Lecture 8 - Different Allais paradox explanations

1/22

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

23 Terms

models / approaches to explain “Allais paradoxes”

“Maximise something else”

e.g. Cumulative Prospect theory

“Maximise with error”

e.g. “Fechnerian error” model

“Not maximising”

e.g. Salience theory

CCE & CRE features

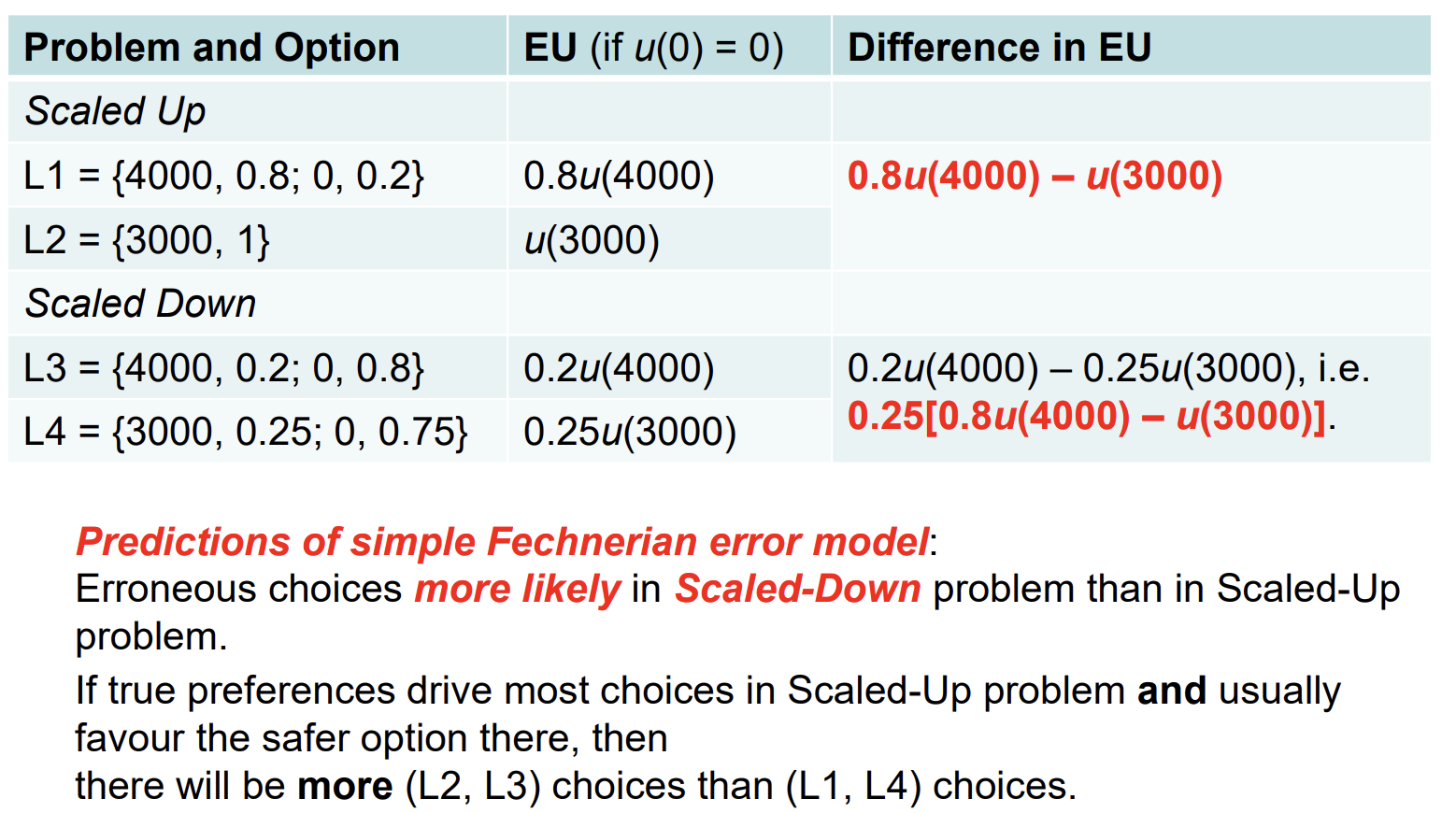

Switch from safer option → riskier option when the same problem is made ‘less attractive’

Violates EUT

Can be riskier in more attractive → safer in less BUT uncommon

how CRE could be random error

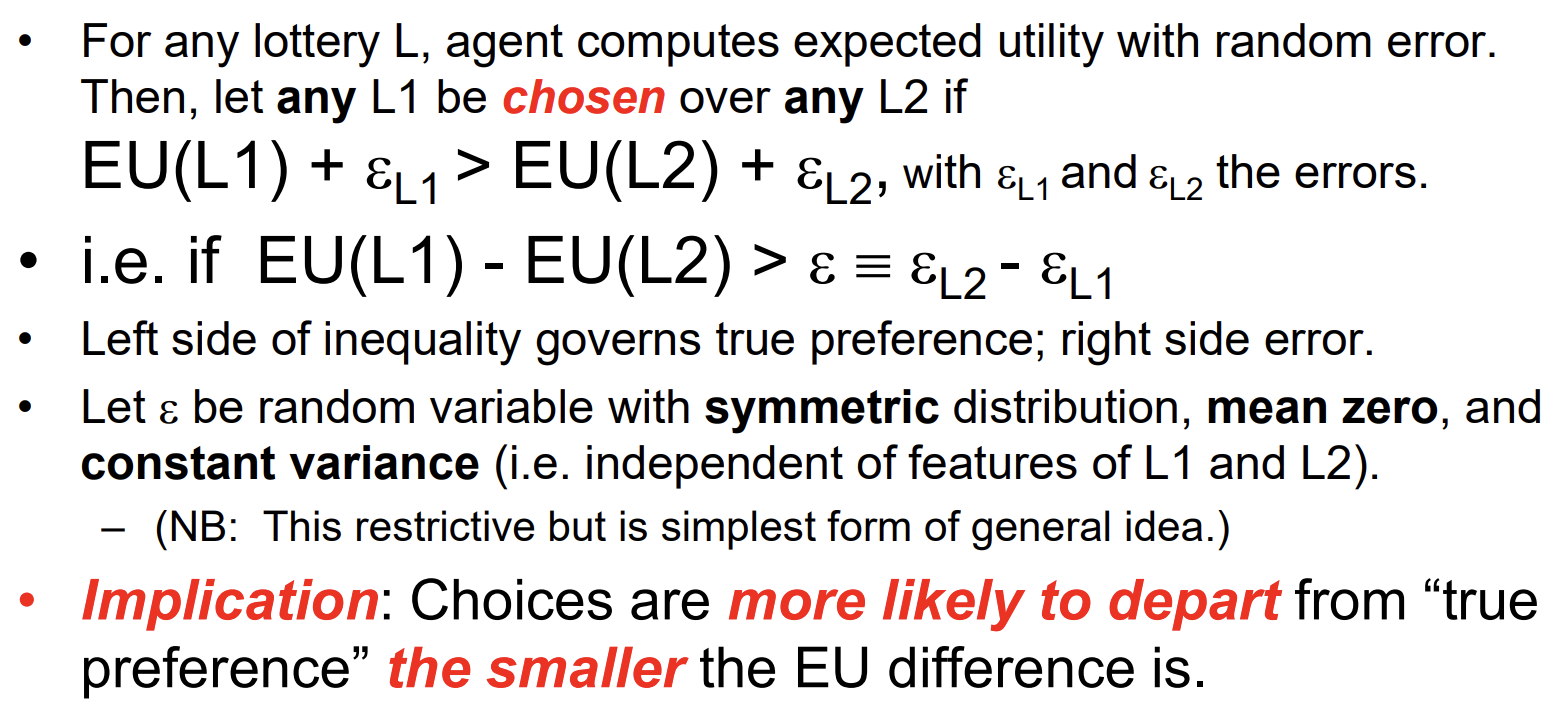

Agents have “true preferences” described by EUT BUT make “white noise” errors in “computing” EU

They then choose actions that maximise “computed EU

Simple Fechnerian error model

Choose L1 so long as true value of 1 not overridden by computation errors

errors random & constant variance so dont favour either choice or depend on the lotteries (big assumption)

Fechnerian error model & CRE

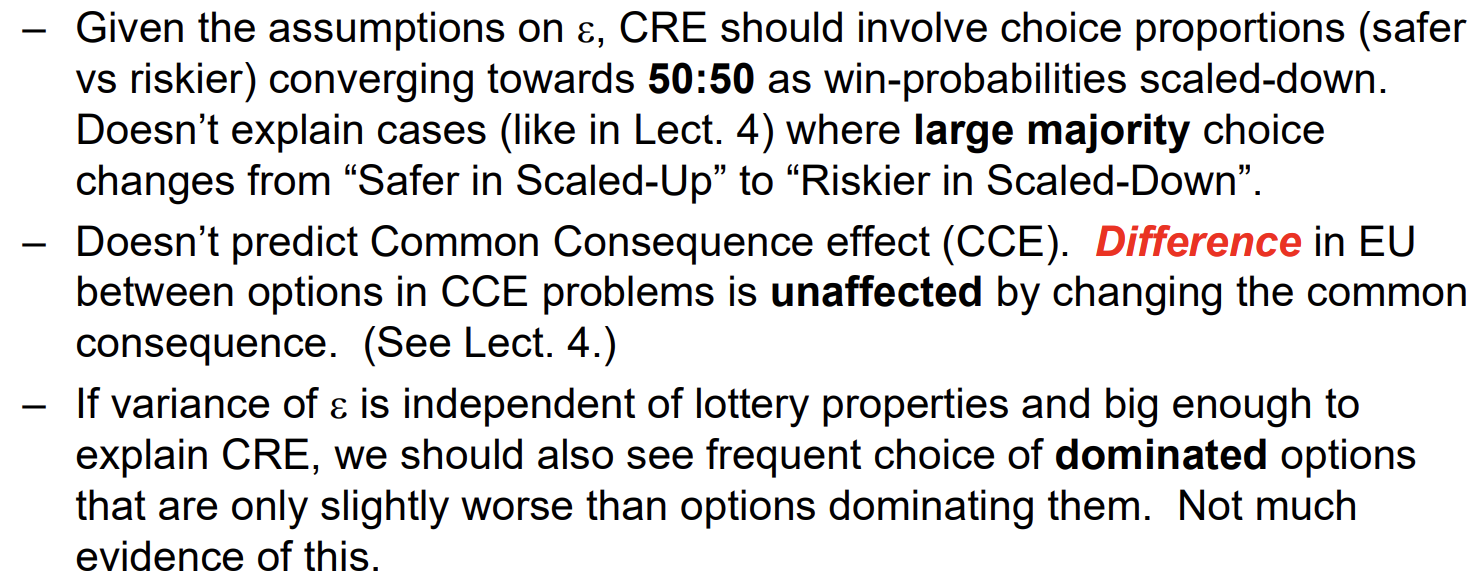

Problems for Fecnerian model

Errors symmetric so choice should converge towards 50/50 not swap in large amounts

Same EU difference for both choices in CCE so cant explain CCE

Predicts more violations of dominance than seen in reality

Problems might be avoided by more complex Fechnerian error model where stochastic properties of errors depend on characteristics of lotteries in “appropriate” way

Are CRE & CCE correlated or independent

Are processes that resolve uncertainty in the less attractive problem correlated

- No difference in EUT or prospect theory

- Now relevant for Salience theory

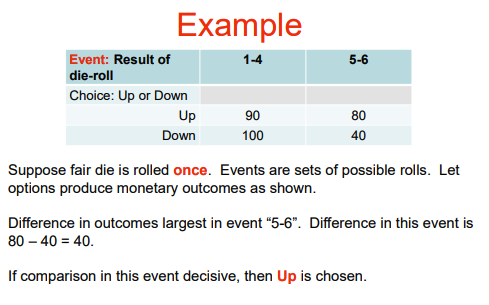

event

A possible resolution of uncertainty

Choices made by comparing available options in different events

Salience theory for risk

Decision-weights now attach to events

People are influenced by events where outcomes differ a lot

Ceteris Paribus, larger the difference is, larger decision weight on event

For simplicity, we approximate this by assuming choice between options fully determined by comparing them in the event where they differ most

Relative to prob we overweight event where outcome changes most

Implication - Available options can’t be evaluated in isolation from one another

Salience theory example

Choose event with largest difference - Pick the one with highest outcome

Attention based theory of salience theory

Decision-maker has limited attention.

Agent drawn (or allocated) to events where choice between options matters most

largest difference draws our attention

Regret based salience theory

Regret arises from comparison of chosen action and what might have been if agent had chosen differently

Decision-makers very averse to large regrets, so act to prevent them them

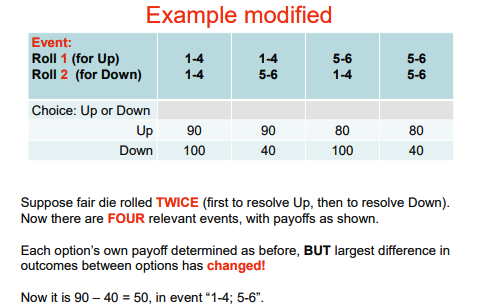

Modified salience theory example

How do simple vs modified salience theory examples differ

Original:

One roll resolves both options - options stochastically-dependent

Outcomes correlated - each option gives its highest payoff in same event, “1-4”

Modified:

Two independent rolls resolve the options, one for each option - options stochastically-independent

Outcomes uncorrelated

e.g. there is an event (“1-4; 5-6”) with best outcome of Up but worst outcome of Down

Under Salience theory, this event has a lot of weight

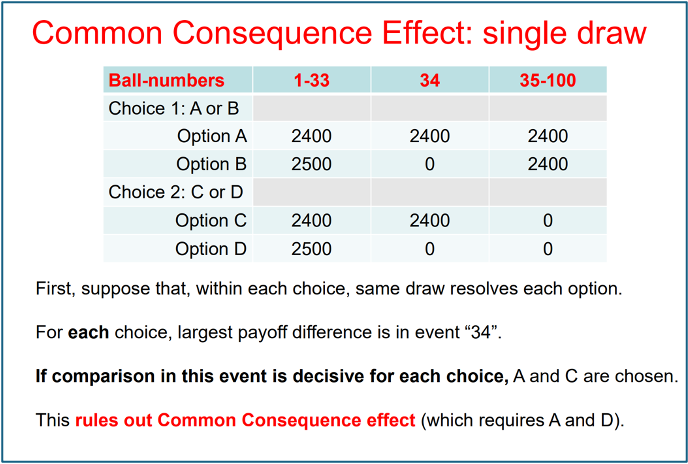

Salience theory & CCE example

CCE would choose A & D (35-100 common outcome)

CCE & salience theory

CCE can occur in Salience theory if risks in options of each problem stochastically independent

i.e. resolved by different draws

CCE will not occur if risks in the options stochastically dependent

i.e. resolved by same draw

CRE follows similar pattern of only appearing if event resolved by different draws

stochastically independence effects on CCE

Compared with stochastic-dependence, stochastic independence:

Makes no difference to the more attractive choice problem provided safer option is a certainty

BUT changes less attractive choice problem by “creating” event where agent “lucky in riskier option, but unlucky in safer one”

This event has large payoff-difference!

If comparison in this event decisive, riskier option chosen in less attractive problem

in line with direction of CCE

CPT vs ST & lotteries

CPT - Decision-weighting driven by probabilities (and rank-order of consequences) within each lottery

ST - Decision-weighting driven by comparisons of consequences across available lotteries

Implication: How lotteries resolved can discriminate between prospect theoretic and salience theoretic accounts.

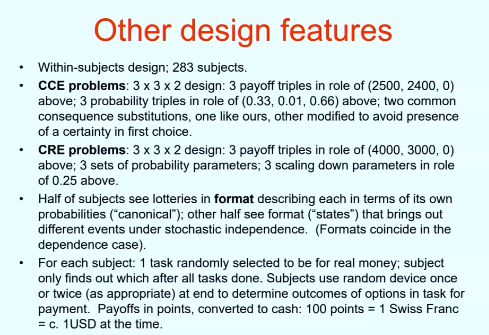

Bruhin et al (2022) - OV

Each subject faces two blocks of choices:

one with choices between stochastically-independent lotteries;

one with corresponding choices between stochastically-dependent lotteries.

Order of blocks and order of tasks in blocks randomised by subject, to avoid order effects

Bruhin et al (2022) - Predictions

Predictions differ between model used

EUT: Subjects will not display CCE or CRE forms of Allais paradox

Cumulative Prospect theory: Subjects may display Allais Paradox behaviours but will be equally prone to this regardless of whether lotteries stochastically dependent or independent

Salience theory: Subjects may display Allais Paradox behaviours but only when lotteries stochastically independent.

Bruhin et al (2022) - Design

½ see ‘states’ which makes stochastic independence very obvious

‘canonical makes it less obvious’

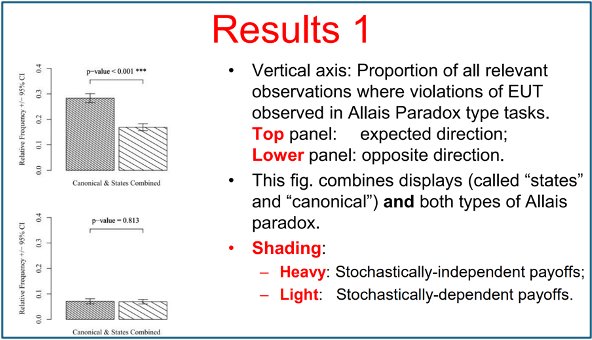

Bruhin et al (2022) - Results aggregated

Aggregates across CRE & CCE

Shows EUT violated but NOT always

EUT violations in expected direction more frequent

EUT violations more frequent when payoffs random/independent - as salience theory predicts

Violations also present in stochastically-dependent payoffs case (no ST but CPT predicts it)

Gap between indep/dep in top diagram shows effect that ST predicts that CPT doesnt - CPT also valid as Allais paradox shown

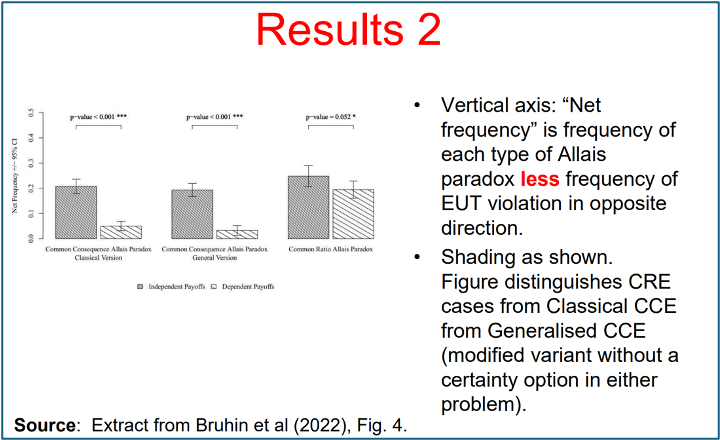

Bruhin et al (2022) - Results individual

Expected direction of EUT violation dominates opposite

especially for stochastically independent payoffs

Dep vs Indep matters more for CCE than CRE

direction of effect predicted by ST

CRE still seen when ST doesnt predict it (CPT present)

Further study ascribed which theory fits best to an individual

EUT, ST or CPT

Roughly all equal at 1/3