Chapter 14 Problems

1/23

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

24 Terms

14-1: Ricardo and Sue are married and file a joint return for 2025 with regular taxable income of $90,000 and tax preferences and adjustments of $12,000.

Calculate their AMT.

$0

14-1: Ricardo and Sue are married and file a joint return for 2025 with regular taxable income of $90,000 and tax preferences and adjustments of $12,000.

14-2: Assume the same facts for Ricardo and Sue as in EX 14-1, except they have tax preferences and adjustments of $90,000.

Calculate their TMT. Do Ricardo and Sue need to pay for the TMT or the regular tax?

TMT of $11,180

14-4: Rita, an unmarried taxpayer filing single, has regular taxable income of $550,000 in 2025, a regular tax liability of $162,047, a positive AMT adjustment (due to limitations on itemized deductions) of $60,000, and tax preferences of $65,000.

Calculate Rita’s AMT.

$909

14-5: Robin, age 45, is a single taxpayer with no dependents. She has AGI of $100,000 and the following itemized deductions for the current tax year:

charitable contributions - $4,000

medical expenses, net of insurance - $10,500

mortgage interest (100% qualified housing interest) - $18,400

real estate taxes - $4,000

state income taxes - $6,000

What would Robin’s regular taxable income would be?

$64,600

14-5: Robin, age 45, is a single taxpayer with no dependents. She has AGI of $100,000 and the following itemized deductions for the current tax year:

charitable contributions - $4,000

medical expenses, net of insurance - $10,500

mortgage interest (100% qualified housing interest) - $18,400

real estate taxes - $4,000

state income taxes - $6,000

From the information above, Robin’s regular taxable income would be:

AGI - $100,000

Minus: Itemized Deductions

charitable contributions - $4,000

medical expenses ($10,500 - Less 7.5% of AGI) - $3,000

mortgage interest - $18,400

real estate taxes $4,000

state income taxes - $6,000

==========================

Taxable income - $64,600

Assume that Robin also has $20,000 of tax preferences.

How much would her AMTI be?

$94,600

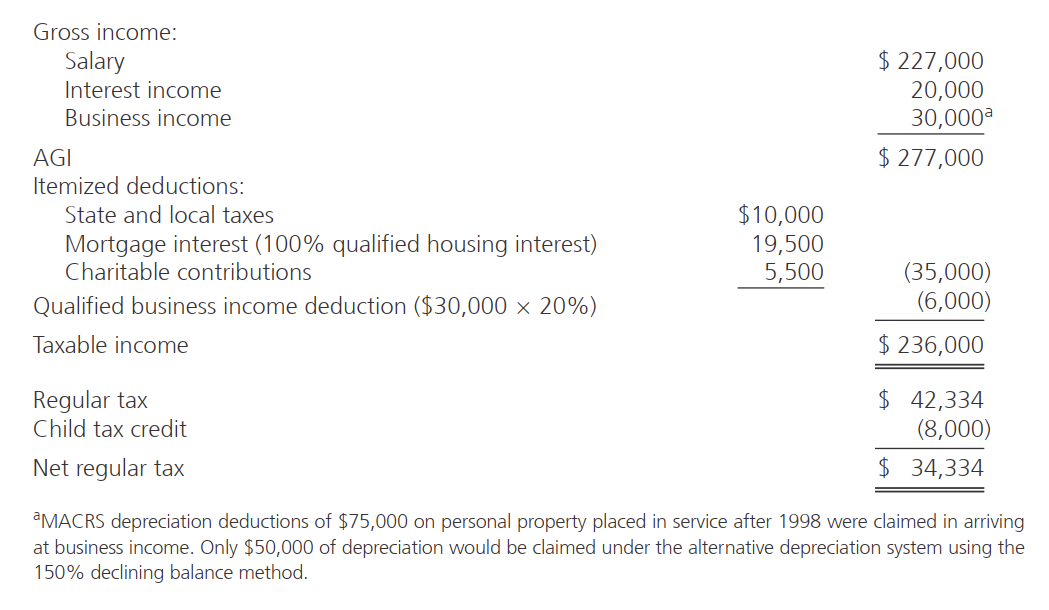

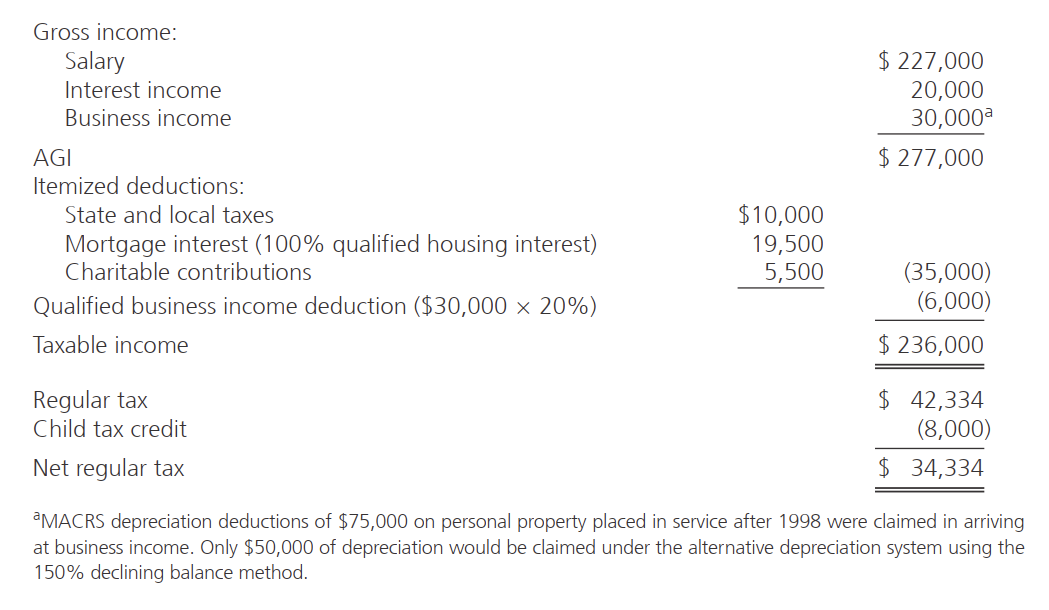

14-7: Roger and Kate are married, file a joint return, and have four dependent children. All of the children are under age 17. Assume that the couple has $30,000 of AMT preference items.

The image attached shows how regular taxable income was computed for 2025.

Compute AMT for Roger and Kate.

$306

14-7: Roger and Kate are married, file a joint return, and have four dependent children. All of the children are under age 17. Assume that the couple has $30,000 of AMT preference items.

The image attached shows how regular taxable income was computed for 2025.

What is the total tax liability for Roger and Kate?

$34,640

14-8: Robert, a cabinet maker, works as a sole proprietor. For 2025, his self-employment earnings totaled $75,000. His net earnings from SE equal $69,263 ($75,000 × 92.35%).

Calculate his SE tax.

$10,598

14-8: Robert, a cabinet maker, works as a sole proprietor. For 2025, his self-employment earnings totaled $75,000. His net earnings from SE equal $69,263 ($75,000 × 92.35%).

What is his SE tax deduction?

$5,299

14-8: Robert, a cabinet maker, works as a sole proprietor. For 2025, his self-employment earnings totaled $75,000. His net earnings from SE equal $69,263 ($75,000 × 92.35%).

14-9: The facts are identical to EX 14-8, except Robert’s self-employment earnings totaled $200,000. His net earnings from SE equal $184,700 ($200,000 × 92.35%).

Calculate his SE tax.

$27,192

14-8: Robert, a cabinet maker, works as a sole proprietor. For 2025, his self-employment earnings totaled $75,000. His net earnings from SE equal $69,263 ($75,000 × 92.35%).

14-9: The facts are identical to EX 14-8, except Robert’s self-employment earnings totaled $200,000. His net earnings from SE equal $184,700 ($200,000 × 92.35%).

What is his SE tax deduction?

$13,596

14-12: Henry, an unmarried taxpayer filing single for 2025, earns a salary of $180,000 plus SE income of $145,000 in consulting fees. His net earnings from SE is $133,908 ($145,000 × 92.35%).

How much will Henry pay for SE tax?

$3,883

14-12: Henry, an unmarried taxpayer filing single for 2025, earns a salary of $180,000 plus SE income of $145,000 in consulting fees. His net earnings from SE is $133,908 ($145,000 × 92.35%).

Does Henry need to pay for the Additional Medicare Tax? Why

Yes, because his earned income exceeds $200,000

14-12: Henry, an unmarried taxpayer filing single for 2025, earns a salary of $180,000 plus SE income of $145,000 in consulting fees. His net earnings from SE is $133,908 ($145,000 × 92.35%).

How much is Henry’s additional medicare tax?

$1,025

14-15: Tim and Tina are married and have two children under age 13. They incur child expenses (e.g., a housekeeper and nurse) to enable both Tim and Tina to work on a full-time basis.

Are these expenditures eligible for the child and dependent care credit?

Yes

14-15: Tim and Tina are married and have two children under age 13. They incur child expenses (e.g., a housekeeper and nurse) to enable both Tim and Tina to work on a full-time basis.

What if, alternatively, Tina was not employed?

Are these expenditures eligible for the child and dependent care credit if Tina were not employed?

No

14-18: Mark and Vicki are married, file a joint return, and have three children under age 13. Mark and Vicki’s employment-related earnings are $25,000 and $10,000, respectively. Including all sources of income, their AGI is $36,000. They incur $8,000 of child care expenses during the year.

Compute Mark and Vicki’s child and dependent care credit amount for this year.