1BO3 Finals Unit 9-12

1/118

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

119 Terms

Unit 9 Product Differentiation

Refers to the features of one firms product that make it different from the offerings of other firms

When products are differentiated, the output from different firms are not perfect substitutes

Sources

Actual or perceived difference in materials, quality, etc.

Brand name or reputation

Location and Convenience

Transaction costs, lock in, switching costs

Incomplete information

Unit 9 Monopolistic Competition

Monoply is a term we use for a firm that dominates a market.

Monopolistic competitive firms do face competiton, but they will dominate their own little segment of the market

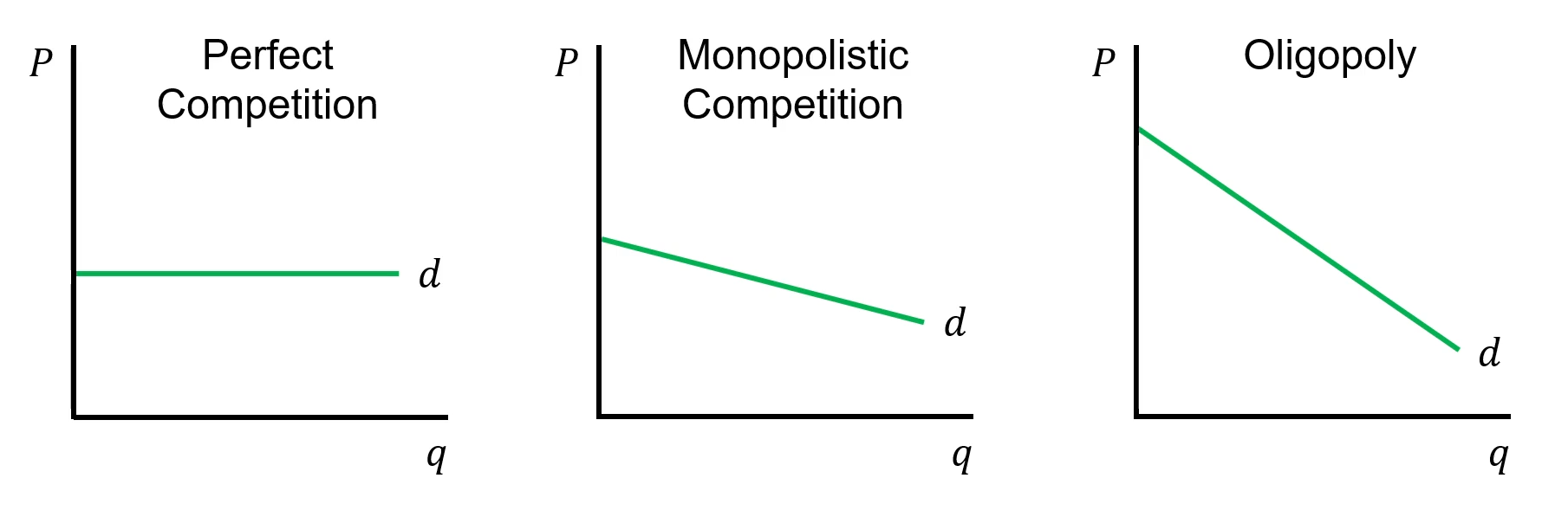

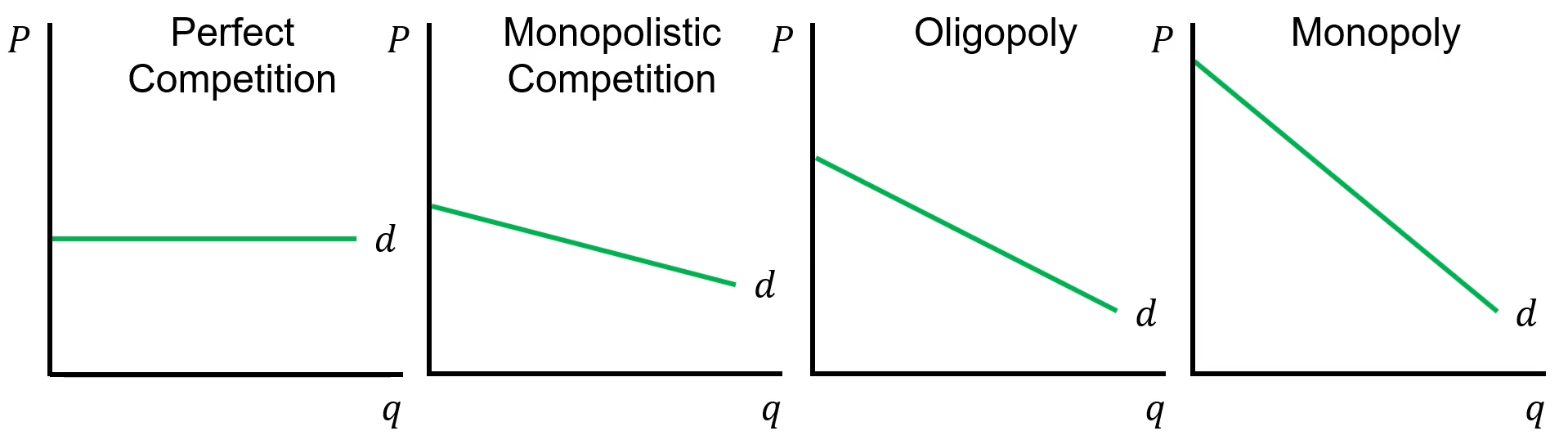

There are many buyers and each buyer is small relative to the overall market size, so they cannot affect the market price with their own actions

There are many sellers and each seller is small relative to the overall market size, but each produces a differentiated good. Sellers therefor have some control over the price they charge, and they can charge prices different from competitors

Firms can easily enter or exit market

MOST MARKETS ARE THIS KIND OF MARKET

Unit 9 Product Demand in Monopolistic Competiton

Monopolistically competitive firms product differentiated goods, so they appeal to different segments of the overall market and face downward sloping demand within their own segment or locale

Unit 9 Perfect Competiton vs Monopolistic Competiton

In perfect competition, firms are price takers, so marginal revenue equals market price (MR = P).

In monopolistic competition, firms face a downward-sloping demand curve, so marginal revenue is less than price (MR < P).

Unit 9 Marginal Revenue in Monopolistic Competiton

Because a monopolistically compettive firm has control over its price, we call it a price setter

To increase sales, it must lower its price

Marginal revenue is less than price

Marginal revenue is always less than the market price

For a linear demand curve, the slope of the marginal revenue curve will be exactly double the slope of the demand curveU

Unit 9 Marginal Revenue and Total Revenue

Because the price chanegs each time we change output, the marginal revenue per unit is less than the market price

Because P changes, total revenue is a non linear function: TR = Pq

Unit 9 Profit Maximization

Profit = TR - TC

When TR < TC, our profits are negative

When TR = TC, our firm breaks even

When TR > TC, our profits are positive

When profits are maximied, the total revenue curve and the total cost curve have the same slope

Therefor, when profits are maximized MR=MC

Unit 9 Monopolistic Competition Analyzing MR and MC

When MR > MC, revenues grow faster than costs and profits will increase

All units up to qMC will gain profit

When MR < MC, costs grow faster than revenues and profits will decrease

All units after qMC will lose profit

Profits reach their maximum point when MR = MC

Unit 9 Monopolisti Competition P and MC

For a monopolistically competitive firm

P > MC

The price consumers pay is higher than the marginal cost to make the good. We call this difference a markup price

Unit 9 Perfect Comp vs Monopolistic Comp RECAP

Perfect Competition

Firms sell homogenous goods so goods from different firms are perfect substitutes

Firms are price takers so price equals marginal revenue

Price equals marginal cost so there is no markup

Monopolistic Competition

Firms sell differentiated goods so goods from different firms are no perfect substitutes leading to customers may prefer one firm over another

Firms are price setters so price is greater than marginal revenue

Price is greater than marginal cost so consumer pay a price market

Unit 9 Price Elasticity and Marginal Revenue

When demand is elastic, lowering price increases total revenue.

When MR = 0, total revenue is at its maximum, demand is unit elastic.

When MR < 0, lowering price reduces total revenue, demand is inelastic.

Unit 9 MR and MC + Firms Operation

Marginal cost is always positive (MC > 0), meaning producing one more unit always adds some cost

Since firms maximize profit where MR = MC, marginal revenue must also be positive at the chosen output

Price-setting firms operate only where demand is elastic, because in the inelastic range MR is negative

The profit-maximizing quantity is lower than the revenue-maximizing quantity, since revenue is maximized where MR = 0 but profit requires MR = MC > 0

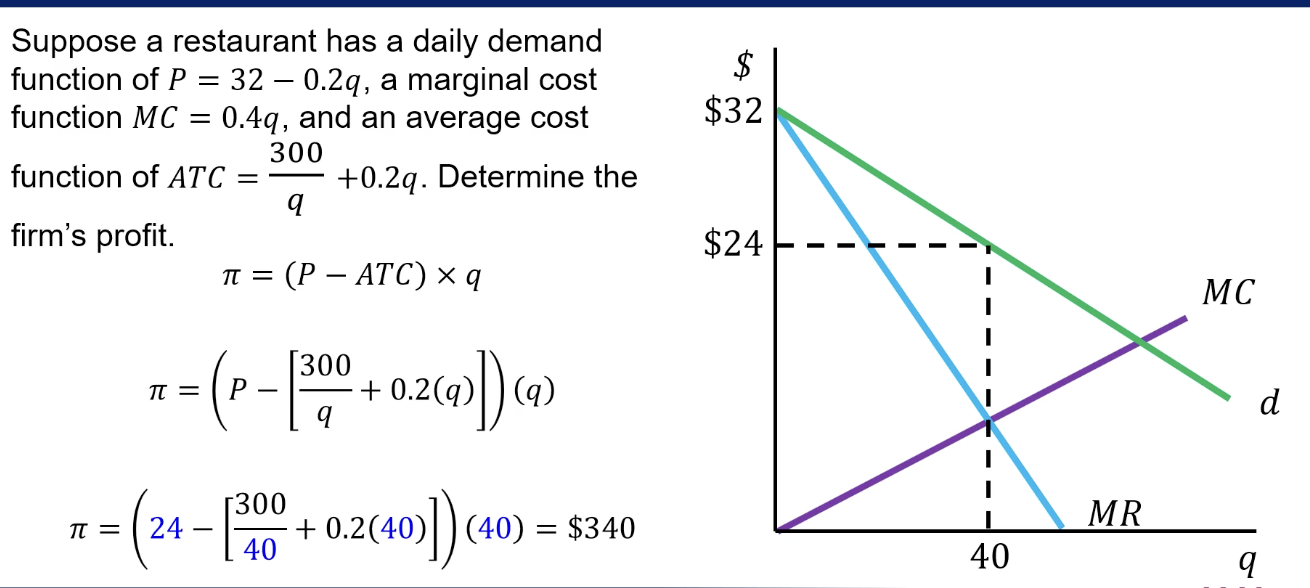

Unit 9 Price and Quantity in Monopolistic Competiton

Suppose restaurant has a daily demand function of P = 32 - 0.2q and a marginal cost function MC = 0.4q

Determine the profit maximizing quantity and price

Multiply the slope of demand curve by 2 for the MR curve

Set MR = MC then drag the line from that point up to the demand curve

Equate lines that intersected to find Q

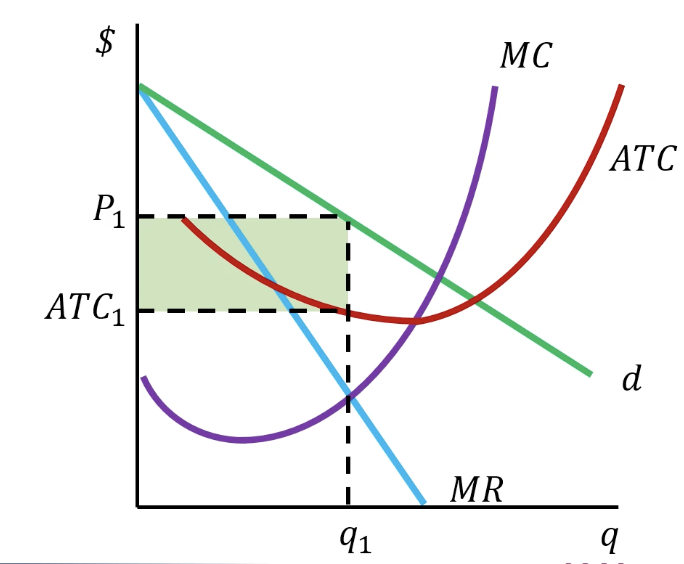

Unit 9 ATC and Profit

ATC reaches a minimum when its equal to MC

When P > ATC, the firm earns a profit per unit

Total profit is difference between production cost and price times q

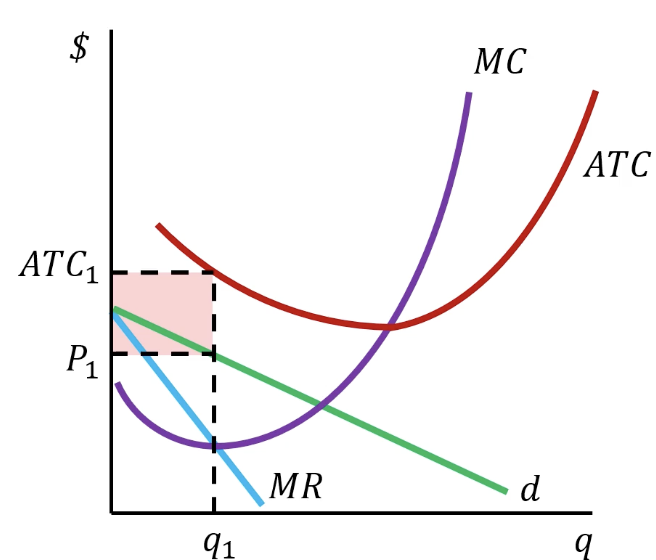

When P < ATC, the firm earns a loss per unit

qMC is the loss minimizing quantity

Unit 9 Short Run Losses

If a firm continues to operate it must pay fixed and variable costs, but it also receives some revenue

If a firm shuts down temporarily, its must pay fixed cost, but it has no variable costs or revenues

Therefor, if revenue > variable cost (there is a producer surplus) then total loss < fixed cost because the producer surplus covers some portion of the fixed cost, in this case the firm will operate

IF revenue < variable cost, total cost > fixed cost and the firm cannot pay its variable cost and must also pay the fixed cost as well, in this case the firm will shut down

Seen often and is why restaurants close for certain hours of the day

Unit 9 Profits in Monopolistic Competition

Suppose a restaurant has a daily demand function of P = 32 - 0.2q, a marginal cost function of MC = 0.4q and an average cost function of 300 over q. Determine the firms profit

Profit = (P-ATC) x q

Unit 9 Long Run Profits and Entry

Economic profits encourage new firms to enter

As new competition enters, demand for an existing firms output falls

Demand will fall until price equals average total cost

P = ATC

Unit 9 Long Run Losses and Exit

Economic losses encourage firms to exit the market

As competitors leave demand for a remaining firms output rises

Demand will rise until price equals average total cost

P = ATC

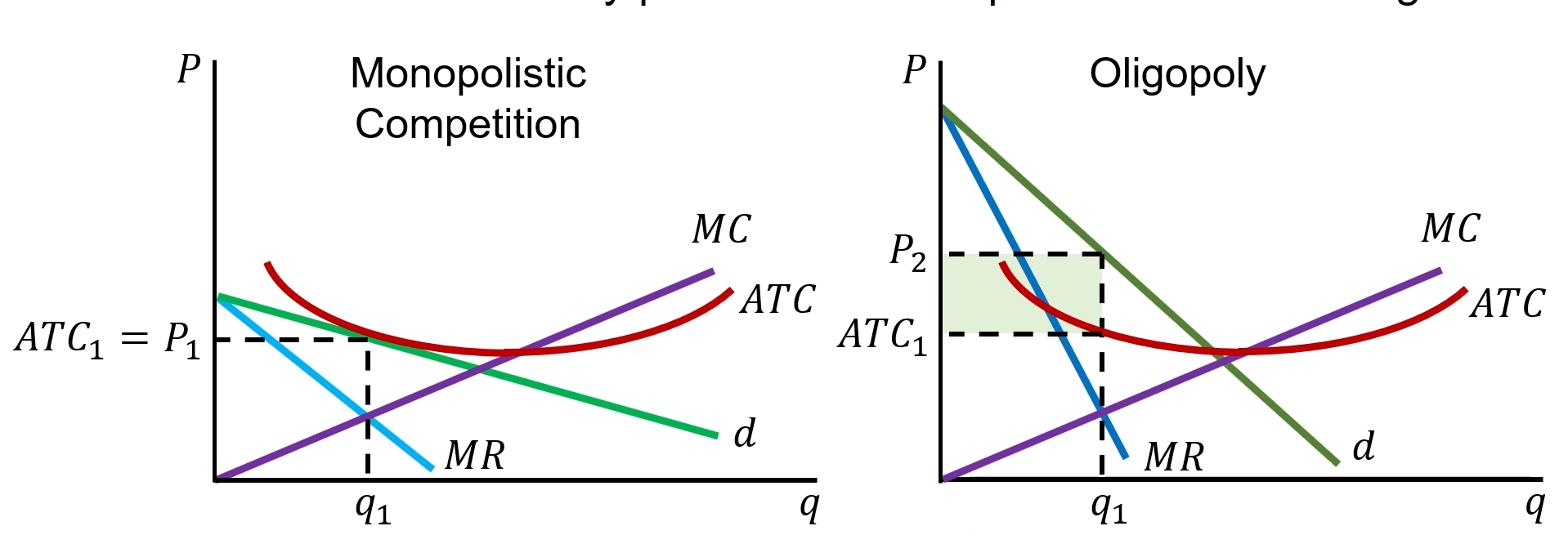

Unit 9 Monopolistic Competition in the Long Run

In the long run, P = ATC, meaning that capital is allocated efficiently

There is no benefit to either investing in or withdrawing from this industry because firms earn an accounting profit equal to investors risk adjusted expected rate or return (zero economic profit or normal profit

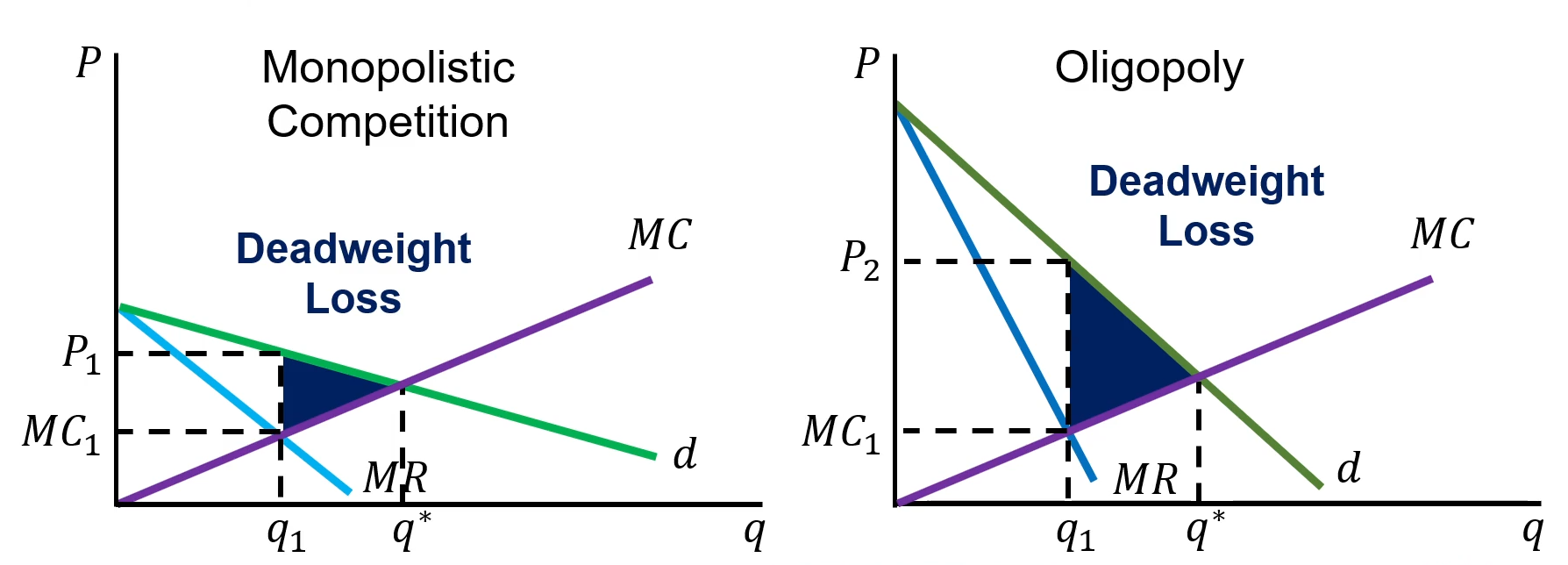

However, P > MC, therefore: ATC > MC. Under monopolistic competition, production is not efficient

Unit 9 Welfare Effects of Competition

With perfect competition, producers would charge a price equal to marginal cost

Because they face downward sloping marginal revenue, they charge a price greater than the marginal cost

The price is higher than it would be under perfect competition, while the quantity sold is lower

Consumer surplus is lower than under perfect competition

In the long run, producer surplus is the same as it would be in perfect competition

Since P = ATC (Producer Surplus = Total Fixed Cost)

Monopolistic Competition creates a deadweight loss, these markets are less efficient than perfectly competitive markets

Unit 10 Oligopoly

An oligopoly is a market with only a few dominant firms

Each firm has market power, meaning it faces a downward sloping demand curve

Barriers to entry limit or prevent new firms from entering the market

Unit 10 Homogenous and Differentiated

In a homogenous oligopoly, the firms product undifferentiated goods and only compete on price.

In a differentiated oligopoly, the firms produce differentiated goods and will compete on both price and quality

Unit 10 Duopoly

At the most extreme case, there are only two firms which is called a duopoly. Because there are only a few firms, each will have a large market share.

Unit 10 Barriers to Entry

A barrier to entry is any phenomenon that prevents new firms from entering. This includes:

Economies of Scale

Government Regulations

Limited Ownership of a resource

Operating history and brand recognition

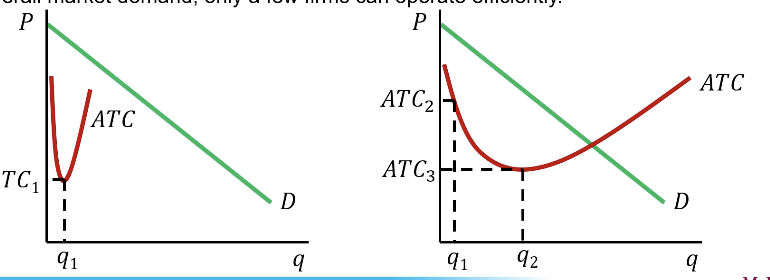

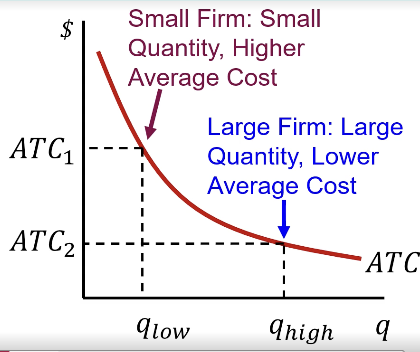

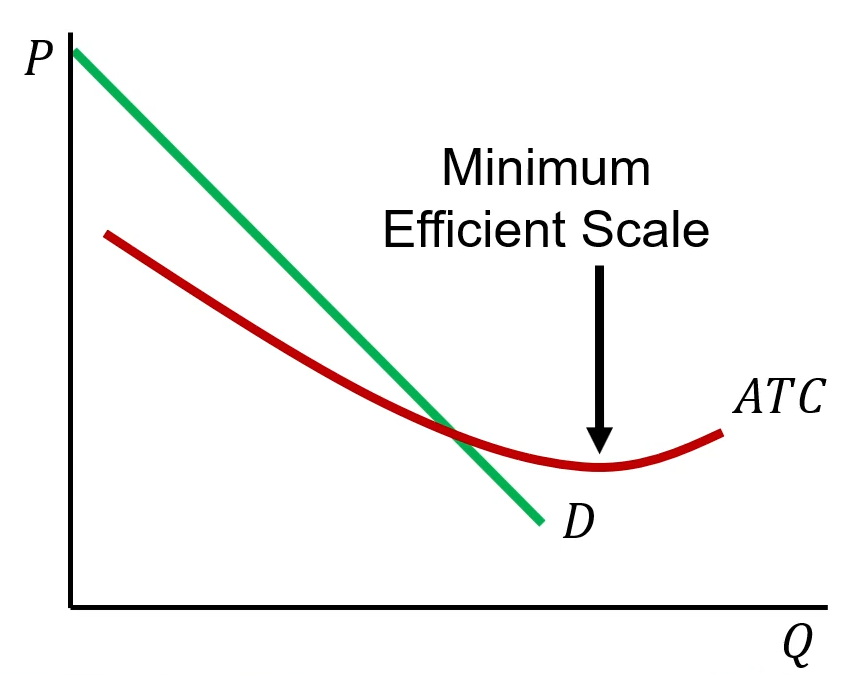

Unit 10 Economies of Scale

If the minimum efficient scale occurs at a level of output that is small relative to overall market demand, there will be room in the market for many firms to operate efficiently, so the market will be competitive

However, if the minimum efficient scale occurs at a level of output that is large relative to overall market demand, only a few firms can operate efficiently

Unit 10 Government Regulations

Governments can restrict market entry through licenses

In some industries, a license is required to operate. The government can restrict the number of licenses available.

Unit 10 Government Regulations Copyrights & Patents

Governments can also restrict market entry through patents and copyrights

A patent provides the inventor of a product the exclusive right to make that product for 20 years

A copyright provides the creator of.a creative work the exclusive right to copy, distribute, and profit from that work for the life of the creator plus an additional 70 years

These policies encourage creators by protecting the investment they make in creating these works

Unit 10 Ownership of a Resource

When production requires a specific input that is not widely available, new firms may have difficulty entering the market

The resource could be a natural resource, a human resource, or a knowledge resource.

Brand value can also be an important resource

Unit 10 Why Oligopolies Examples

Car Manufacturers

High capital costs

High research and development costs

Telecommunications Companies

High capital costs

Government restrictions on wireless and broadcast signals

Airlines

High capital costs

High knowledge costs

Airport landing fees and restrictions

Unit 10 Why Oligopolies

Brand name, reputation, and operating history can represent a significant barrier to entry.

Unit 10 Oligopoly Graphs

When MR > MC, revenues grow faster than costs and profits will increase

When MR < MC, costs grow faster than revenues and profits will decrease

Our profits will reach their maximum level at MR = MC

For an oligopoly firm P > MC

The price consumers pay is higher than the marginal cost to make the good. We call this a difference of a price markup

Unit 10 Profits in an Oligopoly

Profit Per Unit = Profit / Quantity = Profit - ATC

When P > ATC, the firm earns a profit per unit

What is different about an oligopoly through is that this profit could be sustainable in the long run because new firms cannot enter to compete it away

Unit 10 Losses in an Oligopoly

When P < ATC, the firm earns a loss per unit

Qo is the loss minimizing quantity

A firm might go out of business which would increase demand for other firms goods as customers move over to them

Alternatively the firm could try to reduce its average total cost over the long run

Unit 10 Oligopoly Behaviour

Because oligopolies have large market share and face few competitors, they must think carefully about their own actions and the actions of their competitor

Oligopolies will behave more strategically than monopolistically competitive firms

Unit 10 Profit Maximization in an Oligopoly

In an oligopoly, there are few firms, each with a large market share. We can consider two firms ( a duopoly)

Suppose Firm B decides to spend more on advertising

Its ATC will rise, but so will demand for its product. It will then get more customers and earn more profits.

Where did the customers come from? …. Some will come from Firm A

Firm A will see falling demand and will face pressure to cut its price. Its profit will fall.

Unit 10 Strategic Behaviour in an Oligopoly

Will Firm A just accept having a lower market share, lower price, and reduced profit? … Maybe… Maybe not.

Because there are only a few firms, each with a large market share, we say there is mutual interdependence - A firms profit level depends not just on its own decisions, but also on the decisions made by its rivals

When making any business decision, an oligopolist must consider how rivals will react

Unit 10 Game Theory

Game Theory is an analytical tool economists use to predict the actions of agents in different scenarios.

John Von Neumann

Oskar Morgenstern

Merrill M Flood

Melvin Dresher

Albert W Tucker

John Nash

Unit 10 Game Theory Terms

A conjecture is what a player believes a competitor will do.

A strategy is a choice from the available actions.

A best response is the choice that gives the highest profit based on that belief.

A dominant strategy gives the highest profit no matter what others choose.

Unit 10 Game Theory Responses

Rational players will identify a best response for every scenario they face

If their best response is the same for all scenarios (i.e., they would always make the same choice no matter what a competitor does), then the choice is a Dominant Strategy

If both players choose a best response, we have a Nash Equilibrium - the players will be satisfied with their own choice after seeing their opponents choice

If both players choose a Dominant Strategy, we have a Dominant Strategy Equilibrium - dominant strategies do not always exist so this outcome will not occur in all games

Unit 10 Making Decisions

We can use a matrix to map out prospective decisions and profits

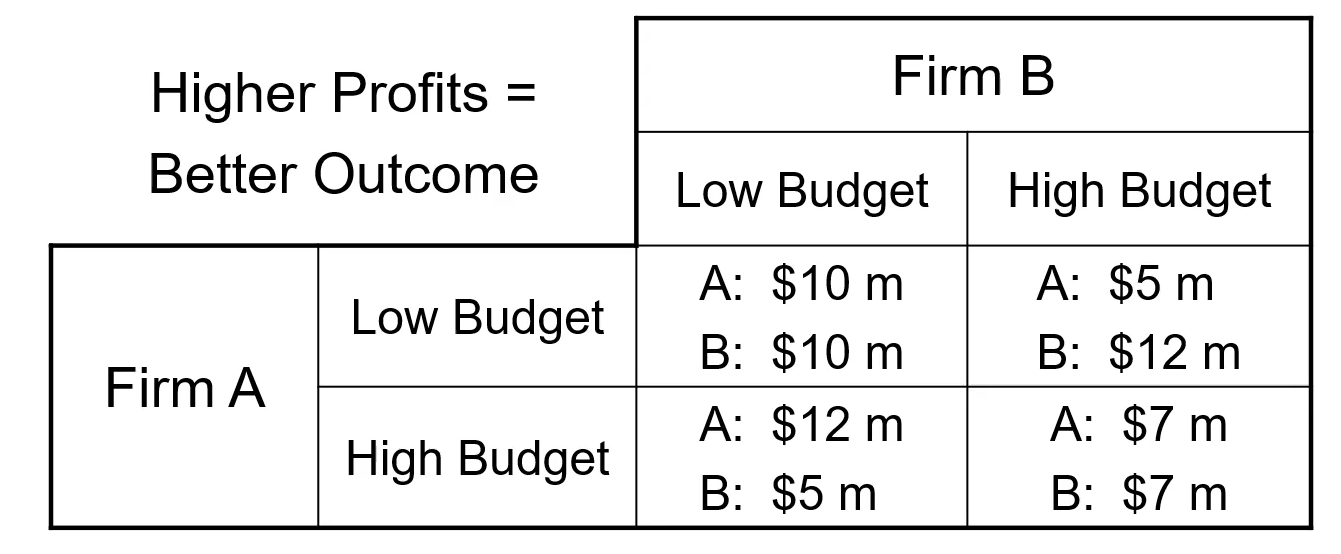

Unit 10 The Advertising Game

Two oligopolists (i.e., a duopoly) must choose their advertising budgets

Each can choose a Low Budget or a High Budget

If they both choose the same budget, they share the consumer market evenly. But, if one chooses High and the other chooses Low, the one who choose a High Budget gets most of the customers

Highlights an important aspect of economic behavior: Individual agents working in their own self interest can naturally end up in a situation that is not socially optimal

Unit 10 The Advertising Game Matrix

We cab examine the profits they each make in Millions of Dollars

We can make a conjecture about behavior and identify best responses

Dominant strategy is when a firm makes the same decision no matter the others actions

Unit 10 Nash Equilibrium

Since Firm A and Firm B both choose a High Budget, that will be our outcome. Both players outcomes are circled (i.e., both are playing best response)

We know it is this because no player would want to change their decision after seeing the other players choice

Unit 10 Dominant Strategy Equilibrium

Since both firms play a Dominant Strategy, it is also this

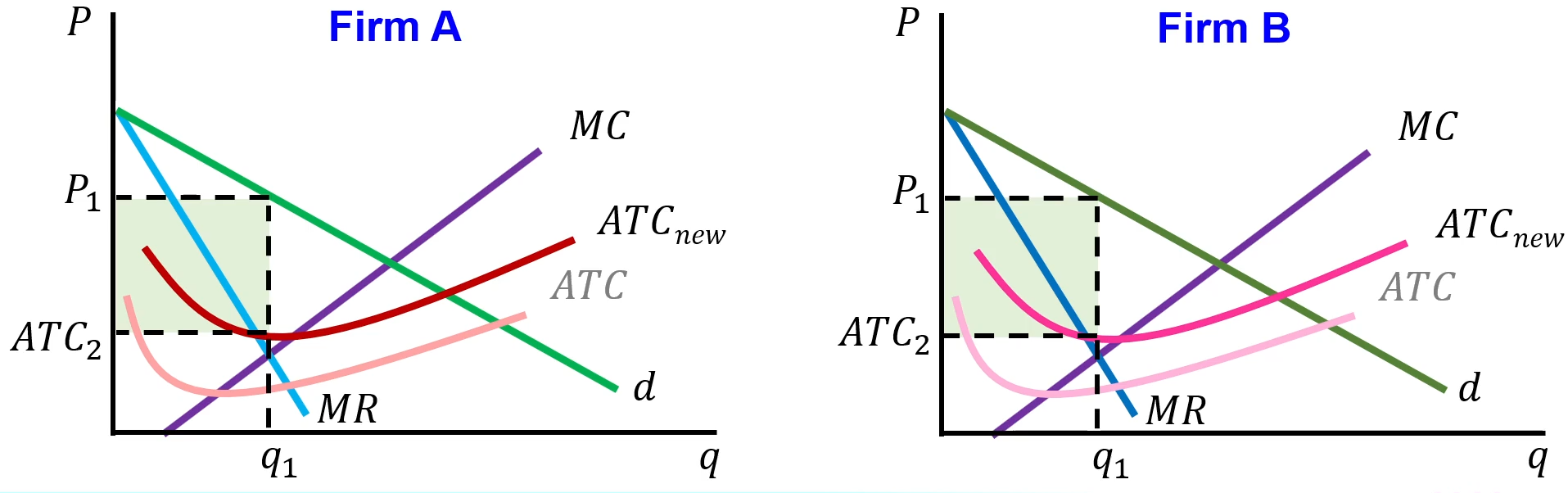

Unit 10 Strategic Behavior in an Oligopoly

Firm B is going to increase its advertising. But it will not get to keep the profits

Firm A will increase its advertising in response and retain (or take back) its customers

Before the change, both firms had lower costs, and therefore higher profits

But now they have higher costs, and lower profits, and they were not able to take customers away from their competitor

Unit 10 Could They Just Agree NOT to Compete

Clearly it would be better for them if neither increased their advertising expenditure

Other situations where they might prefer not to compete with each other include:

Charge higher prices and do not lower price to steal customers from competitors

Pay low wages and do not raise wages to lure talented workers from competitors

If they do this though, it is called collusion and we say they are operating as a cartel

Unit 10 Collusion

When firms coordinate their actions to increase prices above the competitive level or reduce cost below the level that would occur with competition. Firms participating are known as a trust or a cartel

Collusion is illegal in developed countries because it harms consumers, workers or both. Anti trust laws have been enforced since the late 19t century to prevent collusion

Unit 10 Why Collusion Does Not Work

Collusion can work for a short time, but firms have an incentive to cheat

If firms believe the agreement will not last forever, they have an incentive to be the first one to abort it

Confession brings lesser penalties for the individuals involved, so there is an incentive for individual managers / employees of a company to alert competition authorities to anti competitive actions

Whistleblower legislation protects employees of a company who reports illegal activities

Unit 10 The Front Page Game

Two local newspapers compete for readers and must decide each day what type of headline story to run on their front page

Each newspaper can either choose a story about politics or a story about business and the economy

Among the population of potential readers, more people prefer stories about politics to stories about business and the economy

Unit 10 Signaling and Updating

If a game without dominant strategies is played only once, there is no opportunity to learn from your opponents actions

However, if a game is repeated, players have the ability to learn from their opponents actions or to send signals to their opponent through their own actions

Rational players should consider all information available wen making strategic choices

Unit 10 The Price Elasticity of Demand

In Unit 5, we learned that one of the main determinants of the price elasticity of demand was the availability of substitute goods

Unit 10 Oligopoly and Deadweight Loss

The price markup is larger in an oligopoly, so the deadweight loss in an oligo

Unit 10 Oligopoly and Profit

Oligopolies can earn excess economic profits over the long run because barriers to entry prevent new competitors from entering

Unit 10 Oligopoly and Inequality

Income and consumption inequality are a major disadvantage of market economies

Since oligopoly firms can earn excess profits and can grow to become very large enterprises, the owners of these firms can accumulate a disproportionately large share of wealth and associated income in market economies.

Unit 10 Are Oligopolies That Bad

Oligopolies are innovative so they aren’t entirely bad

They have advantages and also disadvantages

The benefits only occur when oligopolies compete against each other, so governments must actively encourage competition and prevent collusion

Unit 10 Oligopolies and Innovation

Joseph Schumpeter argued that oligopoly was the most beneficial form of market structure so long as oligopolists compete rather than collude

Innovation requires research and development expenditure, but perfect competition and monopolistic competition do not generate any excess profit that can be invested into R&D.

Only oligopolies can generate:

The excess profits needed initially to fund R&D

The excess profits needed to provide a return on that investment (remember patents!)

Because oligopoly firms compete against each other for market share, they have an incentive to continually innovate

Failure to innovate will mean that, eventually your rivals will overtake you

Any firm that does not innovate will eventually go out of business

Process is known as creative destruction (major feature of market economics)

Unit 10 Types of Innovation

Product Innovation

Creates new goods and therefore new markets which society can draw economic surplus. The creation of new markets therefore leads to an increase in social welfare

Process innovation

New production process improve productive efficiency. new methods of producing allow for greater output with fewer inputs

Both types of innovations can be protected by patents

Unit 11 Monopoly

A monopoly is the only seller of a good or service that does not have a close substitute

Barriers to entry prevent other firms from entering

Because there is only one firm, the firms demand curve is the same as the market demand curve

Unit 11 Barriers to Entry

Prevent new firms from entering the market

Economies of scale

Government regulations

Ownership of a resource

Unit 11 Economies of Scale

If the minimum efficient scale occurs at a level of output that is larger than the quantity demanded by consumers, a single firm supplying the entire market can produce at a lower cost than multiple smaller firms.

This situation is called a natural monopoly

Electrical company

Water company

Unit 11 Government Regulations

In Unit 10, we learned about licenses, patents, and copyrights as government created barriers to entry.

The government may also grant a public franchise which gives a firm the sole right to provide a good or service. In some cases, the government may grant this franchise to itself and establish a state-owned enterprise (SEO)

Inc Canada we often refer to SEO as a crown corporation

Public Transit

Canada Post

Unit 11 Ownership of a Resource

In unit 10 we learned about ownership of natural resources, human resources, and knowledge resources as barriers to entry

Ownership of a physical premises is a common source of monopoly power

Amusement park and movie theatre concessions

Stadium merchandise and concessions

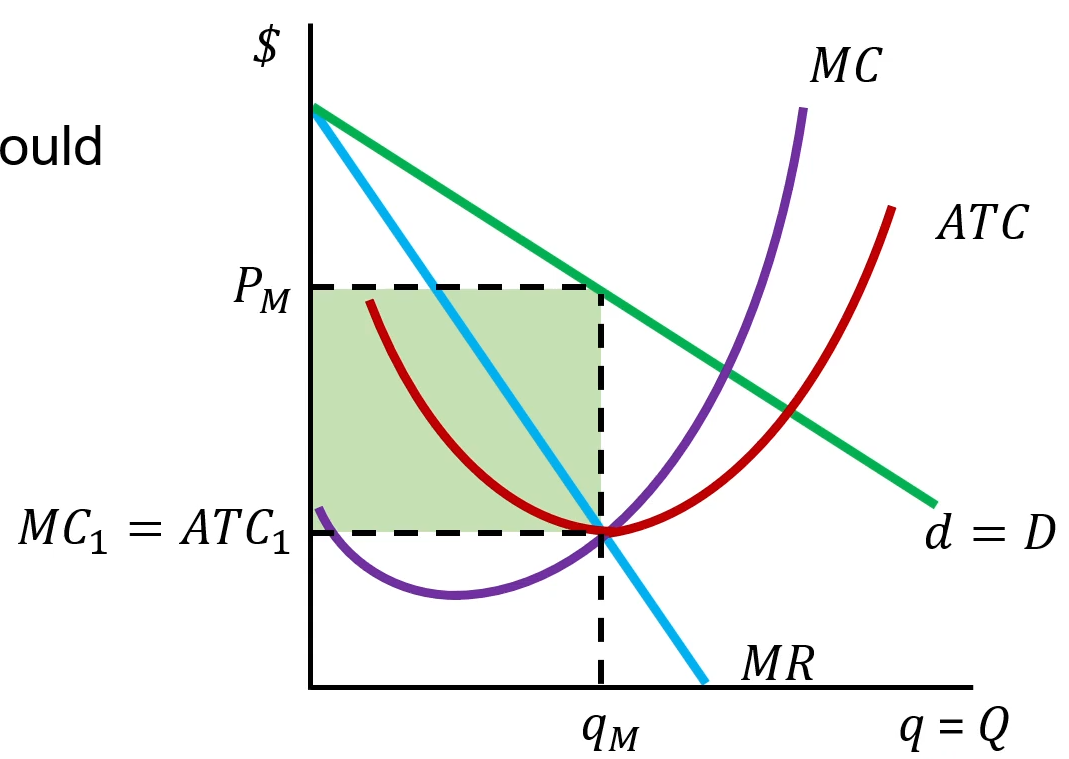

Unit 11 Monopoly MR & D Graph

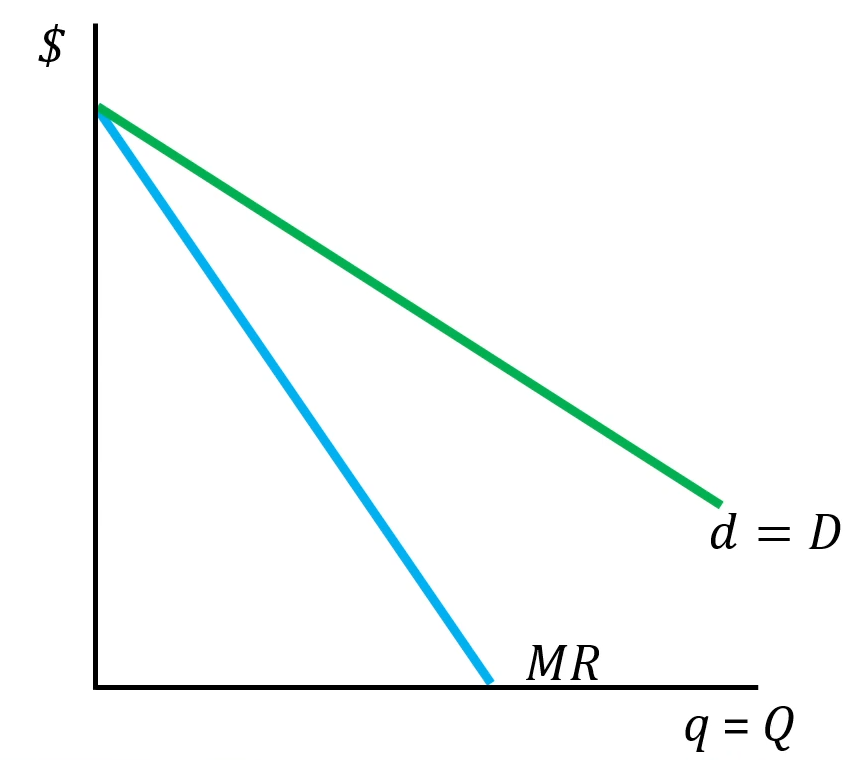

Because a monopoly serves the whole market, its individual product demand (d) is equal to the total market demand (D). Similarly, since it is the only firm, the monopoly’s quantity (q) is the same as the total market quantity (Q)

We know from units 9 and 10 that marginal revenue for firms with market power is always less than the price they charge.

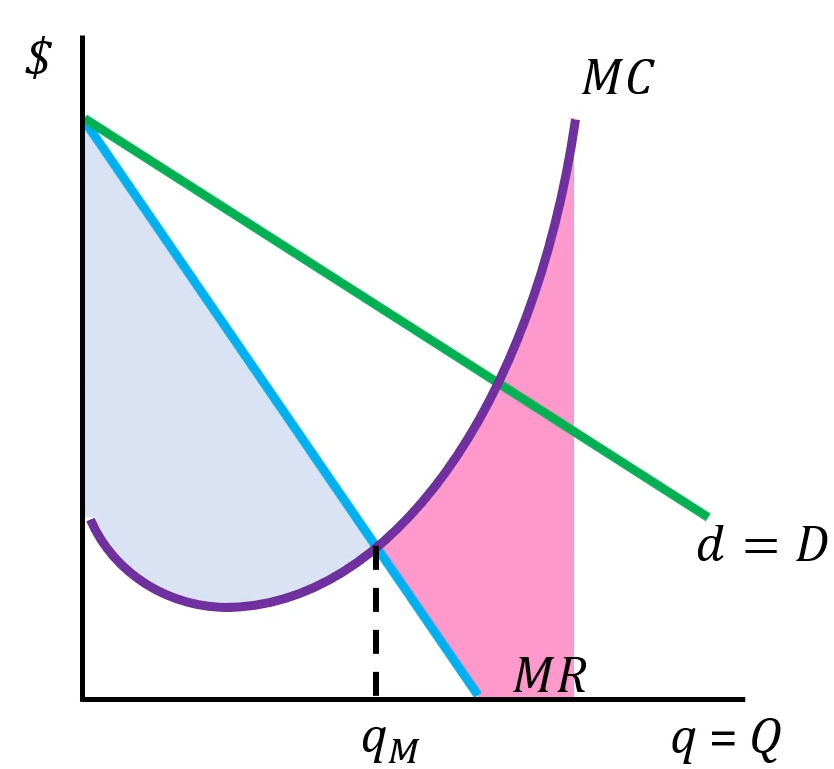

Unit 11 Monopoly MR & MC & D Graph

When MR > MC, revenues grow faster than costs and profits will increase

When MR < MC, costs grow faster than revenues and profits will decrease

Our profits reach their maximum level at MR = MC

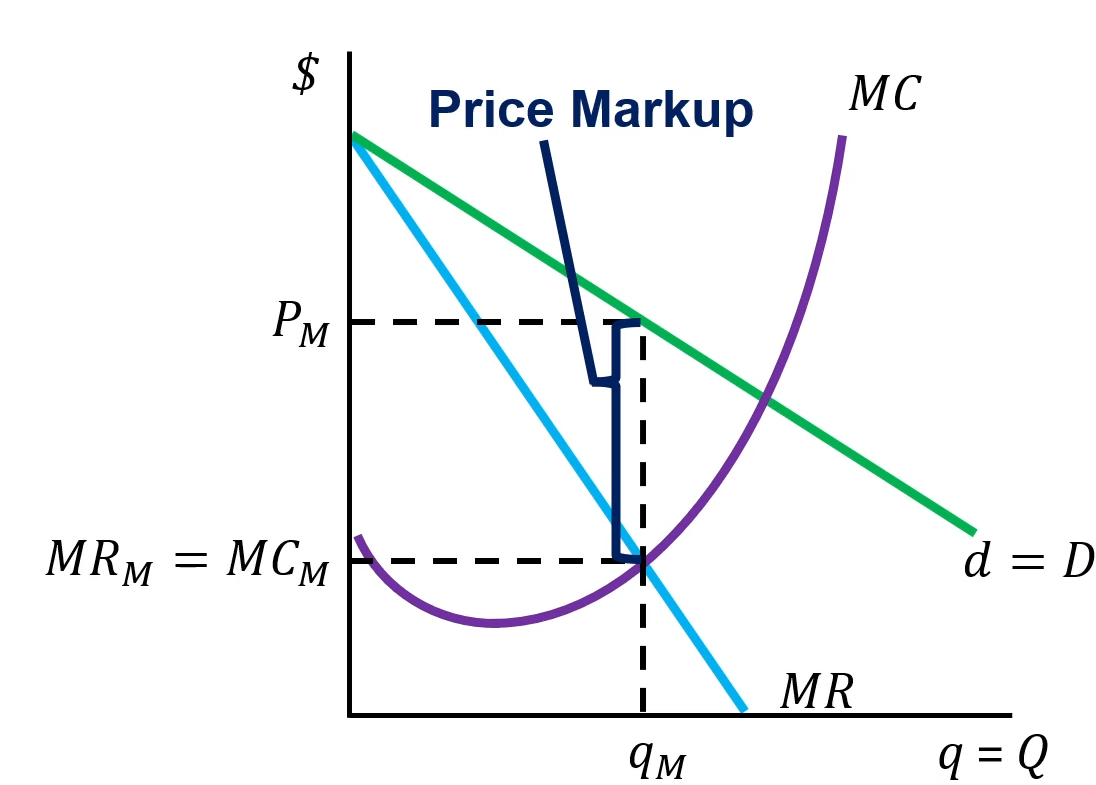

Unit 11 Markup

For a monopoly: P > MC

The price consumers pay is higher than the marginal cost to make the good. We call this difference a price markup.

Markup = P - MC

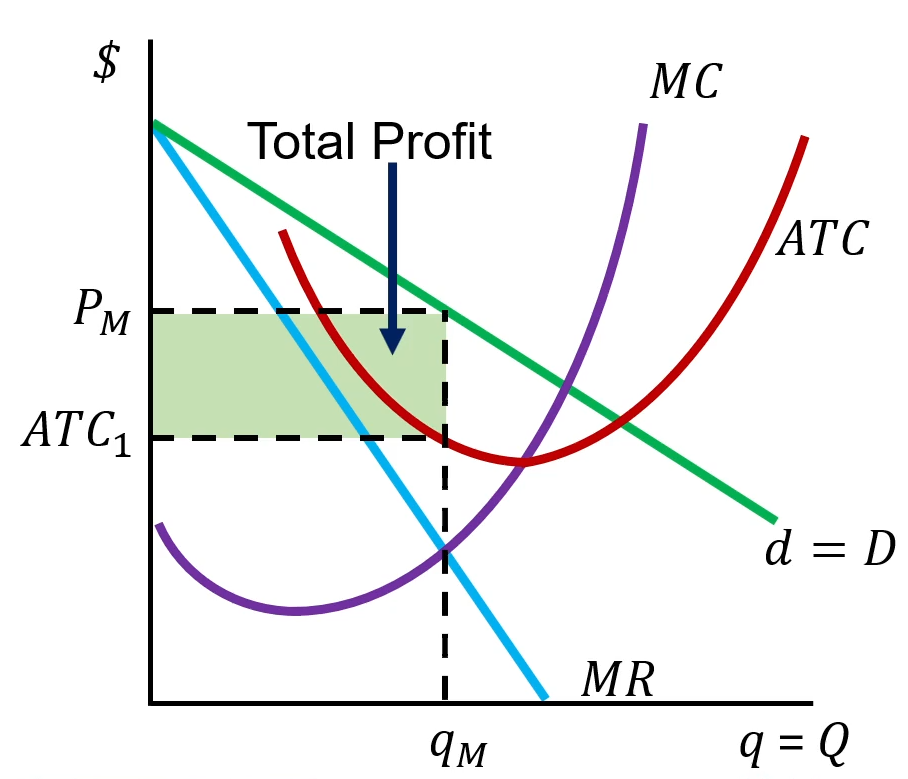

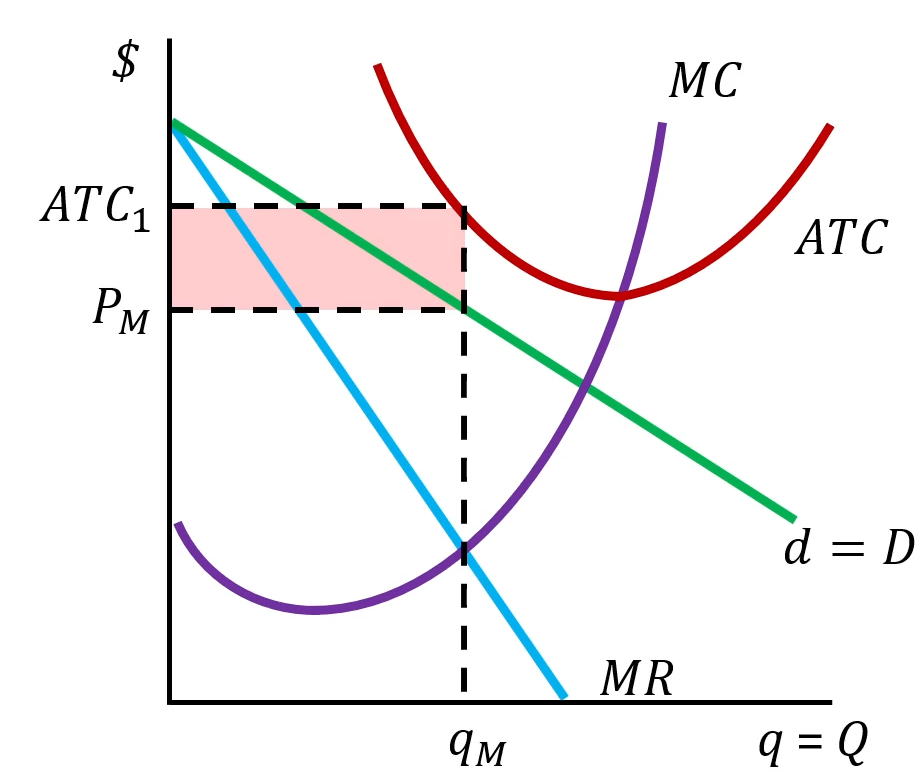

Unit 11 Profits in a Monopoly

Profit per unit = total profit ÷ quantity = price − average total cost (P − ATC)

When P > ATC, the firm earns a profit per unit

For a monopoly, this profit could be sustainable in the long run because new firms cannot enter to compete it away

Unit 11 Losses in a Monopoly

Profit per Unit = profit / quantity = P - ATC

When P < ATC, the firm earns a loss per unit

qM is the loss minimizing quantity

The firm must try to reduce its average total cost over the long-run

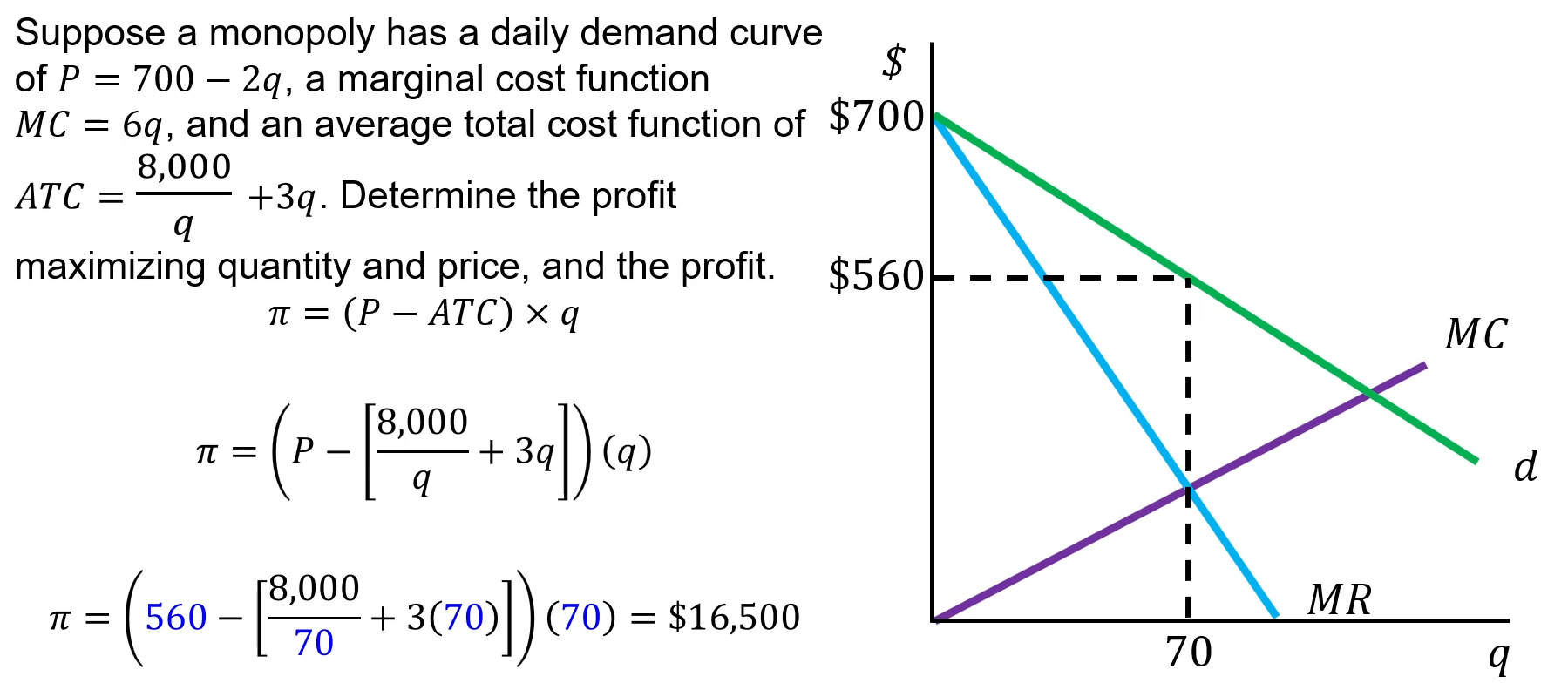

Unit 11 Price and Quantity in Monopoly

Suppose a monopoly has a daily demand curve of P = 700 -2q, a marginal cost function MC = 6q, and an average total cost function of ATC = 8000/q + 3q

Determine the profit maximizing quantity and price, and the profit

Unit 11 The Price Elasticity of Demand

In unit 5, we learned that one of the main determinants of the price elasticity of demand was the availability of substitute goods

Unit 11 Monopoly and Deadweight Loss

The price markup is even larger in a monopoly than in monopolistic competition or oligopoly, so the deadweight loss in a monopoly will also be larger than in any situation with any amount of competition

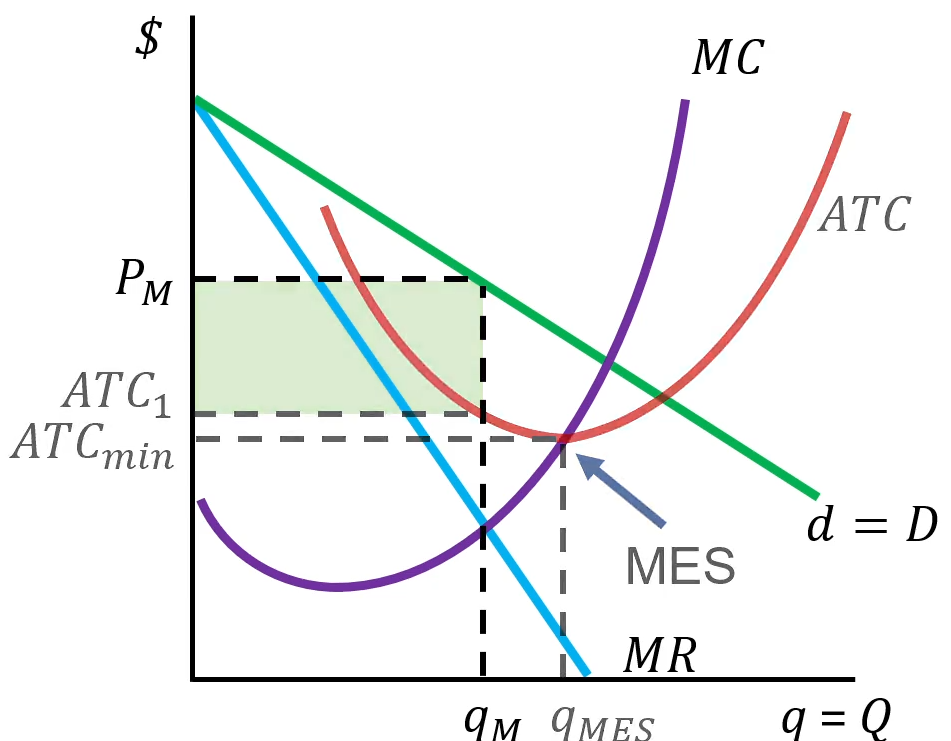

Unit 11 Profits and Production Efficiency in a Monopoly

Monopolies typically earn an economic profit, which is also called a monopoly rent

The profit maximizing quantity is usually not the minimum efficient scale

Monopolies generally do not achieve productive efficiency

Unit 11 Profits and Production Efficiency in a Monopoly

It is possible the monopoly could profit maximize right at the minimum efficient scale quantity

But is NOT likely

Unit 11 Monopoly Inefficiency

Monopolies are inefficient for three main reasons:

Allocative inefficiency

A monopoly sets price above marginal cost (P > MC).

This means some consumers value additional units more than the cost to produce them, but those units are not produced.Productive inefficiency

The firm does not produce at the lowest possible cost.

At the profit-maximizing output, marginal cost does not equal average total cost (MC ≠ ATC), so it is not operating at minimum efficient scale.Inefficient allocation of capital

Barriers to entry let the monopoly earn long-run economic profit (P > ATC).

In a competitive market, profits would attract new firms and push price down to ATC.

Without entry, capital stays in the monopoly instead of flowing to more efficient uses.

Unit 11 Competition Policy

Because monopolies are inefficient, raising prices and making consumers worse off, antitrust laws that we learned about in Unit 10 are designed to prevent competing firms from merging to form monopolies.

When two competing firms in the same industry merge it is called horizontal integration. The federal governments competition bureau typically prevents mergers when the new firm would have more than 35% market share or when the four largest firms in an industry have more than 65% combined market share.

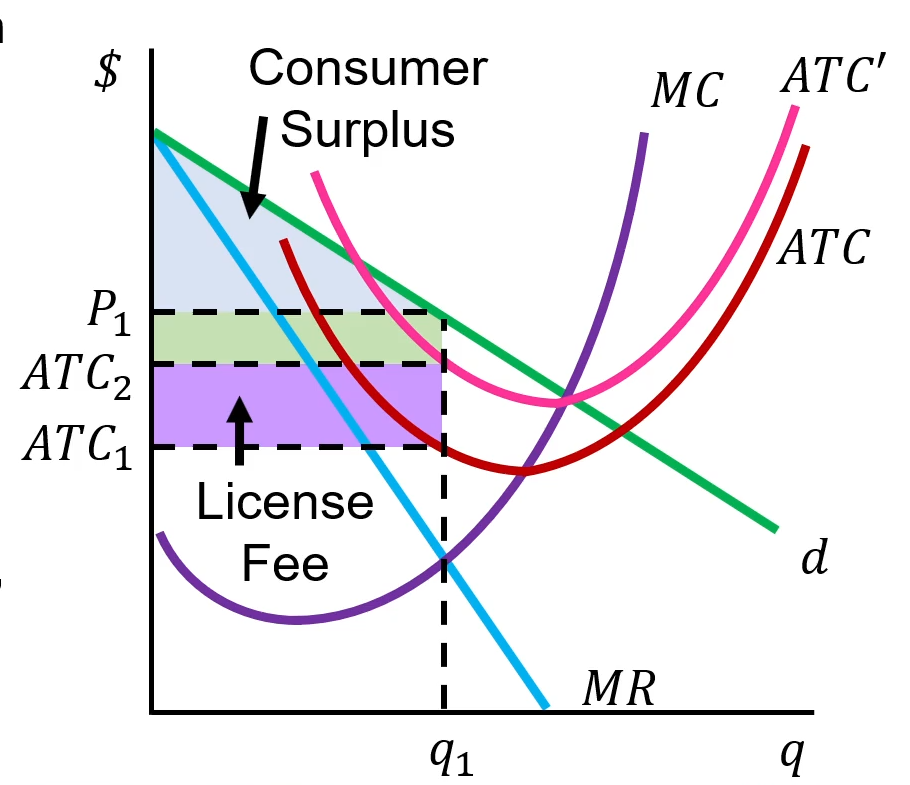

Unit 11 Regulating Monopolies and Oligopolies (Licensing)

Because monopolies and oligopolies can charge high markups and make consumers worse off, governments regularly intervene in these markets.

Government can charge a licensing fee which strips away some of the economic profit. A licensing fee is a fixed cost so it changes ATC but not MC

Since MC is unchanged, q is unchanged, but profit is reduced. The money raised from the market means the government can reduce taxes in other markets.

Consumer surplus increases. The market is more efficient!

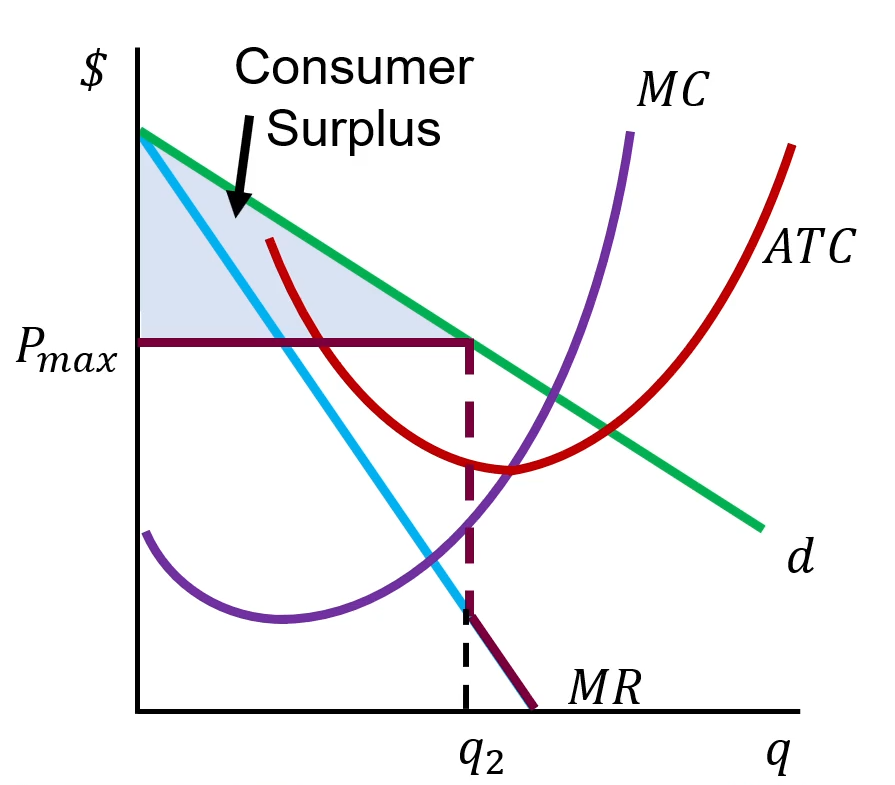

Unit 11 Regulating Monopolies and Oligopolies (Price Ceiling)

Because monopolies and oligopolies can charge high markups and make consumers worse off, governments regularly intervene in these markets.

Sometimes governments will impose price ceilings on oligopoly and monopoly firms.

A price ceiling actually makes MR = P because the firm cannot raise its price (just like in perfect competition)

If the government gets the price ceiling just right, it might even be able to replicate the perfectly competitive outcome!

In practice though, this outcome may be difficult to achieve

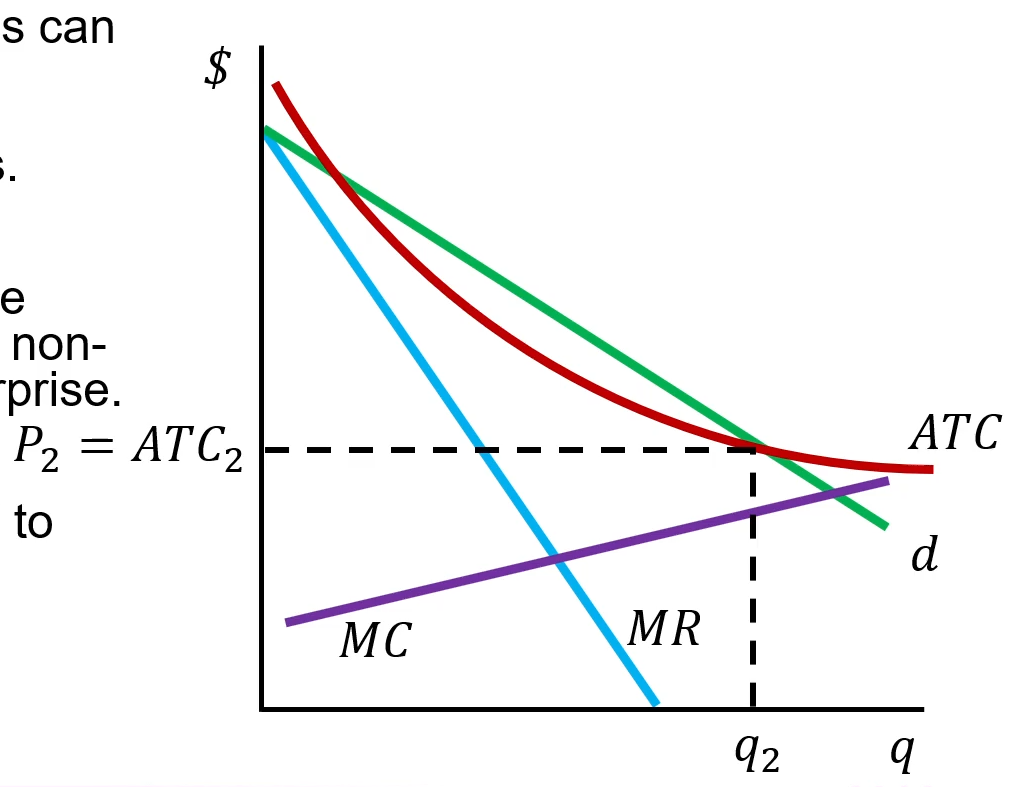

Unit 11 Monopolies and Government Decision

Because monopolies and oligopolies can charge high markups and make consumers worse off, governments regularly intervene in these markets.

In situations of natural monopoly, the government may decide to create a non-profit maximizing state-owned enterprise.

The government will set price equal to average total cost

Unit 11 Federally Regulated Industries

Rail

SEO with a near monopoly on intercity (non commuter) passenger travel

License fee for freight operators and railway owners

Air travel

License fee for all airlines carrying passengers and/or cargo

Telecommunications

Licenses and price ceilings on phone, data/internet, and cable/satellite television

Banking and Lending Services

Price ceilings on service charges and interest payments

Unit 11 Provincially Regulated Industry

Electricity

Some provinces have a state owned monopoly; others have competitive producers; all have some form of price controls

Natural gas

Price ceiling

Water

State-owned monopolies at the municipal level

Public transportation

Price ceiling

College and Universities

Price ceiling

Unit 11 Price Discrimination

Price discrimination is the act of charging different prices to different customers for the same good or service. It is a legal business practice

Only works if

The firm has market power

The firm can identify customers who are willing to pay more than others

The firm can prevent resale

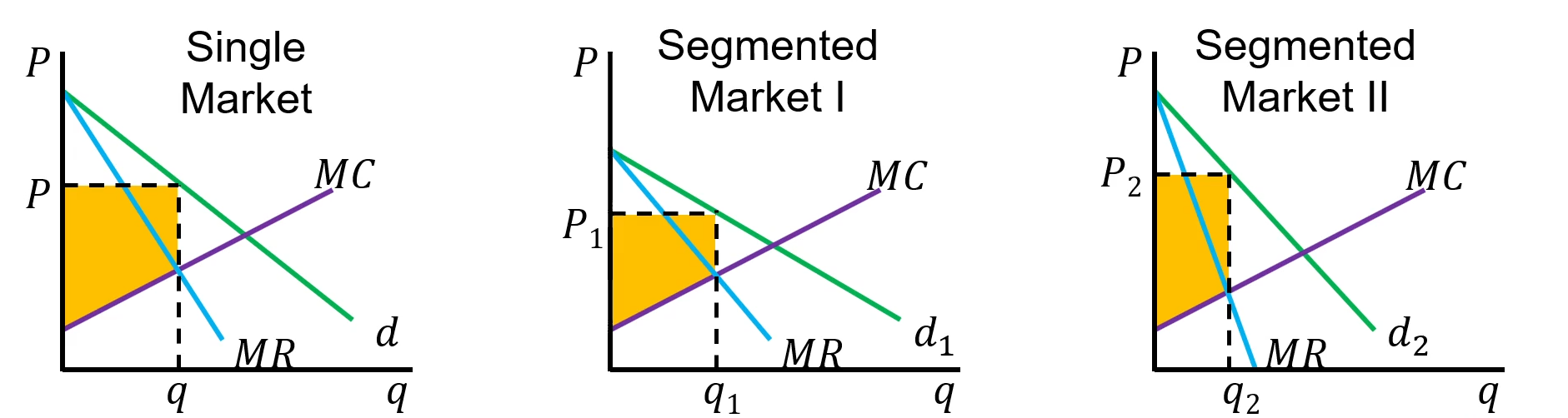

Unit 11 Multi Market Price Discrimination

Third Degree

Charges different prices to different market segments

Could be segmented by geography, age, student status, etc

Overall, output will be higher and producer surplus larger

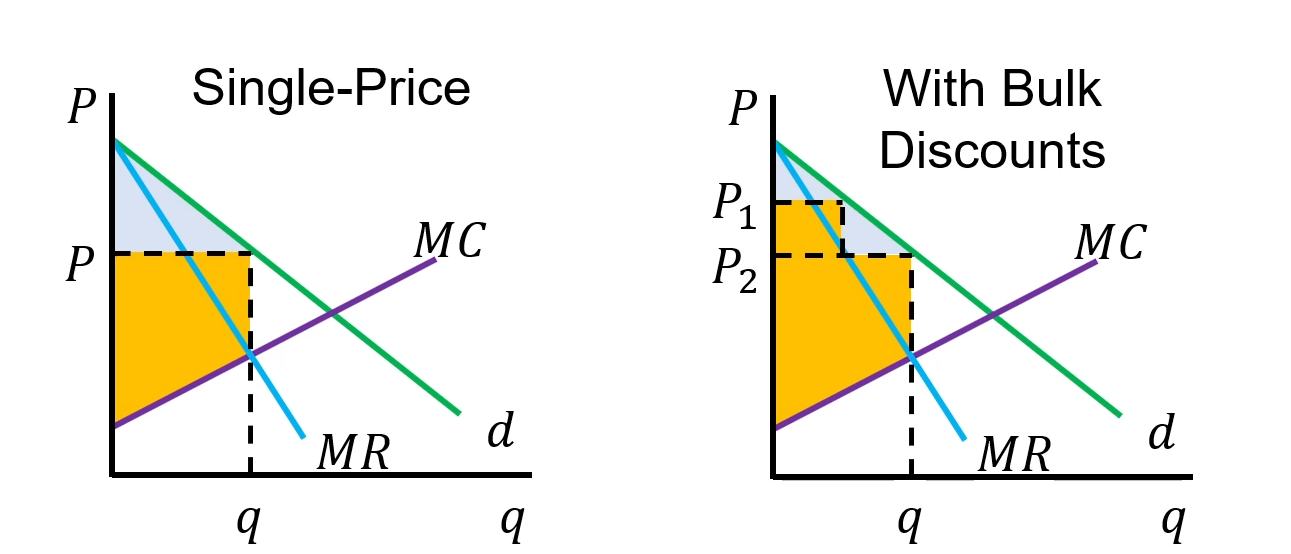

Unit 11 Quantity Based Price Discrimination

Second Degree

Offer bulk discounts

Those wanting to buy a small quantity must pay a higher price

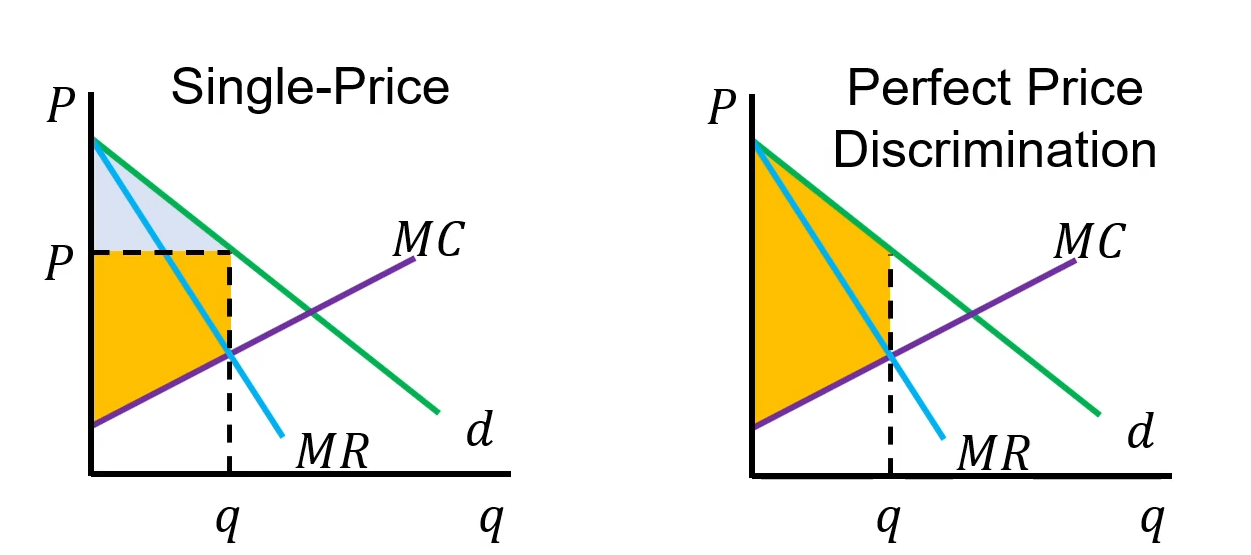

Unit 11 Perfect Price Discrimination

First Degree

Charge each consumer their exact willingness to pay

It is almost impossible in practice, but auctions and negotiations attempt to replicate this outcome

Unit 11 Two Part Tariffs and Junk Fees

With a two part tariff, the firm charges a membership or entrance fee as well as a fee for use, for example a gym charging a monthly fee plus per class charges

With a junk fee, the firm adds a processing or administrative charge on top of the listed price, for example a ticket site adding a service fee at checkout

These fees capture part of the consumer surplus by extracting extra payment beyond the base price

Optimal pricing depends on differences in consumer preferences and willingness to pay, firms set higher fees when consumers value the product more or have fewer alternatives

Unit 11 Price Matching (Low Price Guarantee)

LPGs are good for firm reputation and profits

LPGs can enforce collusion in markets with strong price competition (if your rival lowers its price, you will match them and vice versa so there is no benefit to lowering price)

It also means you do not have to monitor rivals because if they lower their price, your customers will let you know

It allows you to price discriminate by charging a higher price to customers who do not realize there are cheaper prices available

Unit 11 Challenges with Price Matching

You cannot just take your customers word for it; there must be some way to verify that a rival is charging lower prices

Depending on your rivals cost function, they may be able to sell at a lower price which you cannot match profitably. Often, firms will limit this strategy to regular prices and will not match discounted prices

Unit 11 Loss Leaders

For retail firms that sell many products, one of the biggest challenges is getting customers to choose your store over a competitor

A loss leader is an item sold below cost and typically advertised as being on sale. It guarantees the seller will make a loss on this item but also ensures that rivals will not have the same price initially. Rivals may be unwilling to match this price as it guarantees a loss.

Once the customer is in your store to get the discounted item, hopefully they will buy other things as well, the profits from which will make up for the loss taken on the loss leader

Unit 12 Market Failures

Throughout the course, we have learned that free markets and perfect competition should produce the most efficient outcome

However, many markets suffer from market failures, a characteristic of a market that makes it depart from perfect competition and therefore leads to an inefficient outcome

Market failures provide an opportunity for government intervention to improve efficiency and/or correct undesirable outcomes

Unit 12 Common Market Failures

Market power

Externalities

Incomplete information

Unit 12 Market Power

As we saw in units 9, 10, and 11, any firm with market power will charge a price markup and the market will be inefficient

In the case of monopolistic competition, the inefficiency is usually small since the firms are small, but in the case of oligopoly and monopoly, the inefficiency may be large, and the government may become concerned with the impact on consumers

Refer to units 10, and 11 for more information on government regulation of oligopoly and monopoly firms

Unit 12 Externalities

An externality is a benefit or a cost falling on other people not directly involved in a market transaction

Arthur Cecil Pigou - Studied this

The existence of externalities means that the social costs and/or social benefits are not the same as the private costs or private benefits experienced by the private parties involved in the transaction

Unit 12 Negative Externalities

Occur any time one agents actions have negative effects on other people

e.g. pollution and traffic

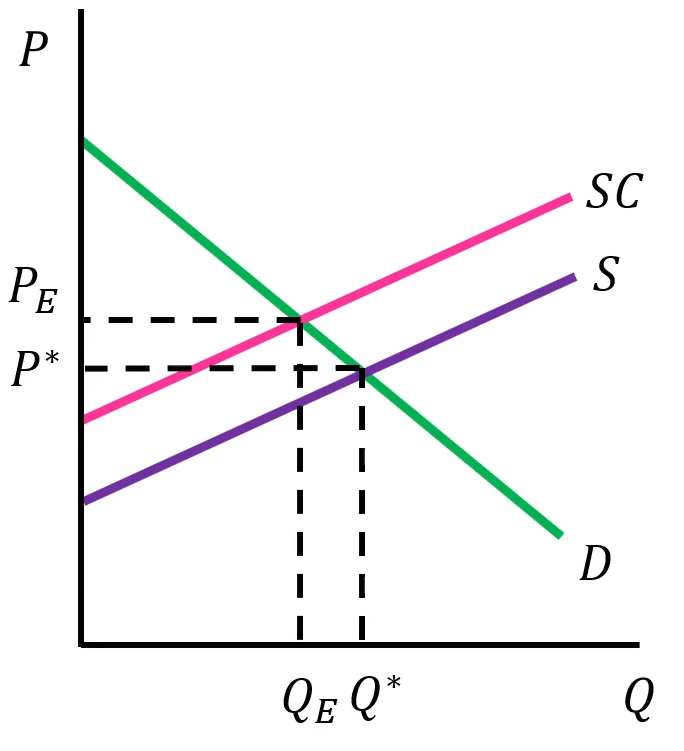

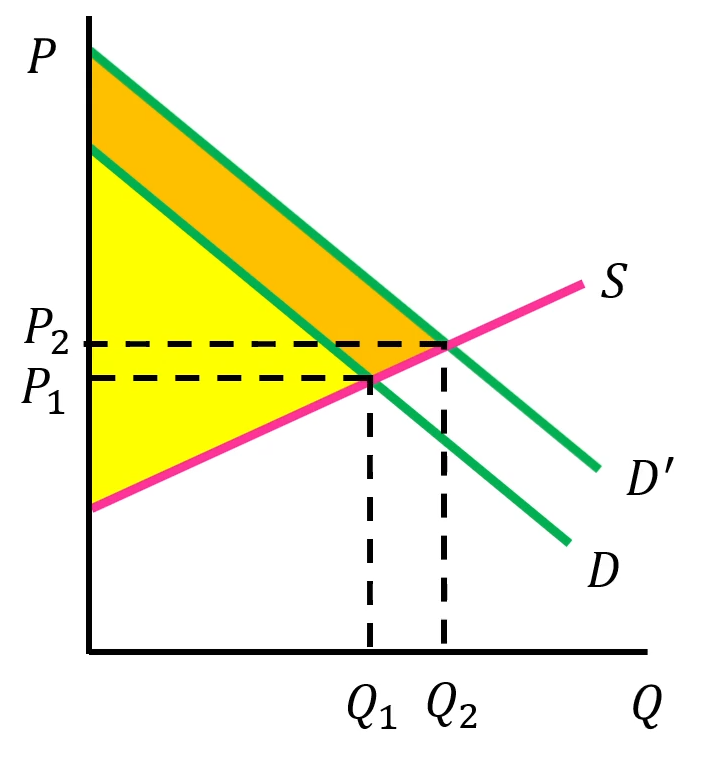

Unit 12 Negative Externalities Graph Effect

When a negative externality is present, the social cost (SC) of producing a good is higher than the private cost as represented by the supply curve

The socially optimal quantity (Qe) is less than Q*, but usually not zero. Goods with negative externalities are overproduced in a free market

Unit 12 Correcting for Negative Externalities

The government has multiple policy options to correct for negative externalities:

Impose regulations to limit the quantity (quota)

Impose a tax that raises the cost to consumers and reduces consumption (Pigouvian Tax)

Unit 12 Positive Externalities

Positive externalities occur any time one agents actions have positive effects on other people

e.g. research, volunteering, university

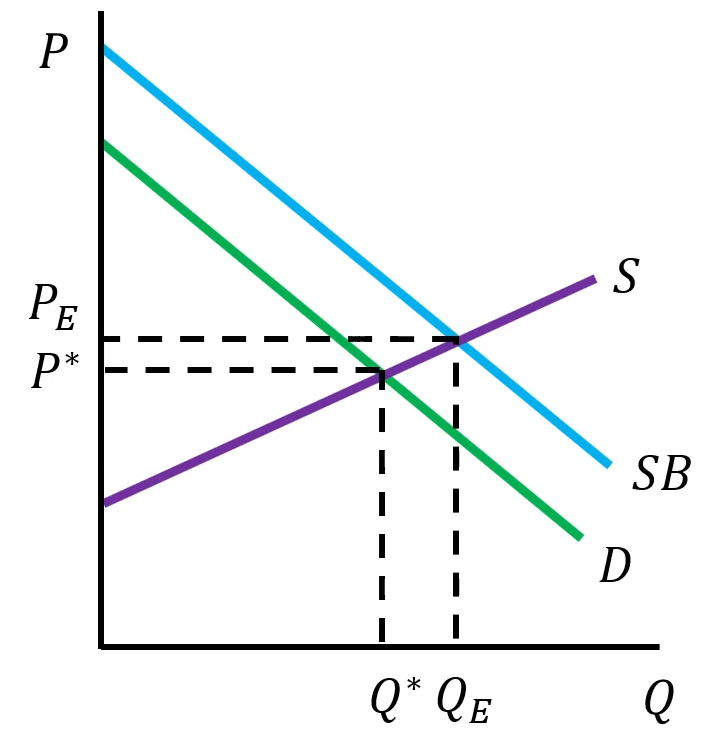

Unit 12 Positive Externalities Graph Effect

When a positive externality is present, the social benefit (SB) of consuming a good is higher than the private benefit as represented by the demand curve

The socially optimal quantity (Qe) is more than Q*. Goods with positive externalities are underprovided in a free market

Unit 12 Correcting for Positive Externalities

The government has multiple policy options to correct for positive externalities

Provide subsidies to firms to lower their costs

Provide subsidies to consumers to increase demand

Provide the good itself, either in competition with or by replacing private firms

Unit 12 Incomplete Information

Many markets suffer from incomplete information regarding product standards and quality. Increased risk and uncertainty can make consumers more hesitant to buy a product or service and can depress market demand

Unit 12 Correcting for Incomplete Information

When the government enforces standardizing regulations, it can reduce consumers uncertainty. Reducing uncertainty increases consumer demand and therefore increases total market surplus

e.g. food regulations, cigarette regulations, etc.

This happens more often than we notice

Unit 12 The Classification of Goods

Rivalry

A good is rivalrous if one person’s use reduces how much is left for others.

A good is non-rivalrous if one person’s use does not affect others.Examples

Rivalrous vs Non-rivalrousPizza vs Car radio signal

Bottle of water vs Streetlight

Laptop vs GPS satellite signal

Seat on a bus vs Public Wi-Fi (light use)

Excludability

A good is excludable if people can be prevented from using it unless they pay.

A good is non-excludable if it is hard or impossible to stop people from using it.Examples

Excludable vs Non-excludableNetflix subscription vs National defense

Toll highway vs Public road (no toll)

Private park vs Public park

Concert ticket vs Fireworks display