Micro/Maco 1: Basic Economic Concepts

1/47

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

48 Terms

Economics

The study of how people, firms, and societies use their scarce productive resources to best satisfy their unlimited material wants.

Resources

Called factors of production, these are commonly grouped into the four categories of labor, physical capital, land or natural resources, and entrepreneurial ability.

Scarcity

The imbalance between limited productive resources and unlimited human wants. Because economic resources are scarce, the goods and services a society can produce are also scarce.

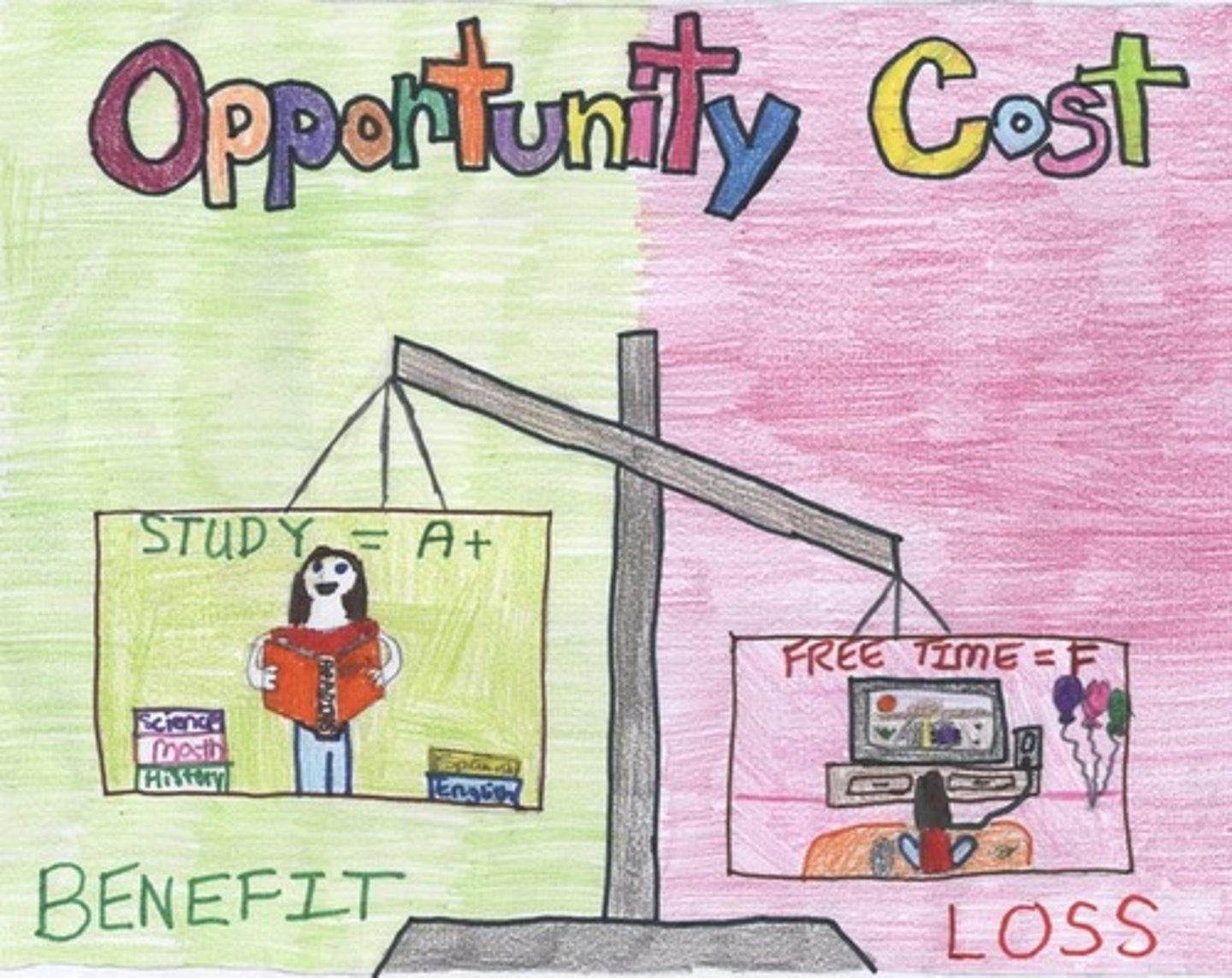

Trade-offs

Scarce resources imply that individuals, firms, and governments are constantly faced with difficult choices that involve benefits and costs.

Opportunity cost

The value of the sacrifice made to pursue a course of action.

cost-benefit analysis

the process of weighing all of the costs of an action against all of the benefits of that action.

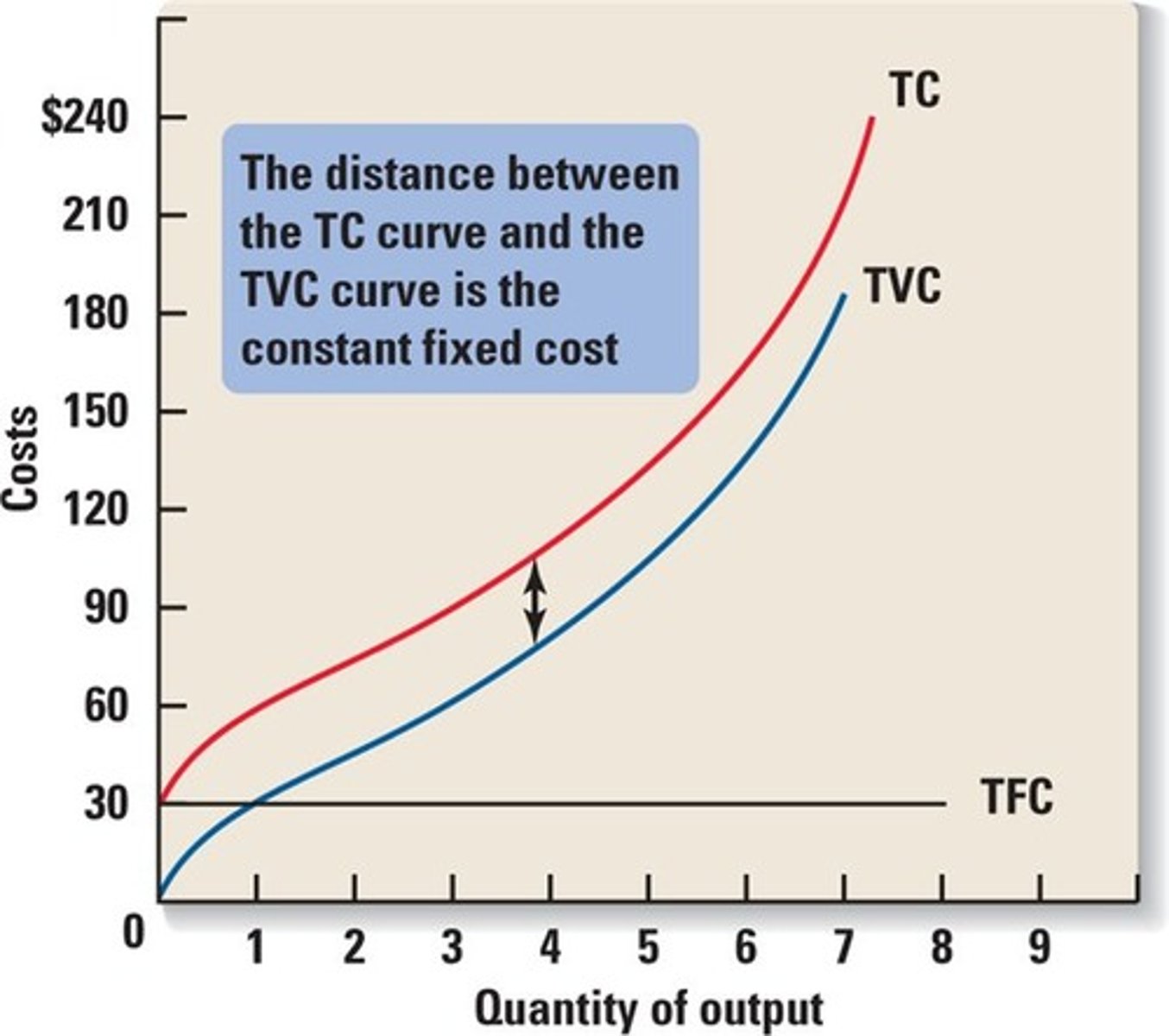

Total cost

the sum of the explicit and implicit costs of an action, or decision, being considered.

Explicit cost

the out-of-pocket costs of an action being considered.

Implicit cost

the cost of an action being considered, measured by the value of the next best forgone alternative.

Total benefit

the sum of all expected enjoyment, as measured by willingness to pay, of an action being considered.

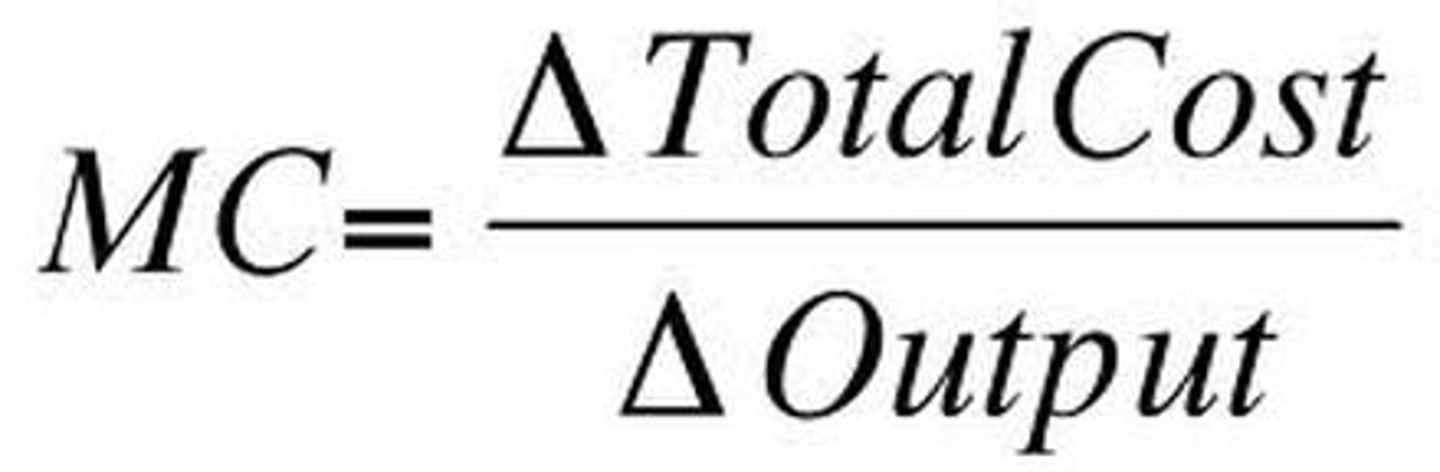

Marginal

The next unit or increment of an action.

marginal social benefit

The additional benefit that society receives from the consumption of the next unit of a good or service.

marginal social cost

The additional cost that society incurs from the production of the next unit of a good or service.

marginal analysis

Making decisions based upon weighing the marginal benefits and costs of that action. The rational decision maker chooses an action if the MB ≥ MC.

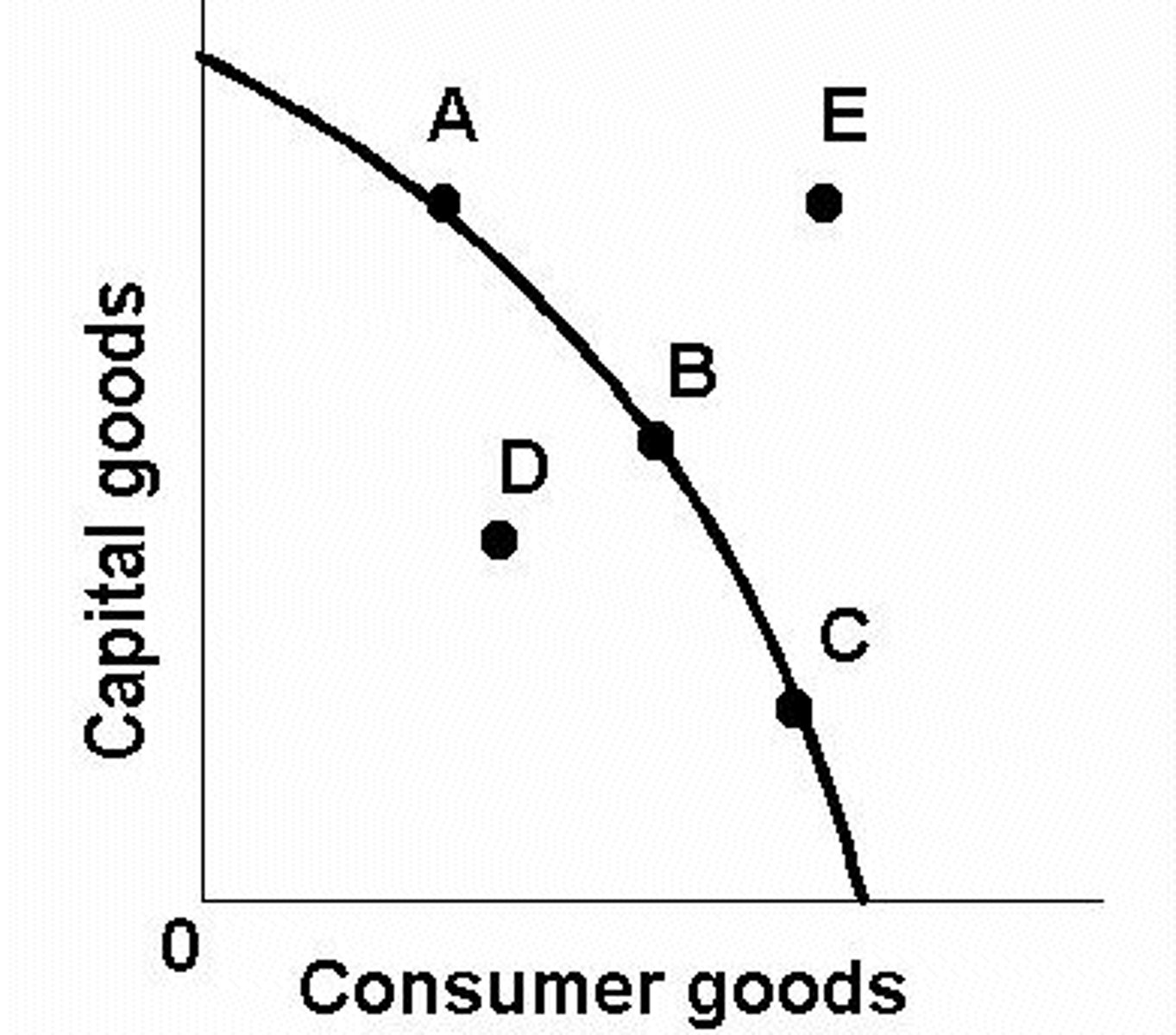

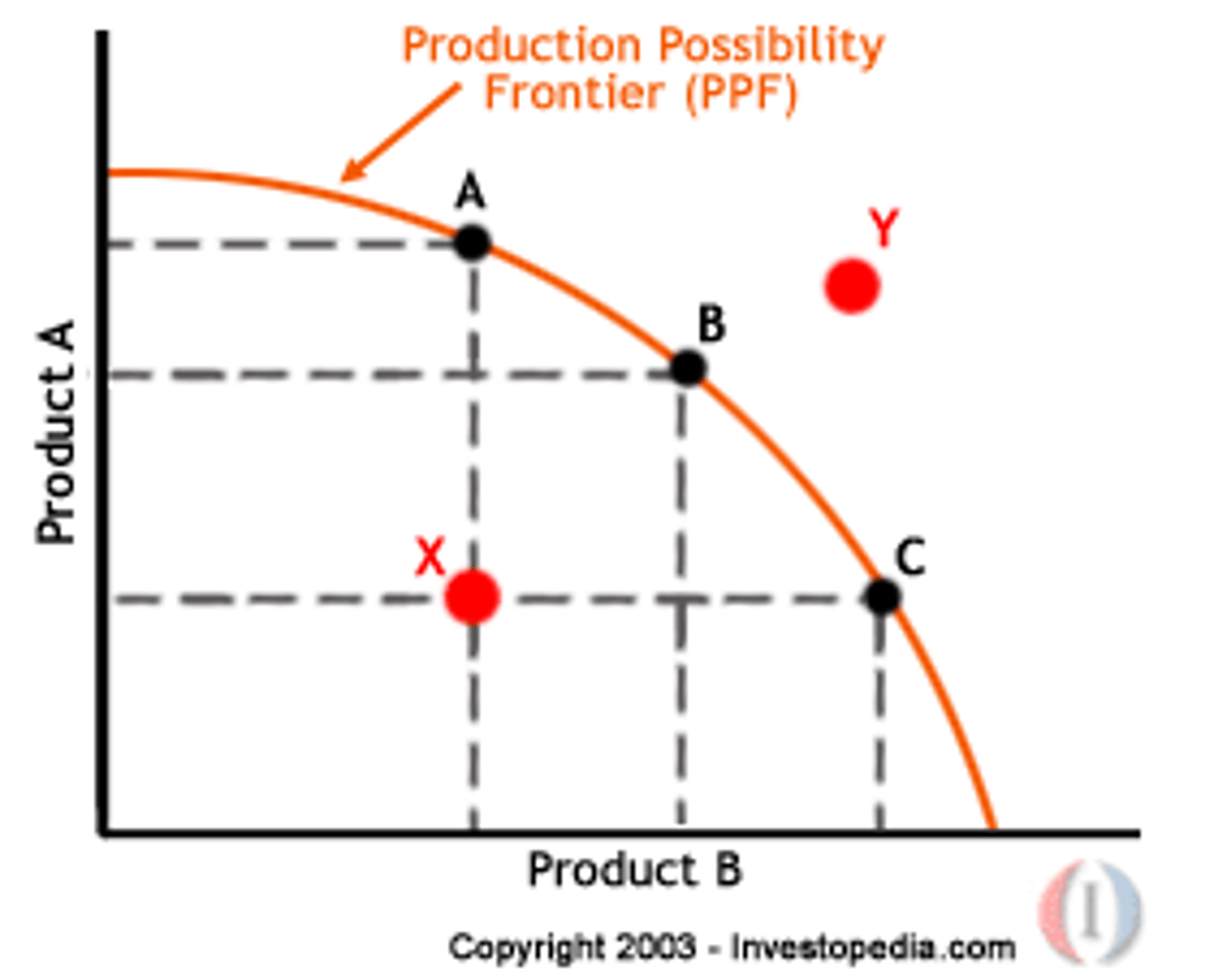

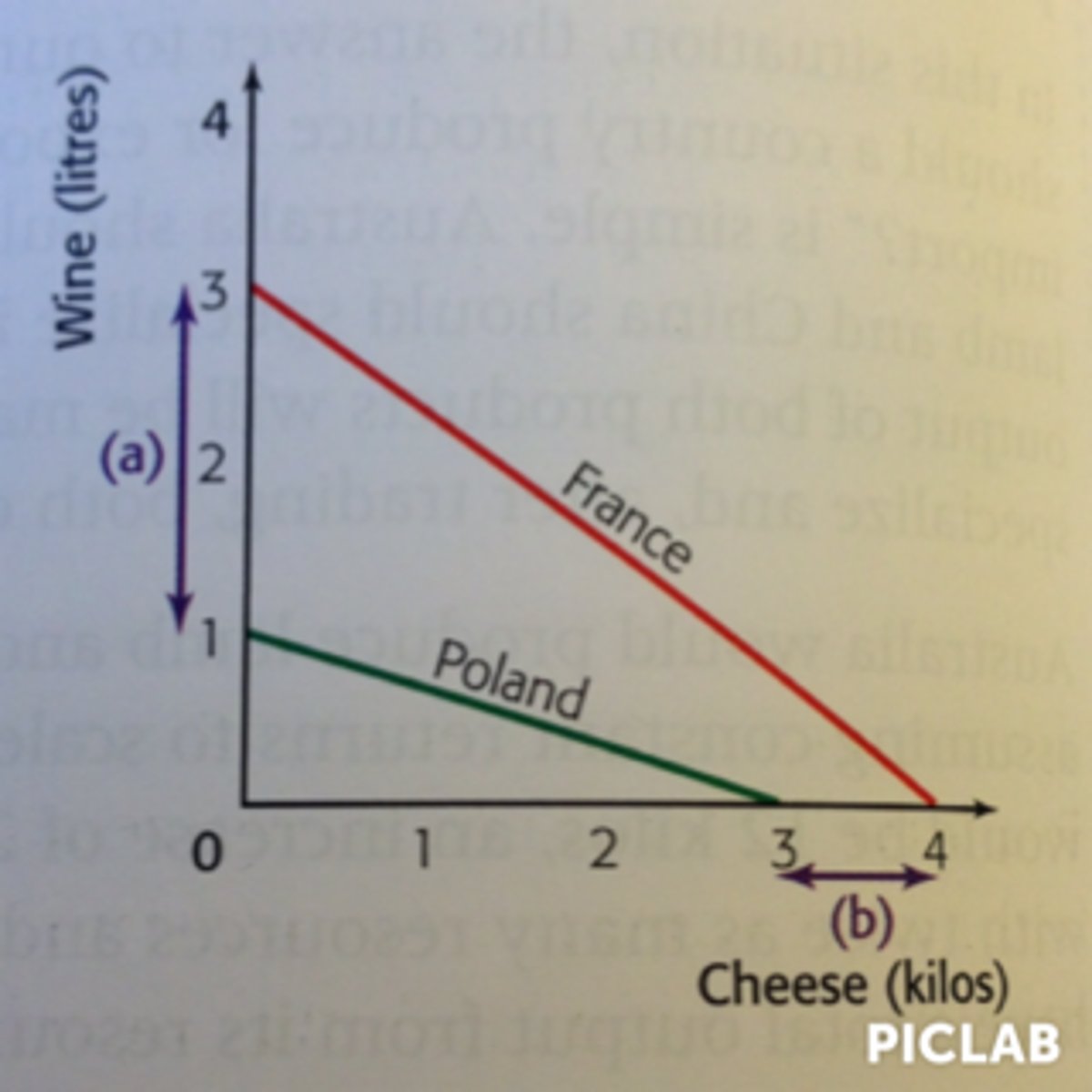

Production possibilities

Different quantities of goods that an economy can produce with a given amount of scarce resources. Graphically, the trade-off between the production of two goods is portrayed as a production possibility curve or frontier (PPC or PPF).

Production possibility curve or frontier

A graphical illustration that shows the maximum quantity of one good that can be produced, given the quantity of the other good being produced.

Law of increasing costs

The more of a good that is produced, the greater the opportunity cost of producing the next unit of that good.

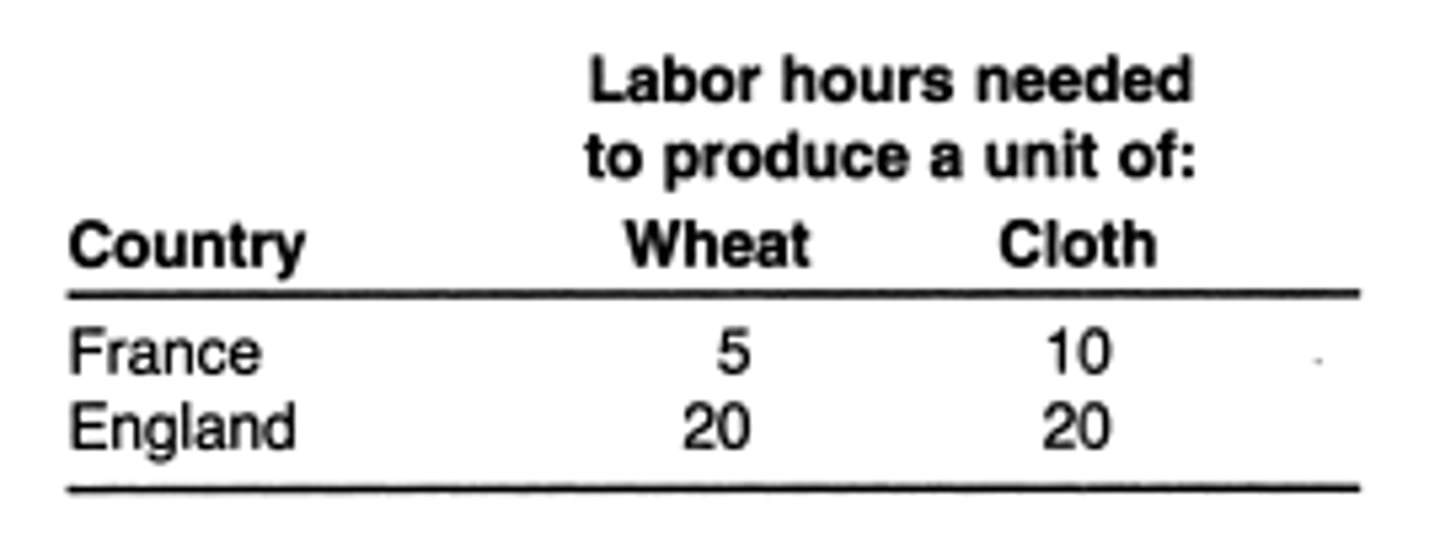

absolute advantage

This exists if a producer can produce more of a good with the same quantity of resources, or the same quantity of goods with fewer resources, than all other producers.

comparative advantage

A producer has comparative advantage if he can produce a good at lower opportunity cost than all other producers.

Specialization

When firms focus their resources on production of goods for which they have comparative advantage, they are said to be specializing.

Productive efficiency

Production of maximum output for a given level of technology and resources. All points on the PPF are productively efficient.

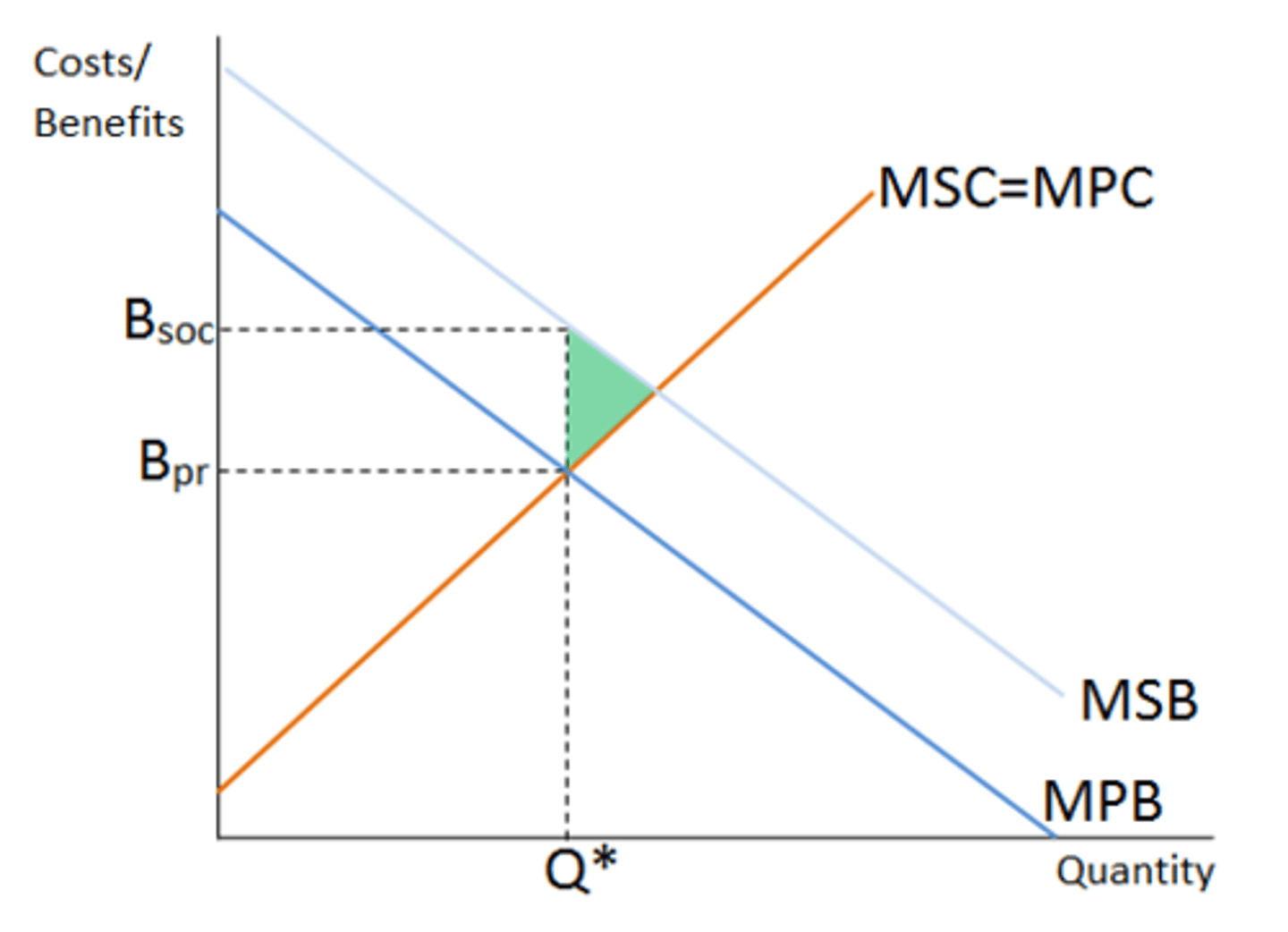

market failure

A market outcome for which the quantity produced is not allocatively efficient (MSB ≠ MSC) and either too many or too few units are produced.

allocative efficiency

Production of the combination of goods and services that provides the most net benefit to society. The optimal quantity of a good is achieved when the MSB = MSC of the next unit. This only occurs at one point on the PPF.

economic growth

This occurs when an economy's production possibilities increase. It can be a result of more resources, better resources, or improvements in technology.

Market economy (capitalism)

An economic system based upon the fundamentals of private property, freedom, self-interest, and prices.

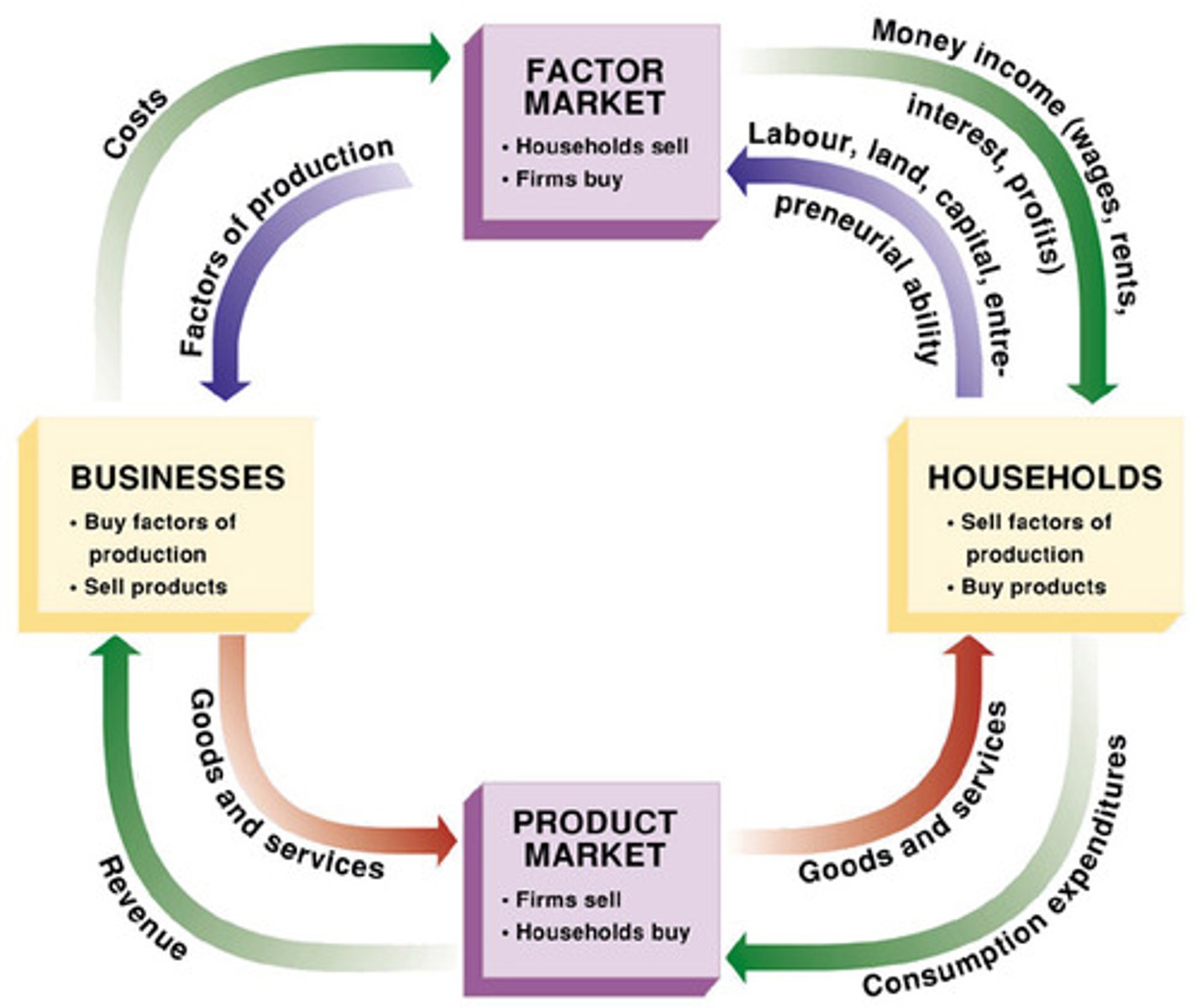

Circular-Flow Diagram

a visual model of the economy that shows how dollars flow through markets among households and firms

command economy

an economy in which production, investment, prices, and incomes are determined centrally by a government.

division of labor

the type of arrangement in which each worker specializes in a particular task or job

Economices of scale

reductions in minimum average cost that come through increase in size or scale of plant and equipment

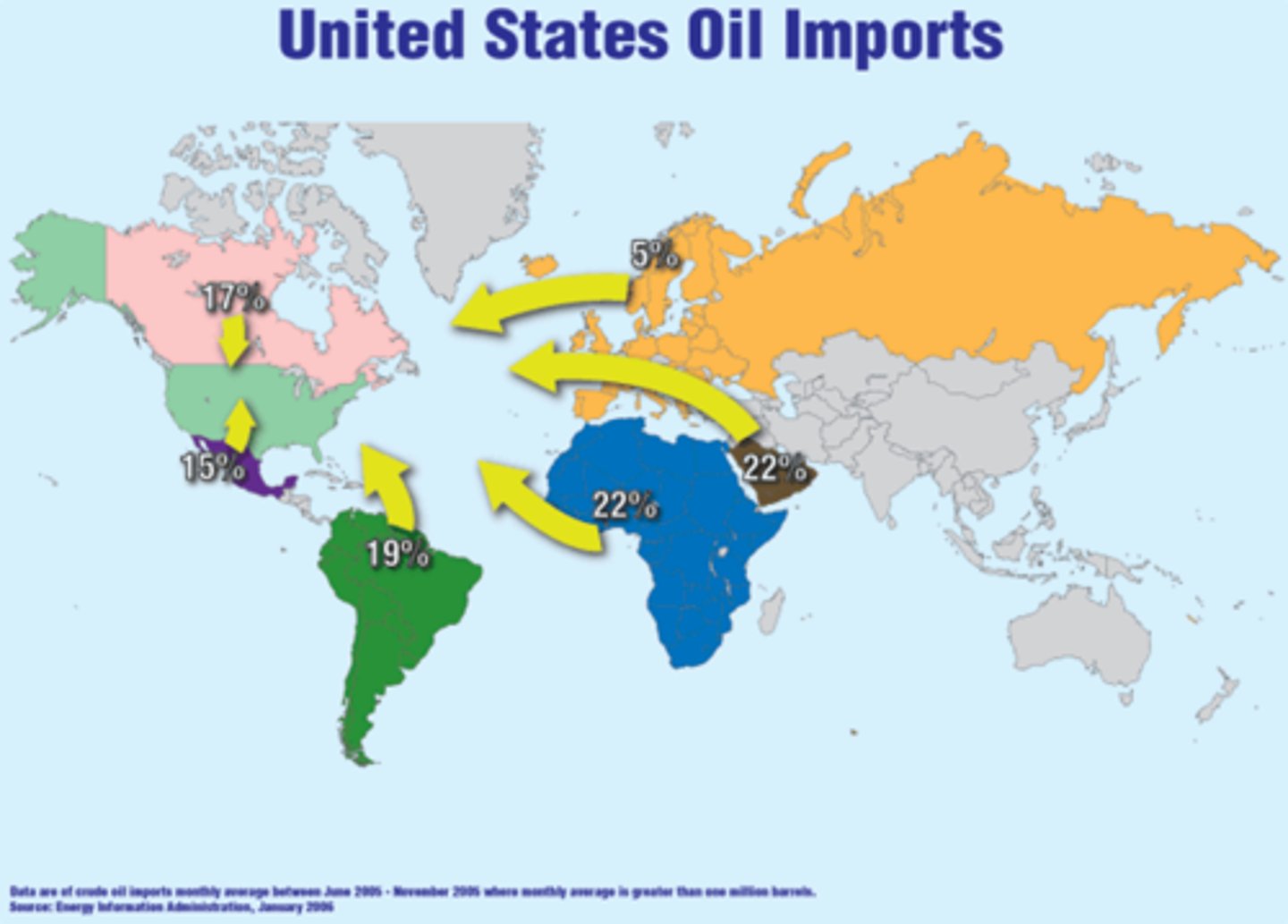

Exports

goods produced domestically and sold abroad

fiscal policy

the use of government spending and revenue collection to influence the economy

Globalization

the process by which businesses or other organizations develop international influence or start operating on an international scale.

goods and services

the objects that people value and produce to satisfy human wants

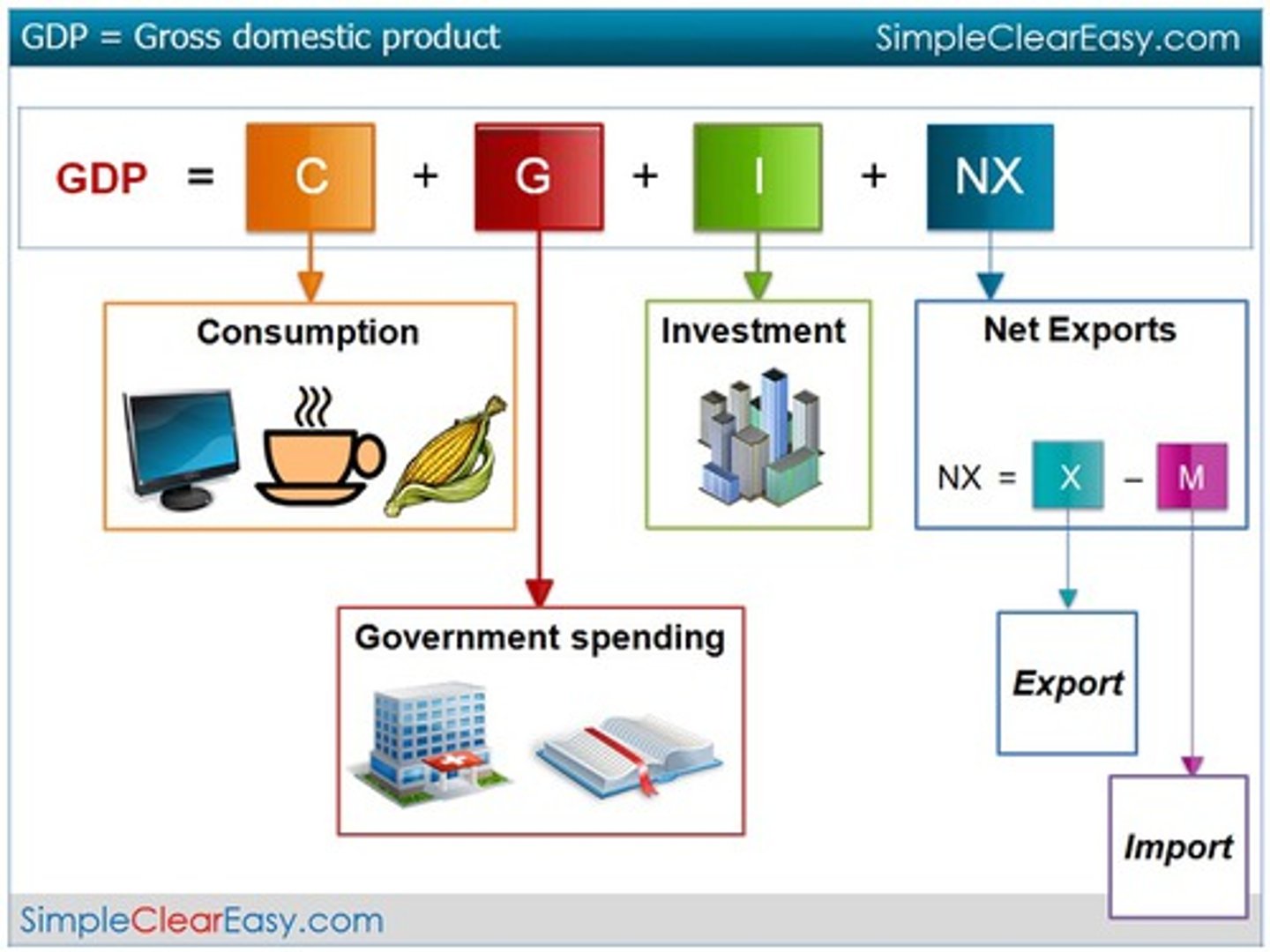

Gross Domestic Product (GDP)

A measurement of the total goods and services produced within a country.

import

bring (goods or services) into a country from abroad for sale.

labor market

the market in which households sell their labor as workers to business firms or other employers

market

a group of buyers and sellers of a particular good or service

market economy

Economic decisions are made by individuals or the open market.

monetary policy

Government policy that attempts to manage the economy by controlling the money supply and thus interest rates.

private enterprise

business ownership by ordinary people, not the government

Traditional Economy

An economy in which production is based on customs and traditions and economic roles are typically passed down from one generation to the next.

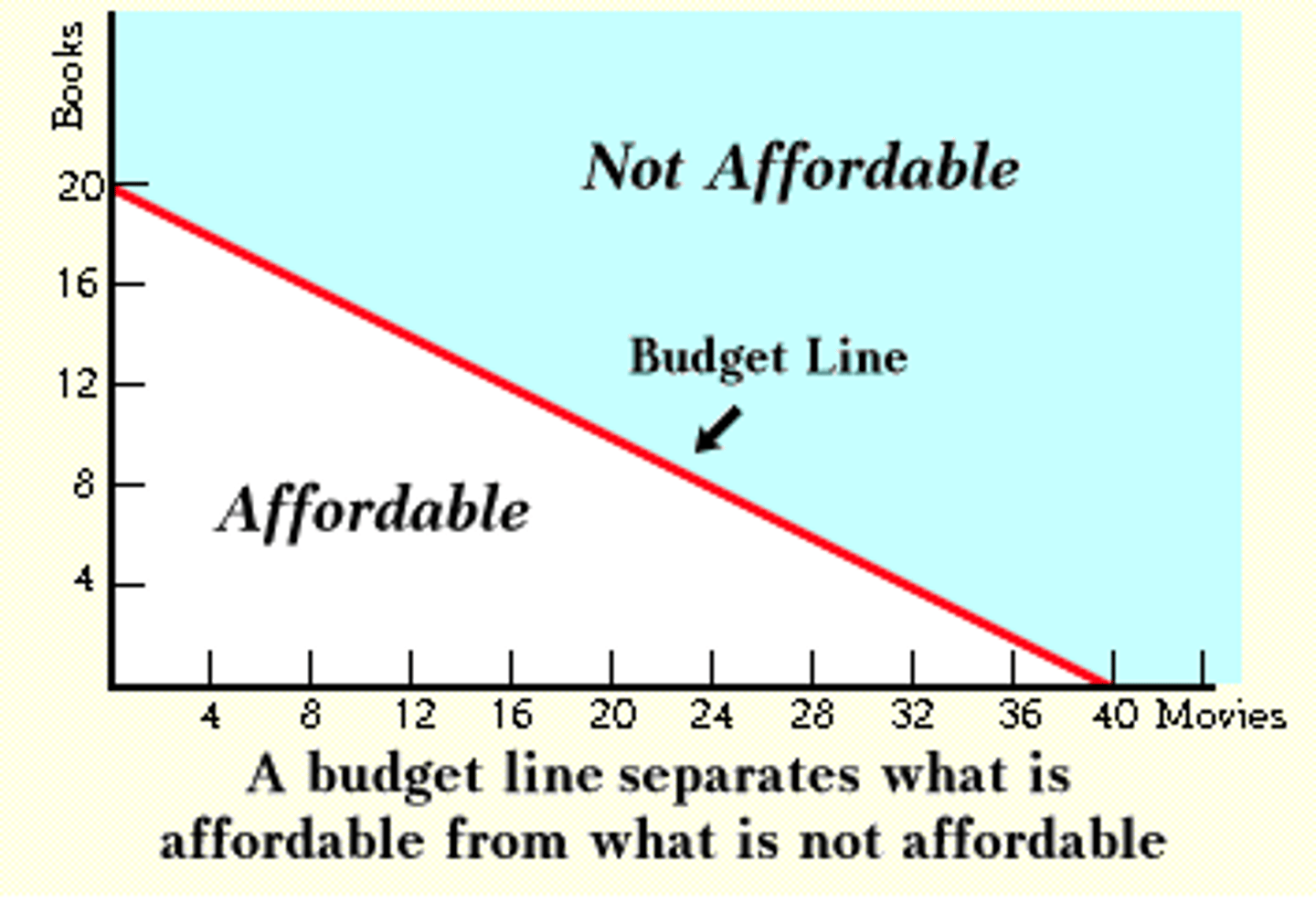

budget constraint

the limited amount of income available to consumers to spend on goods and services

invisible hand

term economists use to describe the self-regulating nature of the marketplace

normative statement

statement which describes how the world should be (opinion)

positive statement

statement which describes the world as it is (can be tested)

productive efficiency

a situation in which a good or service is produced at the lowest possible cost

sunk cost

a cost that has already been committed and cannot be recovered

Utility

Ability or capacity of a good or service to be useful and give satisfaction to someone.