chap 18

1/41

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

42 Terms

shareholders equity

residual amount- whats left over after liabilities have been subtracted from assets (net assets)

ownership interests of shareholders arise primarily from

paid in capital

retained earnings

paid in capital

amounts invested by shareholders in the corporation

purchase shares of stock from corporation

company buying back some of those shares or from share based compensation activities

retained earnings

amounts earned by the corporation on behalf of its shareholders

4 classifications within shareholders equity

paid in capital

retained earnings

accumulated other comprehensive income

treasury stock

comprehensive income

total nonowner changes in equity for a reporting period

not including transactions with owners (dividends, issuance or purchase of the company’s stock)

accumulated other comprehensive income

sum of all oci that has been reported in current and prior periods

reported in the statement of shareholders equity

oci types of gains and losses (not reported in income statement)

net holding gains (losses) on afs investments in debt securities

gains (losses) from and amendments to pensions and other postretirement benefit plans

deferred gains (losses) on derivatives

adjustments from foreign currency translation

oci vs aoci

oci- component of comprehensive income created during the reporting period

aoci- comprehensive income accumulated over the current and prior reporting periods

company organization

sole proprietorship

partnership

corporation

ownership rights held by common shareholders unless specifically withheld by agreement

right to vote

right to share in profits when dividends are declared

right to share in the distribution of assets if company is liquidated

preferred stock ownership rights

typically has preference to a specified amount of dividends ($ amt or %)

preference (over common) as to distribution of assets if company is dissolved

other rights and privileges that may be granted to preferred shareholders

right of conversion

redemption privilege

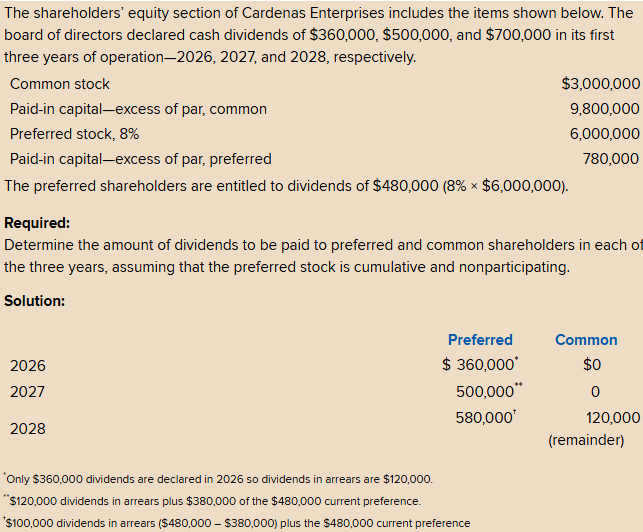

cumulative vs noncumulative

participating vs nonparticipating

right of conversion

exchange shares of preferred stock for common stock at a specified conversion ration

redemption privilege

option, under specified conditions, to return their shares for a predetermined redemption price or callable

cumulative vs noncumulative

cumulative- dividends in arrears must be made up in later year before any dividends are paid on common shares

participating vs nonparticipating

participating-allows preferred shareholders to receive additional dividends beyond the stated amount

par value shares issued for cash

no par shares issued for cash

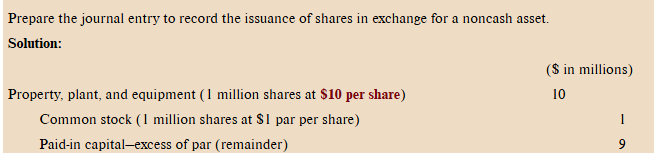

shares issued for noncash consideration

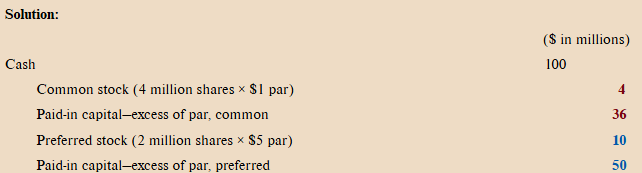

more than one security issued for a single price

share issue cost

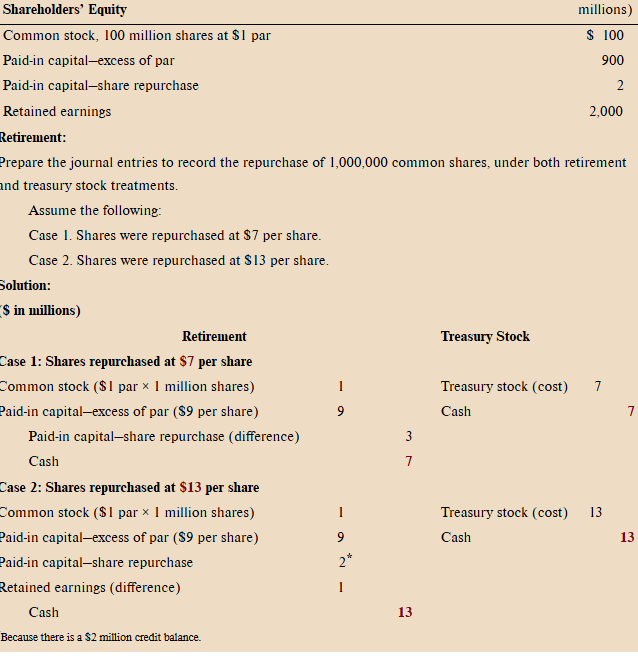

retired stock

shares repurchased and not designated as treasury stock

treasury stock

shares of a company’s own stock repurchased and not retired (no voting rights, no cash dividends)

some shares previously sold to shareholders were bought back by the corporation and are being held for resale

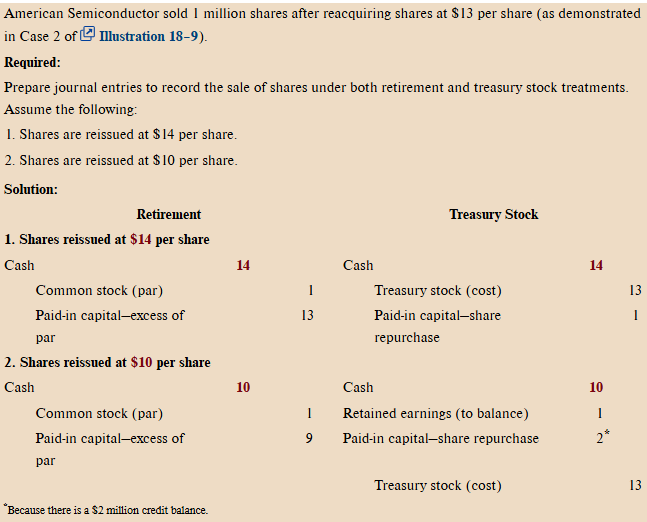

retirement vs treasury share buybacks

retired vs treasury resale of shares

debit vs credit in retained earnings

debit- deficit

credit-$ amt of assets previously earned by the firm but not distributed as dividends to shareholders

dividends

distribution of assets the company has generated on behalf of its shareholders

liquidating dividend

when a dividend exceeds the balance in retained earnings and returns invested capital to owners (might occur when firm liquidating)

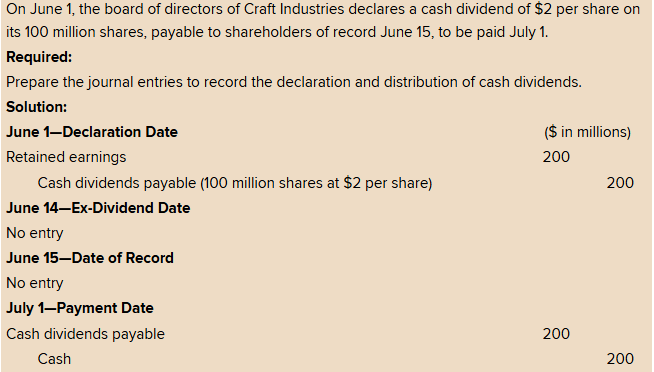

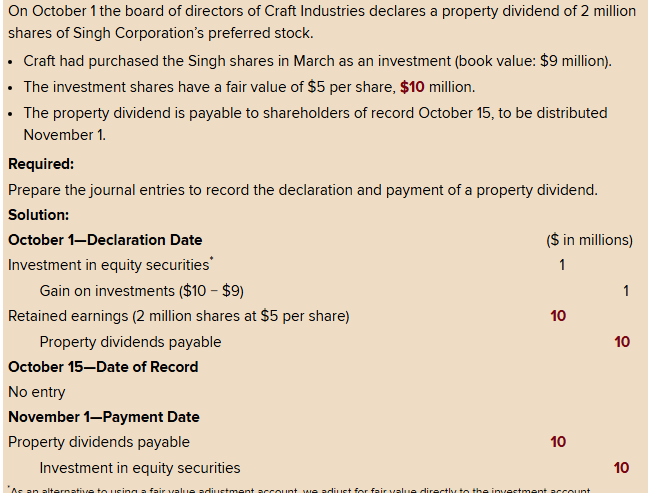

date of record (dividends)

specific date that the company determines which stockholders will receive the dividend

ex-dividend date

to be registers owner of shares on the date of record, an investor must purchase the shares before the ex-dividend date.Usually one business day before the date of record

cash dividends journal entry

distribution of dividends to preferred shareholders

property dividend

noncash asset is distributed (often called a dividend in kind or nonreciprocal transfer to owners)

property dividends journal entry

stock dividend

distribution of additional shares of stock to current shareholders of the corporation

effects neither assets or the liabilities of the firm

declare stock dividend

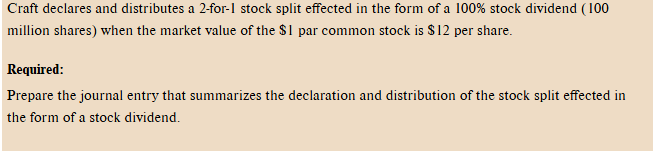

stock split

stock distribution of 25% or higher and also known as a “large” stock dividend

stock split journal entry

no journal entry

stock split effected in the form of a stock dividend

reverse stock split

occurs when a company decreases, rather than increases, its outstanding shares

fractional shares

“cash in lieu of payments