CB1/COMM1240 Essentials

1/74

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

75 Terms

Treasurer

- The Treasurer

o Manages cash flow and maintaining relationships with banks (ensures access to debt capital)

o Goal is to maintain liquidity, and access capital at lowest cost possible

o Manages financial risk, such as interest rate rises meaning less profit, or change in FOREX affecting export base

The Controller

o Known as head accountant

o Manages internal financial reporting (preparing accurate financial statements) and internal auditing

o Manages accounting risk, such as incorrect reporting to ensure historical accuracy

The Chief Financial Officer

o Executive director, communicates with investors and shapes business long term strategy

o Overall financial health and high (but fair and sustainable) stock evaluation

o Conflict with the boards demands for high dividends (in the interest of shareholders), and re-invest cash into the company

Stratergies to Maximise Shareholder Wealth

- Board Pressure

o Shareholders will apply pressure onto the board of directors, in turn discipline mangers

- Compensation

o By tying shareholder wealth to mangers compensation, such as through stock options, then managers will be more incentivised to serve shareholders’ interests

- Reputational Damage

o Poor performance by managers will damage their reputation and reduce their likelihood of future leadership positions

- Takeover and Acquisition Threat

o If a quoted company is underperforming, and its share price is falling, this makes it vulnerable to a hostile takeover

§ When an external party attempts to take control of a company without approval of board of directors

§ Done by either convincing current shareholders to vote out board, or by buying a controlling stake

o Incumbent managers are then able to be easily replaced

§ Evident in the case of Elon Musk twitter takeover

Four Aspects of Financial Management

How should money be raised for an investment

What investments should be made

How to manage current liabilities and assets

How to pass on returns to shareholders

Expected Return

E(r = (r1 X p1) + (r2 X p2) + …+ (rn X pn)

r = Return of nth outcome

p = Probability of nth outcome

Risk

In finance, risk is a measure of how spread out the return is, around expected return

Use formula for standard deviation

Variance = (r1-r)²(P1)+(r2-r)²(P2)+…+(rn-r)²(Pn)

Portfolios

Expected Return of Portfolio

E(rp) = w1E(r1) +w2E(r2) +…+wnE(rn)

w = Weighting of Portfolio

Variance of Portfolios

Variance = (r1-rp)²P1

Systematic Risk Principle

- The expected return on a risky asset, should only be determined by systematic risk

- Unsystematic risk can be easily eliminated by diversification, and hence shouldn’t be rewarded

- Market only rewards for systematic risk

- Stocks have higher expected return, as they bear greater systematic risk

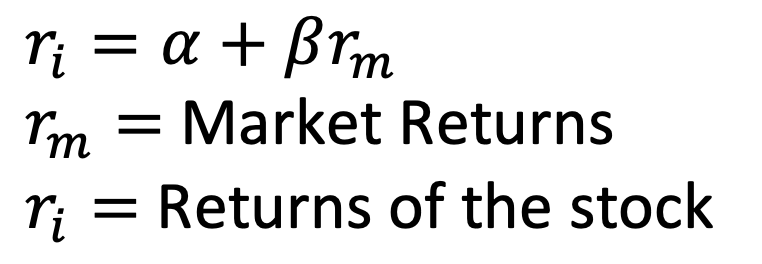

Beta

- The beta co-efficient represents how much systematic risk an asset has, relative to an average asset (a general term for the market, etc the ASX 200)

- The beta measures how responsive a stock is, to changes within said market, ie if , then if the ASX drops 10%, then the stock will drop 1%

- This beta can be used to represent a linear relationship

Bonds

- Long term debt instrument issued by government or corporation

- Owners receive periodic interest payments, before receiving the principal amount (bonds face value), back

Bond Indenture

- Legal agreement that sets out the terms of the bonds

Face Value

- The amount paid when bond matures, and amount used to calculate interest

Coupon Rate

- The annual interest payments, expressed as percentage of bonds face value

Yield to Maturity

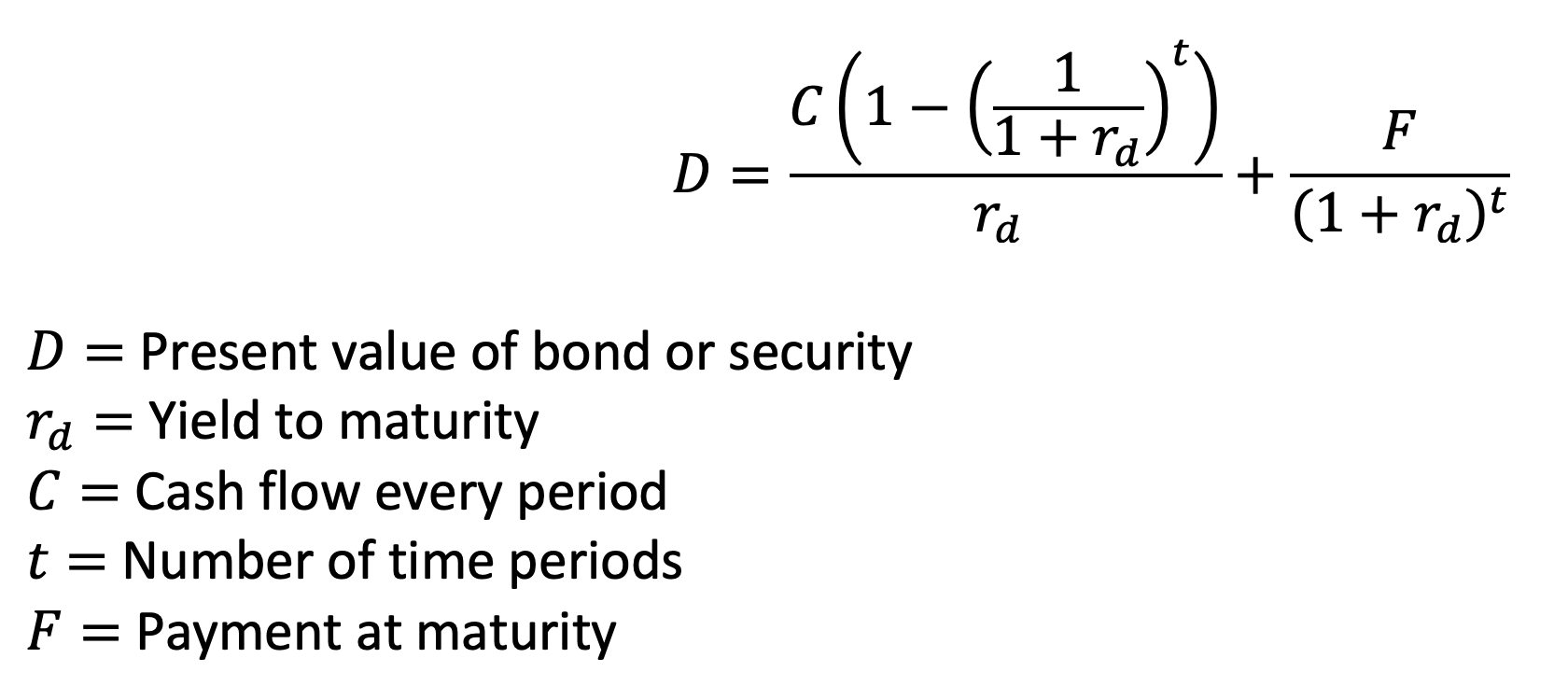

- The discount rate that makes the present value of all future bond cash flows, equal to the current market price

PV of Bonds

PV of Coupon Payments + PV of Bonds Principal

Bond Relationships

Price and YTM

Value of bond is inversely proportional to YTM

- As investors demand higher returns, (ie a higher YTM ratio), then they’d want to buy the bond for a lower price (ie a lower market value)

Coupon Rate and YTM

The market value of a bond will be:

- Greater than face value, if coupon rate is greater than the YTM

o Investors are willing to pay a premium

- Less than face value, if coupon rate is less than YTM

o Investors are willing to pay a discount

Time to Maturity

- As the date to maturity grows closer, the value of decreases

- Meaning the market value of the bond, will approach face value

Interest Rate Risk

- As interest rate affects YTM

o Ie greater interest rates, will increase attractiveness of other debt instruments, leading to greater YTM

Nominal share value

- Minimal amount that a share can be sold for, selling below would be selling share at a discount, and is illegal

Types of Loan

Term Loans

Interest Only Loans

- Interest is paid throughout life of loan, with principal paid back all at end

Amortised Loan

- Interest and a portion of principal paid gradually through life of loan

Deferred Payment Plan

- Loan payments may begin after a certain period, or interest payments may be variable

- Especially useful for projects that won’t expect returns until later

Mortgage Finance

- Type of loan where property is used as collateral

Credit Sale

- An asset is bought in the present, and interest and principal is paid over time in instalments

- Asset is owned from the start

Leasing

- An example of an annuity due, where payment is given first, and then good or service is rendered

Operating Lease

- Asset is rented for a specific period

- The payment is equal to the value of using asset for given period

- Risk usually stays with lessor

o Ie risk of obsolescence, or asset sitting idle

Short Term Finance

Bank Overdraft

- Assist with short term cash flow issues, and is easily accessible

- Often charge higher interest rates compared to a typical loan

Trade Credit

- Allow inventory to be received in advance of payment, assisting with cash flow

Factoring

- Sell companies accounts receivable to a third party for a discount, and receive cash immediately

Bills of Exchange

- Involve the

o Drawer

§ The seller who writes the bill, stating an amount to be paid after a period

o Drawee

§ The buyer who agrees to pay the bill after a period

o The Payee

§ Who holds the bill at maturity

o Example

§ If Bob sells $100 in goods to a retailer, but the retailer can’t pay currently, then Bob may write a bill of exchange, stating the retailor must pay in a certain period

· Bob is the drawer

· Retailor is the drawee

§ Bob can sell the bill of exchange to a bank, and receive $95

· The bank is the payee, as they hold the bill at maturity

Private Equity Market

- A funding source that doesn’t involve the publicly issuing shares

- Usually used for start-ups, or companies in distress

o Bain in 2020 bought Virgin Aus out of administration

- Funds provided by PE own funds, superfunds, life insurance companies

o Undergo a mix of raising funds, and sourcing funds

Types of Private Equity

- Venture Capital – small start-ups

o Invests in startups before profitable, different VC specialise in different stages

§ A seed – Initial investment

§ Early stage – Breakeven point

§ Late stage – Helping companies grow

- Growth Capital – company is growing, but needs more cash

- Mezzanine Financing – an in-between

- Leveraged Buyout – purchasing a mature company, and injecting more capital to help expansion

- Distressed Buyout – purchasing a company in crisis

Tax Systems

Classic System

- Income is subject to double taxation

o Once at company level

Modified Classic System

- Dividends taxed at a preferential rate compared to other income

Full Imputation

- Tax credit given to shareholders for tax on profits already paid

o In Australia, main example is franking credits

Partial Imputation

- A partial tax credit given to shareholders for tax on profits already paid

Partial Inclusion

- A portion of the dividends received are included as taxable income for shareholders

Split Rate System

- Company is taxed at different tax rates depending on if they retain the income, or pay it out to shareholders

o Retained profit taxed at higher rate

No Dividend Tax

- Dividends aren’t taxed at all for shareholders.

Corporate Deductions

- Deduct value of dividends, thus reducing taxable income and overall tax paid.

Reasons for seeking a quotation on stock exchange

Raise Capital

- Access large amounts of funding from public investors

- Easier to raise capital in future with a known cost

Liquidity

- Existing shareholders can buy and sell their shares almost instantly

Profile and Prestige

- Listing shares can increase companies’ visibility and credibility

Employee Incentive

- Provide more diversified compensation for employees, and executives

o Rewarding results, aligning shareholder value

Exit for Founders and Early Investors

- As stock exchange are liquid, founders and investors can exchange their share for cash

Debentures

- Type of bond issued on corporate bond market

- Long term debt instrument issued by a company to raise capital

- Have a higher claim over companies’ assets, compared to unsecured debt holders

Preference Shares

- Type of share that, carries no voting power, generates lower returns, and sits between debt and regular shareholders in being paid out, usually receive fixed dividends

- Uncommon as

o Not tax advantageous, compared to interest which can be tax deducted

o Little incentive for investors, as fixed dividend, and no voting power

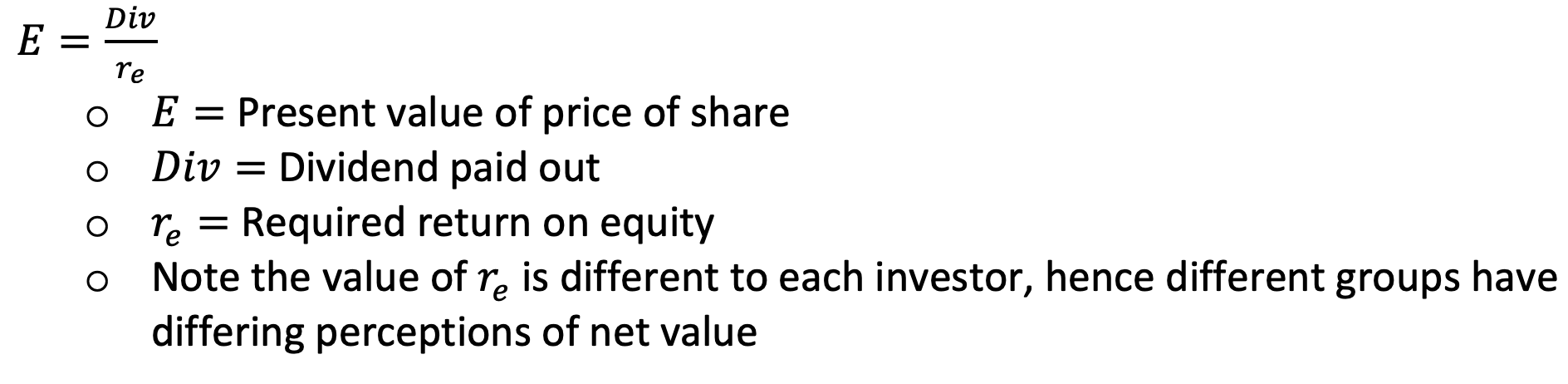

Constant Dividend Model

Used when dividends paid are constant, and unchanging

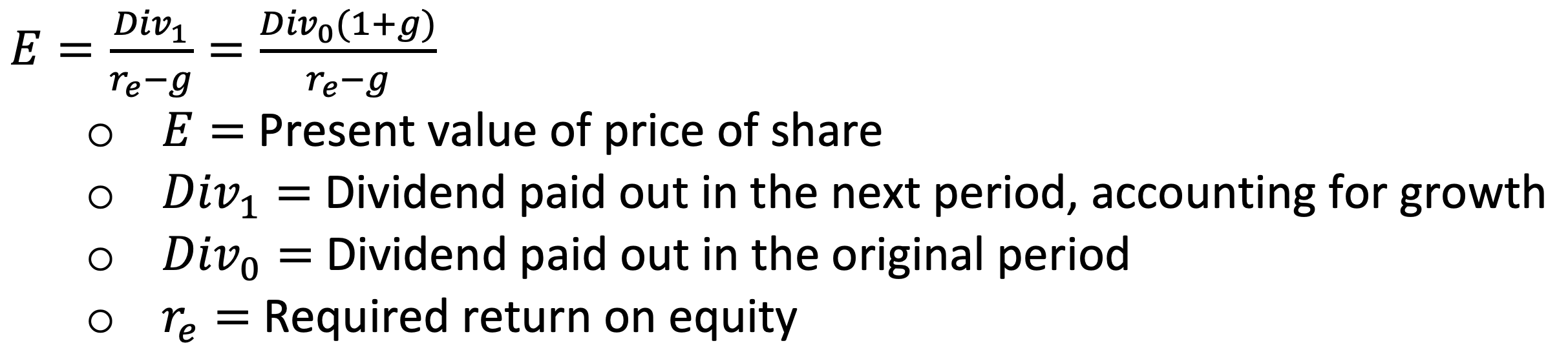

Dividend Growth Model

Used when value of dividends being paid out, is increasing at a constant rate

Valuing Stocks Using Multiples

For example

Value of Share = (Price to Earnings Ratio)*(EPS)

Financial Futures

- A binding contract to buy and/or sell an asset at a set price, at a date

- Provide certainty for both sides, help with budgeting, no need to physically store assets, protects against price shocks

- Common uses include

o Commodities, ie an airline buying jet fuel

o FOREX

Options

- Pay a premium for the right to purchase at a later date

- Call Option

o Right to buy at a strike price

- Put Option

o Right to sell at a strike price

- Strike Price

o Pre-agreed on price, when this price is reached then seller has right to sell, and buyer has right to buy

Interest Rate Swaps

Allow loans to be swapped, for example from a floating to an exchange

- Occurs between company and bank

Can occur between companies, ie one bank is 6% fixed, one is 4% floating

- They can agree to swap future cash flow

Exchange Rate Swaps

Allow companies to access cheaper capital

- Ie an Aus company needs to borrow USD, likewise US company needs to borrow AUD

o However, as each company is new to market, they’ll face high costs of borrowing

o The two companies can collaborate, and take on a loan in each country, on their behalf

o The Aus company can pay the US companies debt obligations in USD, and vise versa

Obtaining Quotation for Securities

Offer for Sale at a Fixed Price

- Sell share at fixed price, this the usual method

Offer for Sale by Tender

- The minimum price that clears all the shares, ie what price will investors be happy to buy all the shares

Offer for Subscription

- Company offers shares directly to public

Placing

- Equity offered to institutional investors, ie pension funds

Introduction

- Acts as a replacement for IPO, allow any existing shares to be traded on a stock exchange

o Etc, an American company on the NASDAQ, can be introduced to the ASX

Rights Issue

Rights Issue

- Allow existing shareholders to purchase newly issued shares on a pro-rata basis, meaning they can buy new shares for a cheaper price

o Can buy a specified number of shares, at a specified price

- This designed to reward loyalty to the company

Effects

- Dilute ownership for shareholders who do not partake

- Decrease in share price

- Send signal company believes stocks are undervalued

Types of Rights Issue

Renounceable

- Existing shareholders can sell their right to buy discounted shares to others

Non – Renounceable

- Rights may not be sold to others by existing shareholders

Role of Underwriting

Underwriters

- Usually the big investment banks, ie Goldman Sachs

o Advise on pricing, timing and method (ie auction or fixed price offer)

- Provide confidence to company offering the IPO, that they’ll raise the full amount by buying any shares that haven’t been bought

o Underwriters don’t hope to purchase the shares as it exposes them to risk

o The discounted price in which they purchase at, is compensation for being exposed to that risk

Fully Subscribed

- The public has bought all shares, the underwriter can collect their commission

Partly Subscribed

- The public hasn’t bought all shares, underwriter still collects fees but now must buy all remaining shares at the agreed price

Types of Underwriters

Firm Commitment

- Underwriter will buy all remaining shares, and assume financial responsibility if unable to sell

Best Effort

- Underwriter sells as much shares as possible, but if underwriter unable to do so, then shares can be returned

Dutch Auction

- Offer price is set based on competitive bidding by investors

WACC

Interpreting the WACC

- The WACC is the percentage return the firm must earn on assets, to maintain stock

Evaluating Performance with WACC

- If cash flows exceed WACC, value is being created

- If cash flows below WACC, value is being lost

Maximising value with WACC

- Firm value is maximised, when WACC is minimised, this is because:

o A low WACC reduces amount needed to be paid to debt and equity holders

o WACC is used to discount general cash flows, hence lower WACC reduces how much it is discounted

Tax Shield

As debt is able to be tax deducted, the cost of debt can be reduced

Factors Affecting Dividend Policy

Opportunity Cost

- If investors see better opportunities elsewhere, then dividends should be paid for those

Reputation and Market View

- Strong dividends indicate the company is in a strong financial position

Cash Reserves

- If companies have surplus cash, then they have greater ability to provide dividends

Other Opportunities

- If there are projects which could generate greater return in future, then companies should invest in those

Taxation

- Dividends are preferred if they are taxed at a preferential rate, this is the case with franking credits

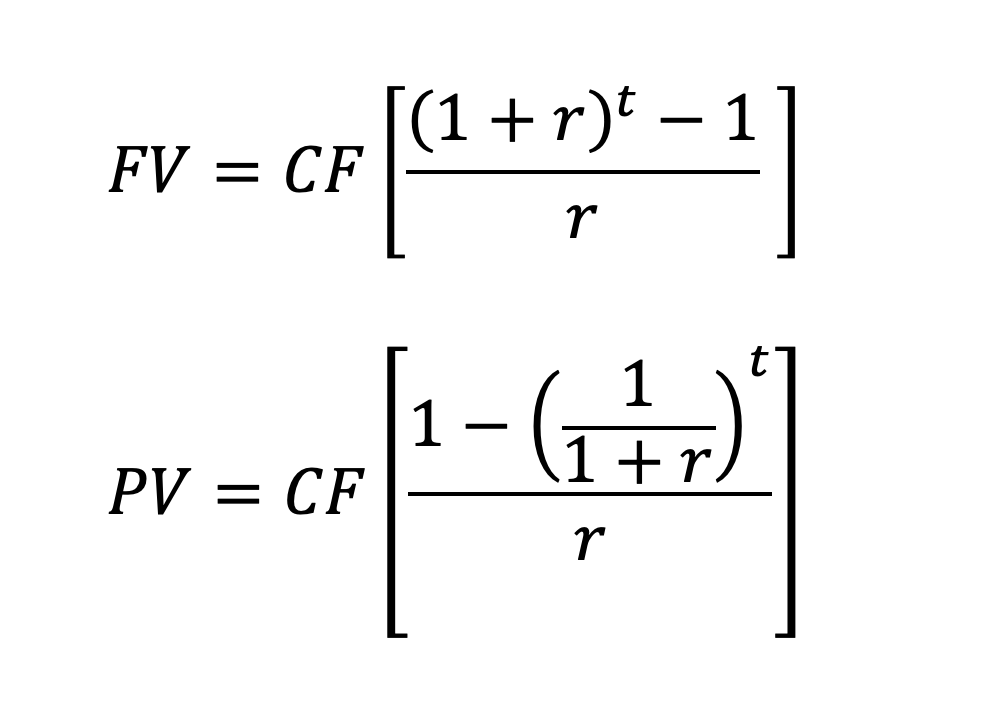

Ordinary Annuity

In certain conditions, discounting can be combined into a single formula, must fit the criteria

Fixed period, cash flows will end eventually

Regular intervals

Fixed payment

Annuity Due

A cash flow is made at the beginning of each period, the formula accounts for an additional period of discounitng

Growing Annuity

Cash flow grows at fixed rate

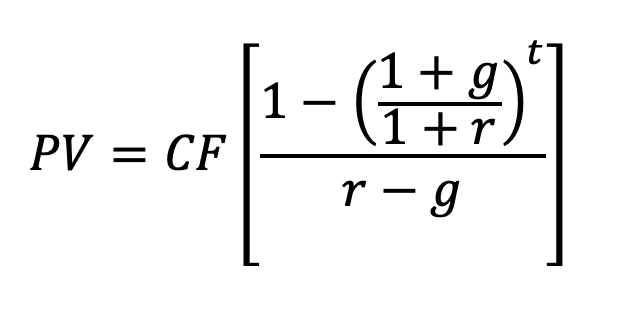

Perpetuities

Growing with Constant Cash Flow

Where cash flows go on forever, and t approaches infinity.

PV = CF/r

Where

Growing with Growing Cash Flow

Cash flows till go on forever, however the rate of said cash flows increase

PV = CF/(r-g)

Net Present Value

The difference between the present value of cash flows, and the cost of the initial investments (which of course occurs in the present)

Discount Rate

- Reflects the risk of the investment, the time value of money, and other potential investments

- Common choices for discount rate include WACC, or cost of equity, will depend on the context

Internal Rate of Return (irr)

The rate which sets NPV = 0

Problems with IRR

there are more than two time periods, ie t>2, then it’ll be very difficult to solve.

- When attempting to solve for , there will be multiple solutions and difficult to distinguish which one is correct

- Especially true when cash flows are changing signs throughout a projects cycle

When projects are mutually exclusive, ie an investor can pick one or the other, but not both

- A high IRR doesn’t mean anything if the cash flow is low

- gives a better picture of the total value of the investment

Profitability Index

A ratio that compares the value of future investments, over an initial investment made today.

PI = (Present Value of Future Cash Flows)/(Initial Investments)

Payback Period

Measures the time required to recover the initial cost of the project.

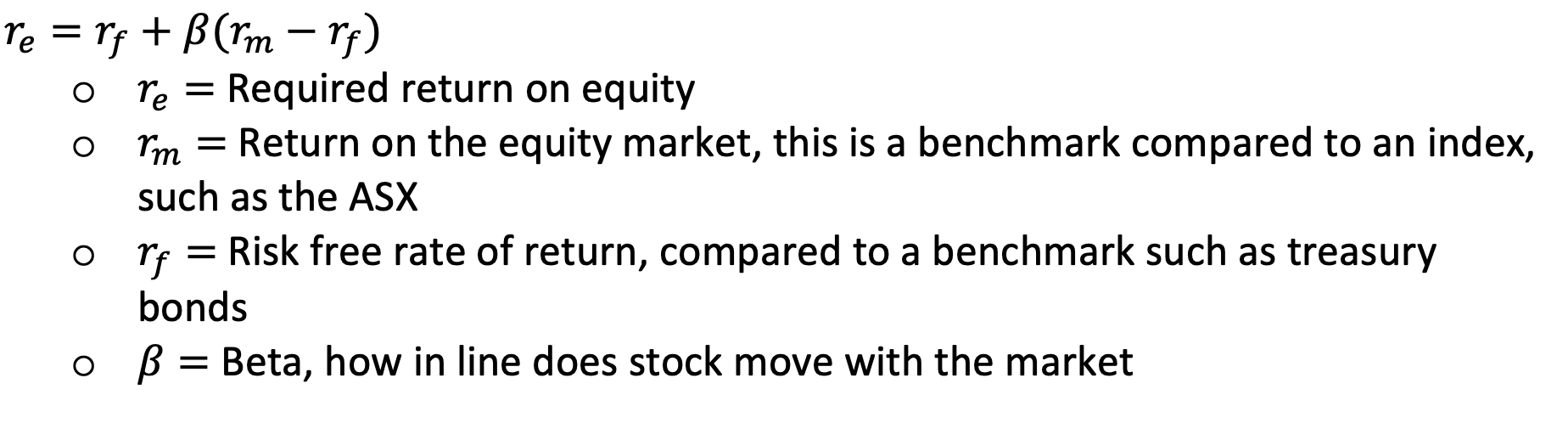

Capital Asset Pricing Model

- Estimates expected return on investment based on its riskiness, in comparison with rest of market

Finding Beta

Beta = (Covariance)/(Market Variance) = How much stock and market move together / How much stock market moves on its own

Monte Carlo Simulations

- Assigns a probability distribution to each variable, such as sales, interest rates, inflation, costs

o ie you think sales could be $1 million, but there’s an 40% chance it could be $900k

- Runs large quantity of simulations in computer, finding all possible outcomes, then computing the net present value for each scenario

- Monte Carlo simulation allows investors to determine range of possible outcomes, and likelihood

Scenario Planning

- Maps a few discrete cases, ie best, base, worst cases for net present value

Certainty Equivalents

- Converts a risky cash flow, into a guaranteed amount the investor will be happy with

o Ie a project may have an E(r ) = $100 however as it is risky, the investor would be satisfied with just $80

Estimations for Cost of Capital

Accrual

- Transaction recognised when good or service is rendered, not when cash is received

Going Concern

- Company will continue operating into the foreseeable future

o If company isn’t expected to survive for 12 months, will be issued with going concern warning

- Assets can be depreciated over its useful life

o If your business is going to close in 3 months, then spreading out depreciation over 3 years is not adequate

Prudence

- Managers should give a fair picture of companies’ finance

- Should account for likely losses, debt, or payout early

- Don’t recognise uncertain gains

o One example is if the company is suing another company

Matching Concept

- Looks at relationship between expenses and revenue

o Links what expenses caused the revenue, for example moving from inventory to cost of goods sold

o Expenses should be recorded in the same period as the expenses that helped generate them

o Links with accrual accounting

Dual Aspect Account

- Every transaction will have two effects on the accounting equation, ensuring it always balances

Materiality

- An item is material if its omission could influence the decision taken by users of a financial statement

o Ie, a company doesn’t disclose a multimillion ongoing lawsuit, this is a liability that hasn’t been recorded

Cash Flow Statement

Operation Activities

· Net Income

· Adjustments (from depreciation and amortisation)

· Changes in working capital (AR and AP)

Investing Activities

· Capital Expenditure (ie buying PPE, will cause to be negative)

· Proceeds from investments and capital gains

Financing Activities

· Debt issuance (repaying and debt servicing)

· Equity raising (dividends and buybacks)

Income Statement

Revenue

Cost of Goods Sold

=Gross Profit

Distribution Cost

Administrative Expenses

Other operating expenses

=Operating Profit

Finance Income

-Finance costs

=Profit before Tax

-Tax expense

=Yearly Profit

Balance Sheet

Assets

Current Assets

Inventory

Trade Receivable

Cash

=Total Current Assets

Non Current Assets

Property Plants and Equipment

Intangibles

=Total Non Current Assets

=Total Assets

Depreciation

Contra Accounts

- Opposite balance to the normal asset account, ie decreases the book value of assets

- Each asset has its own account, and represents the total depreciation of the asset

Book Value = Initial Asset Cost - Depreciation

- Contra accounts used to show initial value of assets, and improves transparency in financial reporting

Vertical Analysis

- Expresses a component of the financial statement over another component (base figure).

Horizontal Analysis

- Comparing financial performance to the base year, over a period of time

Du Pont Analysis

Breaks down the drivers of return on equity

ROE = (Profit Margin)(Asset Turnover)(Leverage)

(Net Profit)/Equity = (Net Profit / Sales Revenue)*(Sales Revenue / Assets)*(Assets / Shareholder Equity)

Operating Profit Margin

(Profit Before Tax and Interest)/(Revenue)

(Revenue - COGS - Operating)/(Revenue)

Gross Profit Margin

(Revenue - COGS)/(Revenue)

Return on Equity

Net Profit / Equity

Return on Assets

(Net Profit)/(Total Assets)

Asset Utilisation Ratio

Revenue/(Total Assets)

Return on Capital Employed

EBIT/(Capital Employed)

(Revenue - COGS - Operating)/(Assets - Current Liabilities)

Receipts Cost Ratio

Measures present value of cash received, over cash being spent

(PV of Receipts)/(PV of Costs)

Current Ratio

(Current Assets)/(Current Liabilities)

Quick Ratio

(Cash + AR + Short Term Investments)/(Current Liabilities)

Cash Ratio

(Cash + Cash Equivalent)/(Current Liabilities)

Leverage Ratio

(Total Assets) / (Shareholder Equity)