PortM P7.4: Trade Cost Measurement

1/3

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

4 Terms

Example: Implementation shortfall

A portfolio manager decides to buy 50,000 shares of stock SJB at 9:00 am when the stock price is $20.00 (this is the decision price for the trade) and submits instructions to the firm's trader. The trader uses a limit price of $20.50 and in total manages to purchase 40,000 shares at an average price of $20.34. The fund is charged a commission of $0.02 per share, and there are no other fees. At the end of the day, SJB closes at $20.55.

Calculate (in basis points) the total IS for this trade.

Answer:

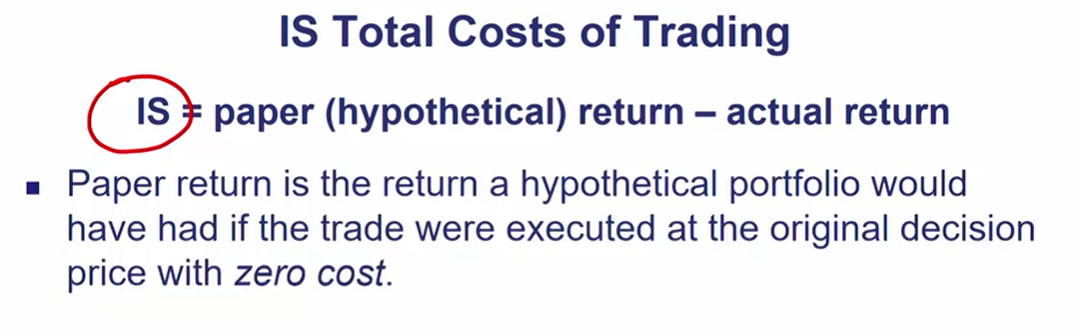

The paper portfolio is hypothetically assumed to fill the full order at the original decision price ($20.00). Hence, the paper return = 50,000 × ($20.55 − $20.00) = $27,500.

The actual return of the portfolio reflects that the trader purchased 40,000 shares at $20.34, and paid 40,000 × $0.02 = $800 for the execution.

Hence, the actual return = 40,000 × ($20.55 − $20.34) − $800 = $7,600.

Therefore, in absolute value terms, IS = $27,500 − $7,600 = $19,900.

The initial cost of the paper portfolio is 50,000 × $20 = $1,000,000, so IS in basis points is calculated as $19,900 / $1,000,000 = 0.0199, or 199 basis points.

Implementation shortfall (IS) =

Components of IS

x

x