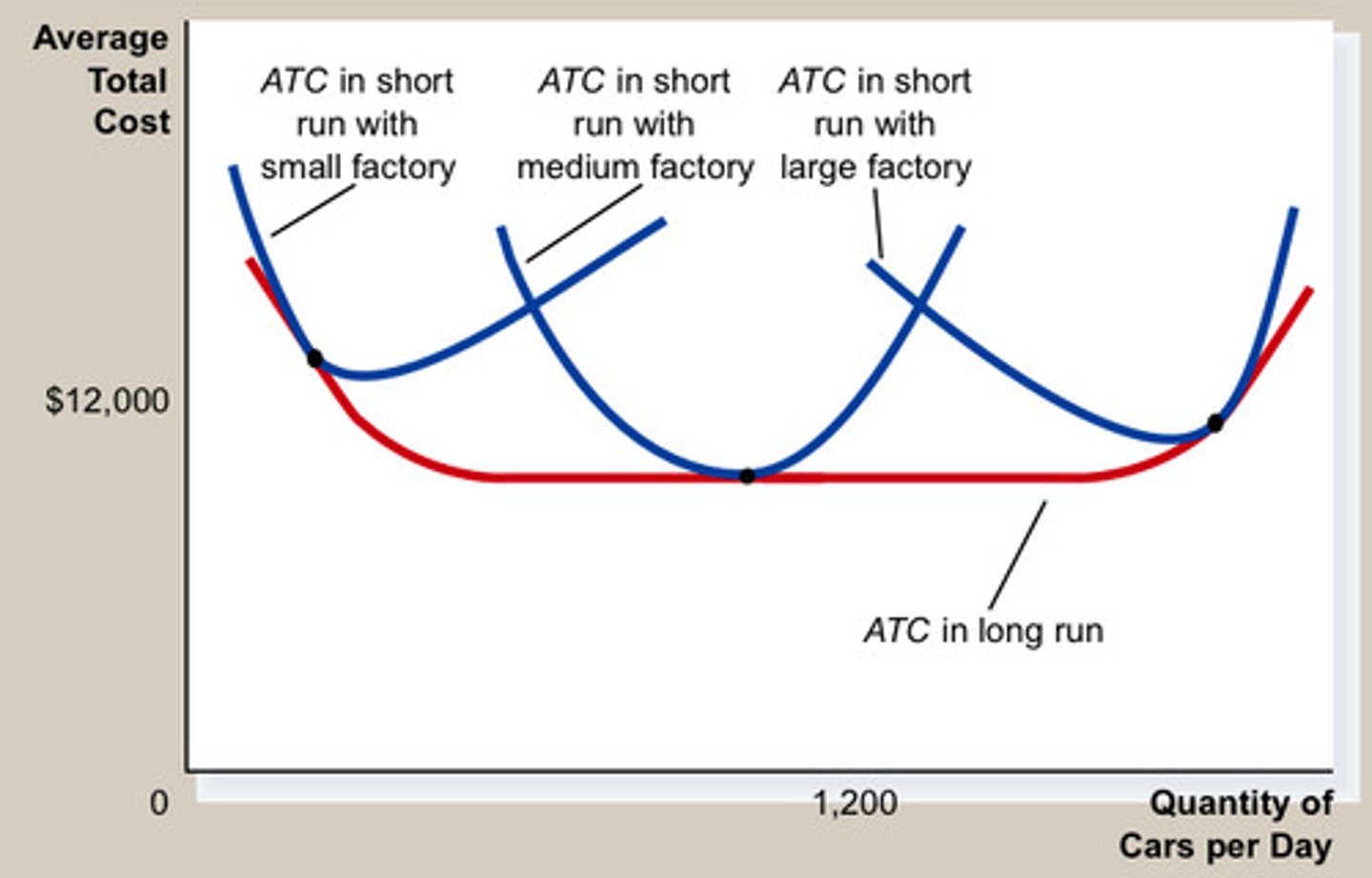

Economies of Scale

Factors that cause a producer's average cost per unit to fall as output rises

- The MC is in constant decline giving a firm the benefit of production over other firms in the industry

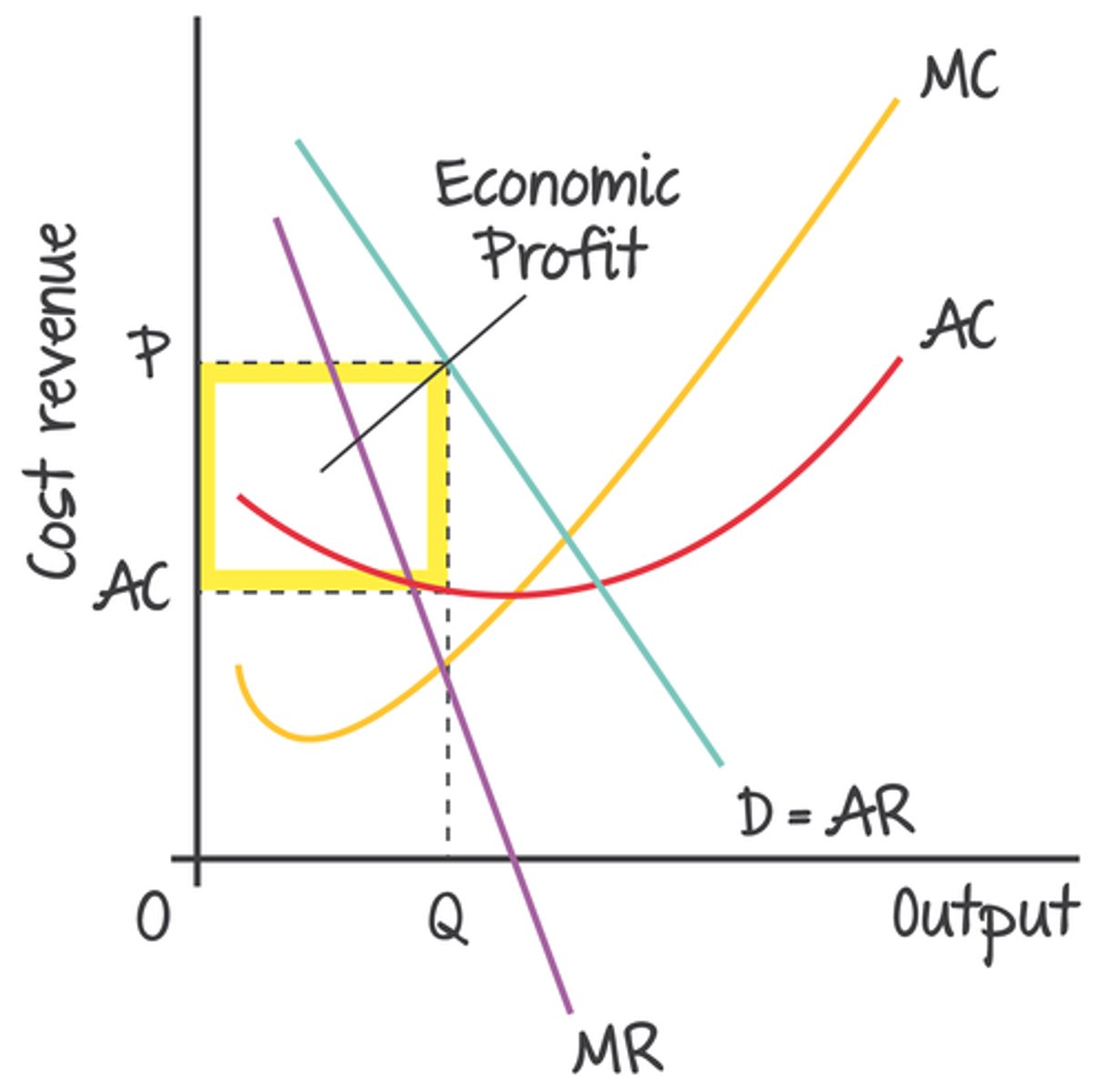

Economic Profits for the company happen when...

When

- Price > Average Total Cost (ATC) Curve

OR

- TR > TC

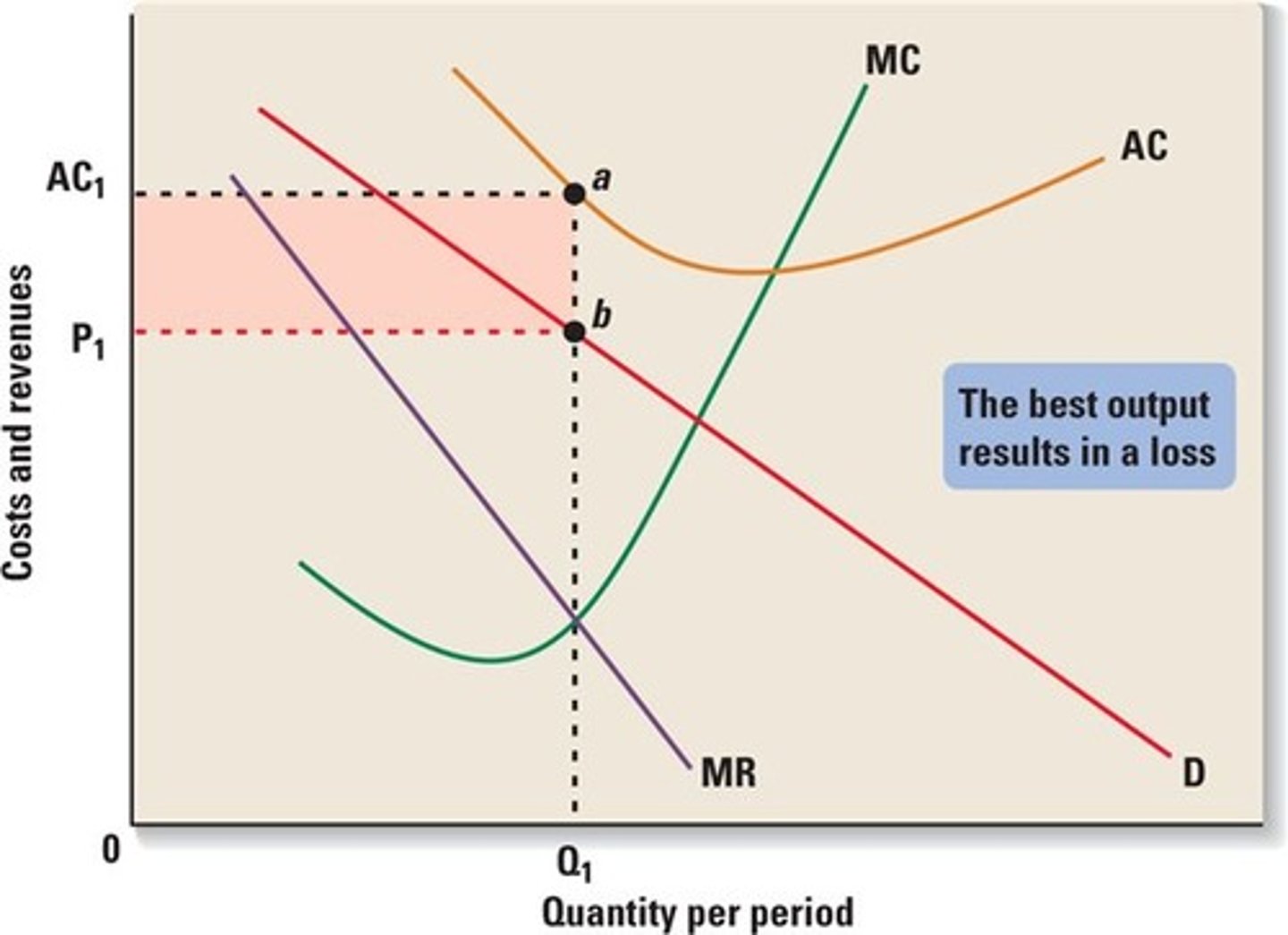

Economic losses occur when...

When

- Price < Average Total Cost Curve (ATC)

OR

- TR < TC

Companies 'break-even', earn 'zero economic profit', or earn 'normal profits' when...

When

- TR = TC

OR

- P = ATC

Resource-allocative efficiency firms produce...

Where P (Price) = MC (Marginal Cost)

Productive efficient firms produce...

Where P (Price) = min AC (ATC = LRAC)

*Market Power

The ability of a company to change prices and output like a monopolist

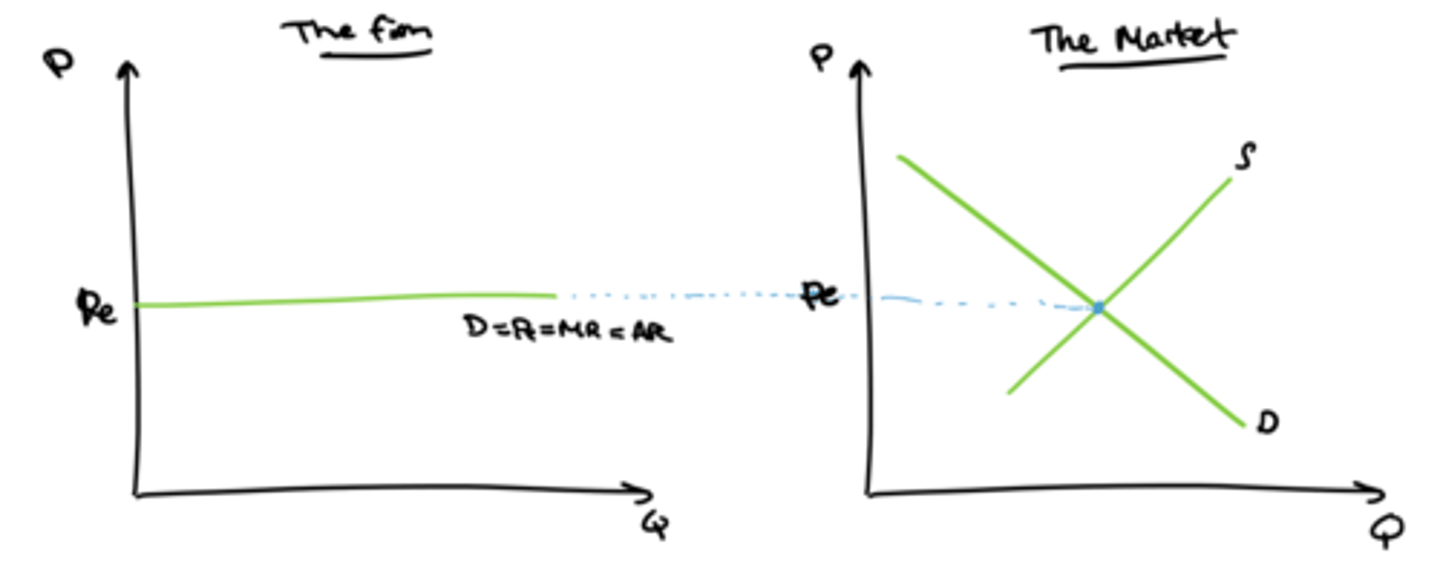

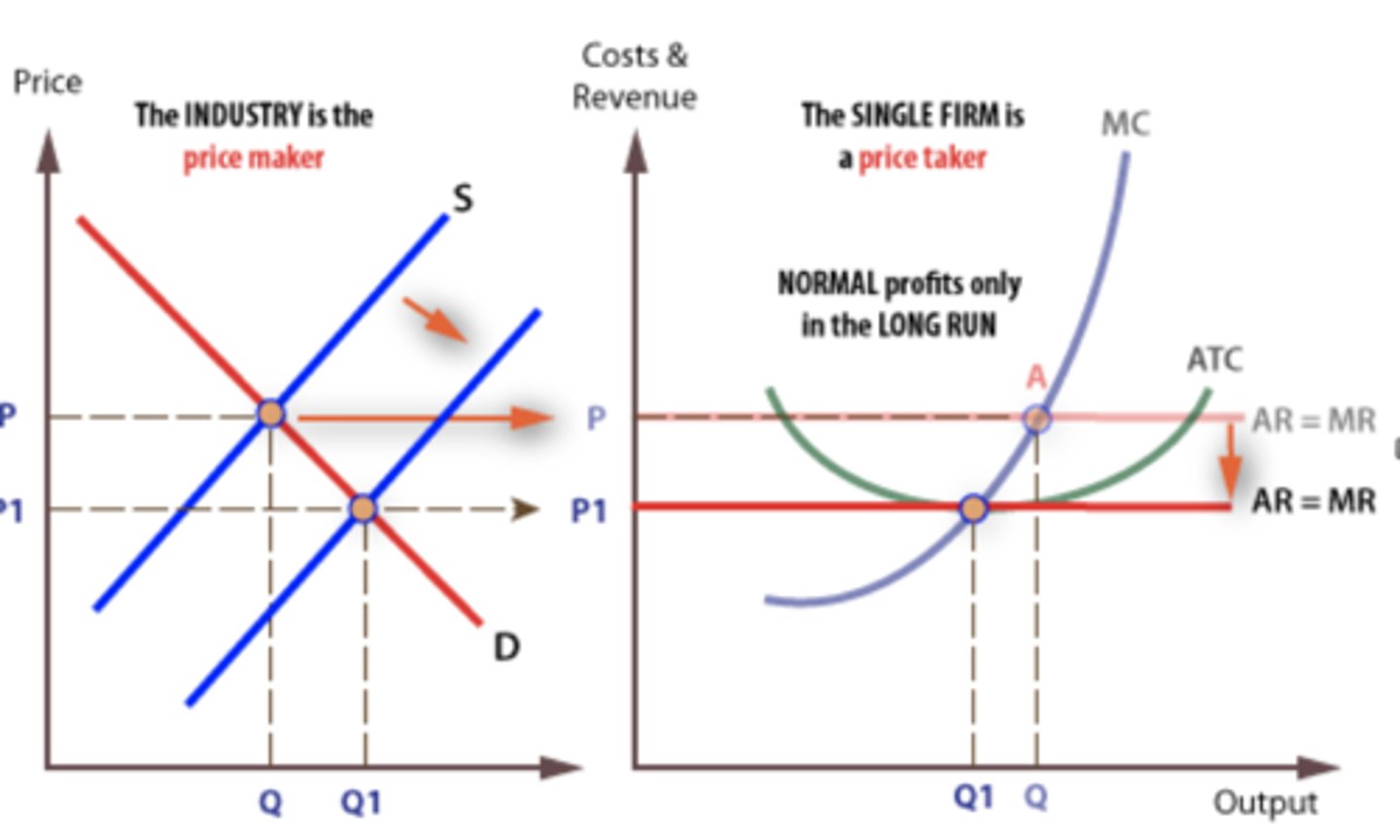

Perfect Competition...

I. Market Structure

1. A very large number of relatively small firms that are independent

2. Homogenous product (consumers cannot tell the difference between your product and another company product) - the product is the same no matter who provided it

- Homogenous Products: Ex. Bottled Water

3. Firms are PRICE TAKERS

4. No barriers to enter or exit into this market

Examples of Perfect Competition

Farmers markets selling similar products like Apples and Tomatoes

- Perfect Competition is a theory, so it doesn't fully exist anywhere in the world

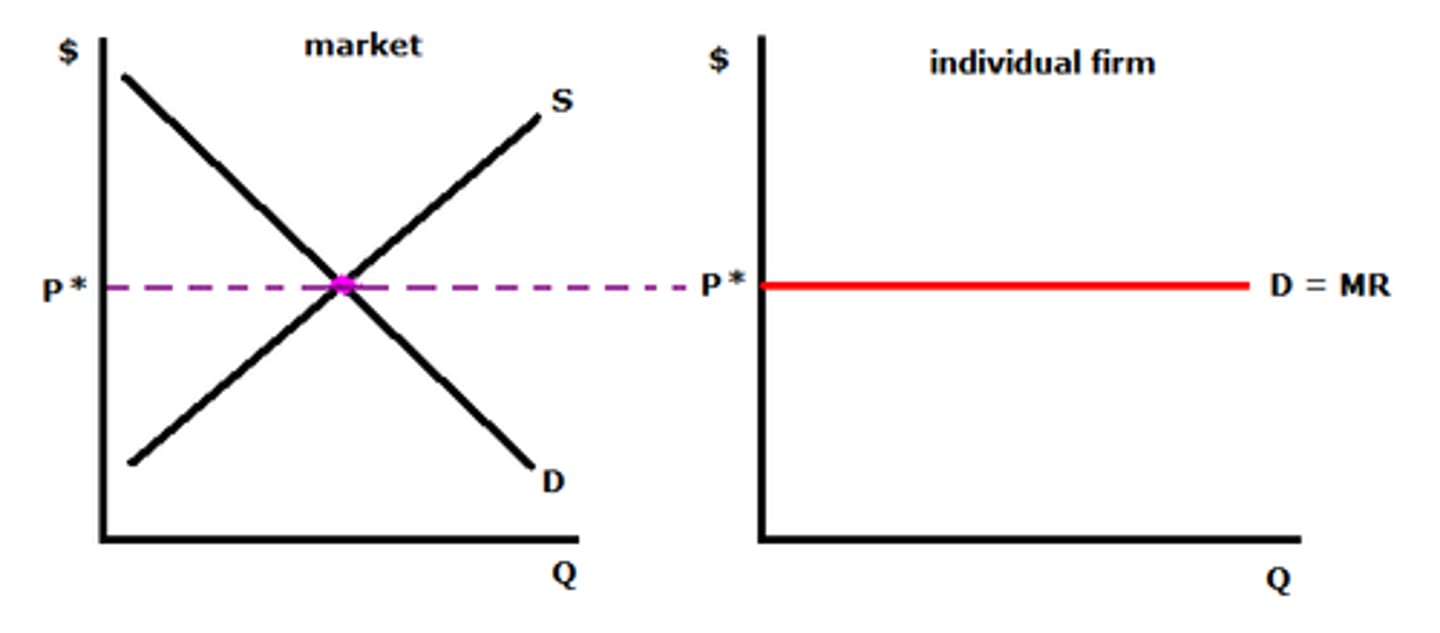

Price Taker (Perfectly Competitive Firm)

Firms that take the price given by the market - NO CONTROL OVER THE PRICE

II. Short run (Perfectly Competitive)

1. Eco Profit

2. Break even

3. Eco loss

- Stay in business if Losses < TFC

- Shut down if Losses > TFC

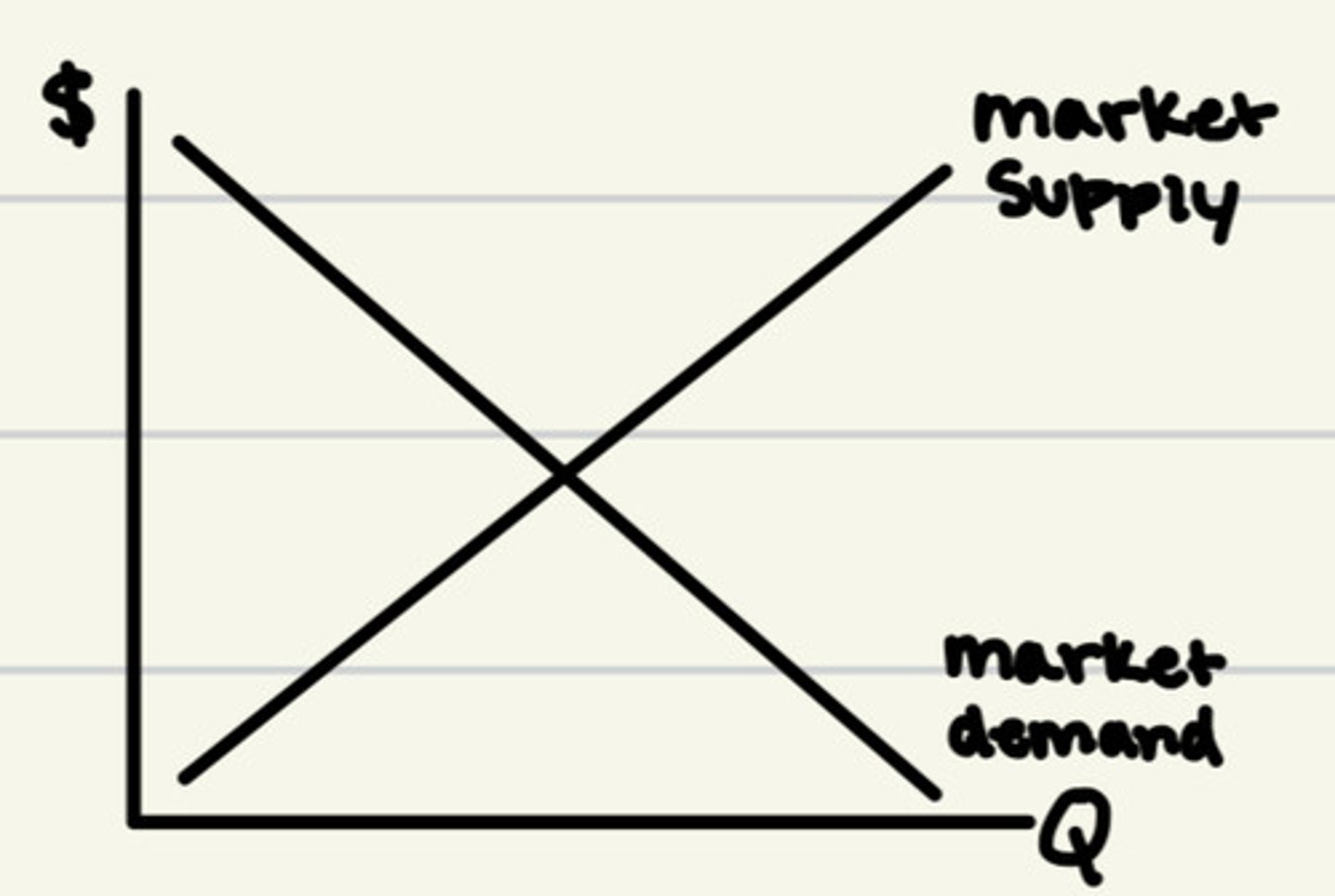

Market Demand

Horizontal summation of individual consumer demands

- Downward sloping illustrating the Law of Demand

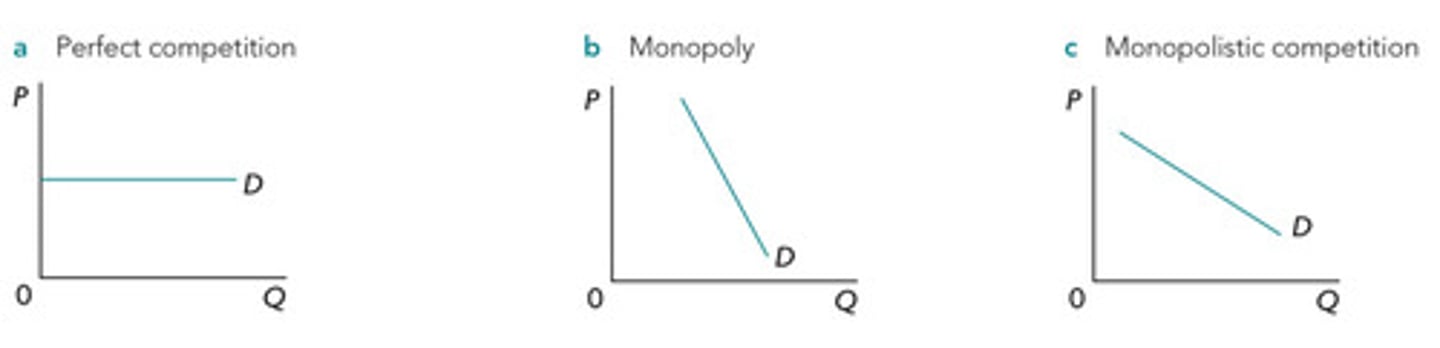

Firm's Demand in Perfectly Competition

- Equals to MR

- Horizontal because there are lots of substitutes

- Perfectly Elastic

Market Supply

Horizontal summation of firms' supply curves

- Generally, it is upward-sloping

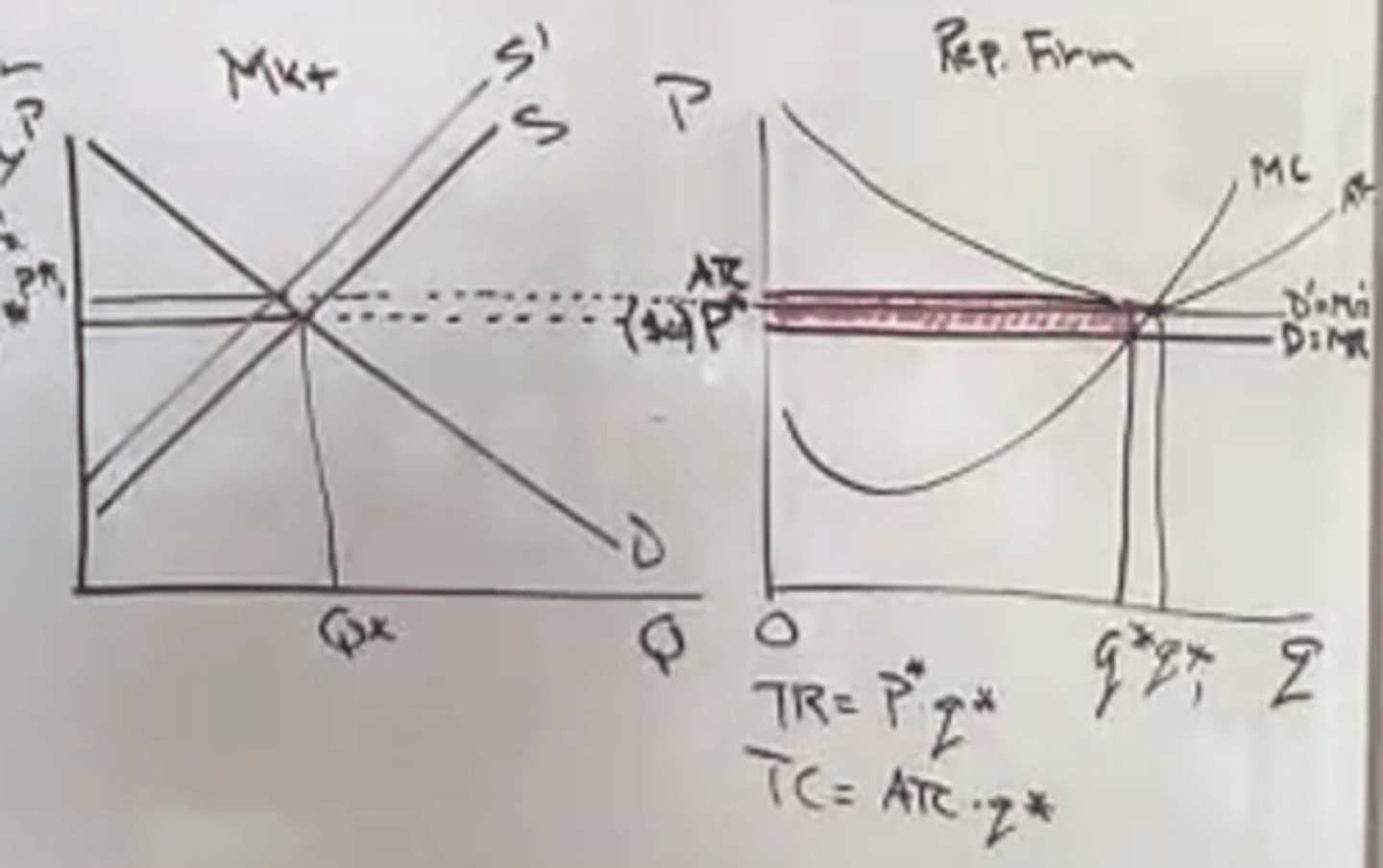

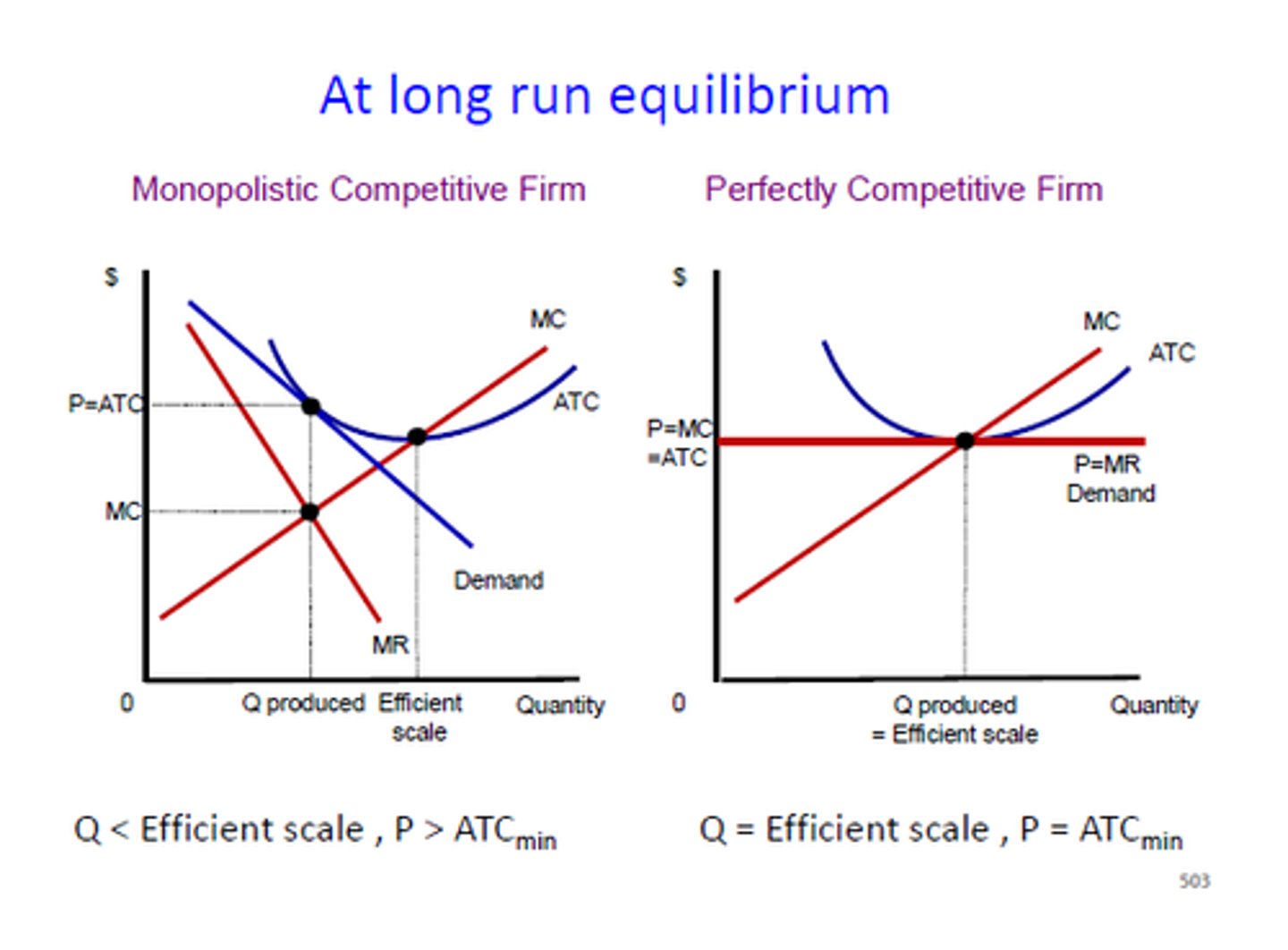

Describe the long run (Perfectly Competitive Market)

You can exit if you are not successful (no need to shut down like the short-run)

- All Perfectly Competitive Firms ONLY can break even (make normal profit) in the long run

III. Performance (Perfectly Competitive Market)

Perfectly competitive firms break even in the long run because it is easy for firms to enter and exit the market

FIRMS ARE!

1. Resource-allocative P = MC

2. Productive efficient P = min AC (ATC = LRAC)

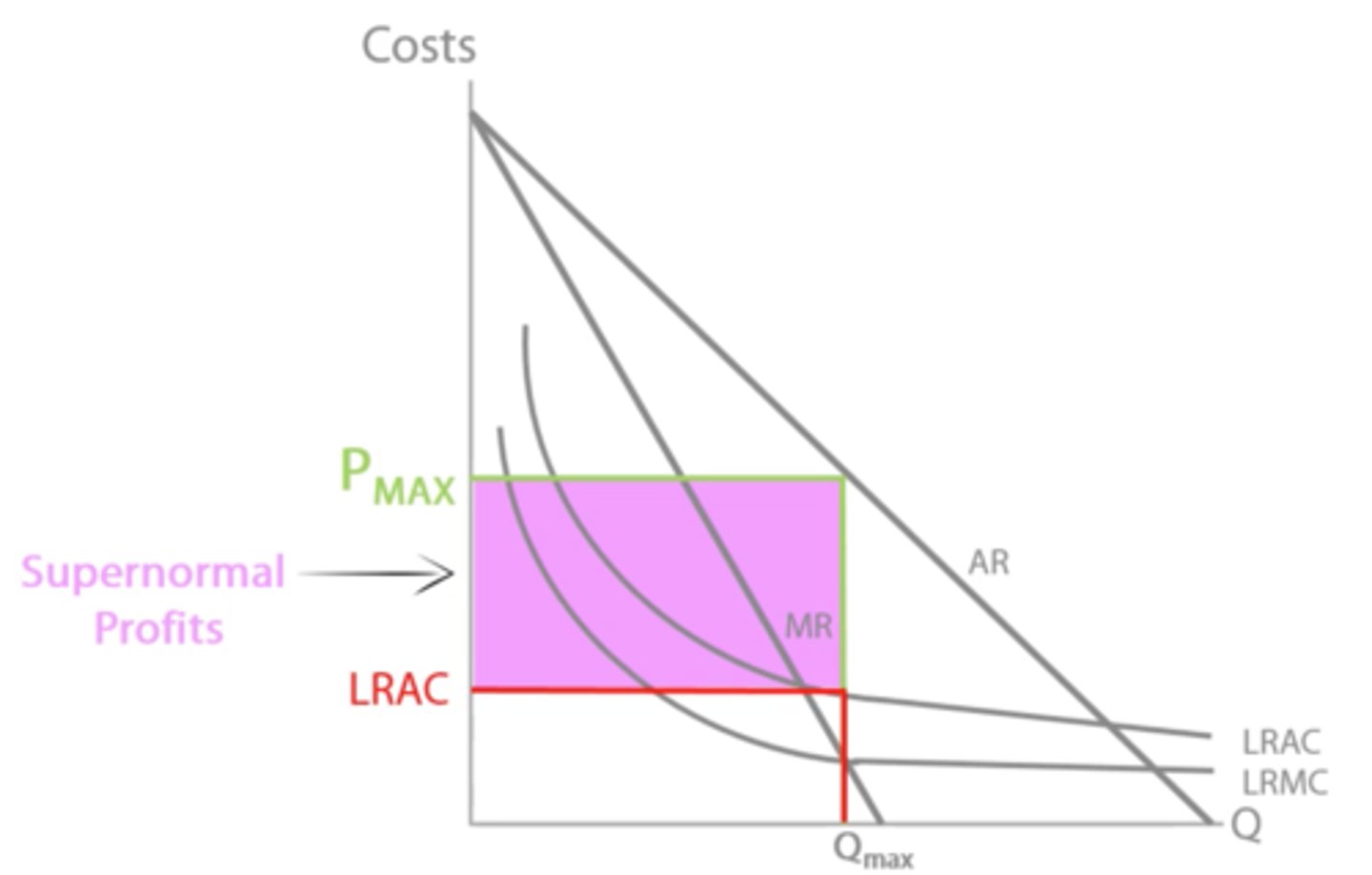

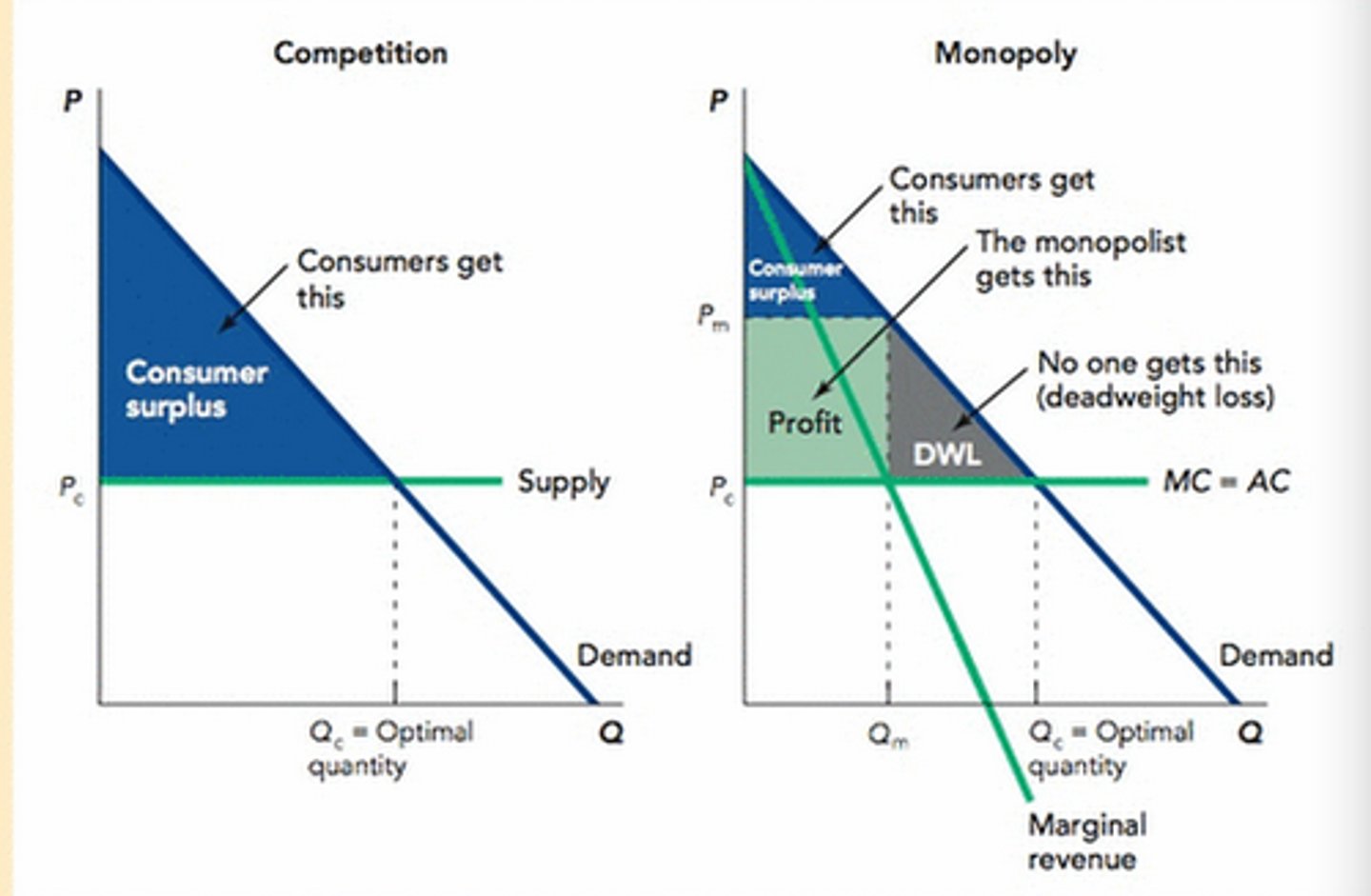

Monopoly

A market in which there are many buyers but only one seller.

I. Structure (Monopoly)

1. Single firm, single seller (firm is the industry)

2. Produce 'unique' products (there are no close substitutes)

3. Price 'maker' or 'price setter'

4. Barriers to entry and exit

- Legal (involving the government)

- Economic

- Ownership of resources

- Economies of Scale (Natural Monopoly)

Examples of Monopolies

Internet

Social Media

Past Monopoly of Cellphones

- AT&T

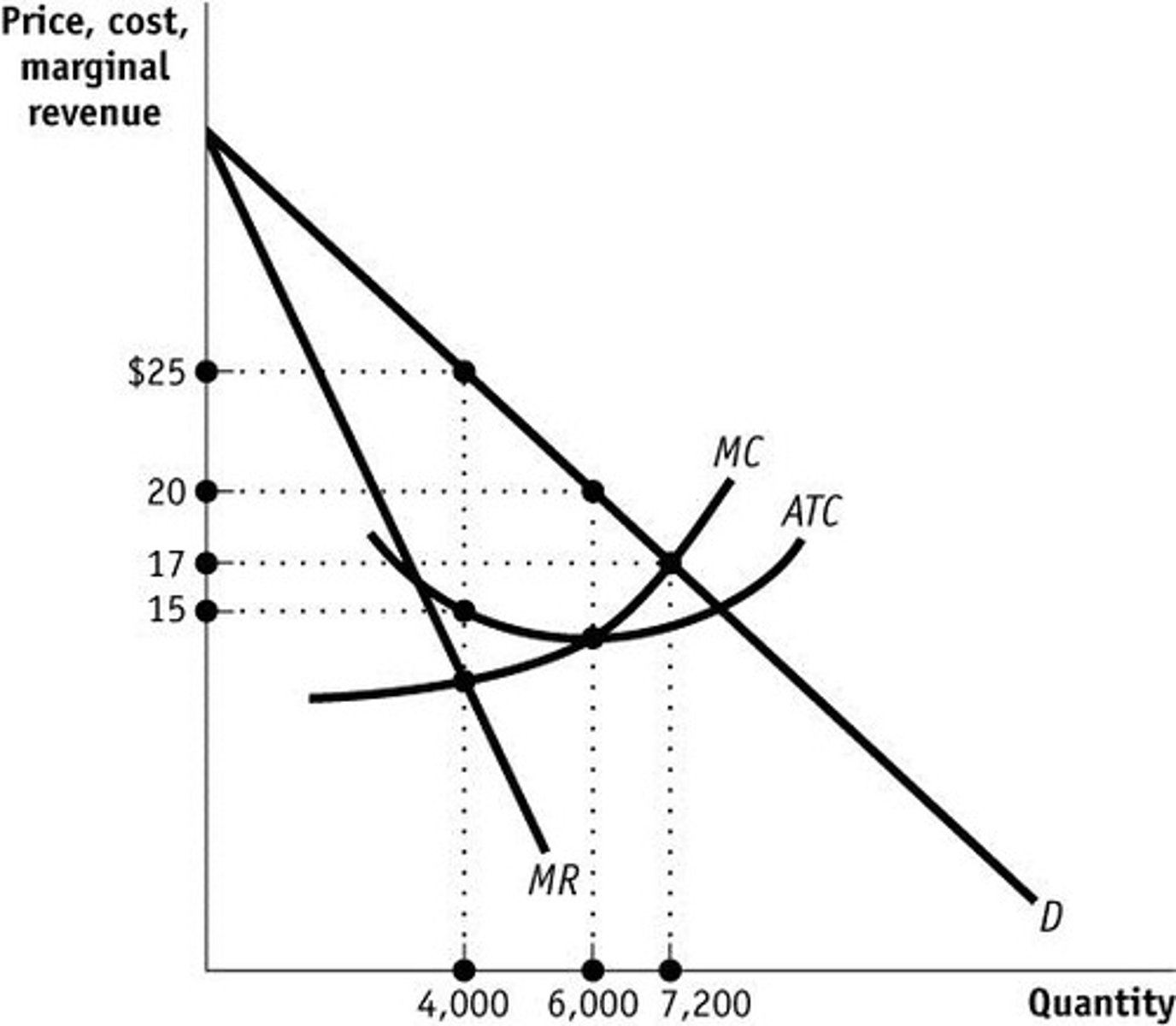

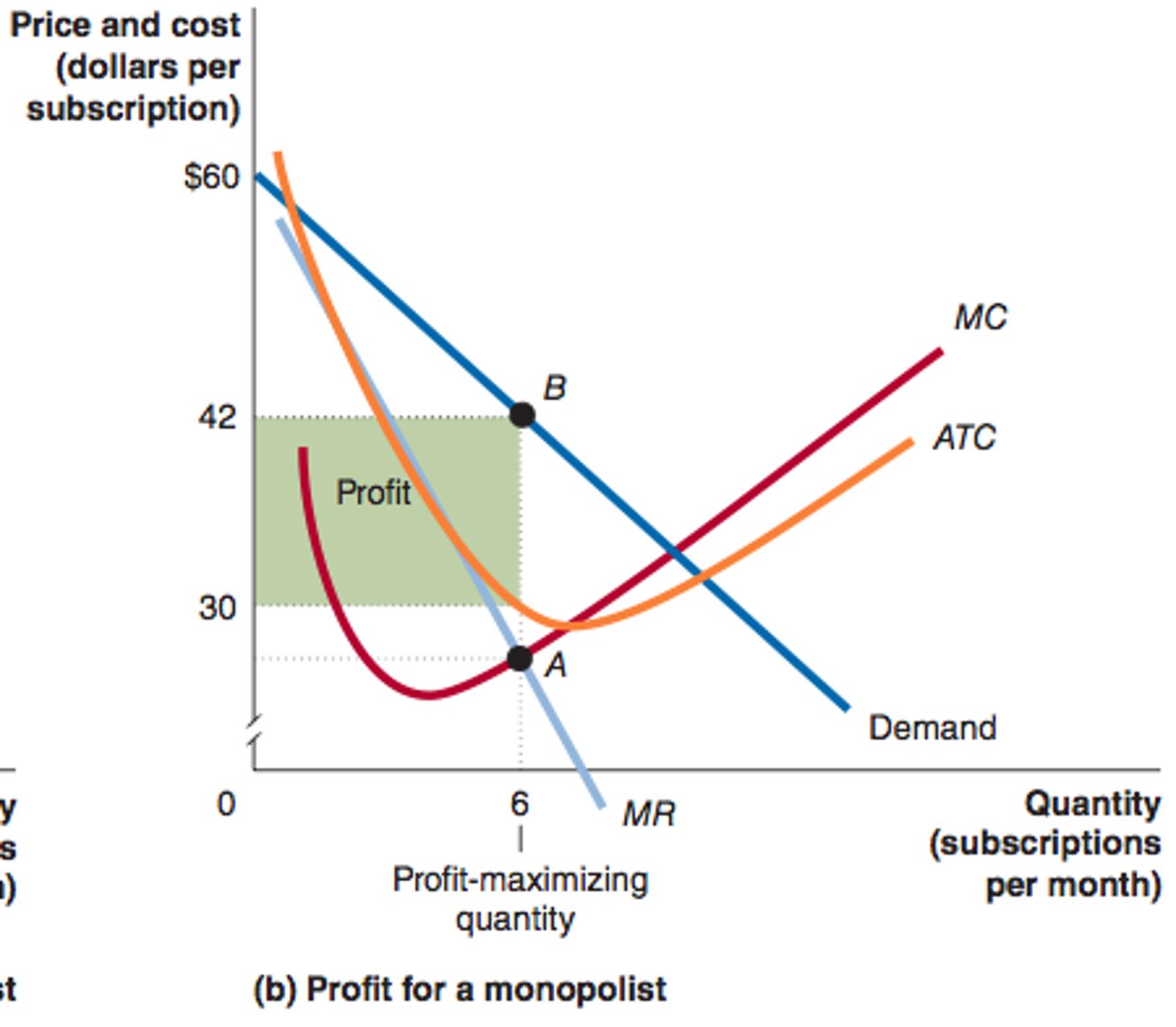

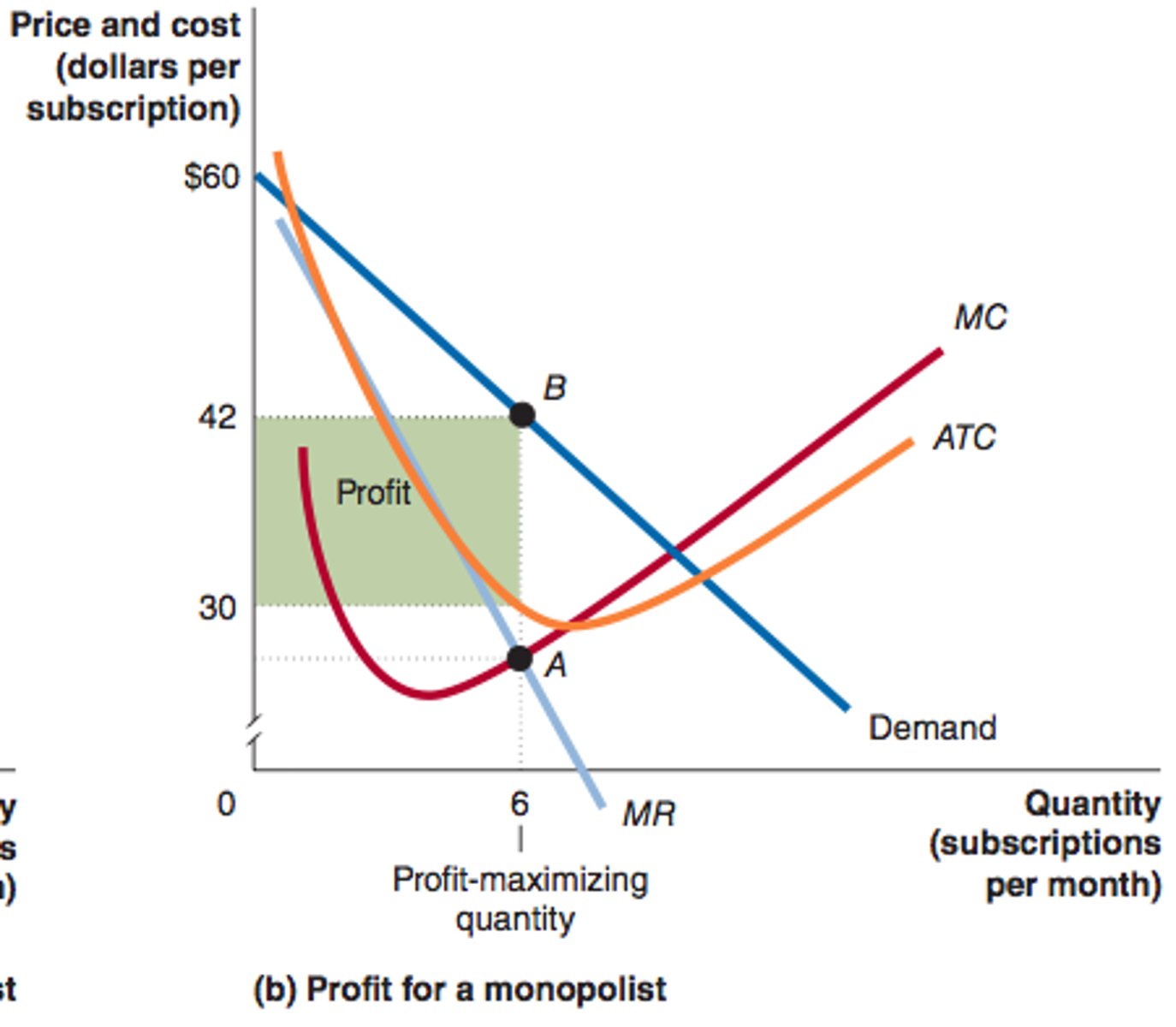

What is the relationship between Demand, Total Revenue, Marginal Revenue, and Elasticity in a Monopoly?

View the graph on Quizlet!

1. Monopolies will sell along the elastic part of the Demand Curve at Point B

2. Monopoly produces where Marginal Revenues are positive

3. Monopoly produces the output where MR = MC (profit-maximizing), but they charge a higher price (which is point B)

4. Total Revenue box is 0 to 42 to Point B to Q1 (6)

What does the Marginal Revenue curve do in a Monopoly?

Downward sloping (eventually goes below the x-axis)

Price vs. Marginal Cost in a Monopoly

Price set above the Marginal Cost

- Monopoly's can charge these outrageous prices because there are no close substitutes

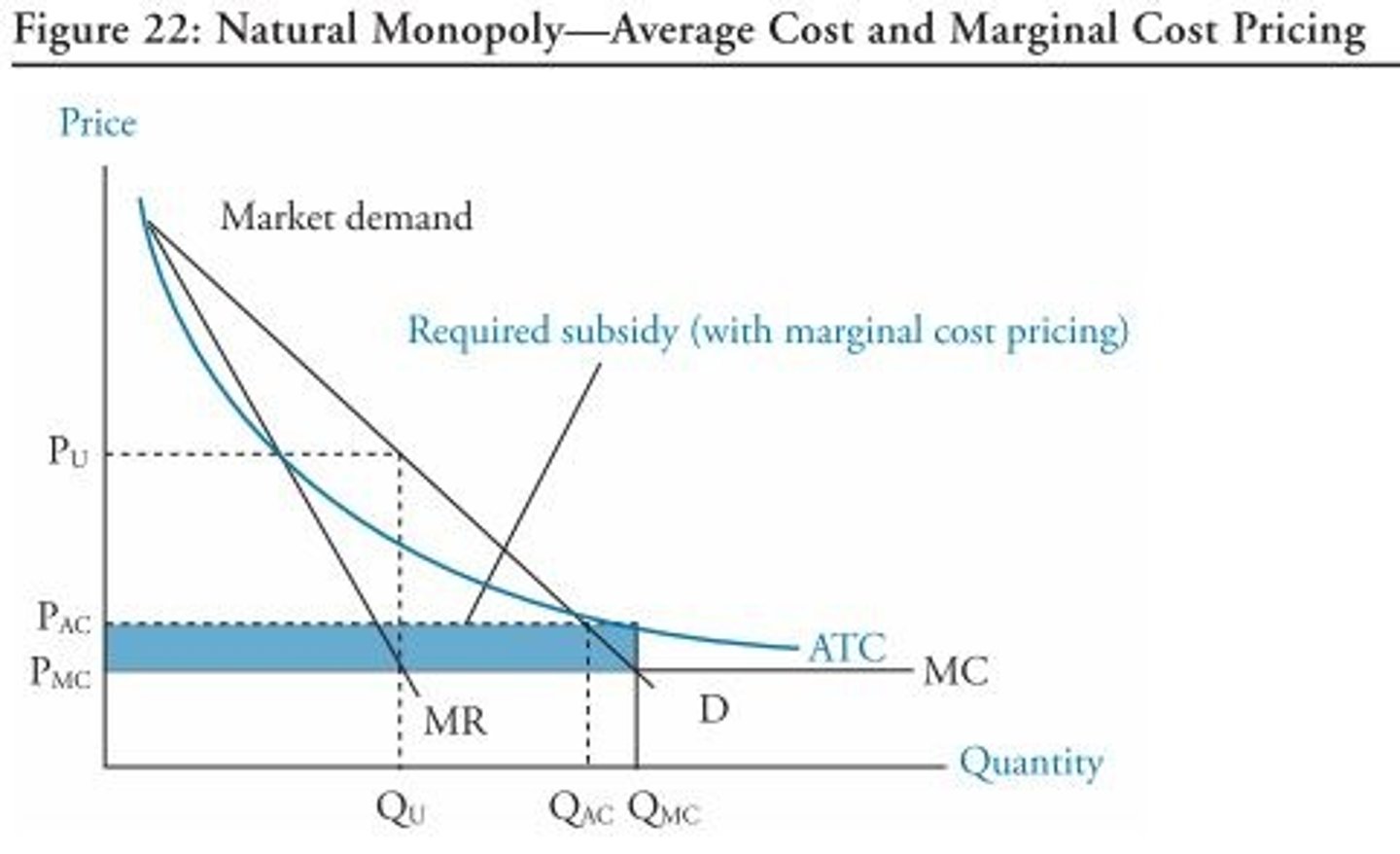

Natural Monopoly

Single sellers (Monopoly) that experience large economies of scale

Marginal cost pricing

P = MC

- The government regulates pricing by making the Natural Monopolies Price = (to their) Marginal Cost

Marginal Cost Pricing Continued

P = MC

Price Ceiling that is meant to eliminate Deadweight Loss

Average Cost Pricing

P = AC

Average cost pricing forces monopolists to reduce prices to where the firm's average total cost (ATC) intersects the market demand curve.

- Firms will make a Normal Profit and not Economic Losses

Short Run vs Long Run

...

Short Run for Monopolies

1. Eco Profit (P > ATC)

2. Break even (P = ATC)

3. Eco Loss (P < ATC)

Long Run for Monopolies (2 outcomes)

1. Eco Profit (P > LRAC)

2. 'Normal Profit' or 'Break Even' (P = LRAC and TR = TC)

Perfectly Competitive vs. Monopoly (key takeaways)

1. Many sellers (PC) with no control of the market vs One Seller (Monopoly) that dictates the price and the supply of goods and services

2. PC has no barriers to entry or exit, while Monopolies have many barriers to entry and exit

3. PC firms are 'Price Takers' while Monopolies are 'Price Makers' or 'Price Setters'

Monopoly vs. Monopolistic Competition (key takeaways)

1. Single firm (Monopoly) vs. Large number of firms (Monopolistic Competition)

2. Produce 'unique' products with no close substitutes (Monopoly) vs. produce products that are differentiated

3. Price 'maker' or 'price setter' (Monopoly) vs. 'Price searchers' - Some Control (Monopolistic Competition)

4. Barriers to entry (Monopoly) vs. Ease to enter and exit (Monopolistic Competition)

Antitrust Laws

...

1890 Sherman Act

Outlaws restraint of trade and monopolies

1914 Clayton Antitrust Act

Aims to promote fair competition and prevent unfair business practices that could harm consumers.

1. Horizontal Mergers

2. Price Discrimination

3. Tying Sales

1914 FTC Act

Created the Federal Trade Commission

1938 Wheeler-Lea Act

To prevent misleading and false deceptive advertising

1950 Cellar-Kefauver Act

Meant to prevent mergers and acquisitions that could reduce competition or create monopolies

1. Anti-merger act

2. Only merge if it lessens competition

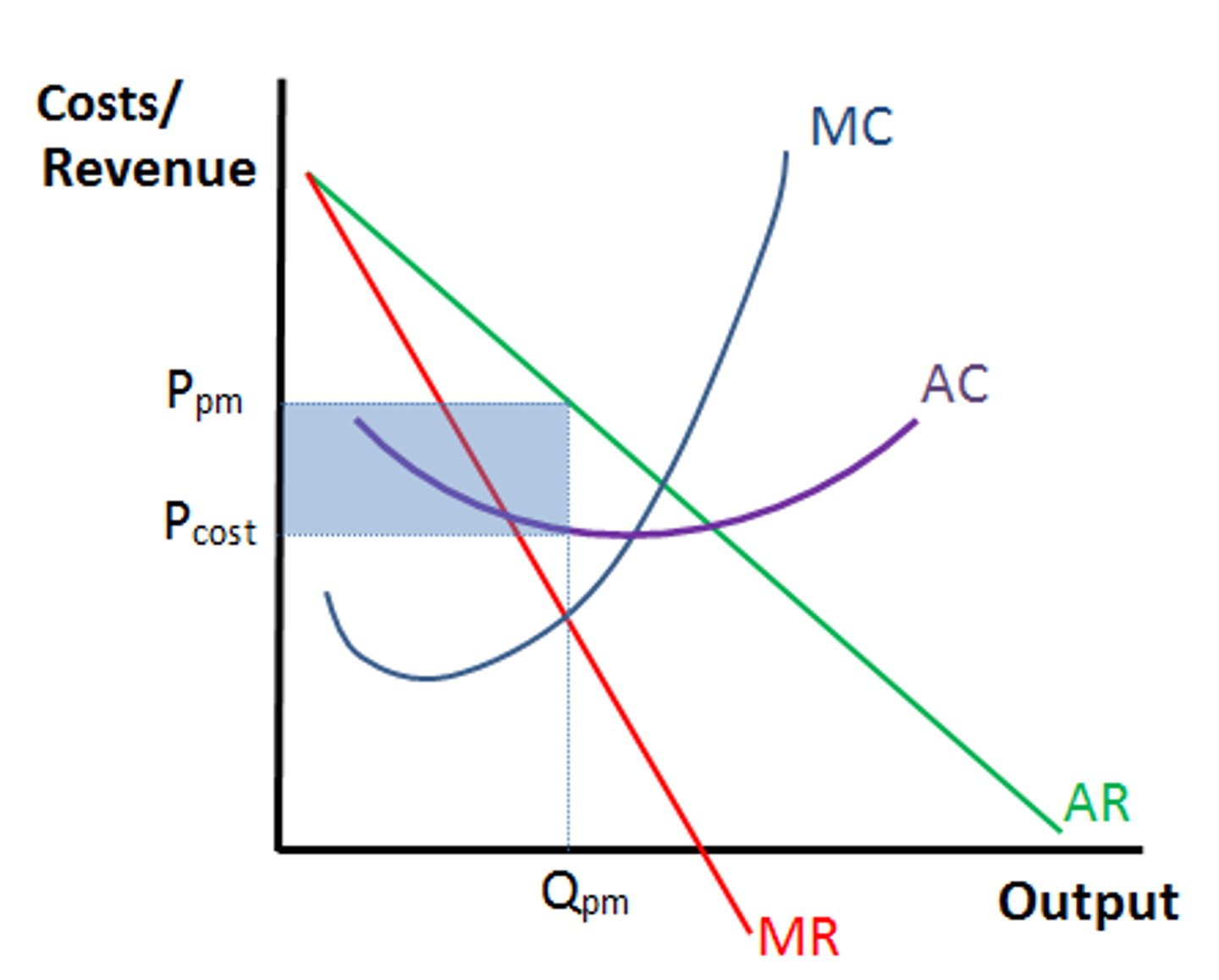

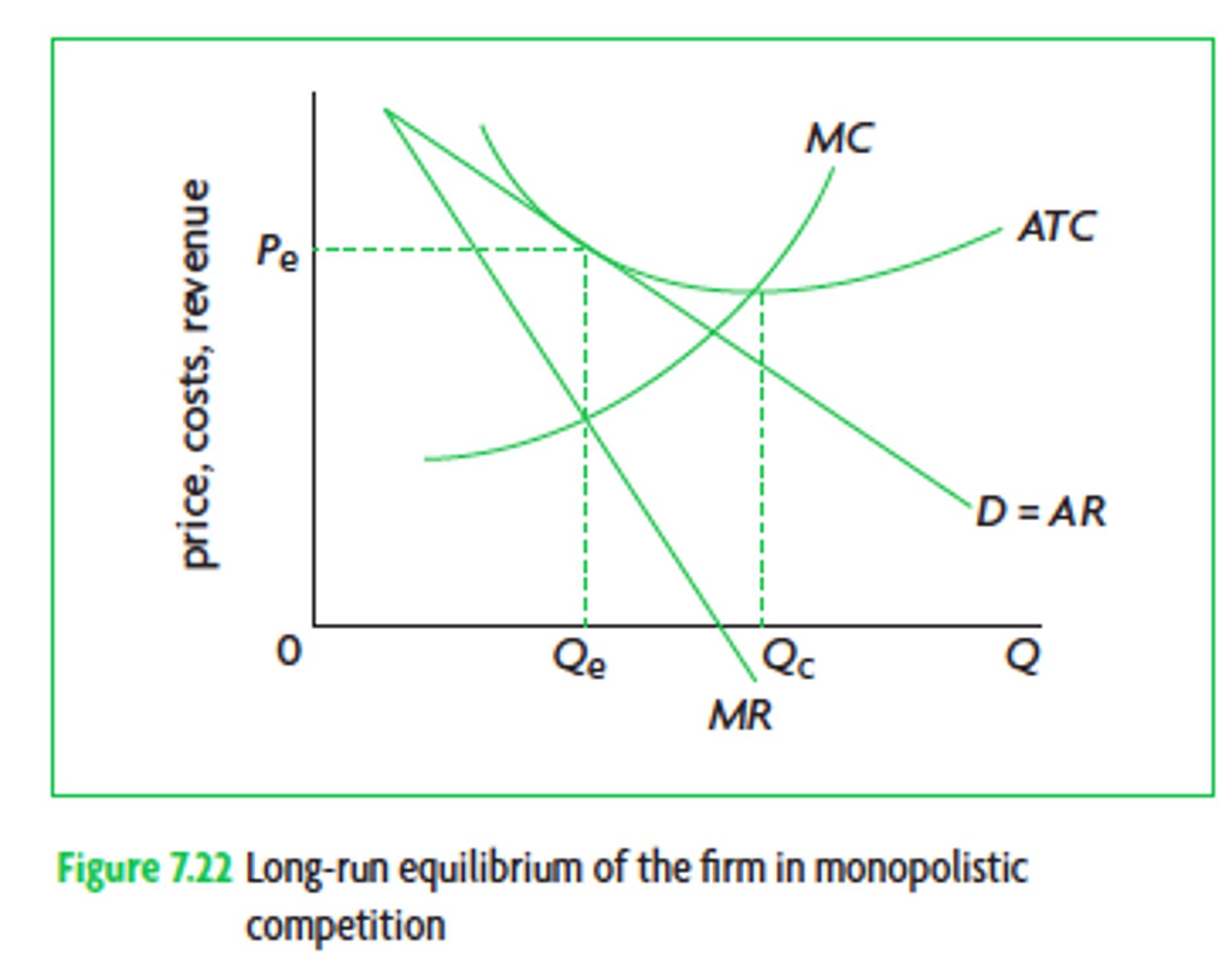

Monopolistic Competition

Relatively smaller firms - they're not all the same size

I. Structure (Monopolistic Competition)

1. Large Number of Firms

*2. The product they're producing is differentiated

3. Price Searchers (Some control over the price)

4. Ease to enter and exit the market

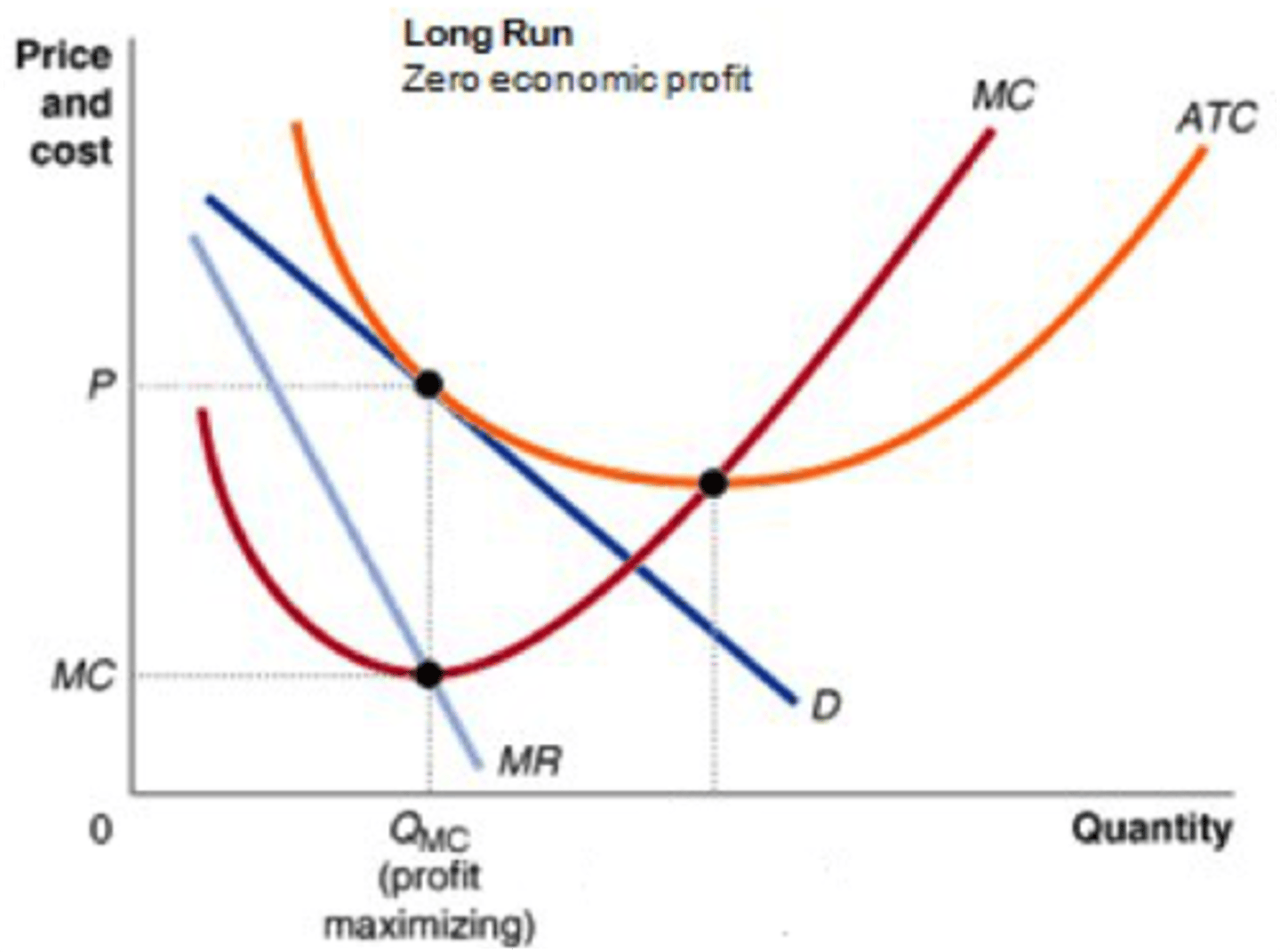

Long Run Equilibrium in Monopolistic Competition

1. NO ECONOMIC PROFIT IN THE LONG RUN!

2. Price is equal to the average total cost at an output below where the average total cost is minimized

Efficiency (Monopolistic Competition)

1. Not Resource-Allocative efficient

2. Not Productive-Efficient

Advertising (Informative Advertising and Persuasive Advertising)

1. D⬆to cause an increase in sales

2. Change the elasticity of demand for consumers

Examples of Informative Advertising...

A beer company selling a light beer might create an ad outlining how the carbs and calories of their light beer compared to a major competitor with a similar product

Examples of Persuasive Advertising...

A Brand's Celebrity Endorsement. ✏️ Ad Copy: "Drive with confidence like [Celebrity Name]. Experience unparalleled performance and luxury in the all-new [Car Model]."

Examples of Monopolistic Competition

Smartphone companies:

- Apple and Samsung

Soft Drink

- Coca-Cola and Pepsi

Taxi

- Uber and Ola

Compared to Perfect Competition...

1. Many relatively small firms (Perfect Competition) vs. Large number of firms (Monopolistic Competition)

2. Product is Homogeneous (Perfect Competition) vs. Product is Differentiated (Monopolistic Competition)

3. Price Takers (Perfect Competition) vs. Price Searchers (Monopolistic Competition)

4. No barriers to entry and exit (Perfect Competition) vs. Ease of entry and exit (Monopolistic Competition)

Compared to a Monopoly...

1. Single Firm, the single seller (the firm is the industry - Monopoly) vs. Large number of firms (Monopolistic Competition)

2. Produce 'unique' products with no closer substitutes (Monopoly) vs. Product is Differentiated (Monopolistic Competition)

3. Price 'makers' or 'price setters' (Monopoly) vs. Price Searchers (Monopolistic Competition)

4. Barriers to entry, both Legal (government-instated) and Economic (ownership of resources and if firms experience Large Economies of Scale) vs. Ease of entry and exit with low barriers (Monopolistic Competition)

Oligopoly

A market structure in which a few large firms dominate a market

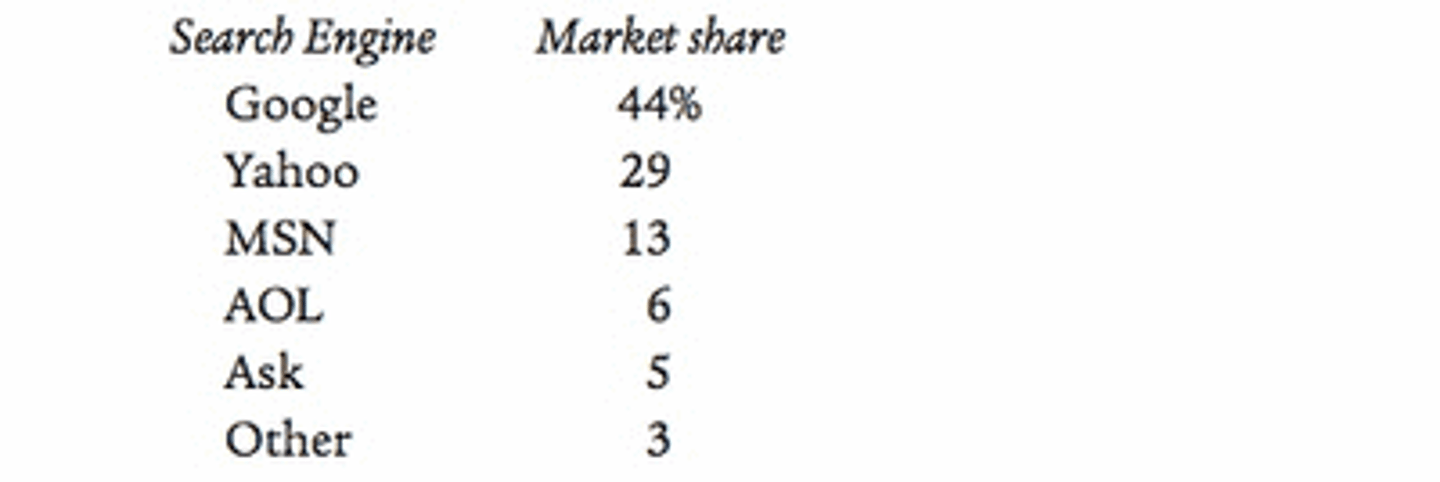

Real-world examples of Oligopoly's

The airline industry

- With companies like United, Southwest, Delta, and American Airlines all holding 55%+ of the airline industry market share

Smartphones

- Verizon, Sprint, AT&T, and T-Mobile all represent the smartphone industry, owning large market shares of the industry

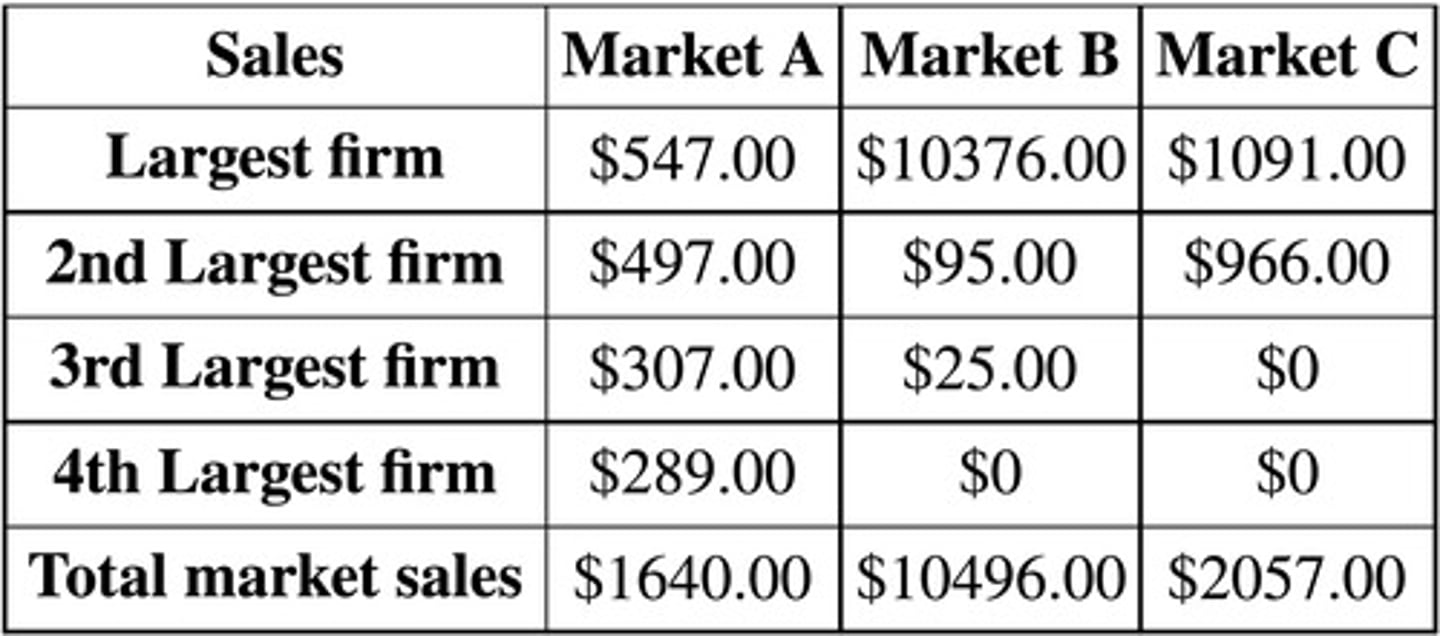

Concentration Ratio

Calculated by adding the market share percentages of the largest firms in an industry.

- It is used to assess the strength of a market over time and to indicate the degree of competition in an industry.

Cartel

A formal organization of producers that agree to coordinate prices and production

- They collude and set prices, production, or other business practices to achieve higher profits than they would under perfect competition.

Mergers

...

Conglomerate Mergers

Mergers between firms in completely different industries

Horizontal Mergers

Mergers between firms in the same industry

Vertical Mergers

Mergers between firms at different stages of the production process

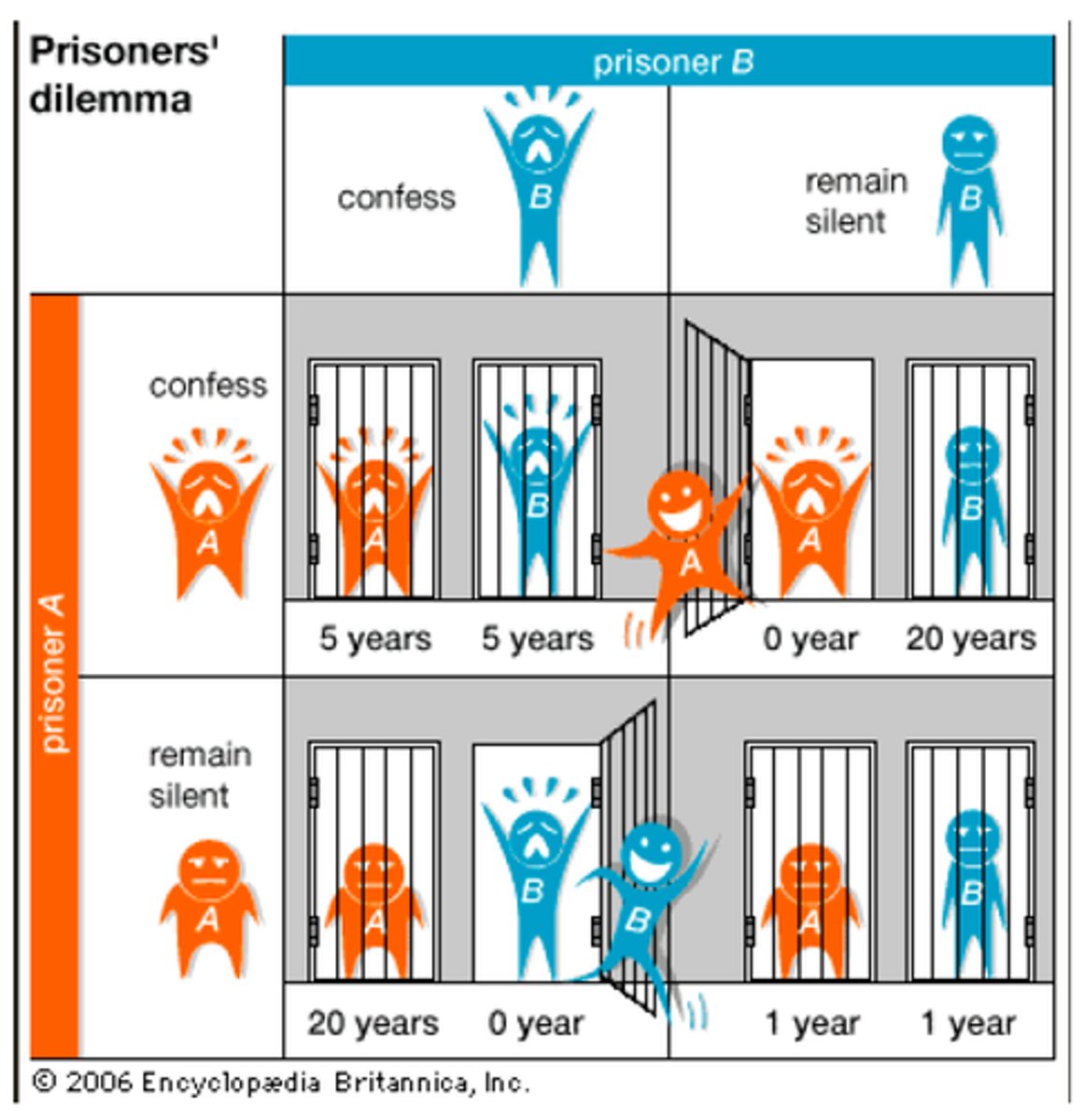

Game Theory

A theoretical framework for conceiving social situations among competing players

- Ex. Prisoner's Dilemma, Game show in class with Mr. Waltman

Herfindahl Index (HHI)

The sum of the squared percentage market shares of all firms in the industry