Accounting Exam 1 & 2

1/82

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

83 Terms

Accounting

information system to measure business activities

The Accounting Equation

Assets = Liabilities + Shockholders’ Equity

The Entity Assumption

any organization (or person) that stands apart as a separate economic unit.

Historical Cost Principle

Assets should be recorded at their historical (original) cost on the date of purchase

The Stable-Monetary-Unit Assumption

Accountants assume that the dollar’s purchasing power is stable over time. (We ignore inflation)

examples of Assets

prepaid expenses, accounting receivable, cash, inventory, etc.

Assets

Things the company owns (economic resources)

examples Liabilities

note payable, long-term debt, accounts payable, ANYTHING PAYABLE (money you need to pay)

Liabilities

money you own (debt)

examples of Equity

common stock, revenue, expenses, dividends, etc

Equity

remaining assets available to stockholders

current assets

resources used for less than a year

long-term liabilities

debt to pay off for more than a year (bonds payable, notes payable)

Current liability example

Accounts payable, accrued liabilities, and unearned revenue

The Income Statement

shows a year’s worth of financial actives

The Income Statement equation

Revenue - Expense = Nest income (or Net loss -)

The statement of retained earnings

shows what the company did with the earns

The statement of retained earnings formula

beginning retained earnings

( + net income or - net loss)

-dividends declared

The balance sheet

reports assets, liabilities, and equity

statement of cash flow

shows cash receipts and cash payments

transaction

any event that has financial impact

T- account

tracking of accounting balances

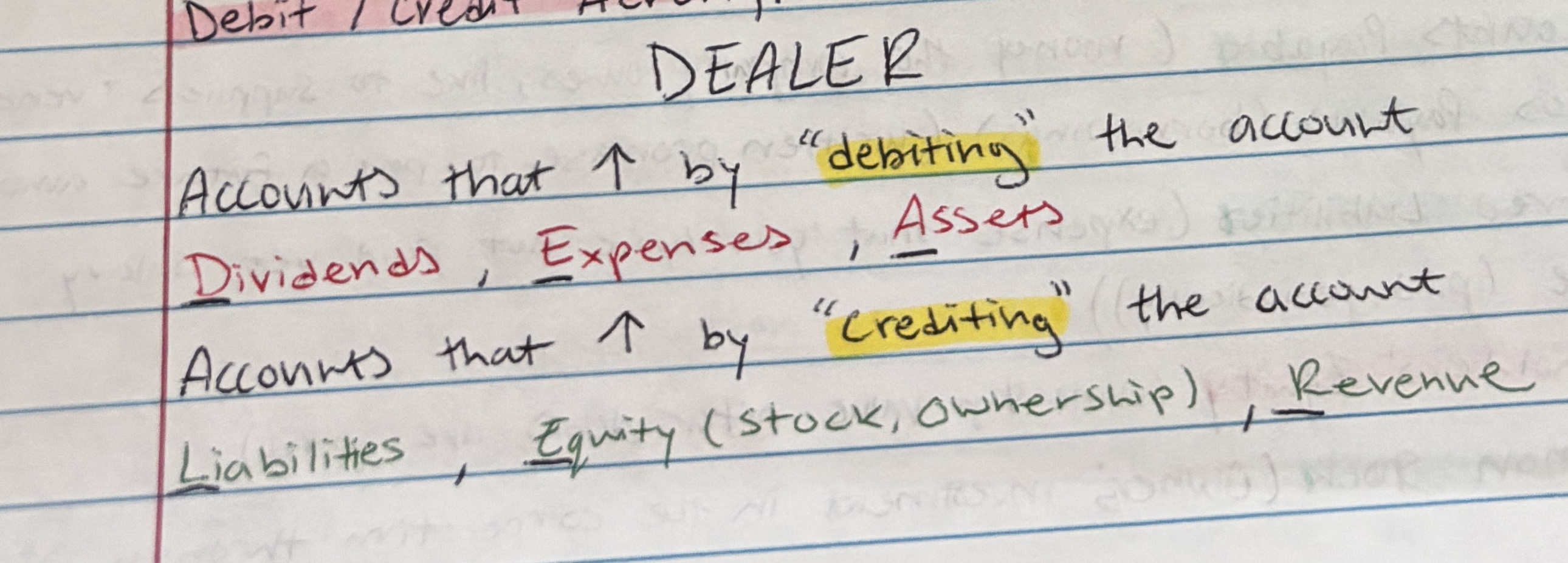

debit is on the

left side

credit is on the

right side

DEALER Acronym means

Proprietorship

single

Liable for business debt

General partner ship

2 or more

Make agreements that legally bind all parties (a disadvantage)

Corporation

stockholders

No personal obligation for the businesses debt

Double taxation (a disadvantage)

debit =

credit

End Bal =

Beg Bal - Cash receipts + cash payments

if the account is high, then there is an

overstated

if the account is low, then there is an

understated

Cash-basis accounting

records only cash transaction

Accrual accounting

Impact of a business transaction

Revenue Principles

Revenue is recorded when it has been earned (when service has been performed)

Expense Recognition Principle

Expenses are recorded when incurred and recognized

Accrued expense

An expense that has not yet been paid

Accrued revenue

Revenue that has been earned but not collected

Closing the books

preparing the accounts for the next period’s transactions

Temporary Accounts (limited period)

Revenue

Expense

Dividends

Permanent Accounts

Assets

Liabilities

Stockholders Equity

Current Ratio - reflects operating liquidity

Total current A / Total current L

Debt Ratio – Measures debt-paying ability

Total L / Total A

Net working capital - how fast an asset can be converted to cash

Total current A - Total current L

Retained earnings have 3 things

Revenue, expense, and dividends

Stockholders equity what 2 accounts increase when debited

Dividend and expense

Net Working Capital – Calculated dollar amount that represents operating liquidity

Total current A - Total current L

Bank statement balance - cash book balance =

The difference (error)

Adjusted bank balance =

Adjusted book balance

Adjusted bank balance has:

beginning balance

Deposit in transit

(-) Outstanding checks

(+-) Bank error

Adjusted book balance

beginning balance

Bank collection

Entrance revenue

EFT receipt (electronic movement of money from one one bank to another)

(-) bank service charge

(-) NSF Check (check bounced)

(-) EFT Payment

(±) bank error

Misappropriation of assets

Steal money from the company then cover it up

Fraudulent financial reporting

Makes FALSE entries in the book to make it look better

The fraud triangle (motive)

Why they did it?

The fraud triangle (opportunity)

Had too much power given

The fraud triangle (rationalization)

“Everyone else is doing it”

For the adjusted book side only

Requires journal entry

Internal control

A way to stop fraud

Separation of duties

Separate handling and signing of checks and etc.

Revenue principle

Revenue is recorded when earned

FOB Shipping

Recognizing when goods LEAVE the shipping dock

FOB (free on board) Destination

Recognize when good is DELIVERED to customer

2/10 means

2% off discount and within 10 days

n/30 means

If the payment is not due at a certain time, they have until 30 days for full payment

Discount =

Price • %

Amount to pay =

Price - discount

Write off does not

affect net receivable

What decreases accounts receivable

Collections of cash and write offs

Specific identification method

Tracks each inventory item

Average cost method

Calculates cost of goods

Average cost method =

Cost goods available / # of units available

First in, first out method (FIFO)

First to come in it’s the first to come out

Last in first out method (LIFO)

Recent purchase items are sold first

COGS (cost of good sold) (Credit)

Number of units sold • average cost per unit

For FIFO, cost of ending inventory

Unit cost (purchase) • number of ending inventory

Allowance for Bad debit

The amount of accounts receivables the company does not expect to collect

Allowance for Bad debit (Creditable) formula

Interest income formula

Inventory (what we sell to customers) formula

Net realizable value

Amount of accounts receivables the company expects to COLLECT

Net realizable value formula

Accounts receivable - allowance of bad debt (estimated uncollectible x sales revenue)

Bad debt expense formula

Net credit sales x estimated uncollectible (%)

Percent of sale method

Estimates a business bad debt expense as a percent