Investments - Financial Statement Analysis

1/22

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

23 Terms

Financial Statements

Primary information that firms publish about themselves

Users of financial statements

Investors

Government

Regulators

Employees

Managers

Courts

All companies listed for public trading in the US must provide

Balance Sheet

Income Statements

Cash Flows Statement

Statement of Shareholders’ Equity

File annual 10-K report with the SEC

File quarterly 10-Q report with the SEC

All these documents are available at the SEC EDGAR database

The use of Financial Statements in Valuation

Multiple analysis

Ratios used in Valuation

P/E, P/B, P/Sales,…

Method of comparables

Basis for fundamental analysis based on

dividends

free cash flows

earnings

Cash Conservation Equation (FCF = d +F) (C - I = d + f)

The cash generated by the business after reinvesting in itself (free cash flow) must equal the net cash paid out to its owners and lenders. Enforces discipline and reality. Highlights sustainability of payouts. Valuation and investment analysis. Detects aggressive accounting or manipulation.

Dividends

If C - I - i > d, then the firm will buy bonds of other firms or its own debt.

If C - I - i < d, then the firm with borrow (issue more bonds) or reduce lending (Treasurer’s Rule)

Ratio Analysis

Payout ratios

Profitability

DuPont Analysis

Financial Leverage

Analysis of credit risk

DuPont Analysis

ROE = Profit margin * Asset turnover * Equity multiplier

Profit Margin

Easy to manipulate. If too high, a competition will arise

Asset Turnover

Difficult to manipulate

Equity Multiplier

A measure of leverage

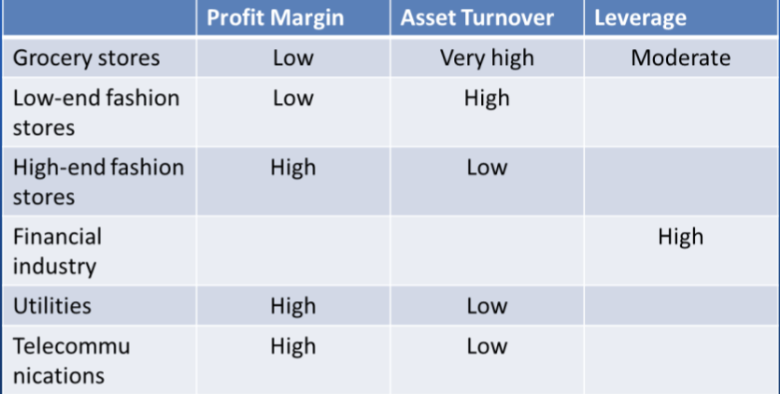

Dupont Analysis for Selected Industries

Financial Leverage

Represents the degree to which a company uses debt to fund its operations, relative to the equity invested by shareholders.

Higher FLEV → more reliance on borrowed money (higher potential returns but also higher risk)

Lower (or negative) FLEV → more constructive financing (or even net lending if the company holds more financial assets than obligations)

Typical FLEV is about 40%

Strong variations in FLEV

Financial Leverage and ROE

Financial Leverage increases ROE only if the operating spread if positive, i.e., RNOA > NOA

If spread is positive, favorable financial leverage or favorable gearing

If spread is negative, unfavorable financial leverage or unfavorable gearing

ROA

ROA mixes operating and financing activities

Poor measure of operating profitability

Median around 7.1% for US non financial firms from 1963 to 2007

RNOA

Appropriately distinguishes operating and financing items

Interest bearing financial assets do not influence the return on operations

Median around 10.5% for US non financial firms from 1963 to 2007

Basic versus diluted earnings per share

Basic EPS is simply earnings available to common shareholders (after preferred dividends) divided by the number of shares outstanding.

Diluted EPS: instead of number of shares outstanding, it uses shares outstanding plus shares that would be outstanding if conversion of stock options and warrants should take place.

Basic EPS should be used for equity valuation.

Analysis of Quality of Financial Statements

The current financial statements are of poor quality if they are not a good indicator of future earnings:

If earnings contain one-time, unusual items

Underestimating bad debt, warranties, deferred revenue or depreciation increases current earnings but lowers future earnings

Earnings Management

Earnings management is a manipulation of earnings:

Manipulated up: borrowing income from the future

Manipulated down: banking income for the future (“taking a big bath”)

How to Detect Accounting Manipulations

Examine possible income shifting

Examine the sales to detect possible manipulation in sales

Examine the OI to detect possible manipulations

Looking for red flags

Manipulation of operating expenses always changes both profit margin and asset turnover but in opposite direction → investigate changes in asset turnover

Be aware of firms that use different accounting methods than is usual in their industy

Analysis of Credit Risk

Liquidity ratios: address short term debt

Solvency ratios: addresses long term debt

Credit Scoring Models

Altman Z-score: indication of the likelihood of a firm not going bankrupt.

Altman Z-Score

Z > 2.99: “safe” zone - low bankruptcy risk

1.81 < Z < 2.99: “Gray” zone - moderate risk, worth monitoring

Z < 1.81: “Distress” Zone - high bankruptcy risk