6. The Modern view of Money and the Banking System

1/16

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

17 Terms

What are the three types of money in a modern banking system?

Each represents an IOU from one sector of the economy to another

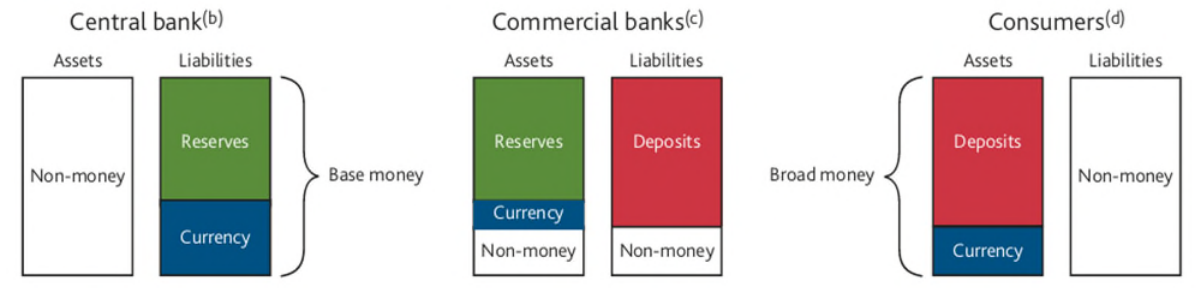

Bank deposits: Represent the money that a bank owes to a consumer or client (broad money)

Central Bank Reserves: An IOU from the Central Bank to a commercial bank (including high-street banks like HSBC, Natwest) (base money)

Currency (notes and coins): An IOU from the Central Bank, mainly to private sectors and companies, jointly called ‘consumers’

What do the balance sheets for the three types of money holders in the economy look like?

What are deposit accounts?

Current accounts or savings accounts which are typically electronic today

Depositing coins into a commercial bank is basically swapping the type of IOU a consumer has

Deposits are a medium of exchange and are a store of value

Assets of consumers and liabilities of commercial banks

What are reserves?

BoE reserves are an electronic record of how much the Central Bank owes to other commercial banks

Converts reserves into cash, which commercial banks then use to meet withdrawals from deposit accounts

Reserves are a medium of exchange which adjust everyday when banks settle accounts with each other

Reserves are assets of commercial banks and liabilities of the Central Bank

Base money

Also known as monetary base or narrow money

Used to be called M0: data for this ceased in 2006

Notes and coins as well as reserves at the Central Bank comprise the two components which make up base money

The ability of the Central Bank to dictate monetary policy stems from the fact they’re the sole issuer of base money

What is broad money?

Consists of notes, coins, and deposits held at commercial banks

The headline broad money measure is M4ex which excludes deposits of IOFC’s (Intermediate other financial corporations like bank holding companies)

Useful because it is held by those who decide spending decisions in the economy

Broad money is proportional to nominal expenditure

What is the quantity relation?

The relationship between broad money and nominal expenditure

Nominal expenditure = Nominal GDP = Price level x Real GDP

Monetarists emphasise the link between broad money, M, and nominal GDP, PY

There is a version of our basic Mv = PY which replaces real GDP Y with number of transactions T

v is the money velocity, how many times the money circulates through agents in the economy in a year must be equal to the money spent on goods in a year

Reserve requirements vs Liquidity Requirements

Reserves can be prudential because they’re highly liquid and can be sold to meet withdrawals

Some banks just have liquidity requirements because reserves aren’t the only liquid asset

The Bank of England has a 0% RRR, but banks do have to meet the LCR (Liquidity Coverage Ratio); effectively making explicit that a bank must have liquidity requirements but not reserve requirements

What qualifies as liquid assets?

The Financial Conduct Authority (FCA) in England treats notes and coins, short term deposits, UK government bonds, and some UK and foreign market funds as High Quality Liquid Assets (HQLA)

The Bank of England then accepts other assets on different levels as collateral for providing liquidity

Level A are assets expected to be liquid in most market conditions like high-quality sovereign debt

Level B are assets which are normally liquid like sovereign debt, private sector debt, and high-quality asset-backed securities

Level C are typically less liquid assets like securities and loan portfolios like mortgages

What are capital adequacy requirements?

This is a buffer to mitigate the risk of a bank being unable to provide liquidity

The two requirements are that a bank must have stable funding and must have a sufficient liquidity buffer

These are requirements of Microprudential Regulation, administered by the Prudential Regulation Authority (PRA) which has been part of the BoE since 2017

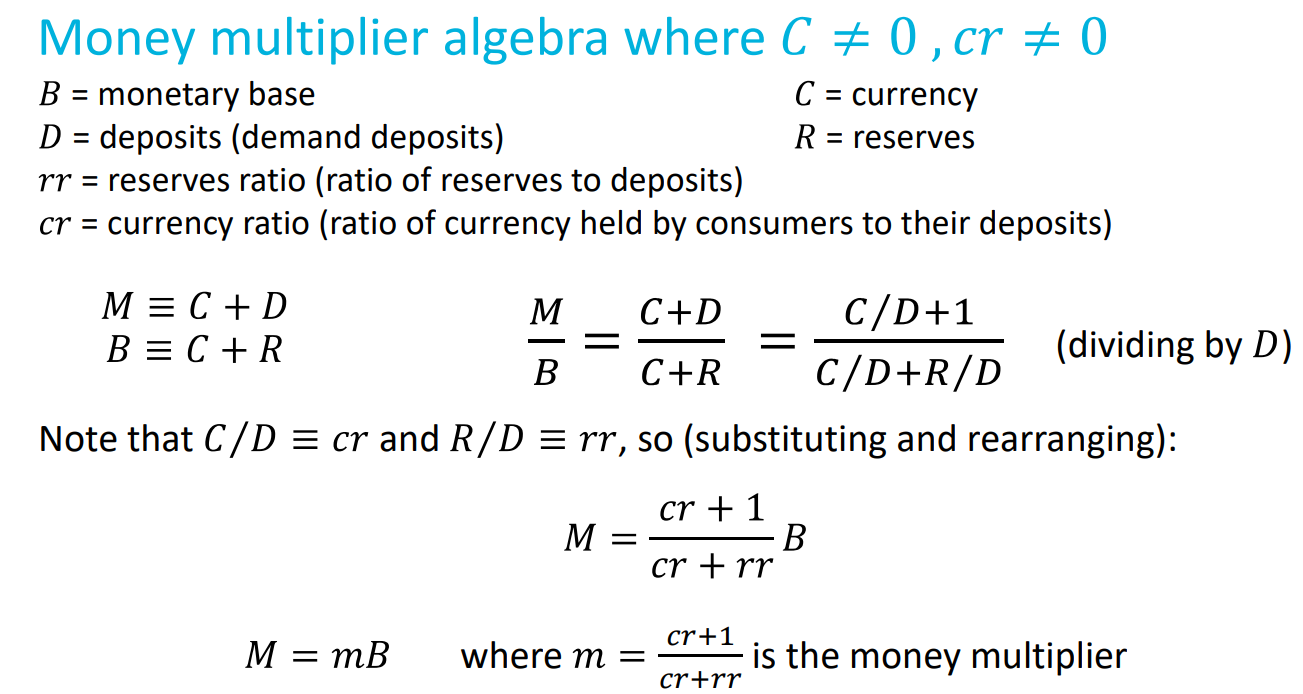

What is the money multiplier?

The ratio of broad money to base money: m = M/B

Broad money is deposits plus cash: M = D + C

Base money is reserves plus cash: B = R + C

The traditional model of the money multiplier

The traditional view implies that monetary base can mainly control inflation, which is central to monetarist economists

Is now held to be invalid by most economists and bankers

The algebra remains fine, but modern beliefs about its assumptions (key parameters are exogenous, like reserve ratio and currency ratio) are doubted

Money Multiplier Algebra and problems

rr = R/D is not exogenous as the model assumes, Central Banks provide R on demand from commercial banks and don’t restrict quantity but instead set the interest rate on it

R responds to D, not the other way around

The problem is that deposits are a source of funds for commercial banks but aren’t the only way they can source money to lend; lending isn’t based on deposits (they can actively attract deposits from other banks, lend in interbank markets etc)

What does the modern money creation view say about commercial banks as intermediaries?

Commercial banks are not just intermediaries in the money market, instead, they are active participants in it

Deposits don’t affect the amount a bank can lend because by making a deposit the aggregate of deposits hasn’t changed, it is just its location (depositing at one bank just means the money isn’t deposited at another bank or a private institution)

Commercial banks make money by choosing to lend according to their demand for loans and profit decisions which are affected by Central Bank policy

How do commercial banks make money?

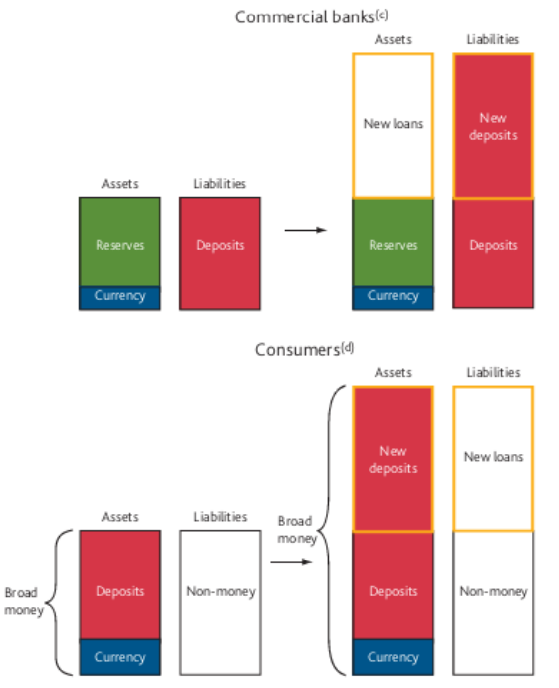

Commercial banks create new deposits any time they loan; by loaning to a consumer, the commercial bank creates a deposit in the borrowers account

Commercial banks create a lot more money than the Central Bank does

In the modern economy most money is in the form of bank deposits made by lending rather than saving existing funds

Balance sheets of commercial banks and consumers before and after making new deposits

The diagram illustrates that rr isn’t exogenous, isn’t constant, isn’t controlled by the central bank, and rr is endogenous regarding the fact that D will vary with the private sector’s willingness to borrow and the bank’s willingness to lend

rr is the ratio between R and D, the green rectangle and the red rectangle