Macroeconomics SUAS

1/100

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

101 Terms

Classics/Classical School

The oldest traditional economic school, the theoretical foundation of a social market economy.

Notable work of the classical school

“An Inquiry into the Nature and Causes of the Wealth of Nations,” by Adam Smith, published in 1776.

Adam Smith

A Scottish moral philosopher, author of “An Inquiry into the Nature and Causes of the Wealth of Nations” (1776) and “Theory of Moral Sentiments” (1759)

Invisible Hand

A term used to describe unseen driving force of the market.

Ordo-Liberalism

Literally “framework liberalism,” a term that can apply to many classical economists.

Social Market Economy/Social Capitalism

Socioeconomic model that combines free-market capitalism with regulations and social policies meant to create a fair but competitive market.

Regulatory Policy

Policy meant to create consistent conditions and achieve compatibility between individual and collective interests.

Process Policy

Policy that emerges through Market activity.

Neo-Classics/Neo-Classical School

One of the most influential models of economics. Emphasis on microeconomic processes, methodological individualism, and the marginal Principal of allocation.

Methodological Individualism

A method of explaining social phenomena in terms of individual decision making.

Notable work of the Neo-Classical School

“General Theory of Employment, Interest, and Money,” by John Maynard Keynes (1936)

John Maynard Keynes

Politician and economist from the early 20th century. Played significant roles in the Great Depression and in post-war peace negotiations.

Marginal Principal of Allocation

Reasoning in infinitesimally small differences.

Price-Taker

Buyers or Sellers that accept the market price and cannot bargain for a better price.

Price-Setter

Buyers or Sellers that can bargain for a better price.

Perfect Competition

Model where we assume all else is equal, and that buyers or sellers are not able to affect the market price.

Quantity Adjuster

Buyers or sellers that have low market power, and can only affect supply or consumption.

Utility

A desirable outcome.

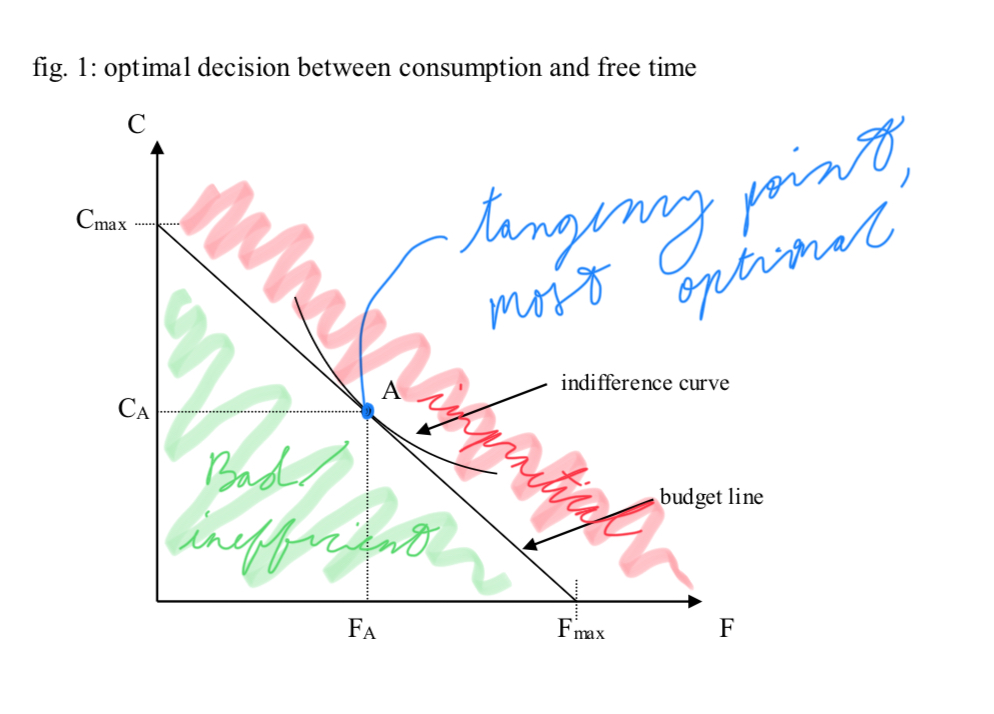

Budget Line

The graph of all combinations of consumption and free time that an actor can afford within a budget constraint.

Abscissa

X on an axis, the horizontal axis

Ordinate

Y on an axis, the vertical axis

Utility maximization

The optimum combination of consumption and free time.

Indifference Curve

Used in a neo-classical labor market to graph the combinations of consumption and free time a household wants to realize. The closer it is to the origin, the lower the level of utility.

Tangency Point of consumption and free time

The most optimal point (intersection) on a graph of a budget line and indifference curve.

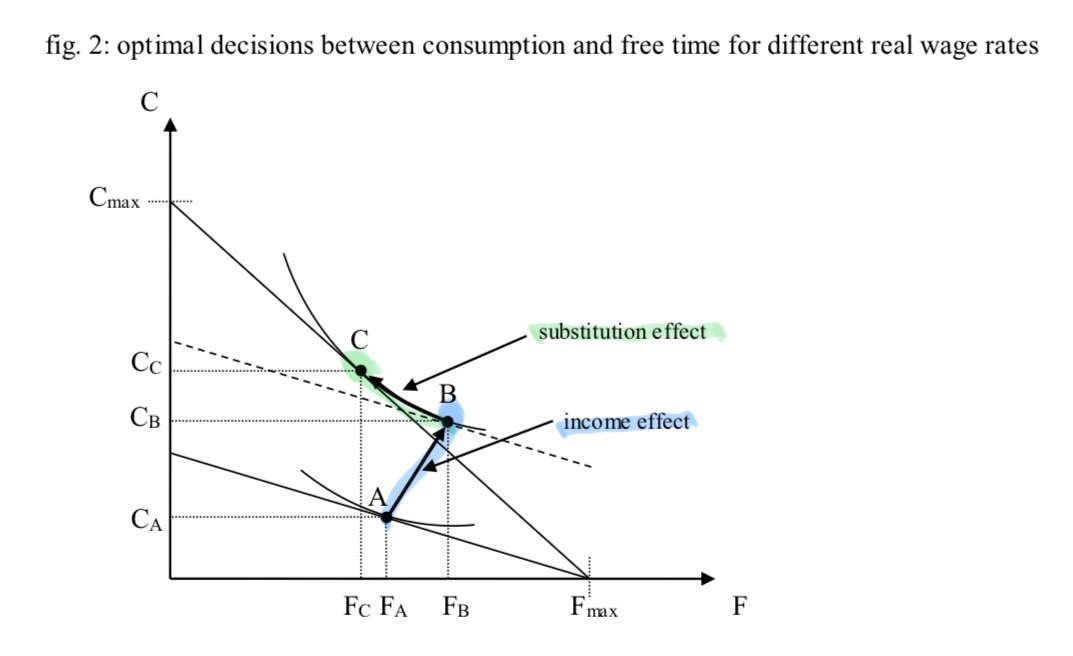

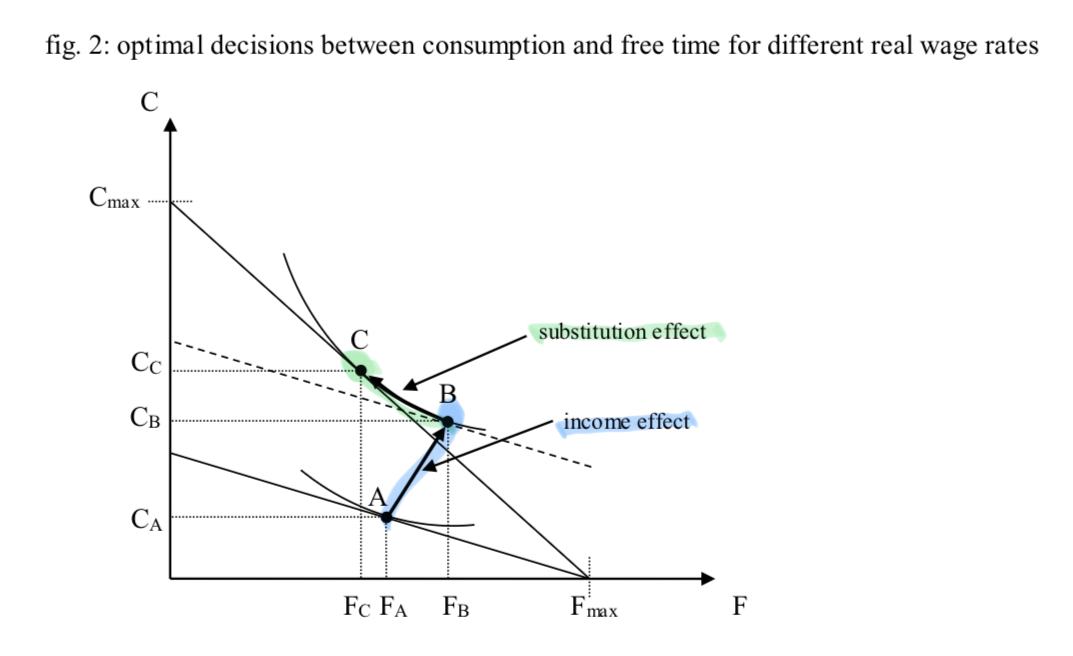

Real Wage Rate (W/P)

wage earned per unit of time, often working hours

Substitution Effect for wages

Observed when a household substitutes free time for more working time because of an increased wage rate, which increases the opportunity cost of free time.

Opportunity Cost

Value lost by choosing one option over another.

Income effect on wages

Observed when a household increases free time due to an increased wage rate, because the same level of consumption can be maintained with fewer working hours.

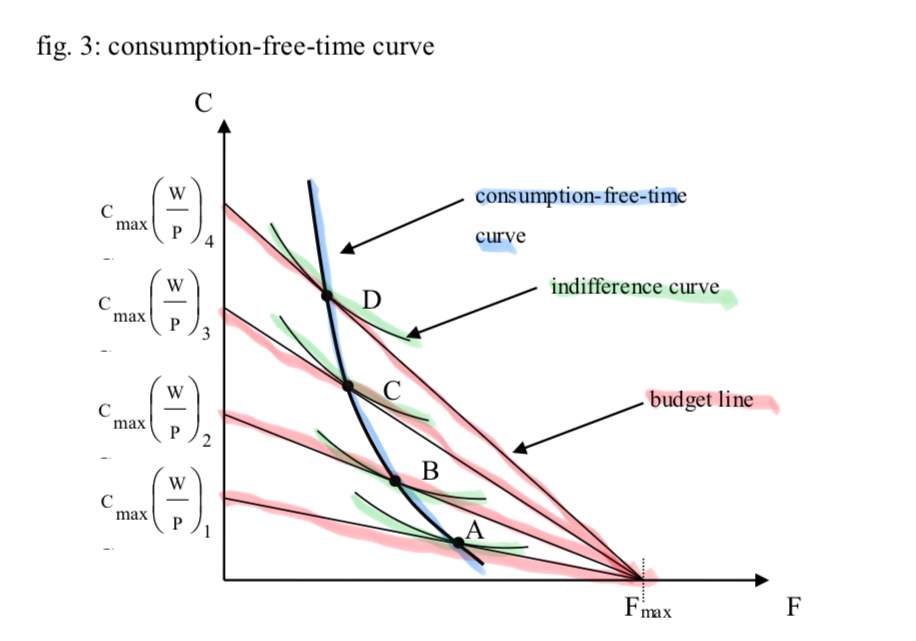

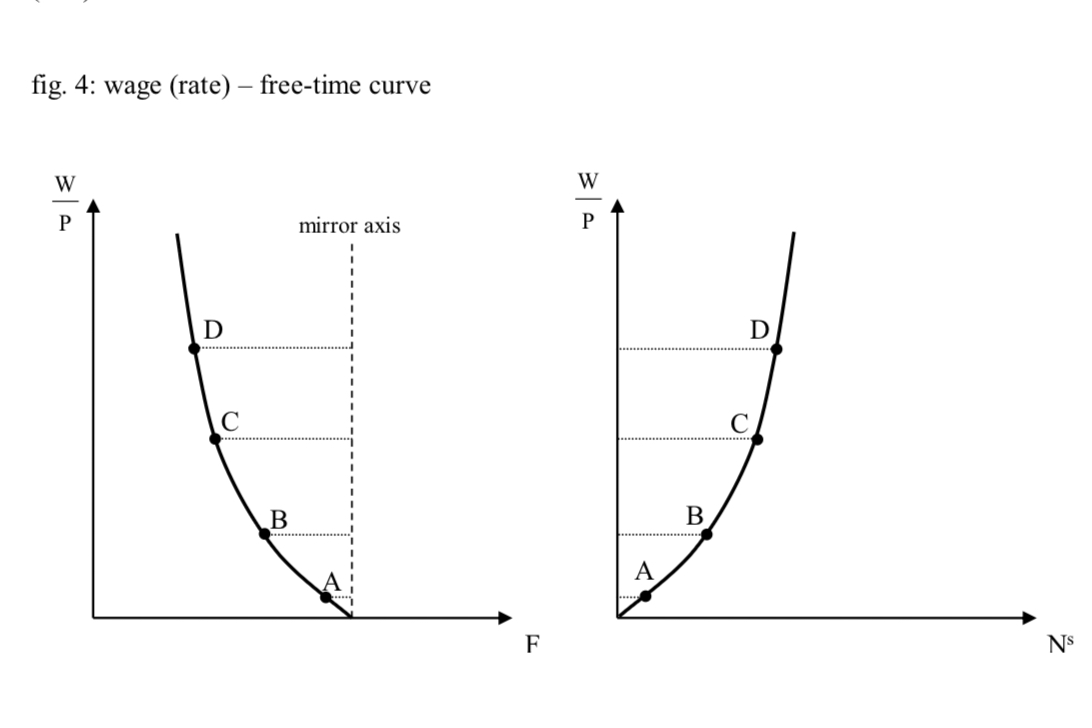

Consumption-Free Time Curve

Graph of all combinations of free time that maximize utility of a household for different wage rates.

Wage-(Rate) Free-Time Curve

Graph of the measurements of utility for real wage rates (ordinate) and free time (abscissa)

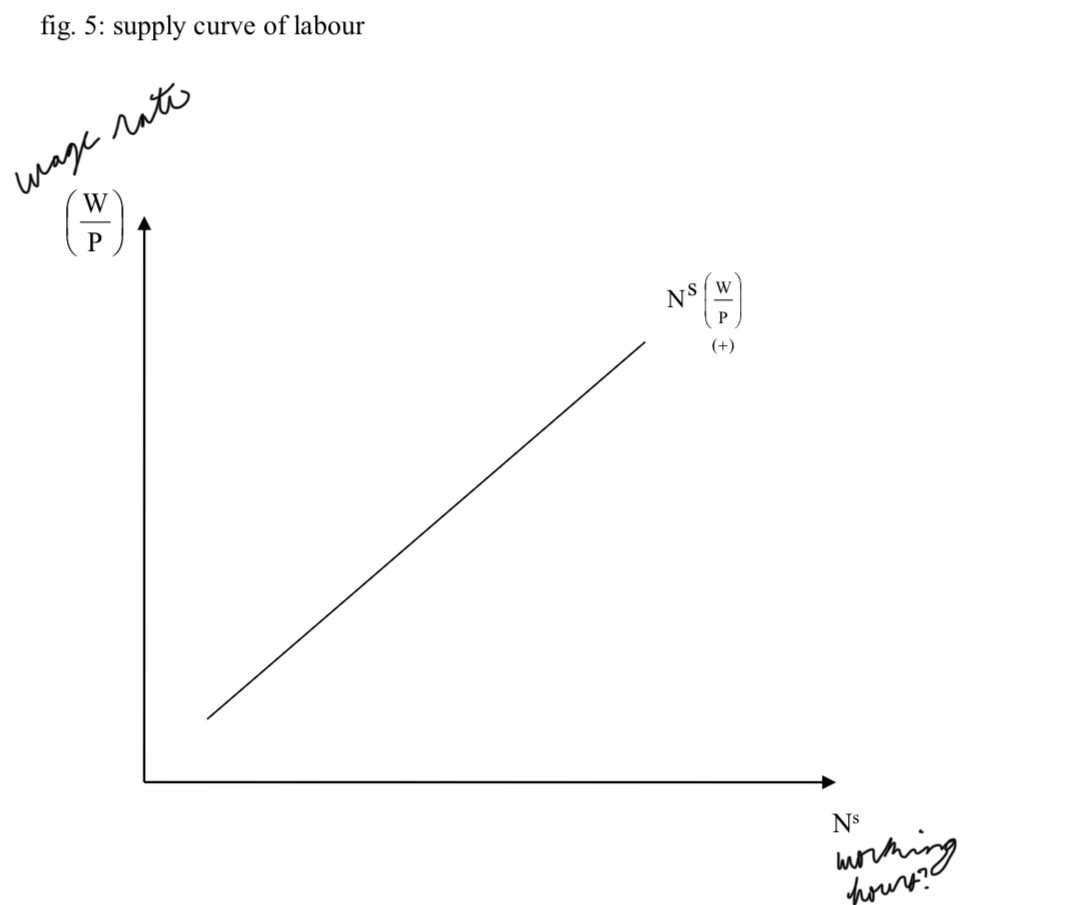

Supply Curve of Labor

Graph of all combinations of real wage rates (ordinate) and working hours (abscissa)

Dependence of Labor on Real Wage Rate

Ns=Ns(pw)+

Profit Equation

π=P⋅y(+N)−W⋅N(PW)

1st Derivation of the Profit Equation

dNdπ=P⋅dY−W⋅dN=0

Neo-Classical equation for optimal labor demand

dNdY=PW

2nd Derivation of the Profit Equation

\frac{d^2Y}{dN^2}<0

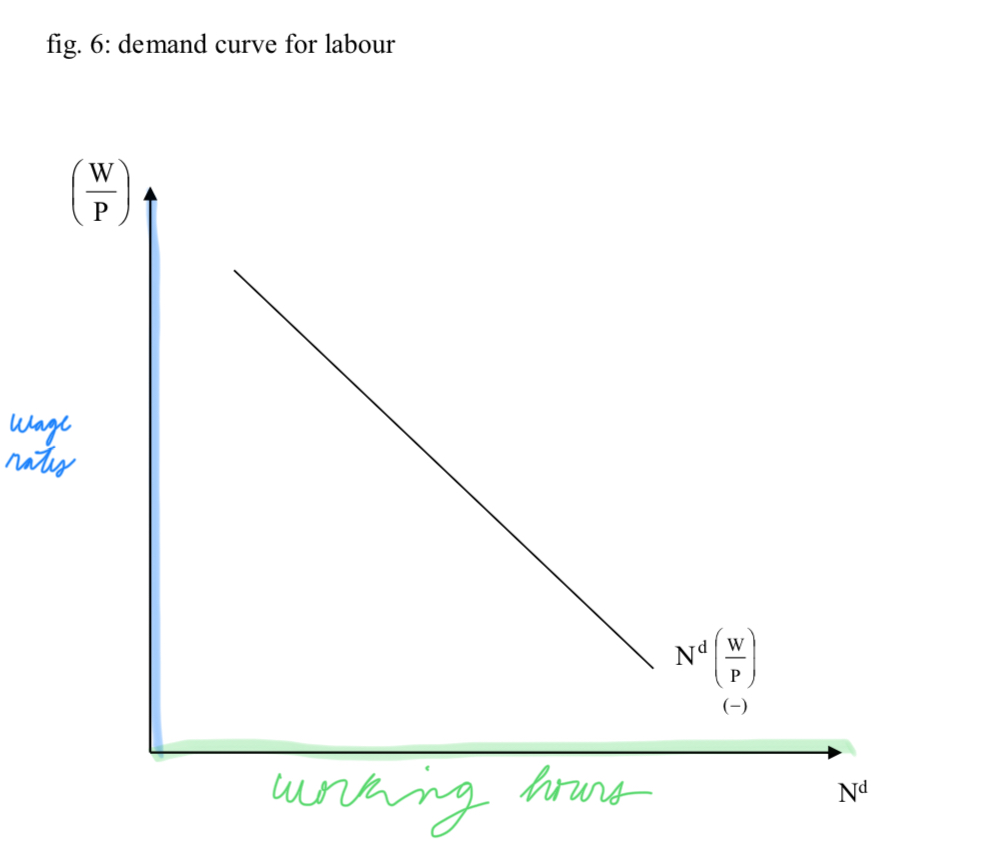

Demand Curve for Labor

Graph of all combinations of real wage rates and working hours that maximize the utility of a private entrepreneur.

Dependence of Demand for Labor on Real Wage Rate

Nd=Nd(PW)−

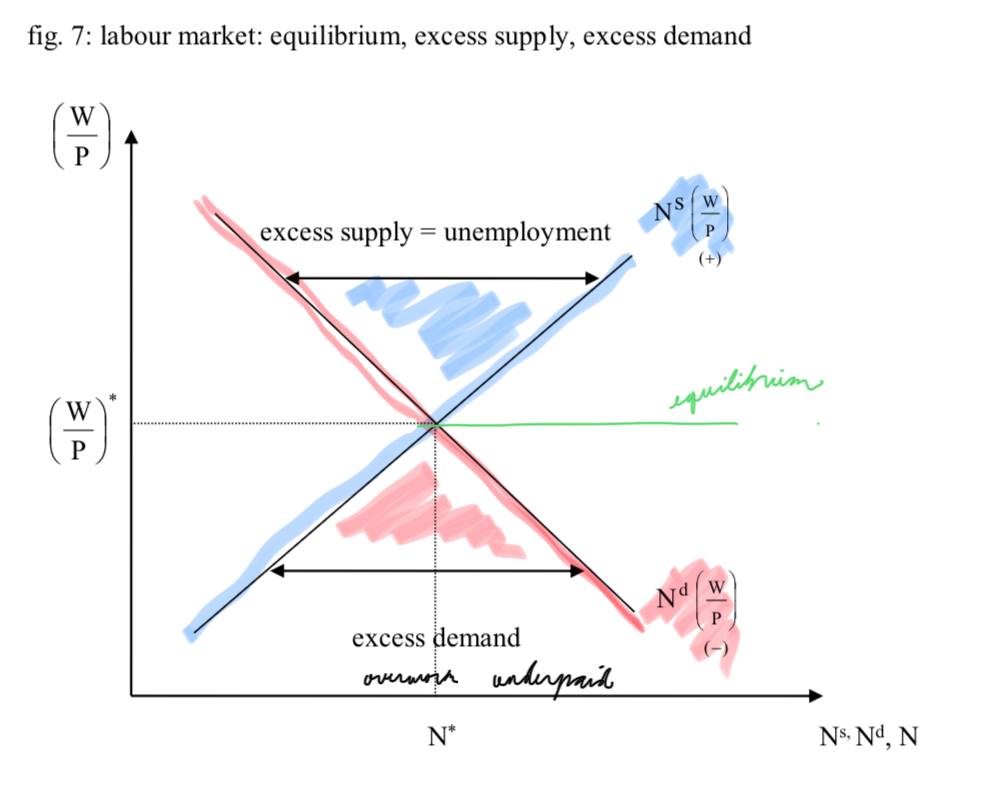

Equation for Equilibrium in the Labor Market

Ns(PW)+=Nd(PW)−

Equilibrium in the Labor Market

The labor market reaches equilibrium when the supply of labor is equal to the demand for labor.

Supply and Demand Curves of the Labor Market

The labor market reaches equilibrium when private households’ supply of labor (positively dependent on W/P) is equal to private entrepreneurs’ demand for labor (negatively dependent on W/P). Above the equilibrium there is excess supply, because employees ask for high wages. Below the equilibrium, there is excess demand, because employers offer wages that are too low.

Objective Theory of Value

“Natural Prices” can be derived from cost factors, “Natural Goods Prices” are determined by production costs, “Natural Interest Rates” by capital costs, “Natural Wages” by labor costs.

Subjective Theory of Value

Market Prices are the result of the relationship between supply and demand.

Say’s Law

Under optimal market conditions, each unit supplied of a good creates demand for another unit of the good.

Real Wage Rate Definition

Wages that are adjusted for purchasing power/inflation, wages that are measured in terms of utility

Nominal Wage Rate Definition

Wages that are measured in terms of amount earned per unit of time, without adjustment.

Production Function

Y=Y(N)−

Equation for aggregate demand in a closed economy

Yd=C+I

Dependence of consumption on interest rate

C=C(i)−

Dependence of Investment on interest rate

I=I(i)−

Walras’ Law

Any excess demand in one market is compensated for by an excess supply in another market

Dependence of Savings on interest rate

S=S(i)+

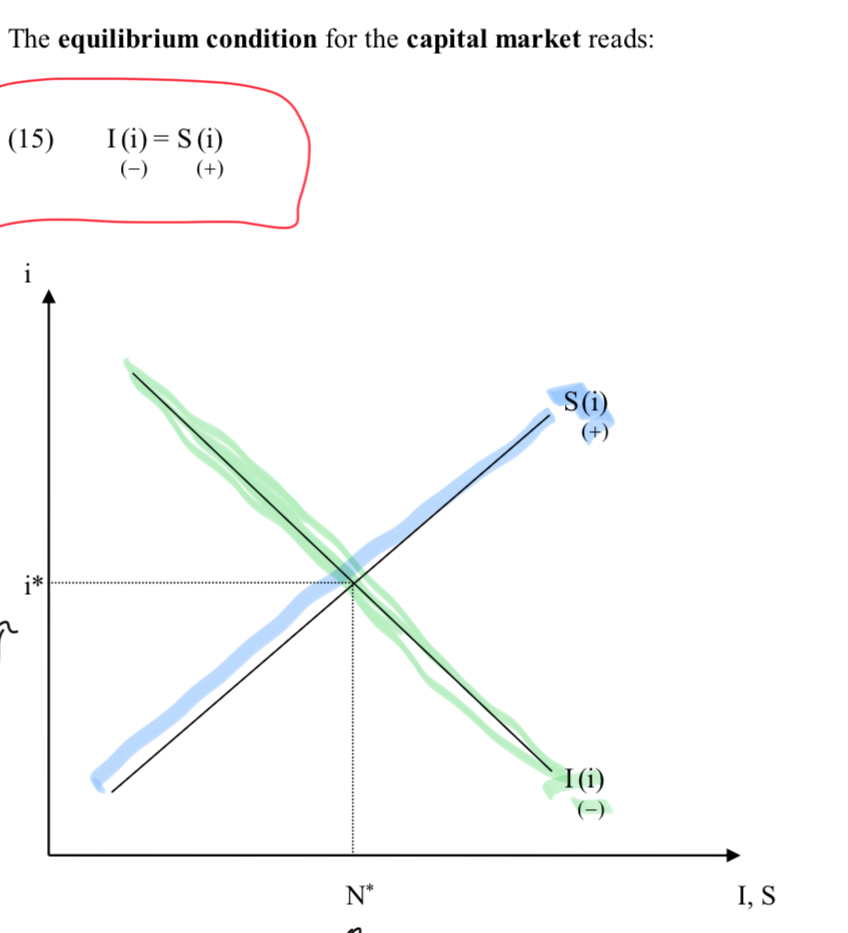

Equilibrium condition for the capital market

I(i)−=S(i)+

graph of capital market equilibrium

when the savings curve intersects with the investment curve

Equation for nominal demand of money

L=k⋅P⋅Y

Equilibrium condition of the money market

M=L

Cambridge Equation

M=k⋅P⋅Y

Quantity Equation/Fisher Equation

M⋅v=P⋅Y

definitional equation of nominal wage rate

W=PW⋅P

equation for optimum nominal wage rate

W∗=(PW)∗⋅P∗

Equilibrium Condition in the goods market

Ys[N(PW)]=C(i)−+I(i)−

endogenous variables

a variable whose measure is determined by the model using it

exogenous variables

variables whose measure is determined outside of a model and is used in the model

Functions of money

medium of exchange, unit of account, store of value

quantity theory of money (classical-neo-classical)

Assumes the cash holding coefficient (k) and the velocity of money (v) are fairly stable. Real output (Y) has been pre-determined by the labor market and production function. Therefore, doubling quantity of money (M) results in doubling price level (P), but only monetarily.

classical dichotomy of the monetary and economic sphere

monetary stimuli do not have an effect on the overall economy

The Cambridge Effect

A rising supply of money means cash holding is too high. Buyers raise demand for goods, but supply does not change, so prices go up. The process repeats until real cash holding returns to initial levels.

Labor Market

The economic area concerned with the balance between wages, working hours, free time, and the supply and/or demand of labor.

Goods Market

The economic area concerned with production, supply, demand, and consumption of goods and investment.

Capital Market

The economic area concerned with savings and investment.

Monetary Market

The monetary area concerned with the supply, demand, quantity, holding, and velocity of money.

Income-Expenditure Model

A Keynesian Model for the goods market, where investment and government expenditure are exogenous, while consumption and savings are endogenous.

components of aggregate demand

private demand and and demand for consumption by private households and demand for investment by entrepreneurs, plus government expenditures and foreign demand

Autonomous Consumption

A concept in Keynesian Economics, the base level of consumption one must do to survive

Income-Induced Consumption

A concept in Keynesian Economics, the tendency for consume in proportion to income

Absolute Income Hypothesis

the question of how a consumer divides their resources between savings and consumption

Average Rate of Consumption

measures the ration of total consumption to total income

Marginal Rate of Consumption

measures ratio of additional consumption to additional income

Keynes’ Fundamental Psychological Law

Additional income is not entirely spent on additional consumption. Income and consumption do not increase at the same rates. Graphically, the marginal rate of consumption is more than zero but less than one.

Two parts of savings

Autonomous savings and income-induced savings

Autonomous Savings

Funds set aside to pay for Autonomous Consumption, really a “dis-saving” value

income-induced savings

the increase in savings as a result of increased income and propensity to save

average rate of savings

ratio of total savings to total income

marginal rate of savings

ratio of additional savings to additional income

marginal productivity of capital

additional productivity from adding one unit of capital, ceteris paribus

marginal efficiency of capital

expected rate of return and expectation of yield per additional unit of input

internal rate of return

the rate of return where the costs are equal to the expected present value of all discounted future revenues

investment trap

where interest rate elasticity is zero.

interest rate elasticity

sensitivity of economic factors to changes in interest rates

ISLM Model / Hicks-Hansen Model

The most popular macroeconomic model, which assumes a closed economy, constant price level, and ignores government financing.

IS Curve

the geometric locus of all combinations of interest rate and income that represent equilibrium in the goods (capital) market

LM Curve

the geometric locus of all combinations of interest rate and income that represent equilibrium in the money (bond) market

Simultaneous Equilibrium

the intersection of the IS and LM curve, when there is equilibrium in the goods (capital) and money (bond) markets

monetary policy

policy concerned with the money supply

expansionary monetary policy

policy that increases the money supply

effectiveness of monetary policy

monetary policy is more effective when the interest rate elasticity of demand for investment is higher or the interest rate elasticity of the demand for money is lower

investment trap

keynesian special case where the interest rate elasticity of demand for investment equals zero

liquidity trap

Keynesian special case where there the interest rate elasticity of demand for investment is approaching infinity

fiscal policy

policy concerned with government spending

expansionary government spending

policy that increases government spending